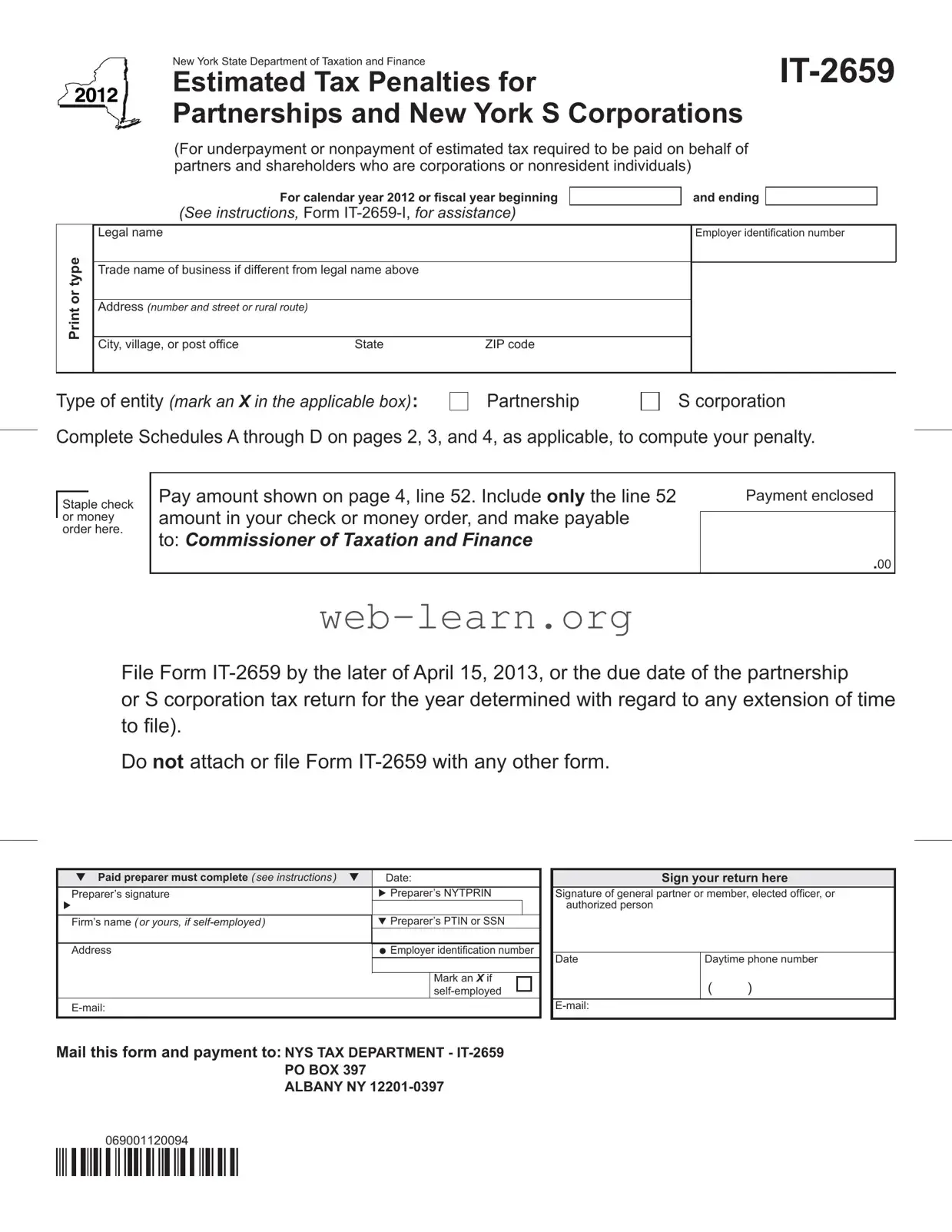

The New York IT-2659 form is essential for partnerships and New York S corporations that need to report estimated tax penalties for underpayment or nonpayment of taxes owed on behalf of their partners and shareholders. This form specifically addresses the obligations of these entities when it comes to estimated tax payments required for nonresident individuals and corporations. When filling out the IT-2659, filers must provide their legal name, trade name, and address, along with their employer identification number. The form includes several schedules that guide the user through the computation of any penalties incurred due to underpayment. Schedule A allows for the detailed calculation of estimated tax underpayment, while Schedule B offers a simplified method for computing penalties. If necessary, Schedule C provides a more comprehensive approach to assess penalties based on specific payment due dates. Filers must ensure they submit the form by the due date, which is typically April 15 of the following year, or the deadline for the partnership or S corporation tax return. It is important to pay careful attention to the instructions provided, as they help clarify the requirements and ensure compliance with New York State tax regulations.

New York State Department of Taxation and Finance |

|

||||

Estimated Tax Penalties for |

|

||||

|

|

|

|||

Partnerships and New York S Corporations |

|||||

(For underpayment or nonpayment of estimated tax required to be paid on behalf of |

|||||

partners and shareholders who are corporations or nonresident individuals) |

|

|

|

||

|

|

|

|

|

|

For calendar year 2012 or iscal year beginning |

|

|

and ending |

|

|

(See instructions, Form IT‑2659‑I, for assistance) |

|

|

|

|

|

|

|

|

|

||

Print or type

Legal name

Trade name of business if different from legal name above

Address (number and street or rural route)

City, village, or post ofice |

State |

ZIP code |

Employer identiication number

Type of entity (mark an X in the applicable box):

Partnership

S corporation

Complete Schedules A through D on pages 2, 3, and 4, as applicable, to compute your penalty.

Staple check or money order here.

Pay amount shown on page 4, line 52. Include only the line 52

amount in your check or money order, and make payable to: COMMISSIONER OF TAXATION AND FINANCE

Payment enclosed

.00

File Form IT‑2659 by the later of April 15, 2013, or the due date of the partnership

or S corporation tax return for the year determined with regard to any extension of time to ile).

Do not attach or ile Form IT‑2659 with any other form.

Paid preparer must complete (see instructions) |

Date: |

||

Preparer’s signature |

Preparer’s NYTPRIN |

||

|

|

|

|

|

|

|

|

Firm’s name (or yours, if |

Preparer’s PTIN or SSN |

|

|

|

|

|

|

Address |

Employer identiication number |

||

|

|

|

|

|

|

Mark an X if |

|

|

|

self‑employed |

|

E‑mail: |

|

|

|

Mail this form and payment to: NYS TAX DEPARTMENT -

ALBANY NY

Sign your return here

Signature of general partner or member, elected oficer, or authorized person

Date |

Daytime phone number |

( )

E‑mail:

069001120094

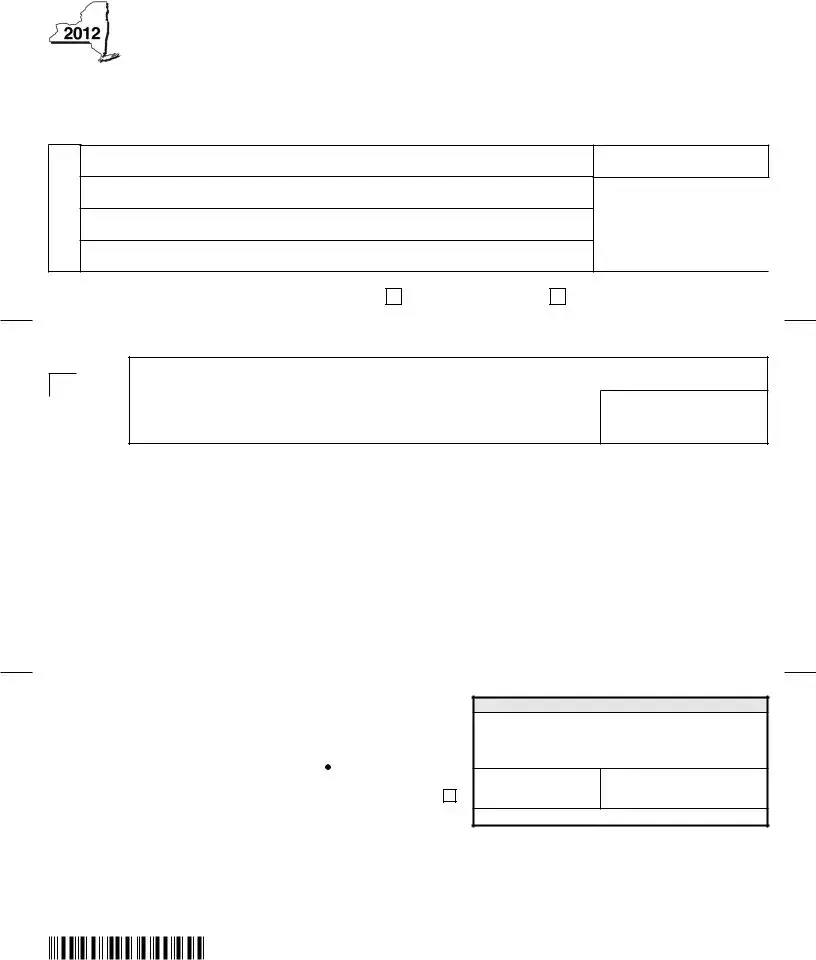

Page 2 of 4

Schedule A – Computation of estimated tax underpayment (if any). All ilers must complete this part. Only include partners and shareholders who are subject to estimated tax paid on their behalf by the partnership or New York S corporation (see instructions).

Current year

1Total of all nonresident individual partners’ or shareholders’ distributive

|

or pro rata shares of 2012 income earned from New York sources.... |

1 |

|

.00 |

|

|

2 |

Total of all nonresident individual partners’ or shareholders’ shares of |

|

|

|

|

|

|

2012 partnership deductions allocated to New York (see instructions) |

2 |

|

.00 |

|

|

3 |

Subtract line 2 from line 1 |

3 |

|

.00 |

|

|

4 |

Individual tax rate (8.82%) |

4 |

|

.0882 |

|

|

5 |

Multiply line 3 by line 4 |

5 |

|

.00 |

|

|

6 |

Total of all nonresident individual partners’ or shareholders’ distributive |

|

|

|

|

|

|

or pro rata shares of 2012 partnership or S corporation credits |

6 |

|

.00 |

|

|

7 |

2012 estimated tax required to be paid on behalf of nonresident individuals (subtract line 6 from line 5) |

............. 7 |

||||

8 |

Total of all corporate partners’ distributive shares of 2012 income earned from NY sources |

8 |

|

.00 |

|

|

9 |

Corporation tax rate (7.1%) |

9 |

|

.071 |

|

|

10 |

Multiply line 8 by line 9 |

10 |

|

.00 |

|

|

11 |

Total of all corporate partners’ distributive shares of 2012 partnership credits |

11 |

|

.00 |

|

|

12 |

2012 estimated tax required to be paid on behalf of corporations (subtract line 11 from line 10) |

|

12 |

|||

13 |

Total estimated tax required to be paid for 2012 (add lines 7 and 12) |

|

|

13 |

||

14 |

90% of the estimated tax required to be paid for 2012 (multiply line 13 by 90% (.90)) |

14 |

||||

.00

.00

.00

.00

Prior year

15Total of all nonresident individual partners’ or shareholders’ distributive

|

or pro rata shares of 2011 income earned from New York sources .... |

|

15 |

|

.00 |

|

|

16 |

Total of all nonresident individual partners’ or shareholders’ shares of |

|

|

|

|

|

|

|

2011 partnership deductions allocated to New York (see instructions).. |

|

16 |

|

.00 |

|

|

17 |

Subtract line 16 from line 15 |

|

17 |

|

.00 |

|

|

18 |

Individual tax rate (8.97%) |

|

18 |

|

.0897 |

|

|

19 |

Multiply line 17 by line 18 |

|

19 |

|

.00 |

|

|

20 |

Total of all nonresident individual partners’ or shareholders’ distributive |

|

|

|

|

|

|

|

or pro rata shares of 2011 partnership or S corporation credits |

20 |

|

.00 |

|

|

|

21 |

2011 estimated tax computed for individuals (subtract line 20 from line 19) |

.......................................................... |

|

21 |

|||

22 |

Total of all corporate partners’ distributive shares of 2011 income earned from NY sources |

|

22 |

|

.00 |

|

|

23 |

Corporation tax rate (7.1%) |

|

23 |

|

.071 |

|

|

24 |

Multiply line 22 by line 23 |

|

24 |

|

.00 |

|

|

25 |

Total of all corporate partners’ distributive shares of 2011 partnership credits |

|

25 |

|

.00 |

|

|

26 |

2011 estimated tax computed for corporations (subtract line 25 from line 24) |

|

26 |

||||

27 |

Total estimated tax computed for 2011 (add lines 21 and 26) |

|

27 |

||||

|

If the sum of lines 17 and 22 is more than $150,000, and the entity is not primarily |

|

|

|

|||

|

engaged in farming or ishing, complete line 28 and continue with Schedule B. If the |

|

|

|

|||

|

sum of lines 17 and 22 is $150,000 or less, skip line 28 and continue with Schedule B. |

|

|

|

|||

28 |

Multiply line 27 by 110% (1.10) |

|

28 |

||||

.00

.00

.00

.00

Schedule B – Short method for computing the penalty. Complete lines 29 through 34 if you paid four equal estimated tax installments (on the due dates), or if you made no payments of estimated tax. Otherwise, you must complete Schedule C.

29If you were not required to make an entry on line 28, enter the lesser of lines 14 or 27.

|

If you were required to make an entry on line 28, enter the lesser of lines 14 or 28 |

29 |

.00 |

30 |

Enter the total amount of estimated tax payments made for 2012 |

30 |

.00 |

31 |

Total underpayment for the year (subtract line 30 from line 29; if zero or less you do not owe the penalty) |

31 |

.00 |

32 |

Multiply line 31 by .04976 and enter the result |

32 |

.00 |

33 |

If the amount on line 31 was paid on or after April 15, 2013, enter 0. If the amount on line 31 was paid |

|

|

|

before April 15, 2013, make the following computation to ind the amount to enter on this line: |

|

|

|

Amount on line 31 × number of days before April 15, 2013 × .00020 = |

33 |

.00 |

34 |

Penalty (subtract line 33 from line 32; enter here and on line 51) |

34 |

.00 |

(continued)

069002120094

|

|

|

|

|

|

|

|

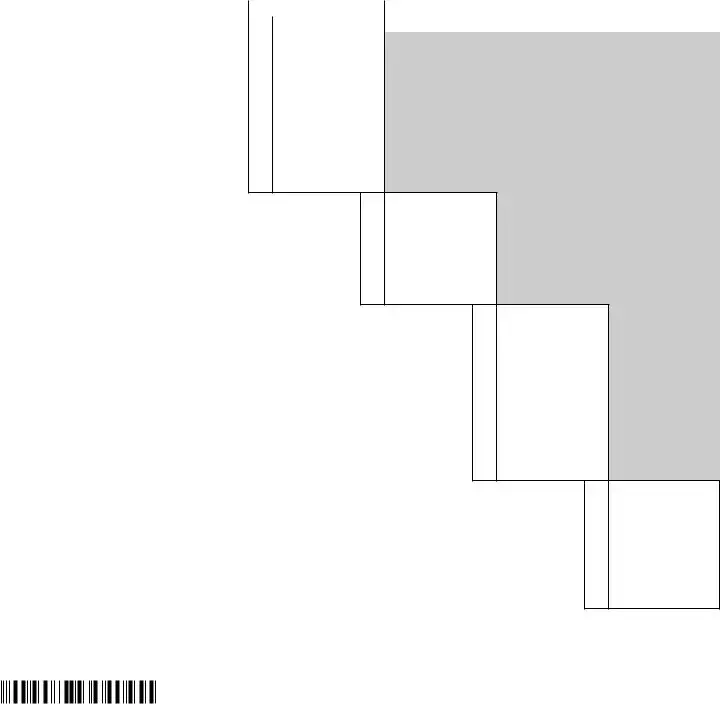

Page 3 of 4 |

|||

|

|

|

|

|

|

|

|

|

|

|

|

Schedule C – Regular method |

|

|

|

|

|

|

|

|

|

|

|

Part 1 – Computing the underpayment |

|

|

|

|

|

|

|

|

|

|

|

|

Payment due dates |

|

A |

4/15/12 |

B |

6/15/12 |

C |

9/15/12 |

|

D |

1/15/13 |

35 |

Required installments (see instructions) |

35 |

|

.00 |

|

.00 |

|

|

.00 |

|

.00 |

36 |

Estimated tax paid |

36 |

|

.00 |

|

.00 |

|

|

.00 |

|

.00 |

Complete lines 37 through 39, one column |

|

|

|

|

|

|

|

|

|

|

|

at a time, starting in column A. |

|

|

|

|

|

|

|

|

|

|

|

37 |

Overpayment or underpayment from prior period .... |

37 |

|

|

|

.00 |

|

|

.00 |

|

.00 |

38 |

If line 37 is an overpayment, add lines 36 |

|

|

|

|

|

|

|

|

|

|

|

and 37; if line 37 is an underpayment, |

|

|

|

|

|

|

|

|

|

|

|

subtract line 37 from line 36 (see instructions) |

38 |

|

.00 |

|

.00 |

|

|

.00 |

|

.00 |

39 |

Underpayment (subtract line 38 from line 35) |

|

|

|

|

|

|

|

|

|

|

|

or overpayment (subtract line 35 from |

|

|

|

|

|

|

|

|

|

|

|

line 38; see instructions) |

39 |

|

.00 |

|

.00 |

|

|

.00 |

|

.00 |

Part 2 – Computing the penalty |

|

|

|

|

|

|

|

|

|

|

|

|

Payment due dates |

|

A |

4/15/12 |

B |

6/15/12 |

C |

9/15/12 |

|

D |

1/15/13 |

|

40 Amount of underpayment (from line 39) |

40 |

|

.00 |

|

.00 |

|

|

.00 |

|

.00 |

First installment (April 15 - June 15, 2012) |

|

|

|

|

|

|

|

|

|

|

|

41April 15 ‑ June 15 =

(61 ÷ 366) × 7.5% = .01249

|

|

|

- or - |

|

||||

April 15 ‑ |

|

|

= |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

( |

|

|

÷ 366) × 7.5% = |

. |

|

|

|

|

|

|

41 |

|

|||||

42 Multiply line 40, column A, by line 41 ............ 42 |

.00 |

|||||||

Second installment (June 15 - September 15, 2012)

43June 15 ‑ September 15 = (92 ÷ 366) × 7.5% = .01884

-or -

June 15 ‑ |

|

= ( |

|

÷ 366) × 7.5% = |

. |

|

43 |

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

44 Multiply line 40, column B, by line 43 |

44 |

.00 |

||||||

Third installment (September 15, 2012 - January 15, 2013)

45September 15 ‑ December 31 = (107 ÷ 366) × 7.5% = .02192

January 1 ‑ January 15 |

= (15 ÷ 365) × 7.5% = .00307 |

|

|

|

|||||

|

|

|

|

|

.02499 |

Total |

|

|

|

|

|

- or - |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

||

September 15 ‑ |

|

|

= ( |

|

÷ 366) × 7.5% = |

. |

|

|

|

|

|

|

|

|

|

|

|

||

January 1 ‑ |

= ( |

|

÷ 365) × 7.5% = |

. |

|

|

|

||

|

|

|

|

|

|

|

Total |

45 |

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

||

46 Multiply line 40, column C, by line 45 |

|

|

|

|

|

||||

|

|

46 |

.00 |

||||||

Fourth installment (January 15 - April 15, 2013)

47January 15 ‑ April 15 = (90 ÷ 365) × 7.5% = .01848

-or -

|

January 15 ‑ |

|

= ( |

|

÷ 365) × 7.5% = |

. |

|

|

|

|

|

|

|

|

47 |

|

|||

48 |

Multiply line 40, column D, by line 47 |

............................................................................................................................ 48 |

.00 |

||||||

49 |

Penalty (add lines 42, 44, 46, and 48) |

49 |

.00 |

||||||

(continued)

069003120094

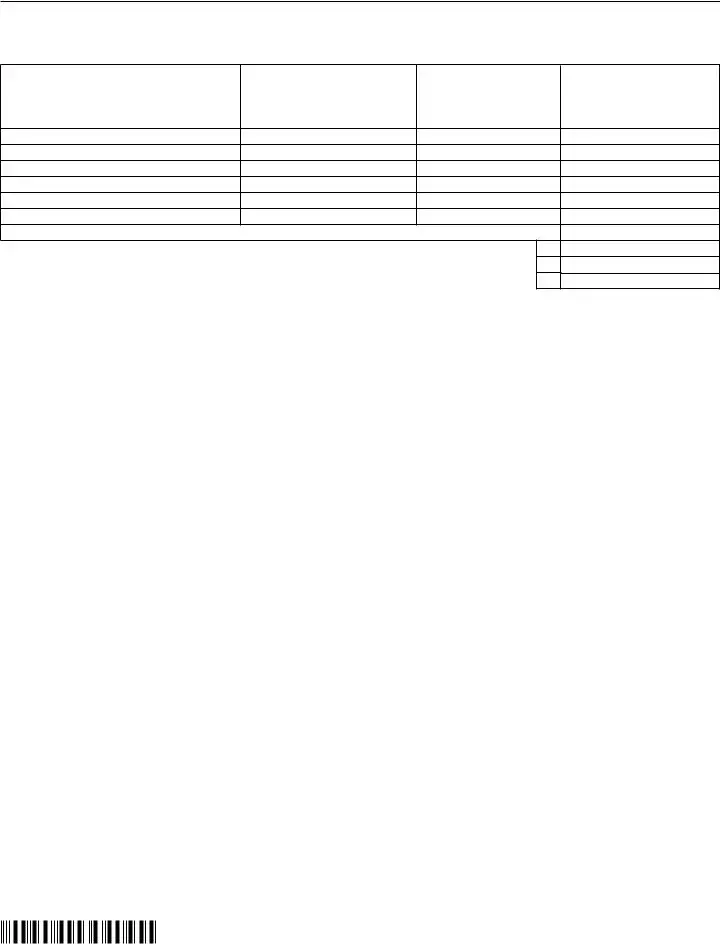

Page 4 of 4

Schedule D – Failure to pay estimated tax on behalf of partners or shareholders who are corporations or nonresident individuals. Only include partners and shareholders who are subject to estimated tax paid on their behalf by the partnership or New York S corporation (see instructions). If you are listing more than six partners or shareholders, attach additional sheet(s) using the same four‑column format as in the chart below. Include all column D totals from additional sheets on the line provided.

A

Name of

partner/shareholder

B

Identifying number

(EIN/SSN)

C

Number of quarters (1‑4)

during the year estimated tax

was not paid

D

Column C × $50

Column D total from attached sheet(s) (if any) |

||

50 |

Penalty (total of column D) |

50 |

51 |

Penalty (from line 34) |

51 |

52 |

Total penalty (add lines 49, 50, and 51, as applicable; enter here and in Payment enclosed box on the front page) |

52 |

.00

.00

.00

069004120094

| Fact Name | Description |

|---|---|

| Form Purpose | The IT-2659 form is used by partnerships and New York S corporations to report estimated tax penalties for underpayment or nonpayment of estimated tax required on behalf of partners and shareholders. |

| Applicable Tax Year | This form is specifically for the calendar year 2012 or for fiscal years beginning and ending in that period. |

| Filing Deadline | Form IT-2659 must be filed by the later of April 15, 2013, or the due date of the partnership or S corporation tax return, considering any extensions. |

| Payment Instructions | Tax payments should be made payable to the "Commissioner of Taxation and Finance" and must be submitted with the form. |

| Governing Law | The form is governed by New York State tax laws, specifically those related to estimated tax requirements for partnerships and S corporations. |

| Penalties Calculation | Penalties are calculated based on underpayments and are detailed in Schedules A through D, which must be completed as applicable. |

Filling out the New York IT-2659 form involves several steps to ensure accurate reporting of estimated tax penalties for partnerships and New York S corporations. It is important to gather all necessary information beforehand to facilitate the process. Following the steps below will help in completing the form correctly.

What is the purpose of the New York IT-2659 form?

The IT-2659 form is used by partnerships and New York S corporations to report and calculate estimated tax penalties for underpayment or nonpayment of estimated taxes on behalf of partners and shareholders. This includes nonresident individuals and corporations. It ensures compliance with New York State tax laws by assessing any penalties that may apply due to insufficient estimated tax payments.

Who needs to file the IT-2659 form?

Any partnership or New York S corporation that has nonresident partners or shareholders who are required to pay estimated taxes must file this form. If the entity fails to pay the required estimated taxes on behalf of these individuals, they may face penalties, which the IT-2659 helps to calculate.

When is the IT-2659 form due?

The IT-2659 form must be filed by the later of April 15 of the following year or the due date of the partnership or S corporation tax return. If an extension has been granted for filing the tax return, the IT-2659 is still due by the same deadline. It is important to note that this form should not be attached to any other tax forms when submitted.

How is the penalty calculated on the IT-2659 form?

The penalty is computed by completing Schedules A through D on the form. Schedule A assesses the estimated tax underpayment for both the current and prior years, while Schedules B and C determine the penalty based on the amount of underpayment and the timing of payments. The form includes specific lines where calculations should be made, and the total penalty is summarized at the end.

What should be included with the IT-2659 form when filing?

When filing the IT-2659 form, you should include a check or money order for the penalty amount calculated on line 52. This payment should be made out to the "Commissioner of Taxation and Finance." Ensure that only the penalty amount is included in the payment, and do not attach the form to any other tax forms.

Where do I mail the completed IT-2659 form?

The completed IT-2659 form, along with the payment, should be mailed to the New York State Tax Department at the following address: NYS TAX DEPARTMENT - IT-2659, PO BOX 397, ALBANY NY 12201-0397. Make sure to double-check the address to avoid any delays in processing.

Completing the New York IT-2659 form can be a straightforward process, but several common mistakes can lead to complications. Awareness of these errors is crucial for ensuring accurate submissions and avoiding penalties.

One frequent mistake is failing to provide complete and accurate information in the legal name and trade name sections. This information must match official records. Any discrepancies can result in delays or rejections. Individuals should double-check the spelling and ensure that the names are consistent with the business registration documents.

Another common error involves incorrect calculation of the estimated tax required. Filers often overlook the need to include all relevant income and deductions. This can lead to an underpayment, resulting in penalties. It is essential to carefully review the figures on Schedules A through D to ensure all applicable amounts are included in the calculations.

In addition, many filers neglect to sign the form. A signature is a critical requirement, as it verifies the authenticity of the submission. Without a signature from a general partner, member, or authorized person, the form may be considered incomplete and could be returned.

Moreover, some individuals mistakenly submit the IT-2659 form with other tax forms. This is a violation of the submission guidelines. The IT-2659 must be mailed separately to avoid processing issues. Ensure that only the required form and payment are included in the envelope.

Another significant mistake is miscalculating the payment amount due. Filers sometimes fail to include only the amount shown on line 52 of the form when submitting payment. It is crucial to follow the instructions precisely to avoid overpayment or underpayment issues.

Additionally, individuals may forget to review the deadlines for filing the form. The IT-2659 must be filed by the later of April 15 or the due date of the partnership or S corporation tax return. Missing the deadline can result in penalties that could have been avoided with timely submission.

Finally, some filers do not keep copies of their submitted forms and payments. Retaining copies is essential for record-keeping and may be necessary for future reference or in case of an audit. Maintaining organized records can help address any discrepancies that may arise later.

The New York IT-2659 form is used by partnerships and S corporations to report estimated tax penalties for underpayment or nonpayment of estimated tax. Several other forms and documents may accompany the IT-2659 to ensure compliance with tax obligations. The following is a list of these documents.

These forms and documents play a crucial role in the tax reporting process for partnerships and S corporations in New York. Ensuring that all necessary paperwork is completed accurately helps to avoid penalties and maintain compliance with state tax regulations.

When completing the New York IT-2659 form, it is essential to approach the task with care and attention to detail. Here are four key actions to consider, along with some pitfalls to avoid:

Many people have misunderstandings about the New York IT-2659 form. Here are five common misconceptions and the truth behind them:

This form is actually for partnerships and S corporations, regardless of size. Even small businesses with few partners need to file if they have nonresident partners or shareholders.

In reality, the IT-2659 must be filed separately. It should not be attached to any other forms. This ensures that the tax department processes it correctly.

Filing is not optional. If your partnership or S corporation has nonresident partners or shareholders, you must file the form, even if there is no estimated tax due.

Penalties can vary based on the specific circumstances of each entity. Factors such as the amount of underpayment and the timing of payments can influence the penalty amount.

An extension for your tax return does not extend the deadline for filing the IT-2659. You still need to submit it by the specified date to avoid penalties.

Filling out the New York IT-2659 form can be straightforward if you keep a few key points in mind. Here are some essential takeaways to help guide you through the process:

By keeping these points in mind, you can navigate the IT-2659 form with greater confidence and ensure compliance with New York State tax requirements.