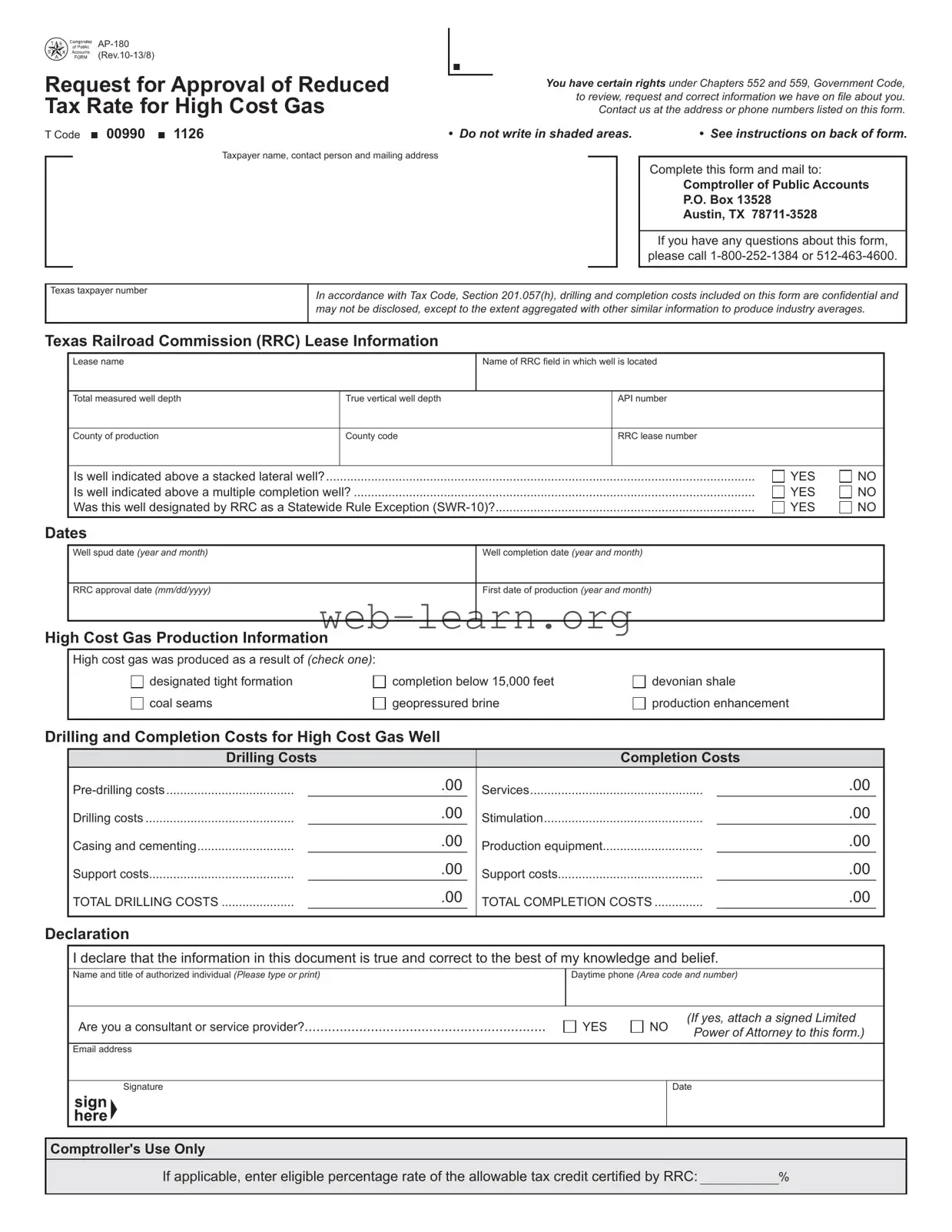

The Texas AP-180 form is a critical document for gas producers seeking a reduced tax rate on high-cost gas wells certified by the Texas Railroad Commission (RRC). This form is designed to facilitate the approval process for tax reductions, ensuring that producers can recoup some of their drilling and completion costs. It requires detailed information, including taxpayer identification, lease information, well specifications, and a breakdown of drilling and completion expenses. The form also mandates a declaration of the truthfulness of the submitted information, which is essential for maintaining transparency and compliance with state regulations. Producers must file this form within specific timeframes to avoid penalties and ensure eligibility for tax credits. Additionally, the AP-180 form emphasizes the confidentiality of certain financial data, protecting sensitive information while allowing for industry averages to be calculated. By following the guidelines outlined in the AP-180, producers can navigate the complexities of tax reductions and maximize their financial benefits.

Request for Approval of Reduced Tax Rate for High Cost Gas

T Code 00990 1126

Taxpayer name, contact person and mailing address

You have certain rights under Chapters 552 and 559, Government Code, to review, request and correct information we have on file about you.

Contact us at the address or phone numbers listed on this form.

• Do not write in shaded areas. |

• See instructions on back of form. |

Complete this form and mail to:

Comptroller of Public Accounts

P.O. Box 13528

Austin, TX

If you have any questions about this form, please call

Texas taxpayer number |

In accordance with Tax Code, Section 201.057(h), drilling and completion costs included on this form are confidential and |

|

|

|

may not be disclosed, except to the extent aggregated with other similar information to produce industry averages. |

|

|

Texas Railroad Commission (RRC) Lease Information

Lease name

Name of RRC field in which well is located

Total measured well depth

True vertical well depth

API number

County of production

County code

RRC lease number

Is well indicated above a stacked lateral well?............................................................................................................................

Is well indicated above a multiple completion well? ....................................................................................................................

Was this well designated by RRC as a Statewide Rule Exception

YES YES YES

NO NO NO

Dates

Well spud date (year and month)

Well completion date (year and month)

RRC approval date (mm/dd/yyyy)

First date of production (year and month)

High Cost Gas Production Information

High cost gas was produced as a result of (check one):

designated tight formation

coal seams

completion below 15,000 feet

geopressured brine

devonian shale

production enhancement

Drilling and Completion Costs for High Cost Gas Well

Drilling Costs |

Completion Costs |

.00 |

Services |

.00 |

|

_______________________ |

_______________________ |

||

Drilling costs |

.00 |

Stimulation |

.00 |

_______________________ |

_______________________ |

||

Casing and cementing |

.00 |

Production equipment |

.00 |

_______________________ |

_______________________ |

||

Support costs |

.00 |

Support costs |

.00 |

_______________________ |

_______________________ |

||

TOTAL DRILLING COSTS |

.00 |

TOTAL COMPLETION COSTS |

.00 |

_______________________ |

_______________________ |

Declaration

I declare that the information in this document is true and correct to the best of my knowledge and belief.

Name and title of authorized individual (Please type or print)

Daytime phone (Area code and number)

Are you a consultant or service provider?..............................................................

YES

NO |

(If yes, attach a signed Limited |

|

Power of Attorney to this form.) |

||

|

Email address

Signature

Date

Comptroller's Use Only

If applicable, enter eligible percentage rate of the allowable tax credit certified by RRC: |

|

% |

Form

General Information

Who Files: Form

What is Needed: A copy of a letter of certification from the Texas Railroad Commission must accompany each completed Form

When to File: To recoup credits for previously paid tax on approved reduced tax rates for high cost gas leases, the information filed on

•

•Ten Percent Penalty: Form

•

•

End Date of Exemption: The end date of an approved exempt high cost gas well is determined by either the earliest of 120 months from the date of first production or when the cumulative value of the tax savings equal to 50 percent of the total drilling and completion costs, whichever situation occurs first.

How to File Reports: An amended report is required to claim a credit for tax previously paid on an approved reduced tax rate for high cost gas leases. On natural gas producer and purchaser tax reports, report approved high cost gas leases as “Type 05” with the actual RRC lease number. Scenarios requiring an amended report are as follows:

•If the actual RRC lease number was previously reported as “Type 02”, credit out volumes and values reported and rebook volumes and values as “Type 05”.

•If no lease data was previously reported, report volumes and values as “Type 05” with the actual RRC lease number.

•If a drilling permit number was previously reported as “Type 02” and the corresponding lease is later approved for the reduced tax rate, credit out volumes and values and rebook as “Type 05” with the actual RRC lease number. Do not report a drilling permit number when initially reporting a “Type 05” lease.

Comptroller’s Website: Detailed Information on approved reduced tax rate for high cost gas leases is available at: http://window.state.tx.us/taxinfo/nat_gas/index.html. Click on the link labeled “CONG WEB Inquiry.”

Drilling Costs to be Included by Category

Predrilling - Damage payments to surface owner and any petroleum engineering or geoscience costs associated with the well location are not to be included. All costs related to surveying, permitting, constructing roads to well sites, including fences and gates, costs to build pad, cellar, concrete pad, rat and mouse holes, conductor hole and pipe, drilling pit and liner and the cost of any water well. Costs of any environmental surveys performed including any monitoring wells drilled at or near the wellsite and the preparation of environmental impact study that may be required and any necessary remediation.

Drilling - Day rates or footage costs including general costs associated with normal rig operations. Include rig mobilization, rig positioning and rig demobiliza- tion charges where applicable. All costs for fuel and power, mud and chemical materials used to drill and condition the hole and/or restore and maintain circulation and chemical materials such as weighting materials, lost circulation materials, crude oil, diesel oil or mineral oil used in the circulating system. Also, if applicable, include the cost for air or gas compression if used for drilling. Cost of drill bits used to drill the well from conductor to total depth including the cost of any diamond drilling bits that are used. Labor, material transportation, services, standby time, tool rentals for setting whipstocks, milling casing windows, setting casing whipstocks, cement plugs for directional drilling, any special bottomhole assemblies or equipment such as Dynadrills, Turbodrills, measurement while drilling assemblies and costs, jet deflecting stabilizers, reamers, hole openers and any other items that affect or influence the directional tendencies of a wellbore. Labor, material and services for mud logging and any drill stem testing during drilling operations. Include test analysis costs where applicable.

Casing and Cementing - Cost of casing, float shoes, float collars, and centralizers used in any portion of the casing program including any liners and liner hangers. Cost of cement, additives and pumping charges for the cement and costs for all plugs.

Support Costs - Costs associated with hauling water, casing or rental equipment to the well site. Costs for special equipment testing. Costs for roustabout crews. Costs of direct supervision of drilling operations.

Completion Costs to be Included by Category

Services - Rig used in completion operations. If the drilling rig is used for the completion operations, the costs must be separated. All wireline operations performed in the cased hole, including logging, perforating and setting tools on wireline. Costs of any fluids used in the wellbore (except fluids used during stimulation) during well operations from the time production casing is cemented until the well is turned to sales. Costs related to testing pay intervals that cannot be attributed to any other category. Costs for site restoration and for any remediation associated with the completion operations.

Well Stimulation - All costs associated with stimulating the pay interval. This includes acidizing and hydraulic fracturing charges as well as equipment costs that are specifically related to stimulation operations such as frac tanks. It includes the cost of coil tubing units and operations if used.

Production Equipment - The production tubing string, packers, bridgeplugs, tubing anchors and gravel packing. Any equipment installed on the wellhead including the wellhead itself. All equipment costs associated with gas lift or rod pumping equipment, including both down hole and surface equipment. Also included in this category are plunger lift and cavity displacement pumps and associated equipment. All equipment from the wing valve to the sales meter that is required to produce the well. This includes production, storage and separation equipment, meters, flowlines, chemical pumps and any location costs such as gates, roads and fences associated with the lease equipment. Drilling and Completion Costs does not include any costs incurred after the outlet of a lease separator or that would otherwise be considered a marketing cost for severance tax purposes.

Support Costs - Costs to transport materials and equipment to the well site that are not specifically chargeable to other more specific operations. This category includes hauling casing or tubing to location, but would not include the cost to haul water for a fracture stimulation. Rental equipment used to complete the well. Costs of roustabout crews used during and after drilling operations have ceased. Costs of direct supervision of completion operations.

| Fact Name | Details |

|---|---|

| Purpose of Form | Form AP-180 is used by producers to request a reduced tax rate for gas from high cost gas wells certified by the Texas Railroad Commission (RRC). |

| Governing Law | The form is governed by Texas Tax Code, Section 201.057(h), which ensures confidentiality of drilling and completion costs. |

| Filing Requirements | Producers must file the form within specific deadlines to avoid penalties. This includes a four-year statute of limitations for credit-amended reports. |

| Contact Information | For questions, contact the Comptroller of Public Accounts at 1-800-252-1384 or 512-463-4600. |

Filling out the Texas AP-180 form is an important step for producers seeking a reduced tax rate for high-cost gas wells. This process requires careful attention to detail to ensure all necessary information is provided accurately. Below are the steps to complete the form effectively.

Once you have completed the form, ensure that all required documentation, such as the letter of certification from the Texas Railroad Commission, is included. Mail the completed form to the Comptroller of Public Accounts at the specified address. If you have any questions during the process, don't hesitate to reach out to the provided contact numbers for assistance.

What is the Texas AP-180 form?

The Texas AP-180 form, also known as the Request for Approval of Reduced Tax Rate for High Cost Gas, is a document that producers must file to seek a reduced tax rate for gas produced from wells certified as high cost gas wells by the Texas Railroad Commission (RRC). This form helps producers recoup credits for taxes paid on these specific gas leases.

Who needs to file the AP-180 form?

Any producer who wants to obtain a reduced tax rate for gas on high cost gas wells must file the AP-180 form. If a consultant or service provider is filing on behalf of a taxpayer, a Limited Power of Attorney must be included with the submission.

What information is required when filing the AP-180?

When completing the AP-180, you need to provide:

When should I file the AP-180 form?

It’s crucial to file the AP-180 form within specific timeframes to avoid penalties. Generally, you should file it:

What happens if I miss the filing deadline?

If you do not file the AP-180 form by the applicable deadline, the tax exemption or deduction will be reduced by 10 percent. This reduction applies for the period starting 180 days after the first production date until the form is submitted.

How do I report the approved high cost gas leases?

When reporting approved high cost gas leases, you should use “Type 05” on natural gas producer and purchaser tax reports. Ensure that you include the actual RRC lease number. If there are any discrepancies, such as previously reported lease numbers, you will need to amend your reports accordingly.

What costs can I include in the AP-180 form?

Costs that can be included in the AP-180 form fall into several categories:

However, marketing costs incurred after the outlet of a lease separator should not be included.

Where can I find more information about the AP-180 form?

For detailed information regarding the AP-180 form and the process for filing, you can visit the Texas Comptroller's website at http://window.state.tx.us/taxinfo/nat_gas/index.html. This site contains valuable resources and guidance on approved reduced tax rates for high cost gas leases.

Completing the Texas AP-180 form can be a straightforward process, but several common mistakes can lead to delays or complications. One frequent error is failing to provide accurate contact information. Ensuring that the taxpayer name, contact person, and mailing address are correct is crucial for communication with the Comptroller's office.

Another common mistake involves neglecting to include the Texas taxpayer number. This number is essential for identifying the taxpayer and processing the request. Omitting it can result in unnecessary delays. Additionally, many individuals overlook the shaded areas on the form, which are designated for Comptroller use only. Writing in these areas can lead to confusion and processing errors.

Some filers do not attach the required letter of certification from the Texas Railroad Commission. This letter is necessary to validate the application for reduced tax rates on high-cost gas wells. Without it, the application may be rejected. Similarly, failing to indicate whether the well is a stacked lateral or multiple completion well can lead to complications. Accurate descriptions are vital for proper classification.

Incorrectly reporting drilling and completion costs is another frequent issue. Each cost category must be carefully filled out, and all relevant expenses should be included. Missing costs can affect the overall tax credit. Additionally, many people do not check the appropriate box regarding whether they are a consultant or service provider. This detail is essential, especially if a Limited Power of Attorney is required.

Timeliness is also a critical factor. Submitting the AP-180 form after the applicable deadlines can result in penalties. It is important to be aware of the four-year statute of limitations and other filing deadlines associated with the form. Ignoring these deadlines can significantly reduce the potential tax benefits.

Lastly, some filers fail to sign and date the form. An unsigned form is considered incomplete and will not be processed. Ensuring that all required sections are filled out accurately and completely is essential for a successful submission.

When dealing with the Texas AP-180 form, it is often necessary to accompany it with additional documents to ensure compliance and to streamline the process. Below is a list of forms that are commonly used alongside the AP-180, each serving a specific purpose in the context of tax reduction for high-cost gas wells.

In summary, the Texas AP-180 form is just one part of the process for obtaining a reduced tax rate for high-cost gas wells. The accompanying documents play a crucial role in ensuring that the application is complete and compliant with state regulations. Properly preparing these forms can significantly impact the efficiency of the tax reduction process.

When filling out the Texas AP-180 form, it's important to follow specific guidelines to ensure your submission is correct and complete. Here’s a list of what you should and shouldn't do:

Misconceptions about the Texas AP-180 form can lead to confusion and errors in the filing process. Here are ten common misconceptions:

Filling out and using the Texas AP-180 form requires careful attention to detail. Here are five key takeaways to keep in mind:

Understanding these aspects can streamline the process and help ensure compliance with Texas tax regulations.