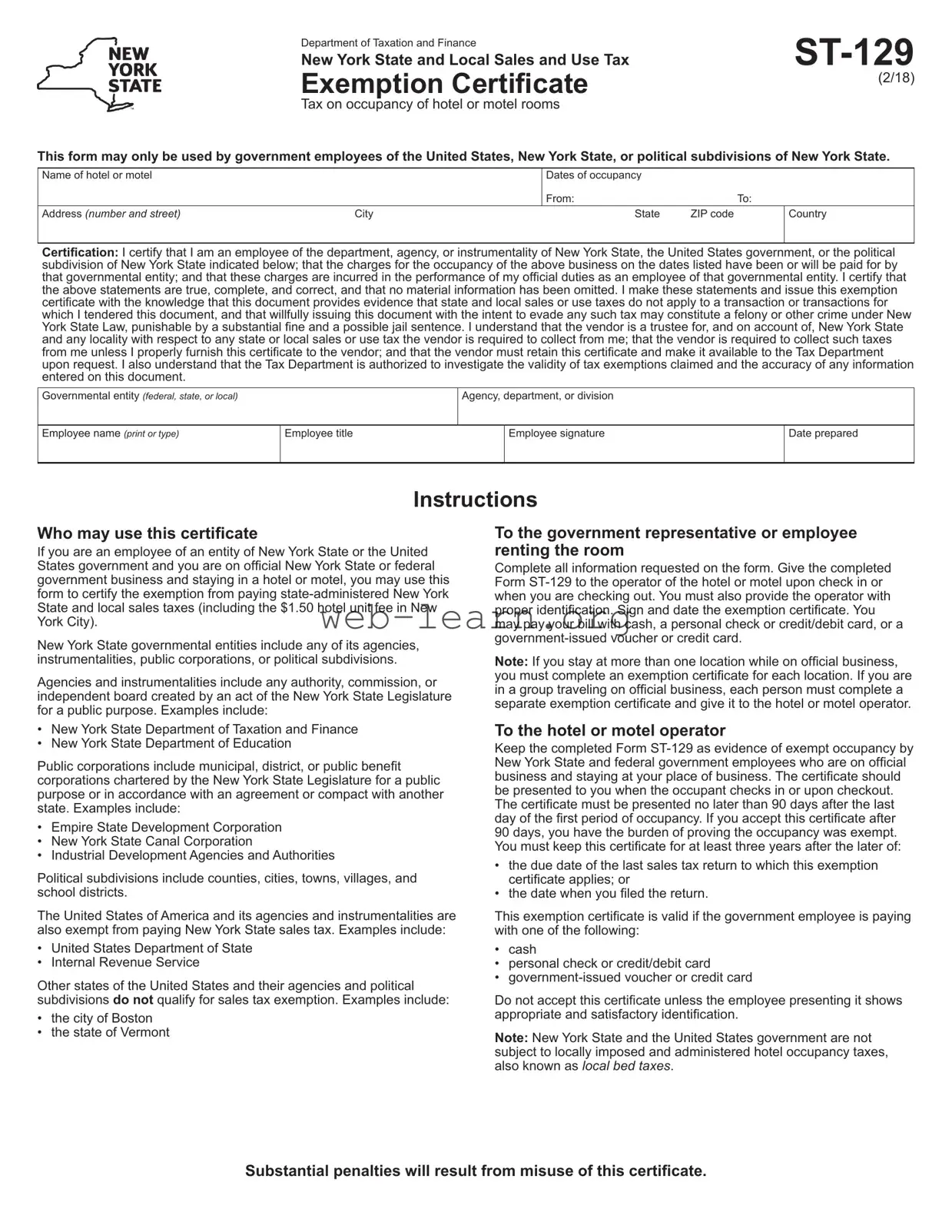

The New York Hotel Tax Exempt form, officially known as Form ST-129, serves as a crucial document for government employees traveling on official business. This form allows eligible individuals—specifically employees of the United States, New York State, or its political subdivisions—to certify their exemption from state and local sales taxes, including the hotel unit fee in New York City. To utilize this exemption, the employee must provide essential details such as the name and address of the hotel, the dates of occupancy, and their government agency affiliation. The form requires the employee to affirm that their hotel charges will be covered by their governmental entity and are incurred in the performance of official duties. Additionally, it emphasizes the importance of accuracy and honesty, warning against the consequences of willfully misrepresenting information. Both the employee and the hotel operator have specific responsibilities regarding the completion and retention of this certificate, ensuring compliance with tax regulations. Understanding the proper use of this form is essential for eligible travelers to avoid unnecessary expenses and penalties.

Department of Taxation and Finance |

|

New York State and Local Sales and Use Tax |

|

Exemption Certificate |

(2/18) |

|

Tax on occupancy of hotel or motel rooms

This form may only be used by government employees of the United States, New York State, or political subdivisions of New York State.

Name of hotel or motel |

|

Dates of occupancy |

|

|

|

|

|

|

|

|

From: |

|

|

|

To: |

|

|

Address (number and street) |

City |

|

State |

ZIP code |

|

|

Country |

|

|

|

|

|

|

|

|

|

|

Certification: I certify that I am an employee of the department, agency, or instrumentality of New York State, the United States government, or the political subdivision of New York State indicated below; that the charges for the occupancy of the above business on the dates listed have been or will be paid for by that governmental entity; and that these charges are incurred in the performance of my official duties as an employee of that governmental entity. I certify that the above statements are true, complete, and correct, and that no material information has been omitted. I make these statements and issue this exemption certificate with the knowledge that this document provides evidence that state and local sales or use taxes do not apply to a transaction or transactions for which I tendered this document, and that willfully issuing this document with the intent to evade any such tax may constitute a felony or other crime under New York State Law, punishable by a substantial fine and a possible jail sentence. I understand that the vendor is a trustee for, and on account of, New York State and any locality with respect to any state or local sales or use tax the vendor is required to collect from me; that the vendor is required to collect such taxes from me unless I properly furnish this certificate to the vendor; and that the vendor must retain this certificate and make it available to the Tax Department upon request. I also understand that the Tax Department is authorized to investigate the validity of tax exemptions claimed and the accuracy of any information entered on this document.

Governmental entity (federal, state, or local)

Agency, department, or division

Employee name (print or type)

Employee title

Employee signature

Date prepared

Instructions

Who may use this certificate

If you are an employee of an entity of New York State or the United States government and you are on official New York State or federal government business and staying in a hotel or motel, you may use this form to certify the exemption from paying

New York State governmental entities include any of its agencies, instrumentalities, public corporations, or political subdivisions.

Agencies and instrumentalities include any authority, commission, or independent board created by an act of the New York State Legislature for a public purpose. Examples include:

•New York State Department of Taxation and Finance

•New York State Department of Education

Public corporations include municipal, district, or public benefit corporations chartered by the New York State Legislature for a public purpose or in accordance with an agreement or compact with another state. Examples include:

•Empire State Development Corporation

•New York State Canal Corporation

•Industrial Development Agencies and Authorities

Political subdivisions include counties, cities, towns, villages, and school districts.

The United States of America and its agencies and instrumentalities are also exempt from paying New York State sales tax. Examples include:

•United States Department of State

•Internal Revenue Service

Other states of the United States and their agencies and political subdivisions do not qualify for sales tax exemption. Examples include:

•the city of Boston

•the state of Vermont

To the government representative or employee renting the room

Complete all information requested on the form. Give the completed Form

Note: If you stay at more than one location while on official business, you must complete an exemption certificate for each location. If you are in a group traveling on official business, each person must complete a separate exemption certificate and give it to the hotel or motel operator.

To the hotel or motel operator

Keep the completed Form

90 days, you have the burden of proving the occupancy was exempt. You must keep this certificate for at least three years after the later of:

•the due date of the last sales tax return to which this exemption certificate applies; or

•the date when you filed the return.

This exemption certificate is valid if the government employee is paying with one of the following:

•cash

•personal check or credit/debit card

•

Do not accept this certificate unless the employee presenting it shows appropriate and satisfactory identification.

Note: New York State and the United States government are not subject to locally imposed and administered hotel occupancy taxes, also known as local bed taxes.

Substantial penalties will result from misuse of this certificate.

| Fact Name | Details |

|---|---|

| Eligible Users | This form is exclusively for government employees of the United States, New York State, or its political subdivisions on official business. |

| Purpose | The ST-129 form certifies exemption from state and local sales taxes, including New York City's hotel unit fee, for eligible government employees. |

| Retention Requirement | Hotel operators must retain the completed ST-129 for at least three years after the last sales tax return it applies to. |

| Governing Law | This exemption is governed by New York State tax law, which stipulates the conditions under which the exemption applies. |

Completing the New York Hotel Tax Exempt form is essential for government employees who are on official business. This document allows you to certify your exemption from certain taxes while staying at a hotel or motel. Follow the steps below to ensure you fill it out correctly.

What is the New York Hotel Tax Exempt form?

The New York Hotel Tax Exempt form, officially known as Form ST-129, is a certificate used by government employees of the United States, New York State, or its political subdivisions. This form certifies that the employee is on official government business and is exempt from paying state and local sales taxes on hotel accommodations.

Who is eligible to use this form?

Only employees of federal, state, or local government entities may use this form. This includes employees of New York State agencies, public corporations, and political subdivisions. However, employees of other states and their agencies do not qualify for this exemption.

How should the form be completed?

The employee must fill out all requested information on the form, including their name, agency, dates of occupancy, and the hotel’s details. The form should be signed and dated by the employee before submission to the hotel operator.

When should the form be presented to the hotel?

The completed Form ST-129 must be presented to the hotel operator at check-in or check-out. It is essential to provide this certificate no later than 90 days after the last day of the stay. Otherwise, the hotel may not accept it, and the burden of proof falls on the hotel operator.

What forms of payment are acceptable when using the exemption certificate?

Employees can pay for their hotel accommodations using cash, a personal check, a credit/debit card, or a government-issued voucher or credit card. The exemption certificate is valid with any of these payment methods.

What should hotels do with the completed form?

Hotels must retain the completed Form ST-129 as evidence of exempt occupancy. This certificate should be kept for at least three years after the last sales tax return it applies to. The hotel must also ensure that the employee presents appropriate identification when submitting the form.

What are the consequences of misusing the exemption certificate?

Misuse of the exemption certificate can lead to substantial penalties. Willfully issuing the form with the intent to evade taxes may result in criminal charges, including fines and potential jail time. It is crucial to use this form correctly and only for legitimate government business.

Filling out the New York Hotel Tax Exempt form can be straightforward, but many individuals make common mistakes that can lead to complications. One prevalent error is failing to provide complete information. Each section of the form requires specific details, such as the name of the hotel, dates of occupancy, and the governmental entity. Omitting any of this information can invalidate the exemption.

Another frequent mistake involves not signing or dating the form. The certification section must be signed by the employee and dated appropriately. Without a signature or date, the form is incomplete and may not be accepted by the hotel or motel operator.

Some individuals mistakenly believe that any government employee can use the form. However, only employees of the United States, New York State, or its political subdivisions are eligible. Employees from other states or local governments do not qualify for this exemption, which can lead to confusion and denial of the tax exemption.

Another common issue is not providing proper identification when presenting the form. The hotel or motel operator requires satisfactory identification to verify the employee's status. Without this identification, the exemption certificate may be rejected, resulting in unexpected charges.

Many people also overlook the requirement of submitting a separate form for each location when traveling on official business. If an employee stays at multiple hotels, they must complete a new exemption certificate for each one. Failing to do so can complicate the tax exemption process.

Additionally, some individuals may attempt to use the form after the 90-day deadline. The exemption certificate must be presented no later than 90 days after the last day of occupancy. If submitted late, the hotel operator may not honor the exemption, and the employee could be responsible for paying taxes.

Another mistake is not understanding the payment methods that qualify for the exemption. Employees can pay with cash, personal checks, or government-issued cards, but using a personal credit card may not qualify for the exemption. This misunderstanding can lead to unexpected tax charges.

Lastly, individuals sometimes neglect to keep a copy of the completed form. It’s essential to retain a copy for personal records. This can be helpful if there are any disputes or questions regarding the tax exemption in the future.

By being aware of these common mistakes, individuals can ensure a smoother experience when filling out the New York Hotel Tax Exempt form, ultimately saving time and avoiding unnecessary complications.

The New York Hotel Tax Exempt form is essential for government employees staying in hotels while on official business. However, there are other documents that may accompany this form to ensure compliance and proper processing of tax exemptions. Below are some commonly used forms and documents that can be relevant in these situations.

Utilizing these documents alongside the New York Hotel Tax Exempt form can streamline the process and ensure compliance with tax regulations. Proper documentation protects both the employee and the hotel from potential legal issues related to tax exemptions.

The New York Hotel Tax Exempt form, known as Form ST-129, serves a specific purpose for government employees who are on official business. It is similar to several other documents that facilitate tax exemptions in various contexts. Here are seven documents that share similarities with the New York Hotel Tax Exempt form:

Each of these documents plays a crucial role in ensuring compliance with tax regulations while facilitating the appropriate use of funds for exempt purposes. Understanding their similarities can help in navigating tax exemption processes more effectively.

When filling out the New York Hotel Tax Exempt form, it is essential to follow specific guidelines to ensure compliance and avoid potential issues. Below is a list of things to do and not to do when completing this form.

The following list outlines common misconceptions regarding the New York Hotel Tax Exempt form, specifically the ST-129, and clarifies the facts associated with each.

When utilizing the New York Hotel Tax Exempt form, there are several important points to keep in mind. Understanding these key takeaways can help ensure that the process runs smoothly for both government employees and hotel operators.