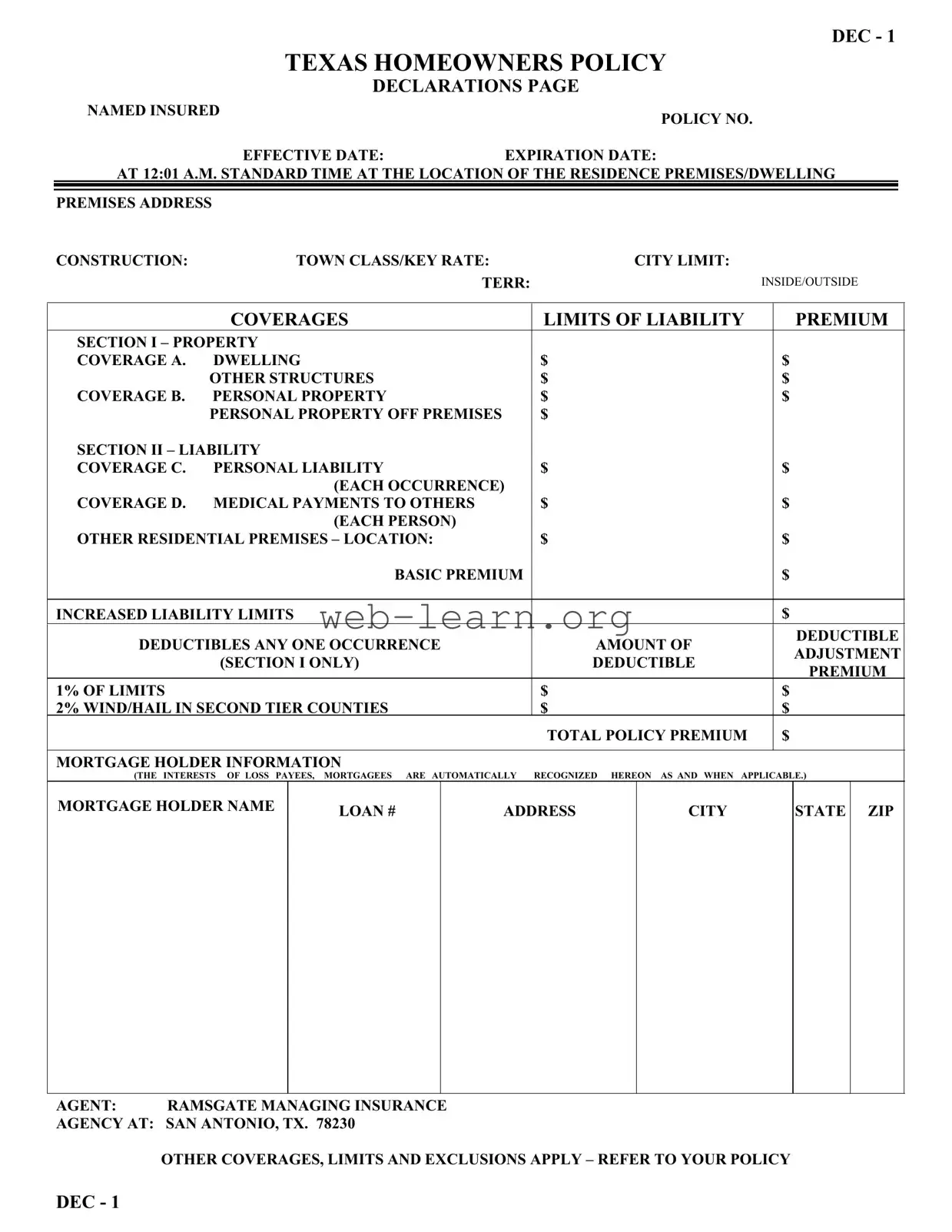

The Texas Dec 1 form serves as the cornerstone of homeowners insurance policies in Texas, encapsulating vital information that protects both property and personal interests. This document outlines essential details such as the named insured, policy number, and effective dates, ensuring that homeowners have a clear understanding of their coverage timeline. Within its structured layout, the form delineates various coverage sections, including property coverage for the dwelling and other structures, as well as personal property protection. It also highlights liability coverage, which safeguards against potential claims, and medical payments for others, adding an extra layer of security. Homeowners will find limits of liability and associated premiums clearly stated, along with information on deductibles, which can significantly impact out-of-pocket expenses during a claim. Additionally, the form accommodates mortgage holder information, recognizing their interests in the event of a loss. As homeowners navigate the complexities of insurance, the Texas Dec 1 form stands as a comprehensive guide, ensuring that they are well-informed about their coverage and responsibilities.

DEC - 1

TEXAS HOMEOWNERS POLICY

DECLARATIONS PAGE

NAMED INSURED |

|

POLICY NO. |

|

|

|

|

EFFECTIVE DATE: |

EXPIRATION DATE: |

AT 12:01 A.M. STANDARD TIME AT THE LOCATION OF THE RESIDENCE PREMISES/DWELLING |

||

|

|

|

|

|

|

PREMISES ADDRESS |

|

|

CONSTRUCTION: |

TOWN CLASS/KEY RATE: |

CITY LIMIT: |

TERR:INSIDE/OUTSIDE

COVERAGES

LIMITS OF LIABILITY

PREMIUM

SECTION I – PROPERTY |

|

|

|

|

||

COVERAGE A. |

DWELLING |

$ |

|

|

$ |

|

|

OTHER STRUCTURES |

$ |

|

|

$ |

|

COVERAGE B. |

PERSONAL PROPERTY |

$ |

|

|

$ |

|

|

PERSONAL PROPERTY OFF PREMISES |

$ |

|

|

|

|

SECTION II – LIABILITY |

|

|

|

|

||

COVERAGE C. |

PERSONAL LIABILITY |

$ |

|

|

$ |

|

|

(EACH OCCURRENCE) |

|

|

|

|

|

COVERAGE D. MEDICAL PAYMENTS TO OTHERS |

$ |

|

|

$ |

||

|

(EACH PERSON) |

|

|

|

|

|

OTHER RESIDENTIAL PREMISES – LOCATION: |

$ |

|

|

$ |

||

|

BASIC PREMIUM |

|

|

|

$ |

|

|

|

|

|

|

|

|

INCREASED LIABILITY LIMITS |

|

|

|

$ |

||

DEDUCTIBLES ANY ONE OCCURRENCE |

AMOUNT OF |

|

DEDUCTIBLE |

|||

|

ADJUSTMENT |

|||||

|

(SECTION I ONLY) |

DEDUCTIBLE |

|

|||

|

|

PREMIUM |

||||

|

|

|

|

|

|

|

1% OF LIMITS |

|

|

$ |

|

|

$ |

2% WIND/HAIL IN SECOND TIER COUNTIES |

$ |

|

|

$ |

||

|

|

|

TOTAL POLICY PREMIUM |

|

$ |

|

|

|

|

|

|

|

|

MORTGAGE HOLDER INFORMATION |

|

|

|

|

||

(THE INTERESTS OF LOSS PAYEES, MORTGAGEES ARE AUTOMATICALLY |

RECOGNIZED HEREON AS AND WHEN APPLICABLE.) |

|||||

|

|

|

|

|

|

|

MORTGAGE HOLDER NAME

LOAN #

ADDRESS

CITY

STATE ZIP

AGENT: RAMSGATE MANAGING INSURANCE

AGENCY AT: SAN ANTONIO, TX. 78230

OTHER COVERAGES, LIMITS AND EXCLUSIONS APPLY – REFER TO YOUR POLICY

DEC - 1

| Fact Name | Details |

|---|---|

| Form Purpose | The DEC - 1 Texas Homeowners Policy Declarations Page outlines the coverage details for homeowners insurance in Texas. |

| Effective Dates | The policy specifies an effective date and an expiration date, ensuring clarity on the coverage period. |

| Coverage Types | The form includes multiple coverage sections, such as property coverage, personal liability, and medical payments to others. |

| Limits of Liability | Each coverage section has defined limits of liability, which indicate the maximum amount the insurer will pay for a claim. |

| Governing Law | This form is governed by Texas insurance law, specifically the Texas Insurance Code, which regulates homeowners insurance policies. |

Completing the Texas Dec 1 form requires careful attention to detail. Ensure you have all necessary information ready before starting. This form is essential for establishing your homeowners policy, and accuracy is crucial for proper coverage.

After filling out the form, ensure that all sections are complete and accurate. Double-check for any errors or omissions. Once confirmed, submit the form as directed by your insurance agency to finalize your homeowners policy.

The Texas Dec 1 form is the declarations page for a Texas Homeowners Policy. It outlines the key details of your insurance coverage, including the named insured, policy number, effective dates, and coverage limits.

The form includes:

Coverage limits are listed next to each type of insurance. For example, under Section I – Property Coverage, you will see limits for the dwelling, other structures, and personal property. These limits indicate the maximum amount the insurance company will pay for claims related to those categories.

Deductibles are the amounts you agree to pay out-of-pocket before your insurance coverage kicks in. The form specifies different deductibles for various occurrences, such as a standard deductible and a higher deductible for wind or hail claims in certain counties.

The mortgage holder information section recognizes the interests of any mortgagees or loss payees. This means that if you have a mortgage on your property, the lender is automatically covered under the policy in case of a loss.

The total policy premium is the amount you will pay for your insurance coverage for the policy term. It includes the basic premium, any increased liability limits, and adjustments for deductibles.

The insurance agent listed on the Texas Dec 1 form is Ramsgate Managing Insurance Agency, located in San Antonio, Texas. They can assist you with questions about your policy and coverage options.

Yes, the form mentions that other coverages, limits, and exclusions apply. It is important to refer to your full policy document for detailed information about what is and isn’t covered.

You can obtain a copy of your Texas Dec 1 form from your insurance agent or directly from your insurance company. It is advisable to keep a copy for your records and review it regularly to ensure your coverage meets your needs.

Filling out the Texas Dec 1 form can be straightforward, but many people make common mistakes that can lead to delays or issues with their insurance coverage. One frequent error is not providing complete information in the named insured section. This area must include the full legal names of all insured parties. Omitting a name or misspelling it can cause complications when filing a claim.

Another mistake often made is failing to accurately report the policy number. The policy number is crucial for identifying your coverage. Double-checking this number ensures that your application is processed smoothly and that you receive the correct policy documents.

Many individuals also overlook the importance of specifying the effective and expiration dates of the policy. These dates determine the coverage period. If these are incorrect or missing, it can lead to gaps in coverage, leaving you vulnerable in case of an incident.

In the coverage limits section, people frequently miscalculate the limits of liability for both property and personal liability. Underestimating these limits can expose you to significant financial risk. Conversely, overestimating may result in higher premiums than necessary. It is essential to evaluate your needs accurately.

Another common oversight is neglecting to provide accurate mortgage holder information. This section is vital for ensuring that the mortgage lender is properly recognized in the event of a claim. Failure to include correct details can lead to complications regarding payments and claims.

Lastly, individuals often forget to review the deductibles they select. Choosing the wrong deductible can have financial implications. A higher deductible may lower your premium, but it also means you will pay more out-of-pocket in the event of a claim. Carefully consider your financial situation when making this choice.

The Texas Dec 1 form serves as a crucial document for homeowners, outlining the details of their insurance coverage. In addition to this form, there are several other documents that often accompany it, each playing a significant role in the overall insurance process. Below is a list of some commonly used forms and documents.

Understanding these documents can empower homeowners to navigate the complexities of their insurance policies more effectively. Each form contributes to a clearer picture of coverage, responsibilities, and protections available to policyholders in Texas.

The Texas Dec 1 form serves as a crucial document in the realm of homeowners insurance. It outlines important information regarding coverage, limits, and premiums. Several other documents share similarities with this form in terms of their purpose and structure. Below is a list of ten such documents, each highlighting how they relate to the Texas Dec 1 form.

When filling out the Texas Dec 1 form, it is essential to follow certain guidelines to ensure accuracy and completeness. Here are four things you should and shouldn't do:

The Texas Dec 1 form is an important document for homeowners insurance, but several misconceptions surround it. Understanding these can help homeowners make informed decisions about their coverage. Here are five common misconceptions:

By clearing up these misconceptions, homeowners can better navigate their insurance options and ensure they have the right coverage for their needs.

Understanding the Texas Dec 1 form is essential for homeowners in Texas. Here are nine key takeaways to help you navigate this important document:

By keeping these takeaways in mind, homeowners can better manage their insurance policies and ensure they are adequately protected.