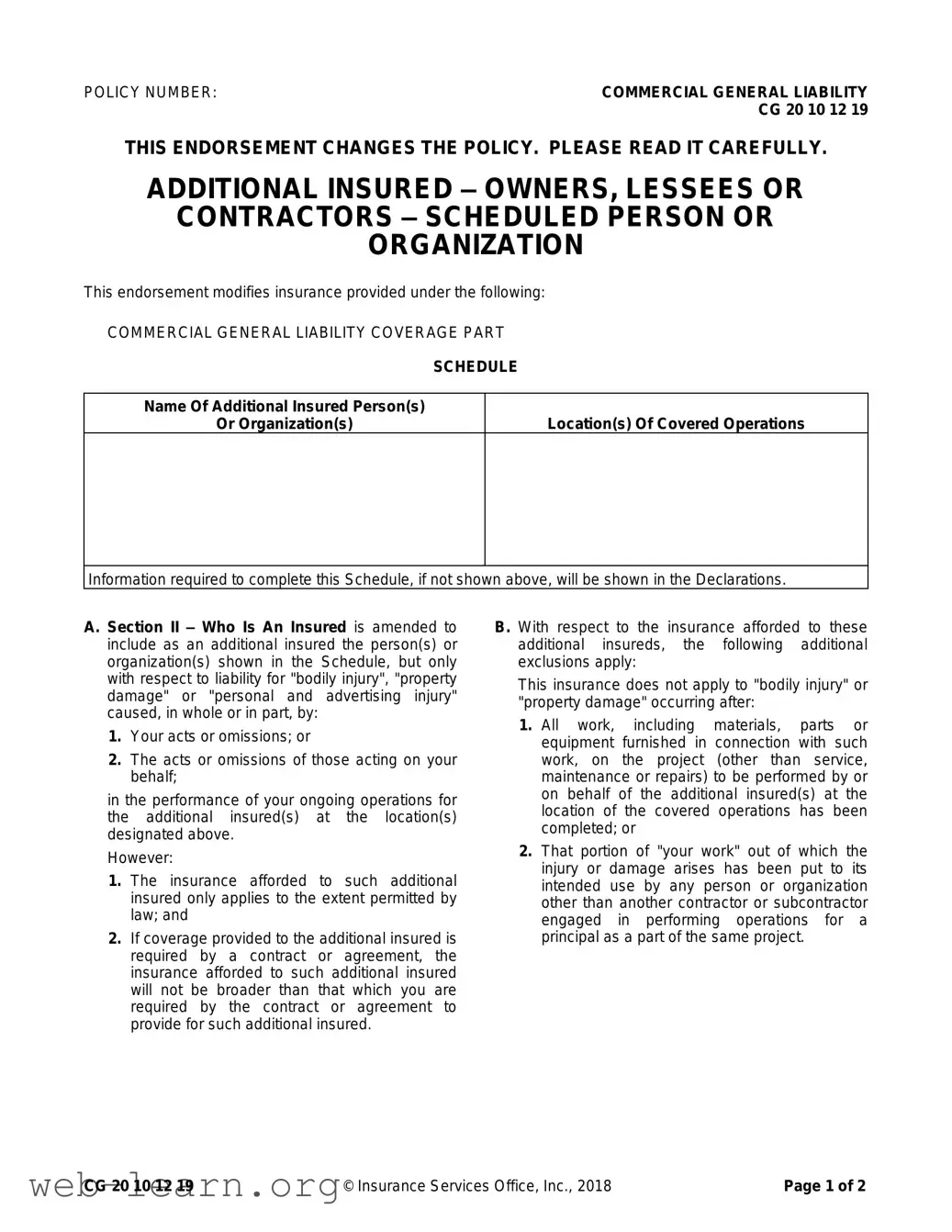

The CG 20 10 07 04 Liability Endorsement form is a critical document designed for businesses and individuals seeking to extend their insurance coverage. Specifically targeted at Commercial General Liability policies, this endorsement allows for the inclusion of additional insured parties, which can often be owners, lessees, or contractors related to a specific project. The endorsement specifies the conditions under which these additional insured individuals or organizations are protected, particularly regarding liability for bodily injury, property damage, or personal and advertising injury. It is essential to note that the coverage applies only in relation to the insured's actions or omissions, as well as those of individuals working on their behalf, while engaged in ongoing operations for the additional insured at designated locations. The document also outlines critical exclusions, particularly emphasizing that coverage will not extend beyond the completion of specified work or after the final use of the materials involved. This careful delineation of coverage limits ensures that businesses involved in contractual agreements understand their responsibilities and the boundaries of their protection. Moreover, it is important for policyholders to recognize that any insurance limits for additional insureds are capped at the lesser of the amounts outlined in the contracts or the available limits under the policy. Ultimately, awareness and comprehension of the CG 20 10 07 04 endorsement details can significantly influence risk management strategies and liability planning for various stakeholders in contractual relationships.

| Fact Name | Description |

|---|---|

| Policy Number | CG 20 10 12 19 is the designated policy number for this endorsement. |

| Coverage Type | This endorsement modifies coverage provided under the Commercial General Liability Coverage Part. |

| Purpose | It serves to add additional insureds, such as owners, lessees, or contractors, as specified in the schedule. |

| Condition of Coverage | Coverage applies for liability related to "bodily injury", "property damage", or "personal and advertising injury" caused by the insured's operations. |

| Extents of Coverage | The coverage for additional insureds is limited to what is required by an agreement or contract. |

| Limitations | The insurance does not cover injury or damage occurring after completion of the work at the designated location. |

| Contractual Requirement | The endorsement notes that coverage cannot exceed what is required by the contract with the additional insured. |

| Exclusions | It specifically excludes coverage for completed operations and intended use by other parties. |

| Limits of Insurance | The maximum payout to the additional insured is either the contract-required amount or the policy limit, whichever is lower. |

| Governing Laws | Varies by state. Generally governed by state regulations on liability insurance. |

Filling out the CG 20 10 07 04 Liability Endorsement form is essential for ensuring that all necessary parties are adequately protected under your insurance policy. Carefully following the steps below will help streamline the process and ensure nothing is overlooked.

After you complete the form, be sure to review it for accuracy. Keep a copy for your own records and submit it according to the requirements of your insurance provider.

What is the CG 20 10 07 04 Liability Endorsement form?

The CG 20 10 07 04 Liability Endorsement form is a modification to the Commercial General Liability (CGL) policy. This endorsement adds additional insured coverage for specific persons or organizations as outlined in the endorsement schedule. It aims to extend insurance protection for certain liabilities that may arise from the insured's operations.

Who is considered an additional insured?

An additional insured is the person or organization specifically listed in the endorsement schedule. They are covered for liability related to bodily injury, property damage, or personal and advertising injury that results from the acts or omissions of the insured or their representatives during ongoing operations.

What types of operations are covered under this endorsement?

The endorsement covers operations happening at designated locations that the additional insureds are involved in. This includes ongoing work performed by the insured on behalf of the additional insured, as long as it is related to the operations specified in the endorsement.

Are there limits to the coverage provided to additional insureds?

Yes, the endorsement stipulates that the coverage for additional insureds will not exceed the limits required by any contracts or agreements. It will be capped at either the contractually required amount or the maximum available limit of insurance, depending on which is lower.

What exclusions apply to the additional insured coverage?

There are specific exclusions to note. Coverage under this endorsement does not apply if bodily injury or property damage occurs after all project work has been completed, or if the work performed has been put to its intended use by someone other than a contractor or subcontractor working on the same project. This helps to clarify when coverage ceases.

Is the coverage provided broader than what is imposed by contracts?

No, if additional insured coverage is required by a contract or agreement, it will not be broader than what is specifically mandated within that contract. This is important to ensure compliance with any existing agreements.

How should the endorsement be used?

To use the endorsement effectively, names and locations of additional insureds should be clearly listed in the endorsement schedule. It’s critical to understand the limits and exclusions related to the coverage to avoid misunderstandings later on.

Does this endorsement increase the overall limits of the insurance policy?

No, the endorsement does not increase the existing limits of the commercial general liability policy. It simply extends coverage to additional insureds without raising the maximum amount available under the policy.

What happens if there is a conflict between the endorsement and the primary policy?

If there’s a conflict, the primary CGL policy will take precedence unless the endorsement specifically modifies its terms. Always review both documents to understand how they work together.

How can I ensure compliance with this endorsement?

It's advisable to communicate clearly with all parties involved in a contract regarding insurance requirements. Keeping accurate records and ensuring that all necessary parties are properly listed in the endorsement will help maintain compliance and protect against liability issues.

Filling out the CG 20 10 07 04 Liability Endorsement form requires attention to detail. One common mistake is failing to correctly input the policy number. It's crucial to ensure that the policy number matches exactly what is in your original policy documentation. An incorrect number could lead to issues with coverage that might not get resolved until it’s too late.

Another frequent error is leaving the name of the additional insured section blank or not specifying the correct person or organization. This could result in serious implications, especially if you need to make a claim. The additional insured must be properly identified to ensure they are covered under the policy.

People often neglect to include the locations of covered operations. Failing to specify where coverage applies can lead to misunderstandings and disputes about where the insurance is valid. Always double-check that you have listed all relevant locations to avoid complications later on.

Inadequate explanation of the scope of coverage for the additional insured is another mistake. Some individuals mistakenly assume the endorsement covers everything. However, it's vital to understand that coverage is limited to what is stipulated in the endorsement and any relevant contracts.

Misunderstanding the exclusions can have serious repercussions. Many overlook sections regarding exclusions that detail when the additional insured is not covered. Ensure that you read these sections clearly—this knowledge is essential to avoid unwanted exposures in your coverage.

Another pitfall is misinterpreting the limits of insurance. Some people think that just because they have an endorsement, the limits automatically increase. However, the endorsement states that limits will not exceed those required by the contract or available under the policy. Clarity here is essential for accurate financial planning.

Inconsistent information can also cause headaches. If different sections of the form contain conflicting information, it can create confusion. Be meticulous about consistency throughout the form to eliminate potential disputes down the line.

Finally, not reviewing the form before submission is a major misstep. Taking a moment to verify all the entries can prevent many common mistakes and ensure that the coverage is as intended. An extra set of eyes can catch issues that may otherwise be overlooked, so take the time to double-check the details before sending it off.

When dealing with the CG 20 10 07 04 Liability Endorsement form, several other documents may accompany it. Each serves a specific purpose and helps ensure comprehensive coverage for individuals and organizations involved in a contract or project. Understanding these forms can help facilitate better communication and clarify responsibilities.

Understanding these documents can help navigate the complex landscape of liability and insurance requirements. They work together to ensure all parties involved are adequately protected and informed about their coverage and obligations.

When filling out the CG 20 10 07 04 Liability Endorsement form, it is essential to follow certain guidelines to ensure accuracy and compliance. Below is a list of things you should and shouldn't do.

Adhering to these guidelines will help mitigate risks and ensure that the endorsement form meets all necessary requirements.

Here are some important points to keep in mind when filling out and using the CG 20 10 07 04 Liability Endorsement form:

Take the time to fill out this form accurately. It can protect both you and the additional insureds from potential liabilities.

Wv Sales and Use Tax Form - Ensure the reverse side of the certificate is completed for validity.

Yes No Maybe List for Couples - Massage can foster intimacy and relaxation, enhancing the overall experience.

California Asset Disclosure Form - Any additional income received in the past three years must be disclosed, including its nature and value.