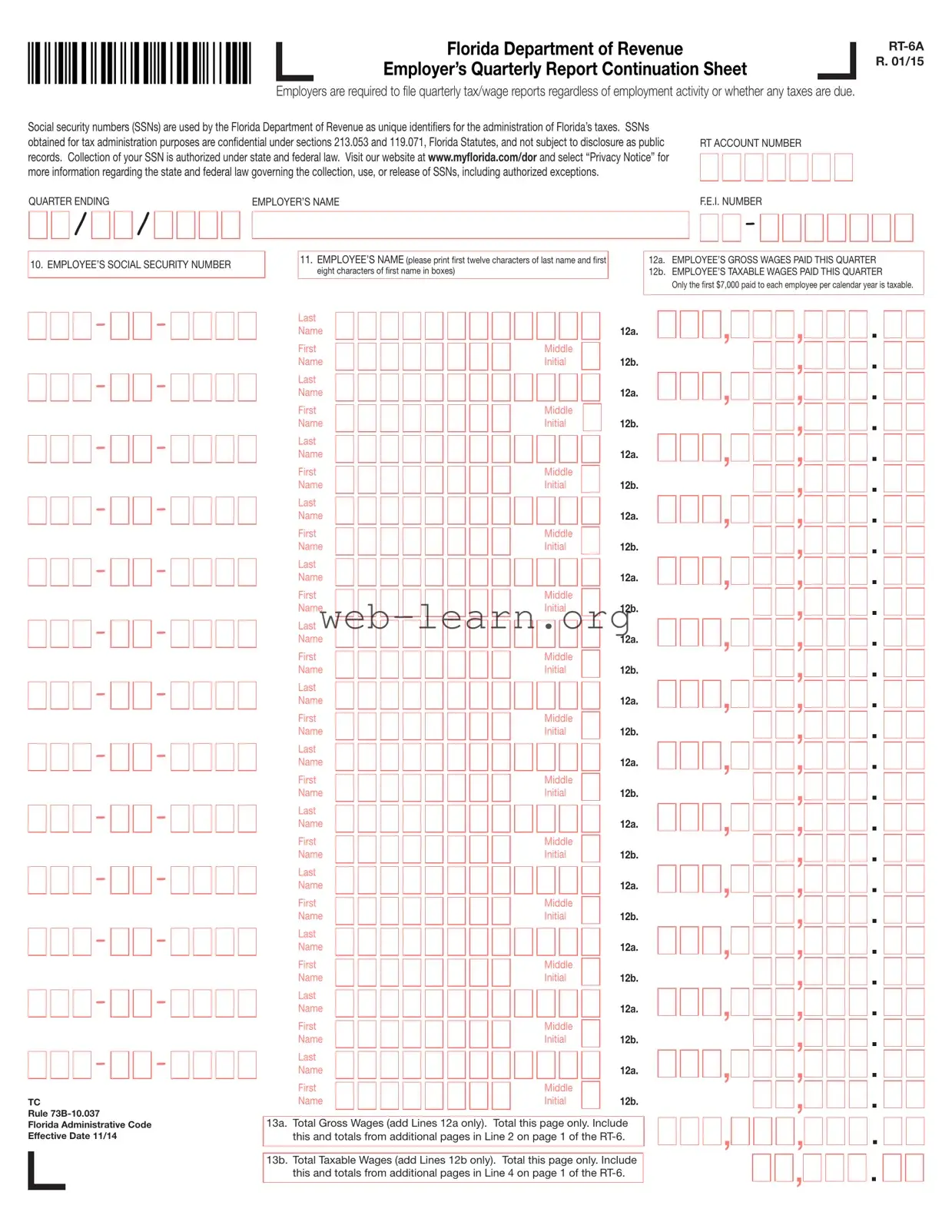

The RT-6A Florida form is an essential tool for employers in the state, designed to facilitate the reporting of wages and taxes on a quarterly basis. Regardless of whether there are employees or tax liabilities, all employers must submit this form to the Florida Department of Revenue. It acts as a continuation sheet for the Employer’s Quarterly Report, ensuring that every aspect of employment activity is documented. This form requires the inclusion of social security numbers, which serve as unique identifiers for tax administration. It's important to note that these numbers are kept confidential under Florida law, protecting them from public disclosure. Employers will need to provide details such as their account number, the quarter ending, and their Federal Employer Identification Number (FEIN). Additionally, the form collects information about each employee's gross and taxable wages, highlighting that only the first $7,000 earned by each employee in a calendar year is subject to taxation. Completing the RT-6A accurately ensures compliance with state regulations and helps maintain organized payroll records.

Florida Department of Revenue

Employer’s Quarterly Report Continuation Sheet

Employers are required to ile quarterly tax/wage reports regardless of employment activity or whether any taxes are due.

Social security numbers (SSNs) are used by the Florida Department of Revenue as unique identiiers for the administration of Florida’s taxes. SSNs

obtained for tax administration purposes are conidential under sections 213.053 and 119.071, Florida Statutes, and not subject to disclosure as public RT ACCOUNT NUMBER records. Collection of your SSN is authorized under state and federal law. Visit our website at www.mylorida.com/dor and select “Privacy Notice” for

more information regarding the state and federal law governing the collection, use, or release of SSNs, including authorized exceptions.

QUARTER ENDING |

EMPLOYER’S NAME |

F.E.I. NUMBER |

/ /

-

10. EMPLOYEE’S SOCIAL SECURITY NUMBER

- -

- -

- -

- -

- -

- -

- -

- -

- -

- -

- -

- -

- -

TC

Rule

Florida Administrative Code

Effective Date 11/14

11. EMPLOYEE’S NAME (please print irst twelve characters of last name and irst eight characters of irst name in boxes)

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

13a. Total Gross Wages (add Lines 12a only). Total this page only. Include this and totals from additional pages in Line 2 on page 1 of the

13b. Total Taxable Wages (add Lines 12b only). Total this page only. Include this and totals from additional pages in Line 4 on page 1 of the

12a. EMPLOYEE’S GROSS WAGES PAID THIS QUARTER

12b. EMPLOYEE’S TAXABLE WAGES PAID THIS QUARTER

Only the irst $7,000 paid to each employee per calendar year is taxable.

| Fact Name | Description |

|---|---|

| Quarterly Reporting Requirement | Employers must file quarterly tax and wage reports regardless of employment activity or tax liability. |

| Use of Social Security Numbers | SSNs serve as unique identifiers for tax administration and are confidential under Florida Statutes sections 213.053 and 119.071. |

| Collection Authorization | The collection of SSNs is authorized by both state and federal law for tax purposes. |

| Effective Date | The RT-6A form is governed by TC Rule 73B-10.037 of the Florida Administrative Code and became effective on November 14. |

| Taxable Wage Limit | Only the first $7,000 paid to each employee per calendar year is considered taxable wages. |

Completing the RT-6A form is essential for employers in Florida to report quarterly tax and wage information. After filling out this form, you will need to submit it along with the RT-6 form to ensure compliance with state tax regulations. Below are the steps to guide you through the process of filling out the RT-6A form accurately.

The RT-6A form is used by employers in Florida to report quarterly tax and wage information to the Florida Department of Revenue. Regardless of whether there are employees or taxes due, employers must file this report. This requirement ensures that the state can effectively manage and monitor tax compliance.

All employers in Florida must submit the RT-6A form. This includes businesses with no employees or those that did not pay any wages during the quarter. Filing is mandatory, and failure to do so can result in penalties or fines.

The Florida Department of Revenue treats social security numbers (SSNs) as confidential information. Under Florida law, specifically sections 213.053 and 119.071 of the Florida Statutes, SSNs are not subject to public disclosure. Employers can feel secure knowing that their employees’ SSNs are protected when submitted on the RT-6A form.

Employers must provide several key pieces of information on the RT-6A form, including:

It's important to accurately complete each section to ensure compliance and avoid issues with the Department of Revenue.

For the purposes of the RT-6A form, only the first $7,000 paid to each employee within a calendar year is considered taxable. This means that any wages paid beyond this limit are not subject to state unemployment tax, which can significantly impact an employer's tax liability.

When filling out the RT-6A Florida form, individuals often make several common mistakes that can lead to complications. One frequent error is the incorrect entry of social security numbers (SSNs). Each SSN must be accurate, as it serves as a unique identifier for tax purposes. A single digit mistake can cause delays in processing and may result in penalties. It is crucial to double-check each number before submission to ensure accuracy.

Another mistake people make is failing to complete all required fields. The RT-6A form has specific sections that must be filled out completely. Omitting information, such as the employer's name or FEI number, can lead to the form being returned or rejected. Individuals should review the form thoroughly and ensure that every section is completed before submitting it.

Additionally, many individuals do not calculate total gross wages and taxable wages correctly. The form requires totals from various lines, and errors in these calculations can lead to incorrect tax reporting. It is essential to carefully add the figures for each employee and verify that the totals match what is reported on the first page of the RT-6 form.

Lastly, some people overlook the importance of timely submission. Employers are required to file quarterly tax reports regardless of employment activity. Failing to submit the form on time can result in late fees or penalties. Setting reminders for due dates can help ensure that the form is submitted promptly and accurately.

The RT-6A form is an essential document for employers in Florida, facilitating the reporting of employee wages and taxes on a quarterly basis. However, it is often accompanied by other important forms that help ensure compliance with state tax laws. Below are four documents that are frequently used alongside the RT-6A form.

Understanding these forms and their interconnections can significantly streamline the reporting process for employers. By ensuring all necessary documentation is completed and submitted, businesses can maintain compliance with both state and federal tax requirements, ultimately fostering a smoother operational environment.

The RT-6A Florida form is essential for employers to report quarterly tax and wage information. Several other documents share similarities with the RT-6A, particularly in their purpose and structure. Here are seven documents that are similar:

Understanding these documents can help employers maintain compliance with tax regulations and ensure accurate reporting of employee wages.

When filling out the RT-6A Florida form, certain practices can help ensure accuracy and compliance. Below is a list of things to do and avoid.

Understanding the RT-6A Florida form is crucial for employers navigating their tax obligations. However, several misconceptions can lead to confusion. Here are ten common misunderstandings, clarified for your benefit:

By addressing these misconceptions, employers can better navigate their responsibilities and ensure compliance with Florida tax regulations. Understanding the requirements of the RT-6A form is not just beneficial; it is essential for maintaining good standing with the Florida Department of Revenue.

When filling out and using the RT-6A Florida form, consider the following key takeaways: