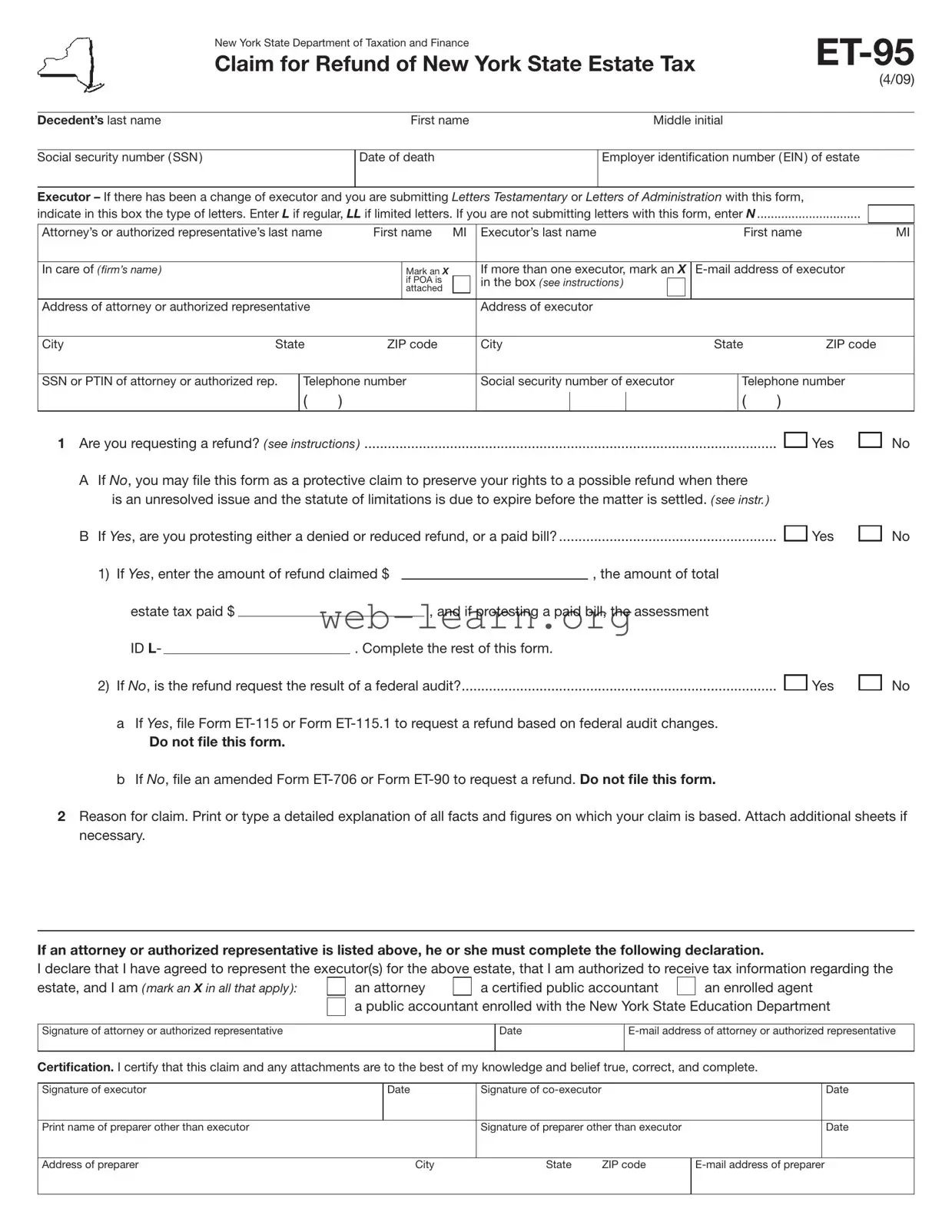

The New York ET-95 form is a crucial document for individuals seeking a refund of New York State estate tax. This form serves several purposes, including the protest of denied refunds, the filing of protective claims, and the contesting of paid bills. Executors or authorized representatives must provide detailed information about the decedent, including their name, Social Security number, and date of death. Additionally, the form requires the executor's details, such as their contact information and any changes in the executor's status. If there are multiple executors, this must also be indicated. The form allows for the submission of claims based on various grounds, including unresolved issues that may affect the estate tax. It is essential for claimants to provide a clear explanation of the reasons for their refund request and to attach any necessary documentation. By completing the ET-95 form accurately, individuals can protect their rights and ensure that any potential overpayment is addressed in a timely manner.

|

New York State Department of Taxation and Finance |

|

||

|

Claim for Refund of New York State Estate Tax |

|||

|

|

|

|

(4/09) |

|

|

|

|

|

Decedent’s last name |

|

First name |

Middle initial |

|

|

|

|

|

|

Social security number ( SSN ) |

|

Date of death |

Employer identiication number ( EIN ) of estate |

|

|

|

|

|

|

Executor – If there has been a change of executor and you are submitting Letters Testamentary or Letters of Administration with this form,

indicate in this box the type of letters. Enter L if regular, LL if limited letters. If you are not submitting letters with this form, enter N..............................

Attorney’s or authorized representative’s last name |

First name |

MI |

Executor’s last name |

|

First name |

MI |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

In care of ( firm’s name ) |

|

|

|

Mark an X |

|

|

If more than one executor, mark an X |

||||||||

|

|

|

|

if POA is |

|

|

in the box ( see instructions ) |

|

|

|

|

|

|

||

|

|

|

|

attached |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address of attorney or authorized representative |

|

|

|

|

Address of executor |

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

State |

ZIP code |

|

|

City |

State |

|

ZIP code |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||

SSN or PTIN of attorney or authorized rep. |

Telephone number |

|

|

Social security number of executor |

|

Telephone number |

|||||||||

|

|

( |

) |

|

|

|

|

|

|

|

|

|

( |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

1 Are you requesting a refund? ( see instructions ) |

|

Yes |

A If No, you may ile this form as a protective claim to preserve your rights to a possible refund when there |

|

|

is an unresolved issue and the statute of limitations is due to expire before the matter is settled. ( see instr. ) |

|

|

B If Yes, are you protesting either a denied or reduced refund, or a paid bill? |

|

Yes |

|

No

No

1) If Yes, enter the amount of refund claimed $ |

|

, the amount of total |

estate tax paid $ |

|

|

, and if protesting a paid bill, the assessment |

|

|

|

ID L- |

|

|

. Complete the rest of this form. |

|

|

|

2) If No, is the refund request the result of a federal audit? |

|

Yes |

||||

|

||||||

aIf Yes, ile Form

Do not file this form.

b If No, ile an amended Form

No

2Reason for claim. Print or type a detailed explanation of all facts and igures on which your claim is based. Attach additional sheets if necessary.

If an attorney or authorized representative is listed above, he or she must complete the following declaration.

I declare that I have agreed to represent the executor(s) for the above estate, that I am authorized to receive tax information regarding the

estate, and I am ( mark an X in all that apply ): an attorney a certiied public accountant an enrolled agent a public accountant enrolled with the New York State Education Department

Signature of attorney or authorized representative |

Date |

|

|

|

|

Certification. I certify that this claim and any attachments are to the best of my knowledge and belief true, correct, and complete.

Signature of executor |

Date |

Signature of |

|

|

Date |

|

|

|

|

|

|

Print name of preparer other than executor |

|

Signature of preparer other than executor |

|

Date |

|

|

|

|

|

|

|

Address of preparer |

City |

State |

ZIP code |

||

|

|

|

|

|

|

Instructions

Use this form to claim a refund of New York State estate tax only for the following types of claims:

Protest of denied refund — If the Tax Department has denied or adjusted your refund for any reason other than offsets to amounts owed to other agencies or tax liabilities, you may immediately ile a formal claim for refund.

Protective claim * — A protective claim is a refund claim that is based on an unresolved issue(s) that involves the Tax Department or another taxing jurisdiction that may affect your New York State estate tax. The purpose of iling a protective claim is to protect any potential overpayment when the statute of limitations is due to expire.

Protest of paid bill * — If the bill was based on Form

*Note: Your protective claim or protest must be iled within three years from the time the return was iled or within two years from the time the tax was paid, whichever is later.

File all other claims, for dates of death after May 25, 1990, and before February 1, 2000, on Form

Executor information

Enter the name (last name irst) and other information for the executor of the estate. The term executor includes executrix, administrator, administratrix, or personal representative of the decedent’s estate; if no executor, executrix, administrator, administratrix, or personal representative is appointed, qualiied, and acting within the United States, executor means any person in actual or constructive possession of any property of the decedent.

If an executor has not been appointed, this form may be signed and iled by a person having knowledge of all the assets in the decedent’s estate. This person must also enter his or her name, address, and social security number in the area provided for the executor on the front of this form.

If the estate has more than one executor, mark an X in the box, enter the name and other information for the primary executor (preferably a person residing in New York State) in the area provided, and attach a list of each of the other executors with their mailing address and social security number if not previously submitted. Submit Letters Testamentary or Letters of Administration with this form if not previously submitted. It is suficient to have one of the coexecutors sign this form.

Attorney/representative information

If you, as the executor of the estate, have authorized a person to represent you regarding the estate, and you would like the department to contact him or her regarding the estate, enter the name (last name irst) of the attorney, accountant, or enrolled agent who is representing you. Also enter the irm’s name, address, and telephone number in the areas provided, and have the representative sign in the area provided on the front of this form.

Note: If you are giving a person power of attorney to represent you, attach a completed Form

Sign this claim and mail to:

NYS TAX DEPARTMENT

TDAB - ESTATE TAX AUDIT

W A HARRIMAN CAMPUS

ALBANY NY 12227

Privacy notification

The Commissioner of Taxation and Finance may collect and maintain personal information pursuant to the New York State Tax Law, including but not limited to, sections

This information will be used to determine and administer tax liabilities and, when authorized by law, for certain tax offset and exchange of tax information programs as well as for any other lawful purpose.

Information concerning quarterly wages paid to employees is provided to certain state agencies for purposes of fraud prevention, support enforcement, evaluation of the effectiveness of certain employment and training programs and other purposes authorized by law.

Failure to provide the required information may subject you to civil or criminal penalties, or both, under the Tax Law.

This information is maintained by the Manager of Document Management, NYS Tax Department, W A Harriman Campus, Albany NY 12227; telephone (518)

Need help?

Internet access: www.nystax.gov

(for information, forms, and publications)

|

|

available 24 hours a day, |

|

7 days a week. |

1 800 |

Telephone assistance is available from 8:00 A.M. to 5:00 P.M. (eastern time), Monday through Friday.

Estate Tax Information Center: |

(518) |

|

1 800 |

||

To order forms and publications: |

(518) |

|

1 800 |

Text Telephone (TTY) Hotline (for persons with hearing and speech disabilities using a TTY): If you have access to a TTY, contact us at 1 800

If you do not own a TTY, check with independent living centers or community action programs to ind out where machines are available for public use.

Persons with disabilities: In compliance with the Americans with Disabilities Act, we will ensure that our lobbies, ofices, meeting rooms, and other facilities are accessible to persons with disabilities. If you have questions about special accommodations for persons with disabilities, call the information center.

| Fact Name | Details |

|---|---|

| Form Purpose | The ET-95 form is used to claim a refund of New York State estate tax. |

| Governing Laws | New York State Tax Law, sections 5-a, 171, 171-a, 287, 308, 429, 475, 505, 697, 1096, 1142, and 1415. |

| Executor Information | The form requires detailed information about the executor, including name, address, and social security number. |

| Change of Executor | If there is a change of executor, the form must indicate the type of letters submitted. |

| Refund Request Types | Requests can be for a denied refund, a protective claim, or a protest of a paid bill. |

| Filing Deadlines | Claims must be filed within three years of the return filing or two years from the tax payment, whichever is later. |

| Attorney Representation | If an attorney or representative is involved, their details must be provided, and they must sign the form. |

| Privacy Notification | Personal information collected is governed by New York State Tax Law and used for tax administration purposes. |

| Contact Information | For assistance, individuals can contact the Estate Tax Information Center at (518) 457-5387. |

Filling out the New York ET-95 form requires careful attention to detail. This form is used to claim a refund of New York State estate tax. Ensure all information is accurate and complete before submission to avoid delays in processing.

What is the purpose of the New York ET-95 form?

The New York ET-95 form is used to claim a refund of New York State estate tax. It can be utilized for various types of claims, including protests against denied refunds, protective claims for unresolved issues, and protests of paid bills.

Who is eligible to file the ET-95 form?

The executor of the estate, or a person authorized to represent the executor, can file the ET-95 form. If no executor has been appointed, a person with knowledge of the estate's assets may file on behalf of the estate.

What information is required on the form?

The form requires details such as:

How do I know if I should file a protective claim?

A protective claim should be filed if there is an unresolved issue that could affect your estate tax refund and the statute of limitations is nearing expiration. This ensures that your rights to a potential refund are preserved.

What is the deadline for filing the ET-95 form?

The ET-95 form must be filed within three years from the date the return was filed or within two years from the date the tax was paid, whichever is later. Timely filing is crucial to protect your claim.

What should I do if my refund claim is denied?

If your refund claim is denied, you can file the ET-95 form to formally protest the denial. Be sure to include the amount of the refund claimed and any relevant assessment ID numbers.

Where should I send the completed ET-95 form?

Mail the completed ET-95 form to the following address:

NYS TAX DEPARTMENT

TDAB - ESTATE TAX AUDIT

W A HARRIMAN CAMPUS

ALBANY NY 12227

Filling out the New York ET-95 form can be a daunting task, especially during a time of loss. Mistakes can lead to delays in processing your claim for a refund of estate tax. One common mistake is failing to provide complete information. Each section of the form requires specific details about the decedent, the executor, and the reason for the claim. Omitting even a small piece of information can result in the form being returned or rejected. Make sure to double-check that all fields are filled out accurately and completely.

Another frequent error involves misunderstanding the purpose of the form. Some individuals mistakenly file the ET-95 when they should be using other forms, such as the ET-115 or ET-706. The ET-95 is specifically for claiming refunds, so if your situation does not fit this description, you may need to explore alternative forms. It's essential to read the instructions carefully and ensure that the ET-95 is the correct choice for your circumstances.

Additionally, many people overlook the importance of signatures. The ET-95 requires the signatures of both the executor and any authorized representatives. If these signatures are missing, the claim may not be processed. Ensure that everyone who needs to sign the form does so before submission. This step may seem minor, but it is crucial for the validity of your claim.

Another mistake is related to the reason for the claim. When detailing the reason for the refund request, it is vital to provide a thorough explanation. Many individuals write vague or incomplete statements, which can lead to confusion and delays. Be clear and concise in your explanation, and attach any necessary documentation to support your claim. This will help the tax department understand your situation better and process your request more efficiently.

Lastly, failing to meet deadlines can be detrimental to your claim. The ET-95 must be filed within specific time frames, depending on the circumstances of the estate. Be aware of these deadlines and ensure that your claim is submitted on time. If you are unsure about the timelines, consult the instructions or seek assistance. Taking these proactive steps can help avoid unnecessary complications and ensure that your claim is handled promptly.

The New York ET-95 form is a crucial document used to claim a refund of New York State estate tax. Along with this form, several other documents may be required or helpful in the process. Here is a brief overview of five commonly used forms and documents associated with the ET-95.

Understanding these forms and their purposes can facilitate the refund process and ensure that all necessary documentation is submitted correctly. Each document plays a specific role in addressing different aspects of estate tax claims and potential refunds.

When filling out the New York ET-95 form, it is crucial to follow specific guidelines to ensure accuracy and compliance. Here are five things to do and five things to avoid.

Misconception 1: The ET-95 form is only for large estates.

This is not true. The ET-95 form can be used for any estate that has overpaid New York State estate tax, regardless of its size. If you believe there has been an overpayment, you can file this form.

Misconception 2: You cannot file the ET-95 if the estate tax was paid more than three years ago.

This is incorrect. While there are time limits for filing certain claims, the ET-95 form can still be filed as a protective claim if there are unresolved issues affecting the estate tax. It is important to act before the statute of limitations expires.

Misconception 3: You must have an attorney to file the ET-95 form.

While having an attorney can be helpful, it is not a requirement. Executors can file the form themselves if they have the necessary information and understand the process.

Misconception 4: The ET-95 form is only for protesting denied refunds.

In reality, the ET-95 can be used for various claims, including protests of denied refunds and protective claims for unresolved issues. It serves multiple purposes in the estate tax refund process.

Misconception 5: You can submit the ET-95 form without supporting documentation.

This is not advisable. A detailed explanation of the claim's basis should accompany the form. Attach any relevant documents to strengthen your case.

Misconception 6: Filing the ET-95 guarantees a refund.

Filing the ET-95 does not guarantee a refund. The claim will be reviewed by the New York State Department of Taxation and Finance, and a determination will be made based on the information provided.

Filling out the New York ET-95 form can seem daunting, but understanding its key components can simplify the process. Here are six essential takeaways to keep in mind:

By following these key points, you can navigate the process of filling out and using the New York ET-95 form with greater confidence. Remember, accurate information and clear communication are vital for a successful claim.