The Texas 12-302 form serves as a vital tool for individuals and organizations seeking to claim exemptions from hotel occupancy taxes while traveling for official business. This form is specifically designed for guests affiliated with exempt entities, such as federal agencies, state government officials, charitable organizations, educational institutions, and religious entities. To successfully utilize the form, guests must provide essential information, including the name and address of the exempt organization, as well as their own details and certification of their travel purpose. It is important for hotel operators to verify the guest's affiliation by requesting a photo ID or other supporting documentation. The form outlines various exemption categories, detailing the specific requirements and limitations for each. For example, while federal agencies and foreign diplomats are exempt from both state and local hotel taxes, charitable and educational entities may only receive exemptions from state taxes. Additionally, the form emphasizes the necessity for accurate completion, as issuing an exemption certificate under false pretenses could lead to serious legal consequences. Understanding the nuances of the Texas 12-302 form can help travelers navigate the complexities of hotel taxes and ensure compliance with state regulations.

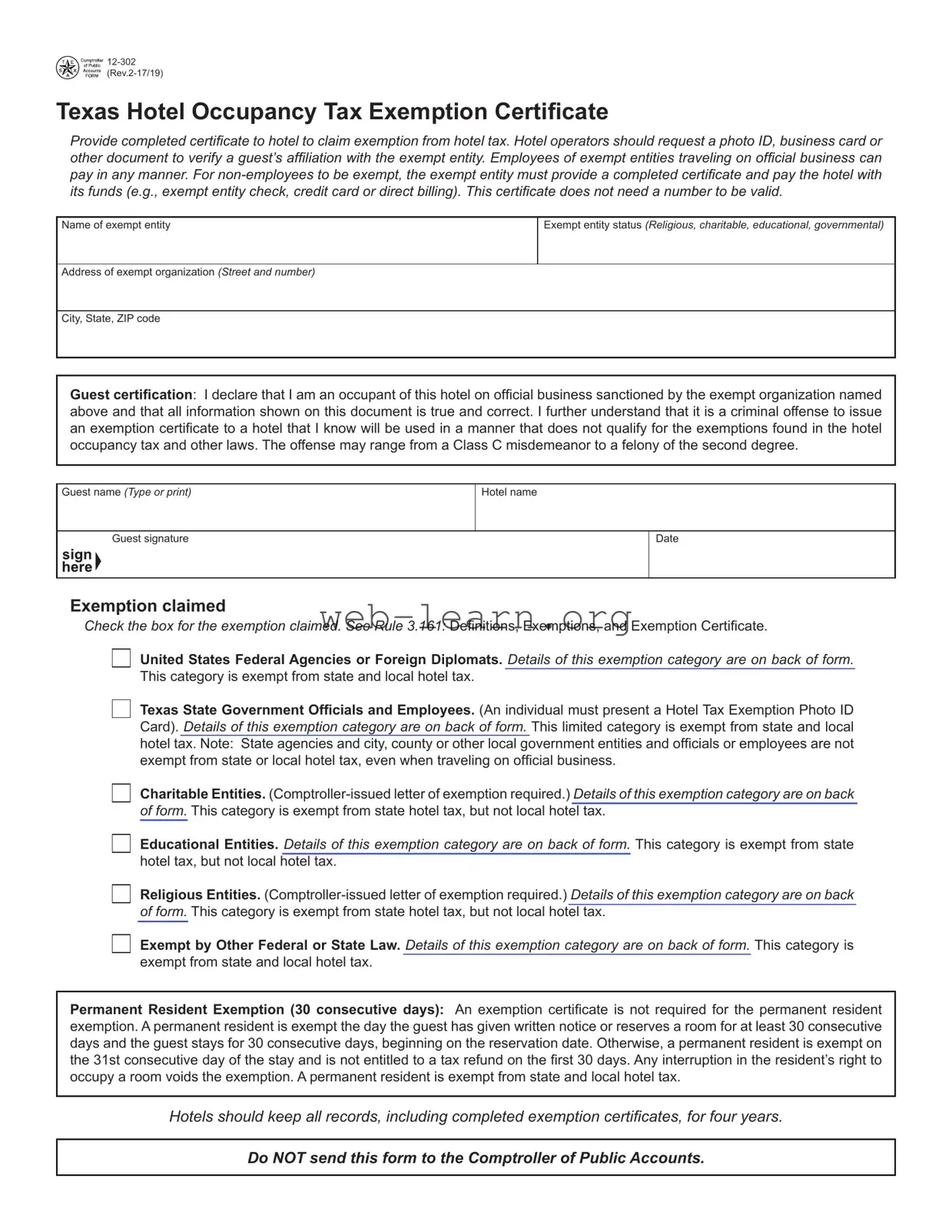

Texas Hotel Occupancy Tax Exemption Certiicate

Provide completed certiicate to hotel to claim exemption from hotel tax. Hotel operators should request a photo ID, business card or other document to verify a guest’s afiliation with the exempt entity. Employees of exempt entities traveling on oficial business can pay in any manner. For

Name of exempt entity

Exempt entity status (Religious, charitable, educational, governmental)

Address of exempt organization (Street and number)

City, State, ZIP code

Guest certiication: I declare that I am an occupant of this hotel on oficial business sanctioned by the exempt organization named above and that all information shown on this document is true and correct. I further understand that it is a criminal offense to issue an exemption certiicate to a hotel that I know will be used in a manner that does not qualify for the exemptions found in the hotel occupancy tax and other laws. The offense may range from a Class C misdemeanor to a felony of the second degree.

Guest name (Type or print)

Hotel name

Guest signature

Date

Exemption claimed

Check the box for the exemption claimed. See Rule 3.161: Deinitions, Exemptions, and Exemption Certiicate.

United States Federal Agencies or Foreign Diplomats. Details of this exemption category are on back of form. This category is exempt from state and local hotel tax.

