The ST 101 Idaho form is a crucial document for businesses and individuals looking to claim exemptions from sales tax in Idaho. This form serves multiple purposes, primarily allowing buyers to certify that their purchases are for resale, exempt use, or fall under specific categories that qualify for tax relief. For instance, businesses purchasing goods for resale must indicate their seller's permit number, while producers can claim exemptions for items directly used in their production processes. Additionally, various organizations, including nonprofit entities and government agencies, can utilize the form to exempt all their purchases from sales tax. The ST 101 also addresses contractor exemptions, enabling construction professionals to acquire materials for projects in non-taxing states without incurring sales tax. Each section of the form requires careful completion, with specific rules governing the eligibility for exemptions. Buyers must read and sign the form, affirming the accuracy of their claims, as any false statements could lead to serious penalties. Understanding the nuances of the ST 101 Idaho form is essential for anyone involved in purchasing goods in the state, ensuring compliance while maximizing potential tax savings.

Form

Sales Tax Resale or Exemption Certificate

(Contractors improving real property, use Form

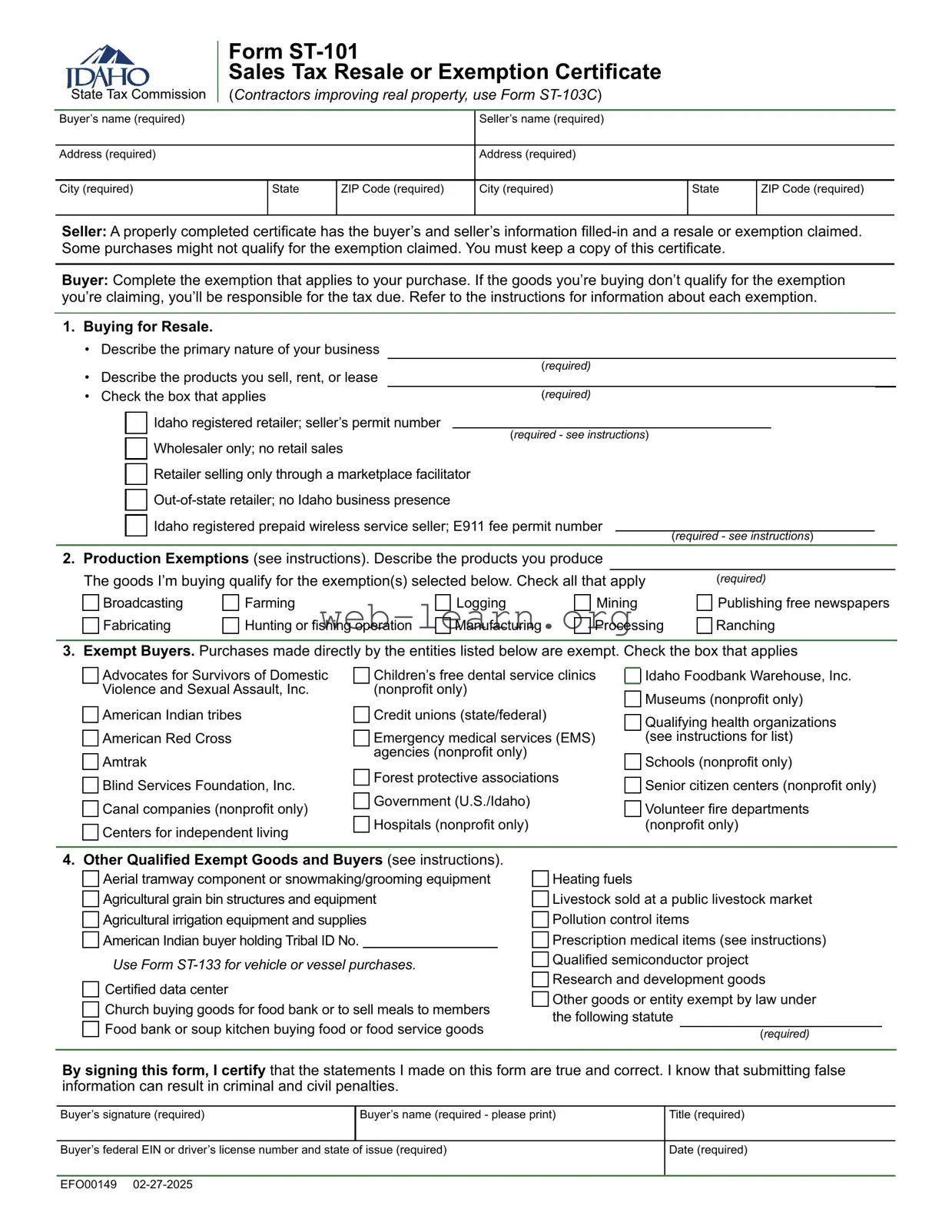

Buyer’s name (required) |

|

|

Seller’s name (required) |

|

|

|

|

|

|

|

|

Address (required) |

|

|

Address (required) |

|

|

|

|

|

|

|

|

City (required) |

State |

ZIP Code (required) |

City (required) |

State |

ZIP Code (required) |

|

|

|

|

|

|

Seller: A properly completed certificate has the buyer’s and seller’s information

Buyer: Complete the exemption that applies to your purchase. If the goods you’re buying don’t qualify for the exemption you’re claiming, you’ll be responsible for the tax due. Refer to the instructions for information about each exemption.

1. Buying for Resale.

• Describe the primary nature of your business

• Describe the products you sell, rent, or lease |

|

(required) |

|

|

|

||||

|

|

|

|

|

|||||

• Check the box that applies |

|

|

(required) |

|

|

|

|||

|

|

Idaho registered retailer; seller’s permit number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

Wholesaler only; no retail sales |

(required - see instructions) |

|

|

|

|||

|

|

|

|

|

|||||

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|||

|

|

Retailer selling only through a marketplace facilitator |

|

|

|

|

|

||

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|||

|

|

Idaho registered prepaid wireless service seller; E911 fee permit number |

|

|

|

|

|||

|

|

|

|

|

|

||||

|

|

|

(required - see instructions) |

|

|||||

|

|

|

|

|

|

|

|

||

2.Production Exemptions (see instructions). Describe the products you produce

|

|

|

|

|

|

The goods I’m buying qualify for the exemption(s) selected below. Check all that apply |

(required) |

||||

Broadcasting |

Farming |

Logging |

Mining |

Publishing free newspapers |

|

Fabricating |

Hunting or fishing operation |

Manufacturing |

Processing |

Ranching |

|

3.Exempt Buyers. Purchases made directly by the entities listed below are exempt. Check the box that applies

Advocates for Survivors of Domestic Violence and Sexual Assault, Inc.

American Indian tribes

American Red Cross

Amtrak

Blind Services Foundation, Inc.

Canal companies (nonprofit only)

Centers for independent living

Children’s free dental service clinics (nonprofit only)

Credit unions (state/federal)

Emergency medical services (EMS) agencies (nonprofit only)

Forest protective associations Government (U.S./Idaho)

Hospitals (nonprofit only)

Idaho Foodbank Warehouse, Inc.

Museums (nonprofit only)

Qualifying health organizations (see instructions for list)

Schools (nonprofit only)

Senior citizen centers (nonprofit only)

Volunteer fire departments (nonprofit only)

4.Other Qualified Exempt Goods and Buyers (see instructions). Aerial tramway component or snowmaking/grooming equipment Agricultural grain bin structures and equipment

Agricultural irrigation equipment and supplies

American Indian buyer holding Tribal ID No.

Use Form

Certified data center

Church buying goods for food bank or to sell meals to members

Food bank or soup kitchen buying food or food service goods

Heating fuels

Livestock sold at a public livestock market

Pollution control items

Prescription medical items (see instructions)

Qualified semiconductor project

Research and development goods

Other goods or entity exempt by law under the following statute

(required)

By signing this form, I certify that the statements I made on this form are true and correct. I know that submitting false information can result in criminal and civil penalties.

Buyer’s signature (required) |

Buyer’s name (required - please print) |

Title (required) |

|

|

|

Buyer’s federal EIN or driver’s license number and state of issue (required) |

Date (required) |

|

|

|

|

EFO00149 |

|

|

Form

Sales Tax Resale or Exemption Certificate

General. To be valid, the certificate must be fully completed and signed. The seller must keep the valid form on file. The seller is responsible for collecting sales tax if the form isn’t valid.

Buyer, if the goods you’re buying don’t qualify for the exemption you’re claiming, you’ll be responsible for the tax due.

Specific Instructions

Section 1 — Buying for Resale

Buyers must have an Idaho seller’s or E911 fee permit number unless they’re:

•Wholesalers making no retail sales.

•Retailers selling only through marketplace facilitators. (A marketplace facilitator is a person who provides a marketplace for

•

An Idaho seller’s or E911 fee permit number has nine digits, such as 000123456. You can validate a permit number by visiting tax.idaho.gov/validseller or contacting the Tax Commission.

Section 2 — Production Exemptions

Businesses that primarily produce goods for resale don’t need to pay tax on qualifying items they directly and primarily use in the production process. Businesses offering the right to hunt or fish as a taxable activity don’t need to pay tax on qualifying items they directly and primarily use in a hunting or fishing activity. See Idaho Code section

Loggers

Qualifying businesses must pay sales tax on the following:

•Goods that become improvements to real property (e.g., fence posts)

•Goods used in selling or distribution

•Janitorial or cleaning equipment and supplies

•Maintenance or repair equipment and supplies

•Office equipment and supplies

•Transportation equipment and supplies

•Any licensed motor vehicle, trailer, aircraft, or parts

•Recreational vehicle (e.g., snowmobile, ATV,

Seller: For production exemptions, you can stamp or imprint an exemption statement on the front of the invoice. (See Exemption Statement section below for the required elements of an exemption statement.)

Section 3 — Exempt Buyers

These buyers are exempt from tax on all purchases. See Idaho Code sections

Advocates for Survivors of Domestic Violence and Sexual Assault, Inc.

American Indian tribes. Only tribal entities qualify.

American Red Cross.

Amtrak.

Blind Services Foundation, Inc.

Canal companies. Nonprofit only.

Centers for independent living. To qualify, a center must be a private, nonprofit, nonresidential organization in which at least 51% of the board, management, and staff are persons with disabilities.

The center also must meet all these criteria:

•It’s designed and operated within a local community by individuals with disabilities.

•It provides a variety of independent living services and programs.

•It’s

Children’s free dental service clinics. Nonprofit only.

Credit unions. Both state and federal credit unions qualify. See Idaho Code section

Emergency medical service (EMS) agencies. Nonprofit only.

Forest protective associations.

Government. Only the U.S. government and Idaho state, county, city, and other political subdivisions qualify. Sales to other states and their political subdivisions are taxable.

EIN00064 |

Page 1 of 3 |

Form

Hospitals. Only licensed nonprofit hospitals qualify. Nursing homes or similar institutions don’t qualify for the hospital exemption.

Idaho Foodbank Warehouse, Inc.

Museums. Nonprofit only. A museum stores, preserves, and exhibits objects of art, history, science, or educational/cultural value on a permanent basis in a building, portion of a building, or outdoor location which provides museum services to the public on a regular basis.

Qualified health organizations:

•American Cancer Society

•American Diabetes Association

•American Heart Association

•Arc, Inc., The

•Arthritis Foundation

•Camp Rainbow Gold

•Children’s Home Society of Idaho

•Easter Seals

•Family Services Alliance of Southeast Idaho

•Idaho Association of Free and Charitable Clinics and its member clinics

•Idaho Community Action Agencies

•Idaho Cystic Fibrosis Foundation

•Idaho Diabetes Youth Programs

•Idaho Epilepsy League

•Idaho Lung Association, aka American Lung Association of Idaho

•Idaho Primary Care Association and its community health centers

•Idaho Ronald McDonald House

•Idaho Women’s and Children’s Alliance

•March of Dimes

•Mental Health Association

•Muscular Dystrophy Foundation

•National Multiple Sclerosis Society

•Rocky Mountain Kidney Association

•Special Olympics Idaho

•United Cerebral Palsy

Schools. Certain public or nonprofit schools qualify. These schools include:

•Colleges and universities

•Primary, secondary, and charter schools

Auxiliary organizations such as

Schools primarily teaching subjects like business, dance, theater arts, music, cosmetology, writing, and gymnastics don’t qualify.

Senior citizen centers. Only nonprofit community centers for senior citizens qualify.

Volunteer fire departments. Nonprofit only.

Section 4 — Other Qualified Exempt Goods

and Buyers

If buyers claim an exemption that isn’t listed on this form, they must mark the “Other” box and list the section of law that applies to the exemption. Otherwise, this certificate isn’t valid.

Aerial tramway, snowmaking/grooming equipment. The sale, storage, use, or other consumption of parts, materials, or equipment that will become a component of an aerial passenger tramway are exempt from tax.

Snowgrooming and snowmaking equipment that a downhill ski area owner or operator buys and uses to prepare

and maintain the downhill ski slopes accessed by aerial tramways is exempt. An aerial tramway includes chair lifts, gondolas,

Agricultural grain bin structures and equipment. All grain bin structures and equipment, including quality control equipment, directly and primarily used in agricultural production are exempt. See Idaho Code subsections

Agricultural irrigation equipment and supplies. All irrigation equipment and supplies used directly and primarily for agriculture are exempt. See Idaho Code section

American Indians. Sales to an enrolled American Indian tribal member are exempt if the goods are delivered on the reservation. The buyer’s Tribal Identification Number is required. For sales of vehicles or boats, use Form

Certified data centers. Only data centers certified with the Tax Commission qualify. Certified data centers can buy the following without paying sales tax:

EIN00064 |

Page 2 of 3 |

Form

•Eligible server equipment including servers, rack servers, chillers, storage devices, generators, cabling, and enabling software integral to or installed on such equipment

•New data center facilities, meaning the building or structural components of a building used primarily as a data center, including equipment, materials, and fixtures

See Idaho Code section

Churches. Churches can buy food for meals they sell to members or qualifying goods for their food bank without paying tax. See Idaho Code section

Food banks and soup kitchens. Food banks and soup kitchens can buy food or other goods used to grow, store, prepare, or serve food exempt from sales tax. The exemption doesn’t include licensed motor vehicles or trailers. See Idaho Code section

Heating fuels. Heating fuels such as wood, coal, petroleum, propane, and natural gas are exempt when purchased to heat any building, or a building under construction, or for domestic home use such as cooking or water heating. See Idaho Code section

Seller: For heating fuel, you can stamp or imprint an exemption statement on the front of the invoice. (See Exemption Statement section below for the required elements of an exemption statement.)

Sales of liquid propane in units of 15 gallons or less that are identified in the vendor’s records as cylinder sales are exempt from tax. You don’t need a Form

Livestock. Sales of cattle, sheep, mules, horses, pigs, and goats are exempt when sold at a public livestock market. Sales of other animals don’t qualify. See Idaho Code section

Pollution control items. The following items qualify: tangible personal property purchased to meet air or water quality standards of a federal or state agency; liners and reagents purchased to meet water quality standards; tangible personal property purchased to meet air or water quality standards and which become an improvement to real property of manufacturing, mining, farming or toxic waste treatment and storage businesses; and

dry transfer systems” used in the dry cleaning industry. This exemption doesn’t apply to items used in road construction, septic or sewer systems, drinking water treatment, or soil erosion prevention. Motor vehicles and buildings don’t qualify. See Idaho Code section

Prescription medical items. To qualify, the goods must

be prescribed to an individual by a licensed practitioner and be included in Idaho Code section

Qualified semiconductor projects. Applicants must

submit a qualifying project outline to the Idaho Department of Commerce. Qualifying entities can purchase materials and supplies permanently installed or placed in or on a qualifying project without paying sales tax. A qualifying project includes activities conducted in Idaho to construct, expand, or modernize a facility for fabrication, assembly, testing, advanced packaging, or research and development of semiconductors. See Idaho Code section

Research and development (R&D). Purchases of goods

that are primarily used to develop, design, manufacture, process, or fabricate a product or potential product qualify for exemption. See Idaho Code section

The Idaho National Laboratory and its contractors can claim an R&D exemption to buy goods directly and primarily used to advance scientific knowledge in areas that don’t have a commercial application. Items that will become a part of real property don’t qualify. See Idaho Code section

Exemption Statement

The required elements include the purchaser’s name, business name, address, a federal employer identification number or driver’s license number and state of issue, signature, date, and the reason for and nature of the claimed exemption.

Penalties

A penalty may be imposed for the misuse of an exemption form. If false exempt purchases are repeatedly or intentionally made, a penalty may be assessed at 5% of the sales price or $200, whichever is greater. See Idaho Code subsection

Contact us:

In the Boise area: (208)

Hearing impaired (TDD) (800)

tax.idaho.gov/contact

EIN00064 |

Page 3 of 3 |

| Fact Name | Description |

|---|---|

| Purpose of Form | The ST 101 Idaho form serves as a Sales Tax Resale or Exemption Certificate, allowing buyers to claim exemptions from sales tax on certain purchases. |

| Governing Law | This form is governed by Idaho Code § 63-3622, which outlines the conditions under which sales tax exemptions can be claimed. |

| Types of Exemptions | Exemptions can be claimed for resale, producer exemptions, and various specific buyer categories, including nonprofit organizations and government entities. |

| Seller's Permit Requirement | Buyers must have an Idaho seller's permit number to claim resale exemptions, unless they are wholesalers or out-of-state retailers making limited sales. |

| Producer Exemptions | Businesses that produce goods for resale may buy materials used directly in the production process without paying sales tax. |

| Exempt Buyers | Certain organizations, like food banks and American Indian tribes, qualify as exempt buyers and can purchase goods without incurring sales tax. |

| Contractor Exemptions | Contractors can claim exemptions for materials used in specific projects, such as agricultural irrigation or jobs in nontaxing states. |

| Validity of Form | The ST 101 form is only valid if all required information is complete and accurate. Sellers may retain this form for their records. |

Filling out the ST 101 form for Idaho is a straightforward process that requires attention to detail. This form is necessary for buyers who are claiming a sales tax exemption. Once completed, it should be provided to the seller to ensure that the correct tax treatment is applied to the transaction.

Once the ST 101 form is filled out completely, it should be submitted to the seller. The seller will keep this form on file to support the exemption claim. It is important to ensure that all information is accurate and complete, as any errors could lead to complications with tax exemptions.

What is the ST 101 Idaho form?

The ST 101 form, also known as the Sales Tax Resale or Exemption Certificate, is a document used in Idaho to claim exemptions from sales tax. It allows buyers to certify that their purchases are either for resale or for exempt uses, thereby avoiding sales tax on those transactions. This form is essential for businesses that regularly buy goods they plan to sell or use in exempt activities.

Who should use the ST 101 form?

This form is intended for various types of buyers, including:

What information is required on the ST 101 form?

When filling out the ST 101 form, buyers must provide specific information, including:

How does one qualify for a resale exemption?

To qualify for a resale exemption, the buyer must hold an Idaho seller’s permit number, unless they are a wholesaler or an out-of-state retailer making limited sales in Idaho. This permit number must be included on the form. It’s important to note that this exemption applies only to items that will be resold in the regular course of business, not to personal purchases.

What are some common exemptions listed on the ST 101 form?

Several exemptions can be claimed using the ST 101 form, including:

What should sellers do with the ST 101 form?

Sellers must retain the ST 101 form for their records, as it serves as proof that they did not collect sales tax on exempt transactions. It is crucial for sellers to ensure that the form is filled out completely and accurately. If a buyer claims an exemption incorrectly, the seller may still be liable for the sales tax.

What are the consequences of falsifying information on the ST 101 form?

Falsifying information on the ST 101 form is considered a serious offense. If a buyer knowingly provides false information to evade sales tax, they may face misdemeanor charges. Additional penalties could also apply, depending on the severity of the violation. It is essential for buyers to be truthful and accurate when completing this form to avoid legal repercussions.

Filling out the ST-101 Idaho form can seem straightforward, but many people make common mistakes that can lead to complications. One frequent error is not providing a valid Idaho seller’s permit number. This number is essential for buyers who are purchasing goods for resale. If the number is incorrect or formatted improperly, the certificate will not be valid. Buyers should ensure that their seller’s permit number follows the correct format, which includes up to nine digits followed by an “S.”

Another mistake involves failing to check the appropriate boxes that apply to their situation. The form has specific sections for different types of exemptions, such as buying for resale or claiming producer exemptions. Skipping this step can lead to confusion and potential tax liability. It’s crucial to read through the options carefully and select the one that accurately reflects the buyer's intent.

Some individuals neglect to provide detailed descriptions of the products being purchased. For instance, when claiming a producer exemption, it's necessary to list the specific products that will be used in the production process. Vague descriptions can result in the rejection of the exemption claim. Clear and concise product descriptions help streamline the process and ensure compliance.

Additionally, buyers often overlook the requirement to sign and date the form. A signature is essential, as it certifies that all information provided is accurate. Without a signature, the form is incomplete and cannot be processed. Buyers should double-check that they have signed and dated the form before submission.

Another common issue arises when buyers claim exemptions that do not apply to their situation. For example, claiming contractor exemptions requires specific conditions to be met. If the project does not qualify under the stated guidelines, the exemption claim may be invalid. Buyers must carefully review the eligibility criteria for each exemption type to avoid misunderstandings.

Some individuals mistakenly believe that all purchases made by exempt organizations are automatically exempt from sales tax. However, this is not the case. Each organization has specific categories of goods that qualify for exemption. Buyers should familiarize themselves with the rules governing their specific organization to ensure compliance and avoid unnecessary tax liabilities.

Another frequent oversight is not keeping copies of the completed form. Buyers should retain a copy for their records, as it serves as proof of the exemption claim. This can be particularly important in the event of an audit or inquiry from tax authorities.

Lastly, individuals sometimes fail to consult the instructions provided on the back of the form. These instructions contain valuable information about the exemptions and the requirements for each category. Ignoring these guidelines can lead to errors and complications in the exemption process. Taking the time to read through the instructions can save buyers from potential headaches down the line.

The ST 101 form is a critical document for businesses in Idaho, enabling buyers to claim exemptions from sales tax under specific circumstances. Alongside this form, several other documents often accompany it to facilitate various transactions and ensure compliance with state regulations. Below is a list of related forms and documents that may be utilized in conjunction with the ST 101.

These documents play a vital role in ensuring that buyers can effectively manage their tax obligations while taking advantage of available exemptions. Each form has specific requirements and uses, reflecting the diverse needs of businesses and organizations in Idaho.

When filling out the ST 101 Idaho form, it’s crucial to follow specific guidelines to ensure accuracy and compliance. Here’s a list of what you should and shouldn’t do:

Understanding the ST-101 Idaho form is essential for businesses and individuals claiming tax exemptions. However, several misconceptions can lead to confusion. Here are eight common misconceptions about the ST-101 form:

Awareness of these misconceptions can help ensure proper use of the ST-101 Idaho form and compliance with tax regulations.

When filling out and using the ST-101 Idaho form, it is essential to understand the following key points: