The New York Loan Agreement form is a critical tool used in the process of borrowing and lending money within the state. It outlines the terms of the loan, including the principal amount, interest rate, repayment schedule, and any applicable fees. A well-drafted loan agreement ensures that both parties understand their rights and obligations. It often includes clauses addressing default, collateral, and dispute resolution, which provide added security and clarity. Parties involved in a loan transaction must pay attention to various important details, such as the duration of the loan and the implications of late payments. Signing this document signifies the mutual intent to adhere to the agreed-upon terms, making it an essential aspect of personal and commercial finance in New York. Understanding how to properly complete and execute this form can significantly reduce the potential for misunderstandings in the future.

New York Loan Agreement Template

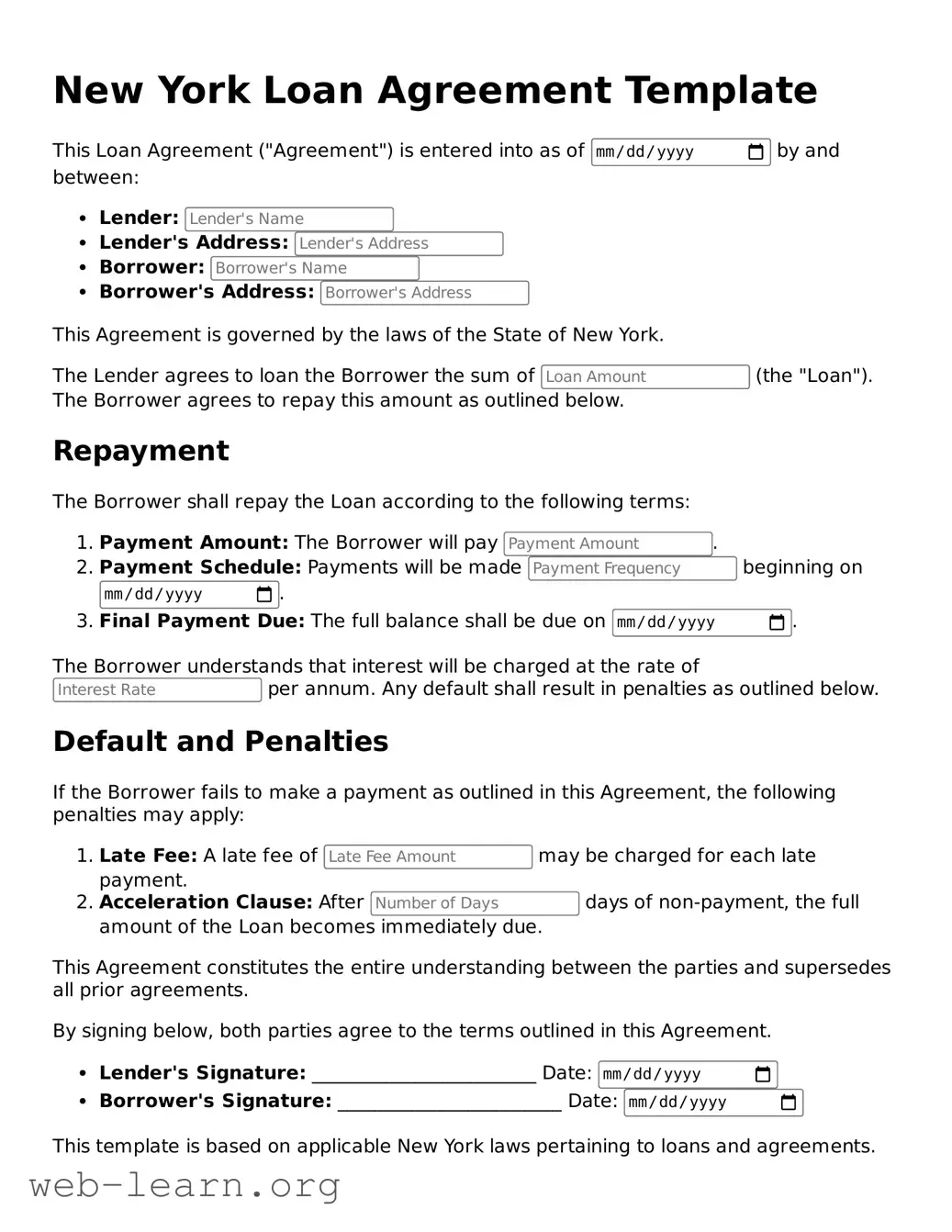

This Loan Agreement ("Agreement") is entered into as of by and between:

This Agreement is governed by the laws of the State of New York.

The Lender agrees to loan the Borrower the sum of (the "Loan"). The Borrower agrees to repay this amount as outlined below.

Repayment

The Borrower shall repay the Loan according to the following terms:

The Borrower understands that interest will be charged at the rate of per annum. Any default shall result in penalties as outlined below.

Default and Penalties

If the Borrower fails to make a payment as outlined in this Agreement, the following penalties may apply:

This Agreement constitutes the entire understanding between the parties and supersedes all prior agreements.

By signing below, both parties agree to the terms outlined in this Agreement.

This template is based on applicable New York laws pertaining to loans and agreements.

| Fact Name | Description |

|---|---|

| Document Purpose | The New York Loan Agreement form is used to outline the terms of a loan between a lender and a borrower. |

| Governing Law | This agreement is governed by New York State law, specifically the Uniform Commercial Code (UCC) as it pertains to secured transactions. |

| Key Components | It typically includes details such as loan amount, interest rate, repayment schedule, and consequences of default. |

| Parties Involved | The document identifies the lender and borrower, providing their full names and contact information. |

| Interest Rates | New York allows specific rates for loans, which must comply with state usury laws; interest rates need to be clearly stated. |

| Repayment Terms | The agreement specifies when payments are due and the total duration of the loan, helping both parties understand their obligations. |

| Default Clauses | Provisions are included to outline the actions taken if the borrower fails to make payments as agreed. |

| Security Interests | If applicable, the form can detail any collateral securing the loan, ensuring the lender’s interests are protected. |

| Signatures | Both parties must sign the agreement, indicating their acceptance of the loan terms and showing evidence of consent. |

As you prepare to fill out the New York Loan Agreement form, it's important to gather all necessary information and documents to ensure accuracy. This process will set the framework for your loan details, ensuring that necessary information is precisely indicated for all parties involved. Below are the steps you should follow when completing the form.

Completing these steps accurately will help ensure that your loan agreement is valid and enforceable. Remember, clarity in each detail fosters better communication between parties, reducing confusion and misunderstanding as the loan proceeds.

What is a New York Loan Agreement form?

The New York Loan Agreement form is a legal document designed to outline the terms and conditions under which a loan is made between a lender and a borrower. This form serves to protect both parties by clearly detailing aspects such as the loan amount, interest rate, repayment schedule, and any collateral involved.

What essential elements are included in the agreement?

Key components of the New York Loan Agreement form include:

How is interest typically calculated?

Interest on loans can be calculated in various ways, often depending on the agreement reached by both the borrower and lender. Common methods include simple interest, which is calculated only on the principal amount, and compound interest, which can accumulate on both the principal and previously accrued interest. It's crucial for both parties to find terms that are mutually agreeable and clearly document this in the agreement.

Can the loan agreement be modified after it is signed?

Yes, a loan agreement can be amended after it has been signed, but both parties must agree to the changes. Any modifications should be documented in writing and signed by both the lender and the borrower. This ensures that all parties are aware of the updated terms and helps prevent disputes later on.

What happens if the borrower defaults on the loan?

If a borrower defaults, meaning they fail to meet the terms of the loan (such as missing payments), the lender has several options. These can include charging late fees, requiring immediate repayment of the remaining loan balance, or taking possession of any collateral listed in the agreement. Default provisions in the loan agreement should clearly outline the consequences, so both parties understand their rights and obligations.

Is a witness or notarization required for a New York Loan Agreement?

While not strictly required, having a witness or notarization can add an extra layer of security to the loan agreement. It can confirm the identities of the parties involved and their understanding of the document when signed. Adding a witness or opting for notarization is often viewed as a best practice, even if it’s not legally mandated.

Where can I find a template for the New York Loan Agreement form?

Templates for the New York Loan Agreement form are widely available online, often provided by legal service websites or financial institutions. However, it is advisable to review any template carefully or consult with a legal professional. Personal circumstances can greatly influence the most suitable terms, leading to the need for specific adjustments to the standard language.

Filling out a loan agreement form can be a straightforward process, but many individuals make errors that may lead to complications. One common mistake is skipping required fields. Each section of the New York Loan Agreement is designed to capture essential information. By overlooking areas such as the borrower's name, loan amount, or interest rate, individuals risk invalidating the entire agreement. Attention to detail is critical, as lenders rely on comprehensive information to assess risk and finalize terms.

Another frequent error involves incorrect calculations. Borrowers often miscalculate interest or fail to consider additional fees. This can lead to misunderstandings about repayment amounts. Accurately documenting the principal loan amount and understanding how interest accrues over time will ensure clarity and prevent future disputes. Simple arithmetic mistakes can have significant financial implications.

Misunderstanding loan terms presents a third mistake. Borrowers may not fully grasp the implications of specific contract clauses. For instance, terms related to late payment penalties, prepayment options, or default consequences can vary widely. Without a clear understanding, individuals might inadvertently agree to conditions that are unfavorable or unrealistic for their financial situation. Engaging with these terms helps borrowers navigate their rights and responsibilities more effectively.

Lastly, failing to properly sign and date the agreement can render the document unenforceable. Even if all information is accurately filled out, a missing signature or date could delay loan processing or affect the legal standing of the agreement. It is vital to carefully review the document and ensure that all necessary signatures are provided before submission.

When entering into a loan agreement in New York, several related documents can enhance the transaction's clarity and protection for all parties involved. Below is a list of important forms and documents typically used alongside a New York Loan Agreement. Understanding these documents can help borrowers and lenders ensure that their rights and responsibilities are clearly defined.

These documents help establish a clear framework for the loan transaction. By working with these forms, borrowers and lenders can create a more secure and transparent lending process.

When filling out the New York Loan Agreement form, attention to detail is crucial. Here are ten tips to guide you through the process:

Many people believe that a loan agreement must always be lengthy and complicated. In fact, while some loan agreements can be quite detailed, the New York Loan Agreement form can vary in complexity based on the parties involved and the type of loan. Simpler agreements can be just as effective.

This is not true. Parties often have the ability to negotiate changes to a loan agreement after it has been signed. However, any modifications should be documented in writing and signed by all parties to ensure clarity and enforceability.

While legal assistance is beneficial, particularly for complex deals, individuals can use the New York Loan Agreement form without a lawyer. It's essential, however, to understand the terms to avoid pitfalls.

Many people think that loan agreements are only for significant loans. In reality, documenting even smaller loans can protect all parties involved. This clarity helps prevent misunderstandings down the line.

Not all loan agreements require notarization. While notarizing a document adds another layer of verification, many agreements, especially between private individuals, are still legally binding without being notarized, provided they meet certain criteria.

Many believe that after signing, nothing more is needed. However, parties should actively monitor the terms of the agreement throughout the loan period. Communication regarding repayment schedules and any necessary adjustments is crucial for a smooth experience.

When filling out and using the New York Loan Agreement form, there are several key considerations that borrowers and lenders should keep in mind.

California Promissory Note Template - Increasing financial literacy can empower borrowers to negotiate better terms.

Promissory Note Template Florida - It may outline the consequences of bankruptcy on the loan's repayment terms.

Free Promissory Note Template Georgia - It might require disclosures about the borrower's financial status.