Texas State Government Oficials and Employees. (An individual must present a Hotel Tax Exemption Photo ID Card). Details of this exemption category are on back of form. This limited category is exempt from state and local hotel tax. Note: State agencies and city, county or other local government entities and oficials or employees are not exempt from state or local hotel tax, even when traveling on oficial business.

Charitable Entities.

Educational Entities. Details of this exemption category are on back of form. This category is exempt from state hotel tax, but not local hotel tax.

Religious Entities.

Exempt by Other Federal or State Law. Details of this exemption category are on back of form. This category is exempt from state and local hotel tax.

Permanent Resident Exemption (30 consecutive days): An exemption certiicate is not required for the permanent resident exemption. A permanent resident is exempt the day the guest has given written notice or reserves a room for at least 30 consecutive days and the guest stays for 30 consecutive days, beginning on the reservation date. Otherwise, a permanent resident is exempt on the 31st consecutive day of the stay and is not entitled to a tax refund on the irst 30 days. Any interruption in the resident’s right to occupy a room voids the exemption. A permanent resident is exempt from state and local hotel tax.

Hotels should keep all records, including completed exemption certiicates, for four years.

Do NOT send this form to the Comptroller of Public Accounts.

Form

Texas Hotel Occupancy Tax Exemptions

See Rule 3.161: Deinitions, Exemptions, and Exemption Certiicate for additional information.

United States Federal Agencies or Foreign Diplomats (exempt from state and local hotel tax)

This exemption category includes the following:

•the United States federal government, its agencies and departments, including branches of the military, federal credit unions, and their employees traveling on oficial business;

•rooms paid by vouchers issued by the American Red Cross and the Federal Emergency Management Agency; and

•foreign diplomats who present a Tax Exemption Card issued by the U.S. Department of State, unless the card speciically excludes hotel occupancy tax.

Federal government contractors are not exempt.

Texas State Government Oficials and Employees (exempt from state and local hotel tax)

This exemption category includes only Texas state oficials or employees who present a Hotel Tax Exemption Photo Identiication Card. State employees without a Hotel Tax Exemption Photo Identiication Card and Texas state agencies are not exempt. (The state employee must pay hotel tax, but their state agency can apply for a refund.)

Charitable Entities (exempt from state hotel tax, but not local hotel tax)

This exemption category includes entities that have been issued a letter of tax exemption as a charitable organization and their employees traveling on oficial business. See website referenced below.

A charitable entity devotes all or substantially all of its activities to the alleviation of poverty, disease, pain and suffering by providing food, clothing, medicine, medical treatment, shelter or psychological counseling directly to indigent or similarly deserving members of society.

Not all 501(c)(3) or nonproit organizations qualify under this category.

Educational Entities (exempt from state hotel tax, but not local hotel tax)

This exemption category includes

A letter of tax exemption from the Comptroller of Public Accounts as an educational organization is not required, but an educational organization might have one.

Religious Organizations (exempt from state hotel tax, but not local hotel tax)

This exemption category includes nonproit churches and their guiding or governing bodies that have been issued a letter of tax exemption from the Comptroller of Public Accounts as a religious organization and their employees traveling on oficial business. See website referenced below.

Exempt by Other Federal or State Law (exempt from state and local hotel tax)

This exemption category includes the following:

•entities exempted by other federal law, such as federal land banks and federal land credit associations and their employees traveling on oficial business; and

•Texas entities exempted by other state law that have been issued a letter of tax exemption from the Comptroller of Public Accounts and their employees traveling on oficial business. See website referenced below. These entities include the following:

•nonproit electric and telephone cooperatives,

•housing authorities,

•housing inance corporations,

•public facility corporations,

•health facilities development corporations,

•cultural education facilities inance corporations, and

•major sporting event local organizing committees.

For Exemption Information

A list of charitable, educational, religious and other organizations that have been issued a letter of exemption is online at www.comptroller.texas.gov/taxes/exempt/search.php. Other information about Texas tax exemptions, including applications, is online at www.comptroller.texas.gov/taxes/exempt/index.php. For questions about exemptions, call

| Fact Name | Description | Governing Law |

|---|---|---|

| Purpose of Form | The Texas 12-302 form is used to claim an exemption from hotel occupancy tax for eligible entities. | Texas Tax Code, Chapter 156 |

| Eligibility Criteria | Entities such as federal agencies, state officials, charitable organizations, educational institutions, and religious groups can qualify for tax exemptions. | Texas Administrative Code, Rule 3.161 |

| Verification Requirements | Hotel operators must verify a guest's affiliation with the exempt entity by requesting a photo ID or business card. | Texas Tax Code, Chapter 156 |

| Record Keeping | Hotels must retain completed exemption certificates for four years as part of their records. | Texas Tax Code, Chapter 156 |

To complete the Texas Hotel Occupancy Tax Exemption Certificate (Form 12-302), follow these steps. Make sure you have all necessary information ready, including your affiliation with the exempt entity and the details of your stay.

After filling out the form, provide it to the hotel to claim your exemption from hotel tax. Ensure that you keep a copy for your records, as hotels must retain completed exemption certificates for four years.

What is the purpose of the Texas 12-302 form?

The Texas 12-302 form serves as a Hotel Occupancy Tax Exemption Certificate. It allows individuals affiliated with certain exempt entities, such as government agencies, educational institutions, and charitable organizations, to claim an exemption from hotel occupancy taxes when traveling for official business. By providing this completed form to the hotel, guests can avoid paying these taxes, provided they meet the necessary criteria.

Who qualifies for the hotel tax exemption under this form?

Several categories of individuals and organizations may qualify for the exemption:

Each category has specific requirements, so it is essential to review them closely.

How should the exemption be claimed?

To claim the exemption, the exempt entity must provide a completed Texas 12-302 form to the hotel. For employees of exempt entities, payment can be made using any method. However, for non-employees, the exempt entity must pay for the hotel using its own funds, such as a company check or credit card. It is important that the form is filled out accurately to ensure compliance with tax regulations.

What happens if a guest provides false information on the form?

Providing false information on the Texas 12-302 form can lead to serious consequences. It is considered a criminal offense to issue an exemption certificate with the knowledge that it will be used improperly. The penalties can range from a Class C misdemeanor to a felony of the second degree. Therefore, it is crucial for guests to ensure that all information provided is true and correct.

How long should hotels keep records of exemption certificates?

Hotels are required to maintain all records related to exemption certificates for a period of four years. This includes the completed Texas 12-302 forms. Keeping accurate records is essential for compliance and can be helpful in the event of an audit or inquiry regarding tax exemptions.

Do I need to send the Texas 12-302 form to the Comptroller of Public Accounts?

No, the Texas 12-302 form should not be sent to the Comptroller of Public Accounts. Instead, it should be provided directly to the hotel at which the guest is staying. This process ensures that the hotel can apply the exemption correctly and maintain proper documentation for its records.

Filling out the Texas Hotel Occupancy Tax Exemption Certificate (Form 12-302) can be straightforward, but many people make common mistakes that can lead to complications. One frequent error is failing to provide the correct name of the exempt entity. This name must match exactly with the records of the entity. If there is a discrepancy, the hotel may deny the exemption.

Another mistake is not checking the appropriate box for the exemption claimed. Each exemption category has specific requirements, and selecting the wrong one can invalidate the certificate. It is essential to read the instructions carefully to ensure that the right exemption is chosen.

Many individuals overlook the requirement for a photo ID or business card to verify their affiliation with the exempt entity. Hotels often request this documentation to confirm that the guest is indeed eligible for the exemption. Without it, the hotel may charge the occupancy tax.

Providing incomplete or inaccurate information is another common issue. Guests must ensure that all fields are filled out correctly, including the address of the exempt organization and the guest's name. Missing or incorrect details can lead to delays or denials in the exemption process.

Some people mistakenly believe that the exemption certificate does not need to be signed. However, the guest's signature is crucial, as it affirms the accuracy of the information provided. A missing signature can render the certificate invalid.

Additionally, guests often fail to understand the limitations of the exemptions. For instance, while charitable and educational entities may be exempt from state hotel tax, they may still be liable for local hotel taxes. It’s important to be aware of these nuances to avoid unexpected charges.

Another frequent oversight involves the duration of stay for the permanent resident exemption. Guests must stay for at least 30 consecutive days to qualify. If there is any interruption in the stay, the exemption is voided. Understanding this requirement can prevent unnecessary tax charges.

Lastly, many individuals forget that the completed certificate should not be sent to the Comptroller of Public Accounts. It must be provided directly to the hotel. Misplacing this form can lead to confusion and potential tax liabilities.

The Texas 12-302 form is essential for claiming an exemption from hotel occupancy tax. Alongside this form, there are several other documents that individuals or organizations may need to provide to ensure compliance with tax regulations. Below is a list of these forms and documents, each playing a crucial role in the exemption process.

Understanding these documents can simplify the process of claiming hotel occupancy tax exemptions. Each document has specific requirements and serves a distinct purpose, ensuring that both guests and hotel operators adhere to the regulations set forth by Texas law.

The Texas 12-302 form serves a specific purpose in relation to hotel occupancy tax exemptions. Several other documents share similarities with this form, each addressing different types of exemptions. Below is a list of documents that are similar to the Texas 12-302 form, highlighting their key features:

Each of these documents plays a crucial role in ensuring that eligible organizations can claim their rightful exemptions while providing necessary proof of their status. Understanding the similarities can help in navigating the requirements for tax exemptions effectively.

When filling out the Texas 12-302 form, it is essential to adhere to specific guidelines to ensure that the process goes smoothly. Here is a list of things you should and shouldn't do:

Misconceptions about the Texas 12 302 form can lead to confusion and potential tax issues. Here are nine common misunderstandings:

Understanding these misconceptions can help ensure compliance and avoid unnecessary tax liabilities. Always verify the specific requirements for exemptions based on your situation.

When filling out and using the Texas 12-302 form, it’s important to keep a few key points in mind to ensure you navigate the process smoothly and correctly.