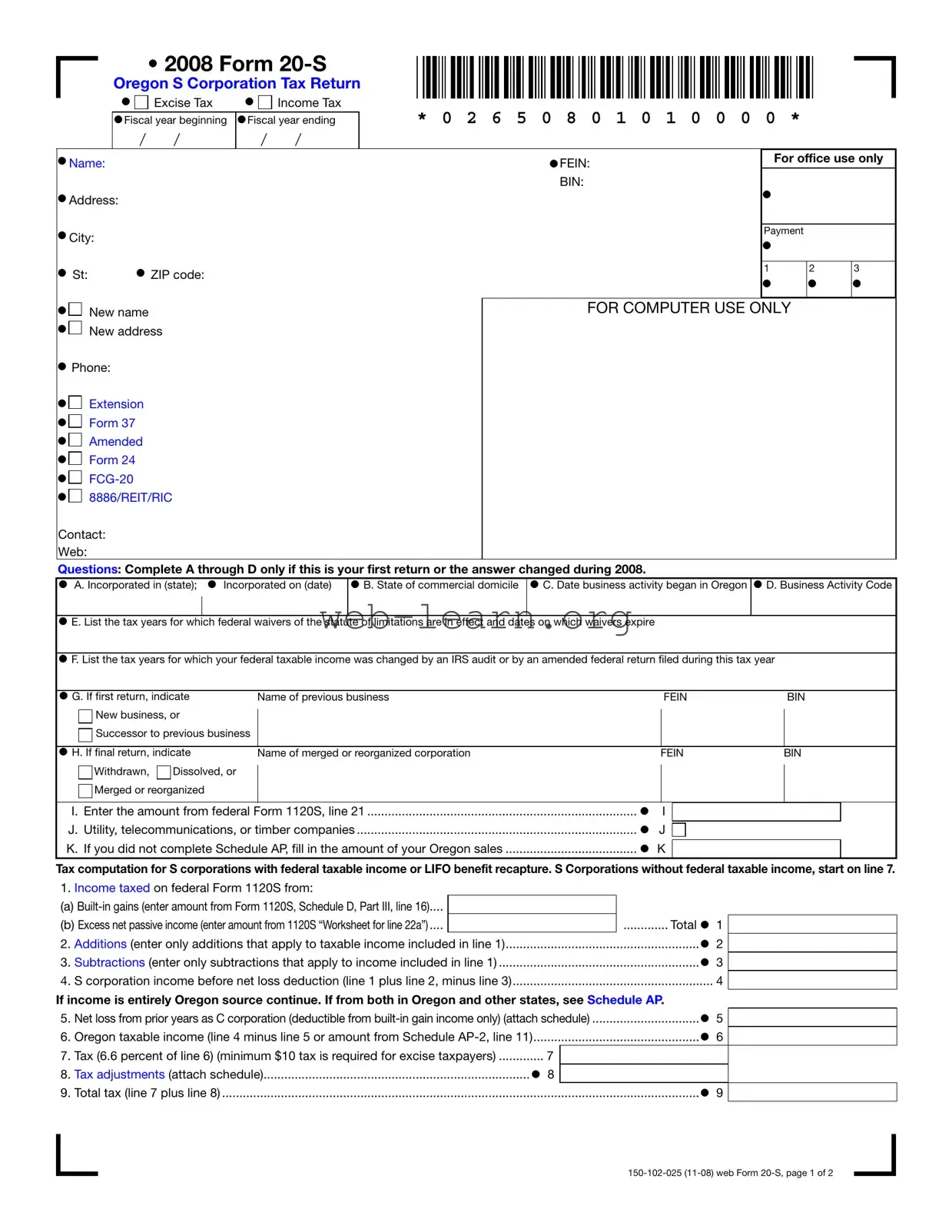

The Oregon 20 S form is an essential document for S corporations operating within the state, specifically designed to report excise and income taxes. This form captures critical information about the corporation's fiscal year, including its beginning and ending dates, name, and federal employer identification number (FEIN). It also requires the corporation to provide its commercial domicile and details regarding its business activities in Oregon. If this is the corporation's first return, the form prompts the inclusion of additional information such as the state of incorporation and the date business activities commenced. The tax computation section of the form is particularly important, detailing how to calculate Oregon taxable income, including adjustments for federal taxable income and any applicable tax credits. Furthermore, the form addresses potential overpayments and penalties, ensuring that corporations stay compliant with state tax regulations. By understanding the various components of the Oregon 20 S form, S corporations can navigate their tax obligations more effectively and avoid common pitfalls.

|

|

|

|

• 2008 Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

Oregon S Corporation Tax Return |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

• |

Excise Tax |

• |

Income Tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

* 0 2 6 5 0 8 0 1 0 1 0 0 0 0 |

* |

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

•Fiscal year beginning |

•Fiscal year ending |

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

/ |

/ |

/ |

/ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

•Name: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

•FEIN: |

|

|

For office use only |

||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||

•Address: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

BIN: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

•City: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Payment |

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

• St: |

|

|

• ZIP code: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

|

|

|

|

|

|

2 |

3 |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

|

|

• |

• |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

• |

New name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FOR COMPUTER USE ONLY |

|

|||||||||||||||||||||||||||||||||||||||||

• |

New address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

•Phone:

• Extension

• Form 37

• Amended

• Form 24

•

• 8886/REIT/RIC

Contact: |

|

|

Web: |

|

|

Questions: Complete A through D only if this is your first return or the answer changed during 2008. |

||

• A. Incorporated in (state); |

• Incorporated on (date) |

• B. State of commercial domicile • C. Date business activity began in Oregon • D. Business Activity Code |

•E. List the tax years for which federal waivers of the statute of limitations are in effect and dates on which waivers expire

•F. List the tax years for which your federal taxable income was changed by an IRS audit or by an amended federal return filed during this tax year

• G. If first return, indicate |

Name of previous business |

|

FEIN |

BIN |

|||

New business, or |

|

|

|

|

|

|

|

Successor to previous business |

|

|

|

|

|

|

|

• H. If final return, indicate |

|

|

|

|

|

|

|

Name of merged or reorganized corporation |

|

FEIN |

BIN |

||||

Withdrawn, |

Dissolved, or |

|

|

|

|

|

|

Merged or reorganized |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I. Enter the amount from federal Form 1120S, line 21 |

• I |

|

|

|

|||

J. Utility, telecommunications, or timber companies |

• J |

|

|

|

|||

|

|

|

|||||

......................................K. If you did not complete Schedule AP, fill in the amount of your Oregon sales |

• K |

|

|

|

|||

Tax computation for S corporations with federal taxable income or LIFO benefit recapture. S Corporations without federal taxable income, start on line 7.

1.Income taxed on federal Form 1120S from:

(a) |

|

|

(b) Excess net passive income (enter amount from 1120S “Worksheet for line 22a”) .... |

............. Total • 1 |

|

2. |

Additions (enter only additions that apply to taxable income included in line 1) |

• 2 |

3. |

Subtractions (enter only subtractions that apply to income included in line 1) |

• 3 |

4. |

S corporation income before net loss deduction (line 1 plus line 2, minus line 3) |

4 |

If income is entirely Oregon source continue. If from both in Oregon and other states, see Schedule AP.

5. |

Net loss from prior years as C corporation (deductible from |

• 5 |

|

|||

|

||||||

6. |

................................................Oregon taxable income (line 4 minus line 5 or amount from Schedule |

|

• 6 |

|

||

7. |

Tax (6.6 percent of line 6) (minimum $10 tax is required for excise taxpayers) |

.............• |

7 |

|

|

|

8. |

Tax adjustments (attach schedule) |

8 |

|

|

|

|

9. |

Total tax (line 7 plus line 8) |

|

|

• 9 |

|

|

|

* |

0 |

2 |

6 |

5 |

0 |

8 |

0 |

1 |

0 |

2 |

0 |

0 |

0 |

0 |

* |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10. |

Total credits (attach schedule and explanation) |

|

|

|

|

|

|

|

|

|

• 10 |

|

|

|

||

11. |

Tax after credits (line 9 minus line 10) (excise tax not less than minimum tax) |

.................................. |

|

|

|

11 |

|

|

|

|||||||

12. |

LIFO benefit recapture addition |

|

|

|

|

|

|

|

|

|

• 12 |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|||||

13. |

Net tax (line 11 plus line 12) (excise tax not less than minimum tax) |

|

|

|

|

|

• 13 |

|

|

|

||||||

|

|

|

|

|

|

|

|

|||||||||

14. |

2008 estimated tax payments from Schedule ES below. Include payments made with extension |

• 14 |

|

|

|

|||||||||||

|

|

|

||||||||||||||

15. |

Tax due. Is line 13 more than line 14? If so, line 13 minus line 14 |

|

|

|

|

Tax due• 15 |

|

|

|

|||||||

................................... |

|

|

|

|

|

|

||||||||||

16. |

Overpayment. Is line 13 less than line 14? If so, line 14 minus line 13 |

|

|

Overpayment• 16 |

|

|

|

|||||||||

|

|

|

|

|

||||||||||||

17. |

Penalty due with this return |

|

|

|

17 |

|

|

|

|

|

|

|

|

|

|

|

18. |

Interest due with this return |

|

|

|

18 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

19. |

Interest on underpayment of estimated tax (attach Form 37) |

|

• 19 |

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|||||||

20. |

Total penalty and interest (add lines 17 through 19) |

|

|

|

|

|

|

|

|

|

20 |

|

|

|

||

21. |

Total due (line 15 plus line 20) |

|

|

|

|

|

|

|

Total due |

21 |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|||||||

22. |

Refund available (line 16 minus line 20) |

|

|

|

|

|

|

|

|

Refund |

22 |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||||||

23. |

Amount of refund to be credited to 2009 estimated tax |

|

|

|

|

|

|

2009 credit• 23 |

|

|

|

|||||

|

|

|

|

|

|

|

|

|||||||||

24. |

Net refund (line 22 minus line 23) |

|

|

|

|

|

|

|

Net refund |

24 |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Schedule

Federal taxable income passed through to the shareholders is adjusted to the extent that items of income, loss, or deduction of the shareholder are required to be adjusted under the provisions of Oregon Revised Statutes, Chapters 314 and 316. Indicate which federal Schedule

Additions |

1. |

Interest on government bonds of other states |

1 |

|

|

|

|

|

|

|

|||||

|

|

|

2. |

Gain or loss on the sale of depreciable property |

2 |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

3. |

Other (attach schedule) |

|

|

3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4. |

Total Oregon additions |

|

|

|

|

|

|

|

4 |

|

||

Subtractions |

5. |

Interest from U.S. government, such as Series EE and HH bonds |

5 |

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|||||||||

|

|

|

6. |

Gain or loss on the sale of depreciable property |

6 |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

7. |

Work opportunity credit wage reductions |

7 |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

8. |

Other (attach schedule) |

|

|

8 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9. |

Total Oregon subtractions |

|

|

|

|

|

|

|

9 |

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

Schedule |

|

|

|

|||||||

|

|

|

|

|

Name of payer |

Payer FEIN |

|

|

|

Date of payment |

|

|

Amount paid |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1. |

Voucher 1 |

|

|

|

|

|

|

|

|

/ |

/ |

|

1 |

|

|

2. |

Voucher 2 |

|

|

|

|

|

|

|

|

/ |

/ |

|

2 |

|

|

3. |

Voucher 3 |

|

|

|

|

|

|

|

|

/ |

/ |

|

3 |

|

|

4. |

Voucher 4 |

|

|

|

|

|

|

|

|

/ |

/ |

|

4 |

|

|

5. |

Overpayment of last year’s tax elected as a credit against this year’s tax |

|

|

|

|

|

5 |

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

6. |

........Payments made with extension or other prepayments for this tax year and date paid |

|

/ |

/ |

|

6 |

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

7. |

Total prepayments (carry to line 14 above) |

|

|

|

|

|

|

|

|

7 |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|||||||||||

Under penalty of false swearing, I declare that the information in this return and any attachments is true, correct, and complete. |

|||||||||||||||

|

|

Signature of officer |

|

Signature of preparer other than taxpayer |

License number of preparer |

||||||||||

Sign |

X |

|

|

|

|

X |

|

|

|

|

|

• |

|||

Here |

|

|

|

|

|

|

|

|

|

||||||

|

|

Date |

|

|

|

|

Date |

|

|

|

|

Telephone number |

|||

|

|

|

|

|

|

|

|

|

|

|

|

( |

) |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

Print name of officer |

|

Print name of preparer |

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

Title of officer |

|

|

Address of preparer |

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Please attach a complete copy of your federal Form 1120S and schedules, including all

Mail refund returns and no tax due returns to: Mail

| Fact Name | Details |

|---|---|

| Form Title | 2008 Form 20-S Oregon S Corporation Tax Return |

| Tax Types | Excise Tax and Income Tax |

| Fiscal Year | Requires the fiscal year beginning and ending dates |

| Identification | Requires the corporation's Name, FEIN, Address, and BIN |

| First Return Requirements | Complete sections A through D if this is the first return |

| Oregon Taxable Income Calculation | Includes additions and subtractions to federal taxable income |

| Minimum Tax | Excise taxpayers must pay a minimum tax of $10 |

| Estimated Payments | Requires reporting of estimated tax payments made |

| Governing Law | Oregon Revised Statutes, Chapters 314 and 316 |

Filling out the Oregon 20 S form is an important step for S Corporations in Oregon. After completing the form, you will need to submit it along with any required attachments to the appropriate state department. Make sure to double-check all information for accuracy before sending it off.

What is the Oregon 20 S form?

The Oregon 20 S form is the tax return specifically designed for S corporations operating in Oregon. This form is used to report the corporation's excise and income tax obligations to the state. It is essential for S corporations to file this form annually to comply with state tax laws and to ensure that all taxable income is accurately reported.

Who needs to file the Oregon 20 S form?

Any corporation that has elected to be treated as an S corporation for federal tax purposes and conducts business in Oregon is required to file the Oregon 20 S form. This includes corporations that have income sourced from Oregon as well as those that may have business activities in the state. If your corporation meets these criteria, it is important to file the form to avoid penalties.

What information is required to complete the Oregon 20 S form?

To complete the Oregon 20 S form, you will need various pieces of information, including:

Gathering this information beforehand will streamline the filing process.

What are the penalties for not filing the Oregon 20 S form?

Failing to file the Oregon 20 S form can result in significant penalties. The state may impose fines for late filings, which can accumulate over time. Additionally, interest may be charged on any unpaid taxes. It is crucial to file the form on time to avoid these financial repercussions and maintain compliance with Oregon tax laws.

How can I get assistance with the Oregon 20 S form?

If you need help with the Oregon 20 S form, there are several resources available. You can contact the Oregon Department of Revenue directly for guidance. Additionally, consulting a tax professional who specializes in corporate taxation can provide personalized assistance. They can help ensure that your form is completed accurately and filed on time, thus easing the stress of the tax process.

Filling out the Oregon 20 S form can be a straightforward process, but there are common mistakes that many individuals make. Understanding these pitfalls can save you time and potential headaches down the road. Here are eight mistakes to avoid.

One frequent error is neglecting to provide complete and accurate information in the name and address sections. Ensure that the name of the corporation matches exactly with the records from the IRS. Missing or incorrect details can lead to processing delays or even rejection of your return. Always double-check for typos in the address, including the ZIP code.

Another common mistake is failing to indicate the correct fiscal year. The form requires you to specify the beginning and ending dates of your fiscal year. If these dates are incorrect, it could complicate your tax calculations and compliance. Make sure that the dates align with your accounting records.

Many filers also overlook the importance of completing all required sections. For instance, if this is your first return, you must fill out sections A through D. Skipping these sections can lead to unnecessary questions from the tax authorities and may delay your filing process.

Not attaching necessary schedules can be another stumbling block. For example, if you have tax credits or adjustments, you need to include the relevant schedules. Failing to do so can result in miscalculations and potential penalties.

Additionally, some individuals mistakenly miscalculate their Oregon taxable income. Carefully follow the instructions for additions and subtractions, as errors in these calculations can significantly impact your tax liability. Always cross-reference your calculations with your federal Form 1120S.

Another mistake is not signing the form. A signature is a critical part of the submission process. Without it, your return may be deemed incomplete. Ensure that both the officer and the preparer sign the form where required.

It's also essential to remember that any estimated tax payments must be accurately reported. Some filers forget to include these payments, which can lead to an unexpected balance due. Keep a record of all payments made and ensure they are accurately reflected on the form.

Lastly, failing to mail your return to the correct address can cause delays in processing. Be sure to review the mailing instructions carefully. Depending on whether you are due a refund or have a payment to make, the addresses differ. Sending your return to the wrong location can slow down the processing time significantly.

By avoiding these common mistakes, you can ensure a smoother experience when filing your Oregon 20 S form. Taking the time to review your submission can save you from potential issues and ensure compliance with state tax regulations.

The Oregon 20 S form is a crucial document for S corporations operating in Oregon, but it is often accompanied by several other forms and documents that provide additional information or fulfill specific requirements. Here is a list of common forms that may be used alongside the Oregon 20 S form.

Each of these forms serves a specific purpose and helps ensure compliance with both state and federal tax laws. When filing the Oregon 20 S form, it's important to consider these additional documents to provide a complete and accurate tax return.

The Oregon 20 S form is a specific tax return for S corporations in Oregon. It shares similarities with several other important tax documents. Here’s a list of those documents and how they relate to the Oregon 20 S form:

Understanding these similarities can help clarify the purpose and requirements of the Oregon 20 S form. Each document serves a specific function but shares the common goal of ensuring compliance with tax obligations.

When filling out the Oregon 20 S form, there are important steps to follow. Here’s a list of things you should and shouldn't do:

Misconception 1: The Oregon 20 S form is only for large corporations.

This form is applicable to all S corporations operating in Oregon, regardless of their size. Small businesses also need to file this form if they meet the criteria for S corporation status.

Misconception 2: Filing the Oregon 20 S form is optional for S corporations.

Filing this form is mandatory for S corporations doing business in Oregon. Failure to file can result in penalties and interest on any owed taxes.

Misconception 3: The Oregon 20 S form is the same as the federal Form 1120S.

While both forms are related to S corporations, they serve different purposes and are required by different jurisdictions. The Oregon 20 S form specifically addresses Oregon's excise and income tax obligations.

Misconception 4: Only corporations with profits need to file the Oregon 20 S form.

Even S corporations that incur losses must file the Oregon 20 S form. The form captures all income and losses, which can affect shareholders' tax situations.

Misconception 5: The Oregon 20 S form can be filed without any supporting documents.

Supporting documents, such as a complete copy of federal Form 1120S and any relevant schedules, must be attached to the Oregon 20 S form upon submission.

Misconception 6: The due date for the Oregon 20 S form is the same as the federal tax return.

The due date for the Oregon 20 S form may differ from the federal return due date. Corporations should verify the specific filing deadlines to ensure compliance.

Ensure all information is accurate and complete. This includes your name, address, and Federal Employer Identification Number (FEIN). Inaccuracies can lead to delays or issues with your tax return.

Understand the purpose of the form. The Oregon 20 S form is primarily for S Corporations to report excise and income tax. Familiarize yourself with the sections to know what information is needed.

Pay attention to deadlines. Submitting the form on time is crucial to avoid penalties. Mark your calendar with the due dates to keep your business compliant.

Review the tax computation carefully. Calculate your Oregon taxable income accurately to ensure that you are paying the correct amount. Miscalculations can lead to underpayment or overpayment.

Attach necessary documentation. Include a complete copy of your federal Form 1120S and any relevant schedules. Missing documents can delay processing and refunds.