The Profit and Loss form, often referred to as the P&L statement, serves as a vital tool for individuals and businesses alike to assess their financial performance over a specific period. This document provides a clear overview of revenues, costs, and expenses, ultimately leading to the calculation of net profit or loss. By detailing income sources and categorizing various expenditures, the form enables users to identify trends, make informed decisions, and strategize for future growth. Additionally, it plays a critical role in financial reporting, allowing stakeholders to understand the profitability of an enterprise. Regularly updating this form can help in tracking financial health and ensuring compliance with accounting standards. Understanding its components, such as gross profit, operating expenses, and net income, is essential for anyone looking to gain insights into their financial standing.

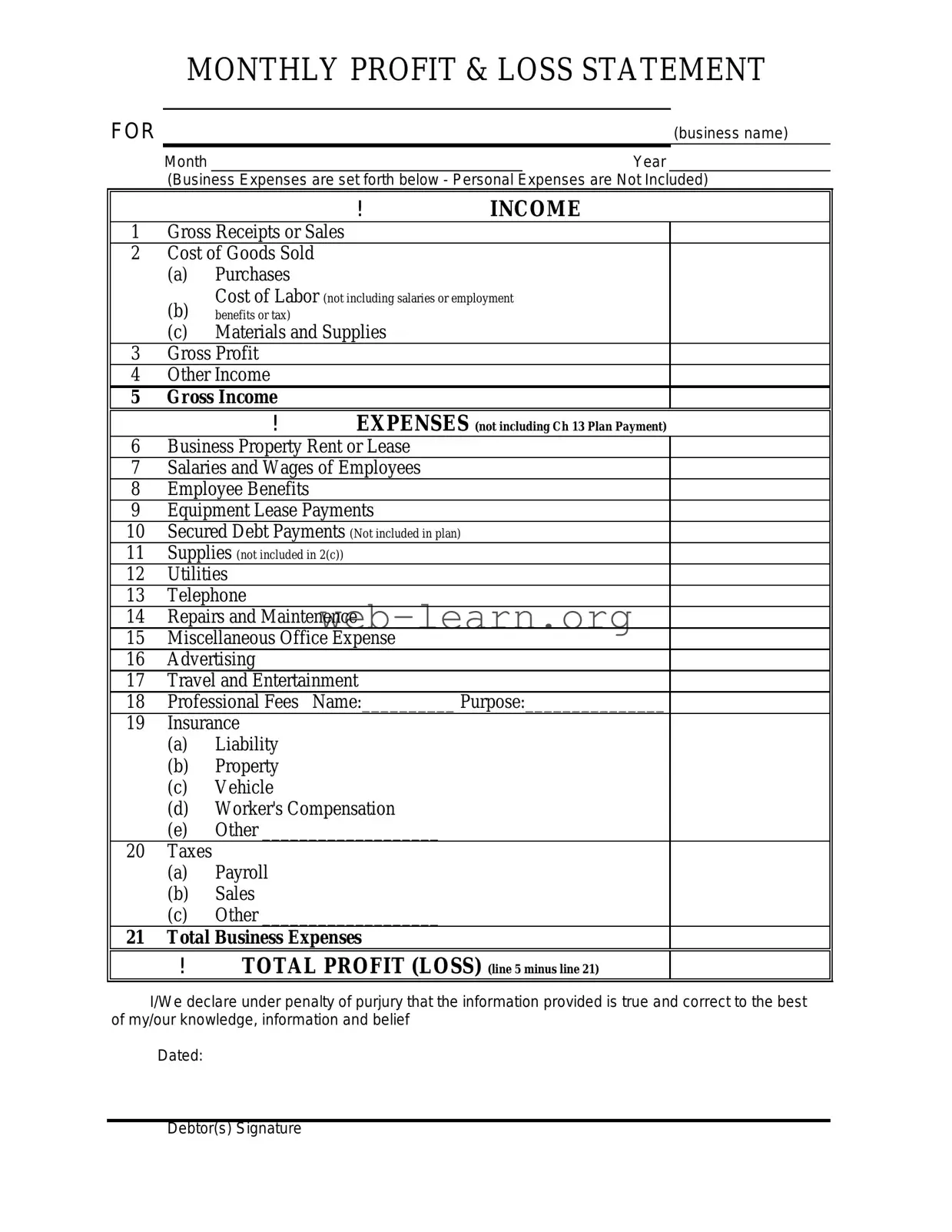

MONTHLY PROFIT & LOSS STATEMENT

FOR |

(business name) |

Month |

Year |

(Business Expenses are set forth below - Personal Expenses are Not Included)

|

|

|

! |

INCOME |

1 |

Gross Receipts or Sales |

|

||

2 |

Cost of Goods Sold |

|

||

|

(a) |

Purchases |

|

|

|

(b) |

Cost of Labor (not including salaries or employment |

||

|

benefits or tax) |

|

|

|

|

(c) |

Materials and Supplies |

|

|

3 |

Gross Profit |

|

|

|

4 |

Other Income |

|

|

|

5 |

Gross Income |

EXPENSES (not including Ch 13 Plan Payment) |

||

|

|

! |

||

6 |

Business Property Rent or Lease |

|

||

7 |

Salaries and Wages of Employees |

|

||

8 |

Employee Benefits |

|

|

|

9 |

Equipment Lease Payments |

|

||

10 |

Secured Debt Payments (Not included in plan) |

|

||

11 |

Supplies (not included in 2(c)) |

|

||

12 |

Utilities |

|

|

|

13 |

Telephone |

|

|

|

14 |

Repairs and Maintenence |

|

||

15 |

Miscellaneous Office Expense |

|

||

16 |

Advertising |

|

|

|

17 |

Travel and Entertainment |

|

||

18 |

Professional Fees |

Name:__________ Purpose:_______________ |

||

19 |

Insurance |

|

|

|

|

(a) |

Liability |

|

|

|

(b) |

Property |

|

|

|

(c) |

Vehicle |

|

|

|

(d) |

Worker's Compensation |

|

|

|

(e) |

Other ___________________ |

|

|

20 |

Taxes |

|

|

|

|

(a) |

Payroll |

|

|

|

(b) |

Sales |

|

|

|

(c) |

Other ___________________ |

|

|

21 |

Total Business Expenses |

|

||

|

! |

TOTAL PROFIT (LOSS) (line 5 minus line 21) |

||

I/We declare under penalty of purjury that the information provided is true and correct to the best of my/our knowledge, information and belief

Dated:

Debtor(s) Signature

| Fact Name | Description |

|---|---|

| Definition | The Profit and Loss form summarizes a company's revenues, costs, and expenses over a specific period. |

| Purpose | This form helps assess the financial performance of a business, indicating profitability or loss. |

| Components | Key components include total revenue, cost of goods sold, gross profit, operating expenses, and net income. |

| Frequency | Businesses typically prepare this form monthly, quarterly, or annually, depending on their reporting needs. |

| State-Specific Forms | Some states may have specific requirements for Profit and Loss forms under their tax laws, such as California Revenue and Taxation Code Section 25101. |

| Importance for Stakeholders | Investors, creditors, and management use the form to make informed decisions regarding investments and operations. |

| Comparison with Other Statements | Unlike the balance sheet, which shows a company's financial position at a specific point, the Profit and Loss form covers a period of time. |

Completing the Profit And Loss form is a critical step in understanding your financial performance. This form will guide you through the necessary sections to accurately report your income and expenses. Make sure to gather all relevant financial documents before you start.

What is a Profit and Loss form?

A Profit and Loss form, often referred to as a P&L statement, is a financial document that summarizes the revenues, costs, and expenses incurred during a specific period of time. It provides a clear picture of a business's financial performance, indicating whether it made a profit or incurred a loss. This form is essential for business owners, investors, and stakeholders to understand the overall financial health of the organization.

Why is the Profit and Loss form important?

The Profit and Loss form is crucial for several reasons:

Overall, this form plays a vital role in strategic planning and decision-making.

How often should a Profit and Loss form be prepared?

The frequency of preparing a Profit and Loss form can vary based on the needs of the business. Many companies prepare this statement monthly or quarterly to closely monitor their financial performance. Others may choose to do it annually. Regular updates allow for timely adjustments to business strategies and help identify trends over time.

What are the main components of a Profit and Loss form?

A typical Profit and Loss form includes several key components:

Understanding these components can help stakeholders make informed decisions about the business's financial strategies.

Filling out a Profit and Loss (P&L) form can be a daunting task, but avoiding common mistakes can lead to more accurate financial reporting. One frequent error is failing to keep records up to date. Many individuals neglect to record their income and expenses regularly, which can result in missing important data. This oversight can skew the overall picture of financial health.

Another mistake involves misclassifying expenses. People often group expenses incorrectly, which can lead to confusion when analyzing financial performance. For example, mixing personal and business expenses can distort the true profitability of a business. It is essential to categorize expenses accurately to ensure clarity and compliance.

Many also overlook the importance of including all sources of income. Some individuals may forget to report secondary income streams, such as freelance work or rental income. This omission can significantly impact the final profit figure, leading to an incomplete financial overview.

Additionally, not reconciling the P&L with bank statements is a common error. Failing to cross-check these documents can result in discrepancies that go unnoticed. Regular reconciliation helps catch errors early and ensures that the P&L accurately reflects the business's financial status.

Another mistake is underestimating the importance of accurate data entry. Simple typos or miscalculations can lead to significant errors in the final figures. It’s crucial to double-check entries and ensure that all calculations are correct to maintain the integrity of the financial report.

Finally, some individuals neglect to seek help when needed. If the P&L form feels overwhelming, reaching out to a financial advisor or accountant can provide valuable guidance. Seeking assistance can prevent costly mistakes and foster a better understanding of financial management.

The Profit and Loss form is an essential document for any business, providing a clear snapshot of financial performance over a specific period. However, it is often accompanied by other forms and documents that enhance its utility and provide a more comprehensive view of a company's financial health. Below are several key documents that are frequently used alongside the Profit and Loss form.

In summary, while the Profit and Loss form provides critical information about a business's financial performance, it is most effective when used in conjunction with other key documents. Together, they paint a fuller picture of a company's financial landscape, aiding in better decision-making and strategic planning.

The Profit and Loss form is an essential financial document that provides insights into a company's revenue and expenses over a specific period. Several other documents serve similar purposes in financial reporting. Here are four documents that share similarities with the Profit and Loss form:

When filling out the Profit and Loss form, accuracy and clarity are essential. Follow these guidelines to ensure your submission is correct.

By adhering to these dos and don'ts, you can ensure that your Profit and Loss form is filled out correctly and effectively communicates your financial situation.

Understanding the Profit and Loss (P&L) form is crucial for anyone involved in managing finances, whether for a business or personal use. However, several misconceptions can lead to confusion. Here are eight common misconceptions about the P&L form:

Many people think the P&L is solely about profits. In reality, it provides a complete picture of revenues, costs, and expenses, showing both profits and losses.

Some confuse the P&L with a balance sheet. While the P&L summarizes income and expenses over a period, a balance sheet provides a snapshot of assets, liabilities, and equity at a specific point in time.

Individuals and small businesses can benefit from a P&L just as much as large corporations. It helps in tracking financial health and making informed decisions.

Not all expenses shown on the P&L are deductible for tax purposes. Some costs may not qualify, and it's essential to understand which ones do.

This form is not just for accountants. Business owners, managers, and even employees can use it to understand financial performance and make strategic decisions.

The P&L does not directly show cash flow. It records revenues and expenses when they are incurred, not necessarily when cash is exchanged.

Many believe a P&L is a one-time document. In truth, it should be updated regularly to reflect ongoing financial activity and provide accurate insights.

While profit is important, other figures like gross margin and operating expenses are also critical for assessing overall financial health.

By addressing these misconceptions, individuals and businesses can better utilize the Profit and Loss form to enhance their financial understanding and decision-making.

Understanding the Profit and Loss form is essential for managing finances effectively. Here are some key takeaways to keep in mind: