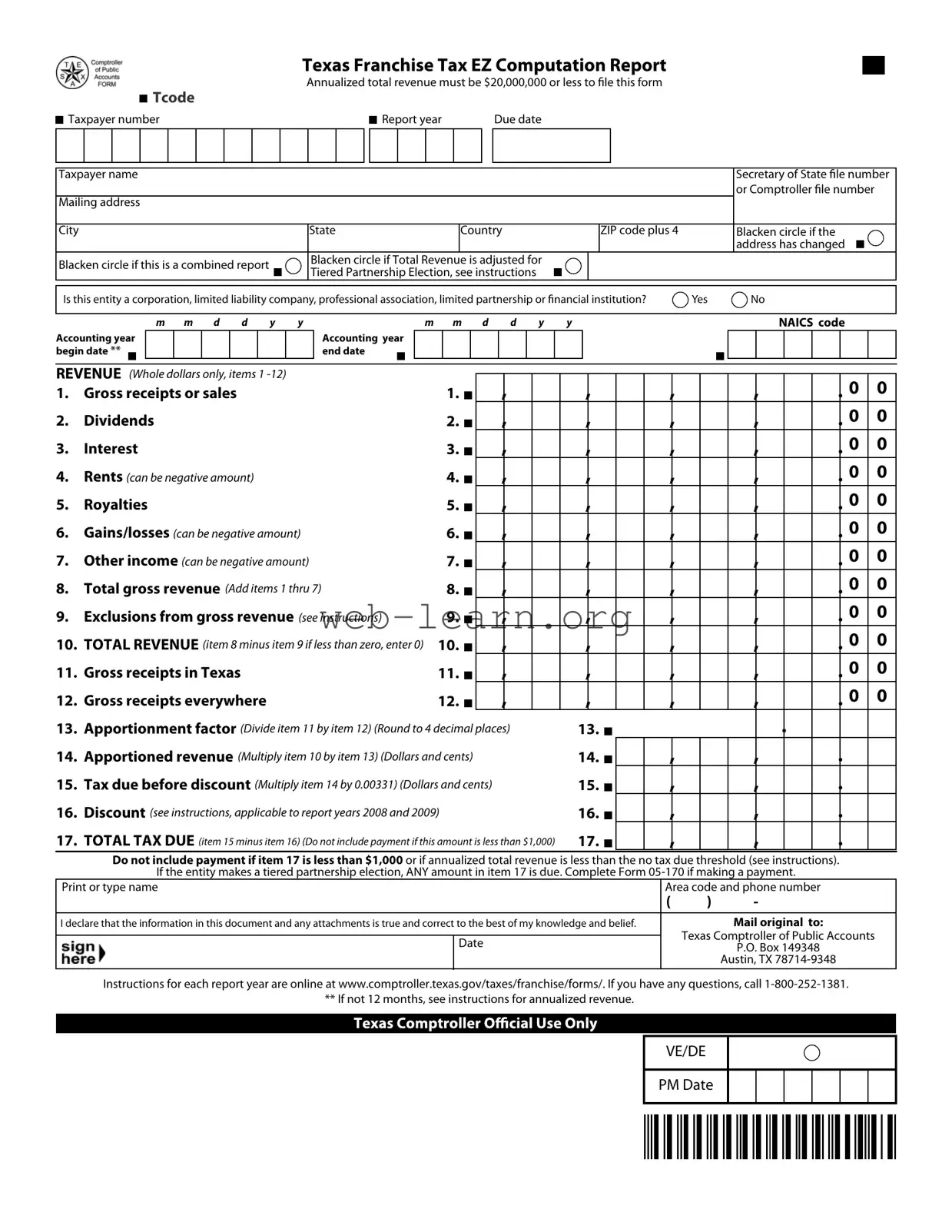

The Texas 05-169 form, also known as the Texas Franchise Tax EZ Computation Report, is an essential document for certain businesses operating in Texas. This form is specifically designed for entities with an annualized total revenue of $20,000,000 or less. It serves as a simplified way to report franchise taxes owed to the state. Key sections of the form require businesses to provide their taxpayer number, report year, and various revenue details, including gross receipts, dividends, and other income sources. Additionally, it includes calculations for total revenue and tax due, ensuring that businesses can determine their financial obligations accurately. Certain options, such as indicating if the address has changed or if the report is combined, help streamline the filing process. The form also addresses tiered partnership elections, which can impact tax liabilities. Completing the 05-169 form accurately is crucial, as it directly affects tax calculations and compliance with state regulations.

|

|

|

|

|

|

Texas Franchise Tax EZ Computation Report |

|

|

|

|

|

||||||||||||||||||||||

|

|

|

|

|

|

Annualized total revenue must be $20,000,000 or less to file this form |

|

|

|

|

|

||||||||||||||||||||||

|

|

|

|

|

Tcode 13252 |

Annual |

|

|

|

|

|

|

|

|

|

|

|

Due date |

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

Taxpayer number |

|

|

|

|

|

|

|

|

Report year |

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

Taxpayer name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Secretary of State file number |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

or Comptroller file number |

|||

Mailing address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

City |

|

|

|

|

State |

|

Country |

ZIP code plus 4 |

|

Blacken circle if the |

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

address has changed |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Blacken circle if this is a combined report |

|

|

|

Blacken circle if Total Revenue is adjusted for |

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Tiered Partnership Election, see instructions |

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

||||||||||||||||||||||||||||

|

Is this entity a corporation, limited liability company, professional association, limited partnership or financial institution? |

Yes |

No |

||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

m m d d y

Accounting year begin date **

y |

m m d d y y |

NAICS code |

Accounting year end date

REVENUE (Whole dollars only, items 1 |

|

|

|

1. |

Gross receipts or sales |

1. |

|

|

|||

2. |

Dividends |

2. |

|

|

|||

3. |

Interest |

3. |

|

|

|||

4. |

Rents (can be negative amount) |

4. |

|

|

|||

5. |

Royalties |

5. |

|

|

|||

6. |

Gains/losses (can be negative amount) |

6. |

|

|

|||

7. |

Other income (can be negative amount) |

7. |

|

|

|||

8. |

Total gross revenue (Add items 1 thru 7) |

8. |

|

|

|||

9. |

Exclusions from gross revenue (see instructions) |

9. |

|

|

|||

|

|||

10. |

TOTAL REVENUE (item 8 minus item 9 if less than zero, enter 0) |

10. |

|

|

|||

11. |

Gross receipts in Texas |

11. |

|

|

|||

12. |

Gross receipts everywhere |

12. |

|

|

|||

13.Apportionment factor (Divide item 11 by item 12) (Round to 4 decimal places)

14.Apportioned revenue (Multiply item 10 by item 13) (Dollars and cents)

15.Tax due before discount (Multiply item 14 by 0.00331) (Dollars and cents)

16.Discount (see instructions, applicable to report years 2008 and 2009)

17.TOTAL TAX DUE (item 15 minus item 16) (Do not include payment if this amount is less than $1,000)

13.

14.

15.

16.

17.

00

00

00

00

00

00

00

00

00

00

00

00

Do not include payment if item 17 is less than $1,000 or if annualized total revenue is less than the no tax due threshold (see instructions).

If the entity makes a tiered partnership election, ANY amount in item 17 is due. Complete Form

Print or type name |

Area code and phone number |

|||

|

|

( |

) |

- |

|

|

|

|

|

I declare that the information in this document and any attachments is true and correct to the best of my knowledge and belief. |

|

|

Mail original to: |

|

|

|

|

Texas Comptroller of Public Accounts |

|

|

Date |

|

||

|

|

|

P.O. Box 149348 |

|

|

|

|

|

|

|

|

|

|

Austin, TX |

|

|

|

|

|

Instructions for each report year are online at www.comptroller.texas.gov/taxes/franchise/forms/. If you have any questions, call

** If not 12 months, see instructions for annualized revenue.

VE/DE

PM Date

| Fact Name | Description |

|---|---|

| Form Title | This form is officially known as the Texas Franchise Tax EZ Computation Report (Form 05-169). |

| Revenue Threshold | To qualify for this form, the annualized total revenue must be $20,000,000 or less. |

| Filing Requirement | Entities must file this form if they meet the revenue threshold and other criteria outlined in the instructions. |

| Due Date | The form is typically due on May 15th of each year, unless it falls on a weekend or holiday. |

| Taxpayer Information | Taxpayer number, name, and address must be provided on the form for identification purposes. |

| Combined Reporting | Taxpayers can indicate if this is a combined report by blackening the appropriate circle on the form. |

| Revenue Reporting | Entities must report various income sources, including gross receipts, dividends, and rents, among others. |

| Apportionment Factor | The apportionment factor is calculated by dividing gross receipts in Texas by gross receipts everywhere. |

| Tax Calculation | The total tax due is calculated based on apportioned revenue and applicable rates, with specific instructions for discounts. |

| Governing Law | This form is governed by the Texas Tax Code, specifically Chapter 171 regarding franchise taxes. |

Filling out the Texas 05-169 form is an essential step for businesses seeking to report their franchise tax in Texas. The process involves providing specific financial information and ensuring that all details are accurate. Once completed, this form must be submitted to the Texas Comptroller of Public Accounts by the designated due date.

What is the Texas 05 169 form?

The Texas 05 169 form is the Franchise Tax EZ Computation Report. It is specifically designed for entities with annualized total revenue of $20,000,000 or less. This form simplifies the process of reporting franchise taxes for qualifying businesses in Texas.

Who needs to file this form?

Entities that are corporations, limited liability companies, professional associations, limited partnerships, or financial institutions must file this form if their annualized total revenue is $20,000,000 or less. If your business meets these criteria, you should consider using this form for your franchise tax reporting.

What information do I need to complete the form?

You will need various pieces of information, including:

Make sure to gather this information before you begin filling out the form to ensure a smooth process.

What if my total revenue is adjusted for a tiered partnership election?

If your entity has made a tiered partnership election, you must indicate this on the form. Regardless of the amount calculated in item 17, if you have made this election, any amount due is required to be paid. It's important to follow the specific instructions provided for tiered partnerships to ensure compliance.

Where do I send the completed form?

Once you have completed the Texas 05 169 form, mail the original to the Texas Comptroller of Public Accounts at:

P.O. Box 149348

Austin, TX 78714-9348

Make sure to check for the most current mailing address and any updates by visiting the Texas Comptroller's website.

Filling out the Texas 05-169 form can be a straightforward process, but several common mistakes often occur. One frequent error is failing to check the annualized total revenue. The form requires that the total revenue must be $20,000,000 or less. If this threshold is exceeded, individuals should not use this form. Ignoring this crucial detail can lead to complications down the line.

Another mistake involves the taxpayer number. This number must be accurately entered. Omitting it or providing an incorrect number can delay processing and lead to unnecessary confusion. It is essential to verify this information before submission.

Many people also overlook the importance of the accounting year dates. The form requires both the beginning and ending dates of the accounting year. If these dates are not filled out correctly, it can affect the calculations of revenue and tax due. Ensure that the format is consistent and clear.

Inaccurate reporting of revenue is another common pitfall. Each revenue item must be reported in whole dollars only. Entering decimal points or incorrect figures can result in errors in total revenue calculations. Double-check each line item to ensure accuracy.

Additionally, some individuals fail to blacken the appropriate circles regarding address changes or combined reports. This oversight can lead to miscommunication and potential issues with the filing. Clarity in these sections is vital.

Exclusions from gross revenue must also be reported accurately. Many filers mistakenly leave this section blank or miscalculate the exclusions. This can significantly impact the total revenue reported. Review the instructions carefully to ensure compliance.

Another frequent error is the calculation of the apportionment factor. This factor is derived by dividing gross receipts in Texas by gross receipts everywhere. Rounding to four decimal places is required, and inaccuracies here can lead to incorrect tax calculations.

Some individuals neglect to include the tax due before any discounts. This oversight can lead to confusion about the total tax liability. Ensure that all calculations are clearly noted and easy to follow.

Lastly, failing to declare the information as true and correct can result in penalties. It is crucial to sign and date the form, confirming the accuracy of the information provided. This step is not merely a formality; it is an essential part of the process.

The Texas 05-169 form, also known as the Texas Franchise Tax EZ Computation Report, is utilized by entities with annualized total revenue of $20,000,000 or less to report their franchise tax obligations. Along with this form, various other documents may be required or beneficial for comprehensive tax reporting and compliance. Below is a list of related forms and documents often used in conjunction with the Texas 05-169 form.

Understanding these documents and their purposes can aid in the accurate and timely filing of franchise tax obligations in Texas. Proper documentation is essential for compliance and to avoid potential penalties or issues with the Texas Comptroller's office.

The Texas 05-169 form is used for filing the Franchise Tax EZ Computation Report. Several other documents serve similar purposes in reporting income and tax obligations. Here are six documents that are comparable to the Texas 05-169 form:

When filling out the Texas 05-169 form, attention to detail is crucial. Here are ten important dos and don’ts to consider:

Understanding the Texas 05-169 form is crucial for businesses operating in Texas. However, several misconceptions can lead to confusion. Here are four common misconceptions:

This is incorrect. The form is specifically designed for entities with an annualized total revenue of $20,000,000 or less. If a business exceeds this threshold, it must use a different form for reporting.

Not all entities are required to file this form. Only corporations, limited liability companies, professional associations, limited partnerships, and financial institutions that meet the revenue criteria must submit it.

This is misleading. While the form provides a structure for calculating tax due, taxpayers must carefully follow the instructions to ensure accurate calculations, particularly in sections regarding total revenue and apportionment factors.

The due date can vary based on the reporting year. It is essential for taxpayers to verify the specific due date for their report year to avoid penalties.

When filling out the Texas 05-169 form, there are several important points to keep in mind. Here are four key takeaways:

By keeping these points in mind, you can ensure a smoother process when filing your Texas Franchise Tax EZ Computation Report.