The Texas 811 form, known as the Certificate of Reinstatement, serves a crucial role for businesses looking to restore their legal standing in the state. This form is necessary for reinstating various types of entities that may have been voluntarily or involuntarily terminated. It applies to domestic entities that have been voluntarily dissolved, those that faced involuntary termination by the Secretary of State, and foreign entities whose registrations have been revoked. However, it is important to note that not all situations qualify for this form; entities forfeited under the Tax Code or terminated by court order should not use it. The form includes specific instructions for providing essential information, such as the entity's name, file number, and jurisdiction, as well as the date of termination or revocation. Additionally, it outlines the conditions for reinstatement and the necessary steps to ensure compliance with Texas law. Timeliness is key, as reinstatement must typically occur within three years of termination or revocation. Understanding the requirements and processes involved can help businesses navigate the reinstatement landscape effectively.

Form

The attached form is designed to meet minimal statutory filing requirements pursuant to the relevant code provisions. This form and the information provided are not substitutes for the advice and services of an attorney and tax specialist.

Commentary

This form may be used to reinstate: (1) the existence of a domestic filing entity that has been voluntarily terminated; (2) the existence of a domestic filing entity that has been involuntarily terminated by action of the secretary of state; or (3) the registration of a foreign filing entity whose registration has been revoked by action of the secretary of state.

Do Not Use This Form If:

クThe entity’s existence or registration was forfeited under the Tax Code. See Form 801.

クThe entity is a professional association that was terminated or revoked for failure to timely file an annual statement. See Form 814.

クThe entity was terminated or revoked by court order.

ンTime Frames for Reinstatement ン

ᄒVoluntarily Terminated Domestic Entity: Certificate of reinstatement must be filed no later than the third (3rd) anniversary of the effective date of the termination. (See part 4A of the form.)

ᄒInvoluntarily Terminated Domestic Entity: Certificate of reinstatement may be filed at any time so long as the entity would otherwise have continued to exist. However, the entity is considered to have

continued in existence without interruption from the date of termination only if the entity is reinstated before the third (3rd) anniversary of the date of involuntary termination. (See 4B.)

ᄒRevoked Foreign Entity Registration: Certificate of reinstatement must be filed no later than the third (3rd) anniversary of the effective date of the revocation. (See 4C.)

Instructions for Form

クItem

クItem

クItem

クItem

4A. Reinstatement of a Texas Entity Following Voluntary Termination: Sections 11.201 and 11.202 of the BOC permit reinstatement no later than the third anniversary of the effective date of termination if the owners, members, governing persons, or other persons specified by the BOC approve the reinstatement in the manner provided by the title of the BOC governing the entity and:

Form 811 |

1 |

(1)the termination was by mistake or was inadvertent;

(2)the termination occurred without the approval of the entity’s governing persons when approval is required by the title of the BOC governing the entity;

(3)the process of winding up before termination had not been completed by the entity; or

(4)the legal existence of the entity is necessary to convey or assign property, to settle or release a claim or liability, to take an action, or to sign an instrument or agreement.

4B. Reinstatement of a Texas Entity Following Involuntary Termination: Section 11.251 of the BOC authorizes the secretary of state to involuntarily terminate a domestic filing entity, other than a domestic real estate investment trust, if the secretary finds that the entity has failed to:

(1)file a report within the period required by law or to pay a fee or penalty prescribed by law when due and payable;

(2)maintain a registered agent or registered office in Texas as required by law; or

(3)pay a fee required in connection with a filing, or payment of the fee was dishonored when presented by the state for payment.

As a condition to reinstatement, the entity must correct the circumstances that led to termination and any other circumstances of the type described above, including paying any fees, interest or penalties.

4C. Reinstatement of a Foreign Entity Following Revocation: Section 9.101 of the BOC authorizes the secretary of state to revoke the registration of a foreign filing entity if the secretary finds that the entity has failed to:

(1)file a report within the period required by law or to pay a fee or penalty prescribed by law when due and payable;

(2)maintain a registered agent or registered office in Texas as required by law;

(3)amend its registration when required by law; or

(4)pay a fee required in connection with a filing, or payment of the fee was dishonored when presented by the state for payment.

As a condition to reinstatement, the entity must correct the circumstances that led to revocation and any other circumstances of the type described above, including paying any fees, interest or penalties.

クItem

An entity that was involuntarily terminated or that had its registration revoked for failure to maintain a registered agent or registered office in Texas need not submit an additional filing to change the registered agent or registered office.

Consent: A person designated as the registered agent of an entity must have consented, either in a written or electronic form, to serve as the registered agent of the entity. Although consent is required, a copy of the person’s written or electronic consent need not be submitted with the reinstatement. The liabilities and penalties imposed by sections 4.007 and 4.008 of the BOC apply with respect to a false statement in a filing instrument that names a person as the registered agent of an entity without that person’s consent. (BOC § 5.207)

Office Address Requirements: The registered office address must be located at a street address where service of process may be personally served on the entity’s registered agent during normal

Form 811 |

2 |

business hours. Although the registered office is not required to be the entity’s principal place of business, the registered office may not be solely a mailbox service or telephone answering service (BOC § 5.201).

クEntity Name Availability: The reinstatement cannot be filed if the entity name is the same as, deceptively similar to, or similar to the name of any existing domestic or foreign filing entity, or any name reservation or registration filed with the secretary of state. The administrative rules for determining entity name availability (Texas Administrative Code, title 1, part 4, chapter 79, subchapter C) may be viewed at http://www.sos.state.tx.us/tac/index.shtml.

If the entity name is no longer available or written consent for the use of the name is required but cannot be obtained, the entity must amend its certificate of formation or application for registration, as appropriate, to state an available name. The amendment must be submitted at the same time as the certificate of reinstatement.

クTax Clearance: Unless the entity is a nonprofit corporation, a certificate of reinstatement must be accompanied by a tax clearance letter from the Texas Comptroller of Public Accounts stating that the entity has satisfied all franchise tax liabilities and may be reinstated.

Contact the Comptroller for assistance in complying with franchise tax filing requirements and obtaining the necessary tax clearance letter. The Comptroller may be contacted by

クExecution: The reinstatement must be signed by a person authorized to act on behalf of the entity in regard to the filing instrument. Generally, a governing person or managerial official of the entity signs a filing instrument.

The certificate of reinstatement need not be notarized. However, before signing, please read the statements on this form carefully. The designation or appointment of a person as the registered agent by a managerial official is an affirmation by that official that the person named in the instrument has consented to serve as registered agent. (BOC § 5.2011)

A person commits an offense under section 4.008 of the BOC if the person signs or directs the filing of a filing instrument the person knows is materially false with the intent that the instrument be delivered to the secretary of state for filing. The offense is a Class A misdemeanor unless the person’s intent is to harm or defraud another, in which case the offense is a state jail felony.

クPayment and Delivery Instructions: Unless the entity is a nonprofit corporation or cooperative association, the filing fee for reinstatement following an involuntary termination or revocation is $75, and the filing fee for reinstatement following a voluntary termination is $15. The filing fee for reinstating a nonprofit corporation or a cooperative association is $5.

Fees may be paid by personal checks, money orders, LegalEase debit cards, or American Express, Discover, MasterCard, and Visa credit cards. Checks or money orders must be payable through a U.S. bank or financial institution and made payable to the secretary of state. Fees paid by credit card are subject to a statutorily authorized convenience fee of 2.7 percent of the total fees. Applicable fees for any additional filings required as a condition for reinstatement must be submitted together with the appropriate filing fee for the certificate of reinstatement.

Submit the completed form in duplicate along with the filing fee. The form may be mailed to P.O. Box 13697, Austin, Texas

Revised 05/11

Form 811 |

3 |

Form 811 (Revised 05/11)

Submit in duplicate to: Secretary of State P.O. Box 13697 Austin, TX

512

Filing Fee: See instructions

This space reserved for office use.

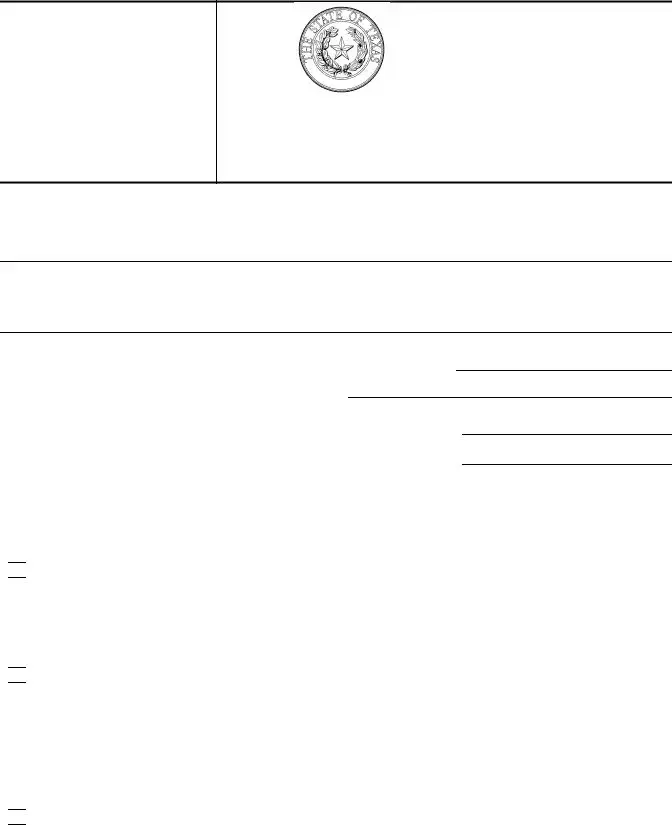

Certificate of

Reinstatement

1. The name of the entity is:

The entity is a foreign entity that was required to obtain its registration under a name that differs from the legal name stated above. The name under which the entity is registered is:

The file number issued to the filing entity by the secretary of state is:

2. The jurisdiction of organization of the entity is:

(state or country)

The entity was organized or obtained its certificate of registration on:

mm/dd/yyyy

3. The effective date of the entity’s termination or revocation is:

mm/dd/yyyy

4.The condition giving rise to the termination of the entity’s existence or the revocation of its registration is described below. The entity requests reinstatement under the following code provision:

(Select the appropriate box below. Do not check more than one box.)

4A. Reinstatement of a Texas Entity Following a Voluntary Termination (3 year limit)

The domestic filing entity requests reinstatement under section 11.202 of the BOC following the filing of a certificate of termination. The undersigned certifies that the conditions for reinstatement of the entity’s certificate of formation are met and that the reinstatement of the filing entity has been approved in the manner provided by the Texas Business Organizations Code.

4B. Reinstatement of a Texas Entity Following an Involuntary Termination

The domestic filing entity requests reinstatement of its certificate of formation after the involuntary termination of its existence by the secretary of state pursuant to subchapter F of chapter 11 of the Code. The entity has corrected the circumstances giving rise to its involuntary termination and has taken any other action required for its reinstatement, including the payment of any fees, interest, or penalties. The undersigned certifies that the reinstatement of the filing entity has been approved in the manner required by the Texas Business Organizations Code.

4C. Reinstatement Following Revocation of Registration of a Foreign Entity (3 year limit)

The foreign filing entity requests the reinstatement of its certificate of registration after its revocation by the secretary of state pursuant to subchapter C of chapter 9 of the BOC. The entity has corrected the circumstances giving rise to its revocation and has taken any other action required for its reinstatement, including the payment of any fees, interest, or penalties.

Form 811 |

4 |

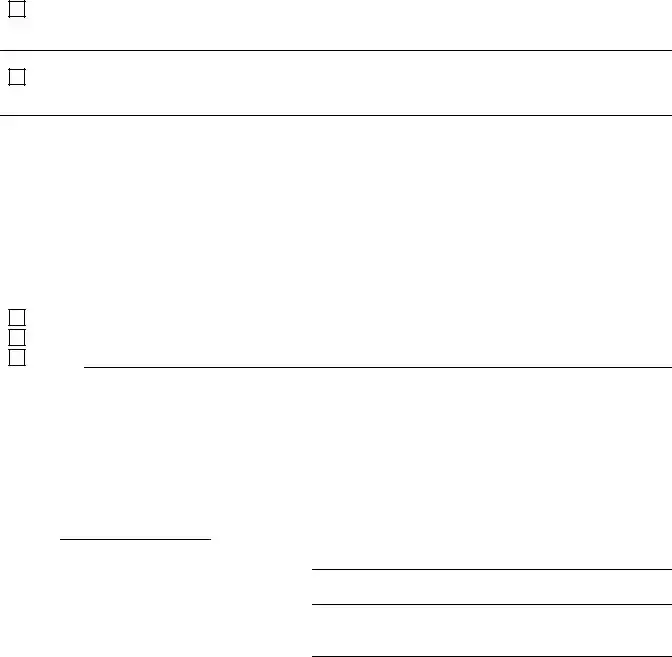

5.The name of the entity’s registered agent and the address of the entity’s registered office are as

follows: (Select and complete either A or B and complete C)

A. The registered agent is an organization (cannot be the entity seeking reinstatement) by the name of:

OR

B. The registered agent is an individual resident of the state whose name is set forth below:

First Name |

M.I. |

Last Name |

Suffix |

C. The business address of the registered agent and the registered office address is:

|

|

TX |

|

Street Address |

City |

State |

Zip Code |

The street address of the registered office as stated in this instrument is the same as the registered agent’s business address.

Additional Documentation or Filings

Comptroller of Public Accounts Tax Clearance Letter (Required, unless entity is a nonprofit corporation.)

Amendment to Certificate of Formation or Registration (Required if entity name is no longer available.) Other

(A certificate of reinstatement may be conditioned on the submission of additional filings. See instructions.)

Execution

The undersigned affirms that the person designated as registered agent has consented to the appointment. The undersigned signs this document subject to the penalties imposed by law for the submission of a materially false or fraudulent instrument and certifies under penalty of perjury that the undersigned is authorized under the provisions of law governing the entity to execute the filing instrument.

Date:

By:

Signature of authorized person (see instructions)

Printed or typed name of authorized person

Form 811 |

5 |

| Fact Name | Details |

|---|---|

| Purpose | The Texas 811 form is used to reinstate the existence of certain domestic and foreign filing entities that have been terminated or revoked. |

| Governing Law | The form is governed by the Texas Business Organizations Code (BOC), specifically sections 11.201, 11.202, and 9.101. |

| Eligibility | This form is applicable for reinstating voluntarily terminated entities, involuntarily terminated entities, and revoked foreign entity registrations. |

| Filing Deadlines | Reinstatement must occur within three years of termination or revocation for all applicable entities. |

| Registered Agent Requirement | Entities must designate a registered agent who has consented to serve. The agent cannot be the entity itself. |

| Tax Clearance | A tax clearance letter from the Texas Comptroller is required unless the entity is a nonprofit corporation. |

| Filing Fees | The fees vary: $15 for voluntary termination, $75 for involuntary termination, and $5 for nonprofit entities. |

Filling out the Texas 811 form is an important step in reinstating your entity's status. Make sure to have all necessary information ready, as this will streamline the process. Follow the steps below to complete the form accurately.

After submission, the secretary of state will process your request. Keep an eye out for confirmation and any additional documentation that may be returned to you. This will include a file-stamped copy of your form, confirming the reinstatement of your entity.

What is the Texas 811 form used for?

The Texas 811 form, also known as the Certificate of Reinstatement, is utilized to reinstate the existence of a domestic filing entity that has been voluntarily or involuntarily terminated. It can also be used to reinstate a foreign filing entity whose registration has been revoked. Essentially, this form helps restore an entity's legal standing in Texas.

Who should use the Texas 811 form?

This form is appropriate for entities that have faced termination or revocation but wish to continue their operations. Specifically, it applies to:

When must the Texas 811 form be filed?

The timing for filing the Texas 811 form varies based on the type of termination:

What information is required to complete the Texas 811 form?

When filling out the Texas 811 form, you will need to provide:

Can I use the Texas 811 form if my entity was forfeited under the Tax Code?

No, the Texas 811 form cannot be used for entities that were forfeited under the Tax Code. In such cases, you would need to refer to Form 801 instead. It's important to ensure that you are using the correct form for your specific situation.

What are the fees associated with filing the Texas 811 form?

The filing fees vary depending on the type of entity and the circumstances of reinstatement:

Additional fees may apply for any required filings related to the reinstatement process.

What is a tax clearance letter, and why is it needed?

A tax clearance letter is a document from the Texas Comptroller of Public Accounts confirming that the entity has satisfied all franchise tax obligations. This letter is required to accompany the Texas 811 form unless the entity is a nonprofit corporation. It ensures that all financial obligations are met before reinstatement.

Who can serve as a registered agent for my entity?

The registered agent can either be:

However, the entity itself cannot act as its own registered agent, and the agent must consent to the appointment.

What happens after I submit the Texas 811 form?

Once the Texas 811 form is submitted, the Secretary of State will review it. If everything is in order, they will process the reinstatement and return evidence of filing along with a file-stamped copy of the document. This confirmation is crucial for your records.

What should I do if my entity name is no longer available?

If the name of your entity is no longer available, you must amend your certificate of formation or registration to reflect a new, available name. This amendment must be submitted alongside the Texas 811 form to ensure compliance with naming regulations.

Filling out the Texas 811 form can be a straightforward process, but many individuals make common mistakes that can delay their reinstatement. One significant error is failing to provide the correct entity name and file number. It’s essential to ensure that the legal name of the entity matches exactly with the name on record with the Secretary of State. Any discrepancies can lead to rejection of the application.

Another common mistake involves the jurisdictional information. Applicants often overlook the importance of specifying the correct jurisdiction of organization and the date of organization or registration in Texas. Providing inaccurate or incomplete information can complicate the reinstatement process.

Many people also neglect to include the effective date of termination or revocation. This date is crucial for determining the timeline for reinstatement. Without it, the Secretary of State may not process the application correctly, leading to unnecessary delays.

Choosing the wrong grounds for reinstatement is yet another frequent error. The form requires applicants to select only one condition for reinstatement. Some individuals mistakenly check multiple boxes, which can invalidate the application. If there is uncertainty about the reason for inactive status, it’s advisable to contact the Secretary of State for clarification before submitting the form.

Providing outdated or incorrect information for the registered agent and registered office is also a common pitfall. The registered agent must be either a domestic entity or a qualified individual resident of Texas. If the entity acts as its own registered agent, the application will be rejected. Ensure that the registered office address is a physical location and not just a mailbox service.

Lastly, failing to obtain a tax clearance letter can halt the reinstatement process. Unless the entity is a nonprofit corporation, this letter is necessary to confirm that all franchise tax obligations have been met. It’s crucial to reach out to the Texas Comptroller of Public Accounts for assistance in obtaining this document before submitting the form.

The Texas 811 form is essential for reinstating a business entity in Texas, but it often works alongside other important documents. Each of these documents serves a specific purpose and helps ensure that the reinstatement process runs smoothly. Below is a list of commonly used forms and documents that may accompany the Texas 811 form.

Each of these documents plays a vital role in the reinstatement process for business entities in Texas. Ensuring that all necessary paperwork is completed and submitted can help avoid delays and complications. Always consider consulting with a legal professional for tailored advice based on your specific situation.

When filling out the Texas 811 form, it is important to follow specific guidelines to ensure a smooth process. Here are seven things you should and shouldn't do:

Understanding the Texas 811 form is essential for anyone looking to reinstate a business entity. However, several misconceptions can lead to confusion. Here are nine common misconceptions and clarifications:

By addressing these misconceptions, individuals can navigate the reinstatement process more effectively and ensure compliance with Texas regulations.

Filling out and using the Texas 811 form for reinstatement is a critical process for entities that have faced termination or revocation. Here are nine key takeaways to consider: