The NC-4 form, known as the Employee’s Withholding Allowance Certificate, plays a vital role in ensuring that North Carolina employees have the correct amount of state income tax withheld from their paychecks. This form is essential for both employees and employers, as it helps determine how much tax should be withheld based on the employee's specific circumstances. When filling out the NC-4, individuals must consider their filing status, such as Single, Married Filing Jointly, or Head of Household, and accurately report their allowances. Importantly, if an employee does not submit an NC-4, the employer will default to withholding taxes based on the "Single" status with zero allowances, which may not reflect the employee's actual tax situation. The form also includes specific guidelines for different categories of employees, including nonresident aliens and those who qualify for certain deductions or credits. For those with multiple jobs, it is crucial to calculate allowances correctly to avoid under-withholding. Overall, the NC-4 form is a key component in managing state tax obligations, helping individuals maintain financial stability throughout the year.

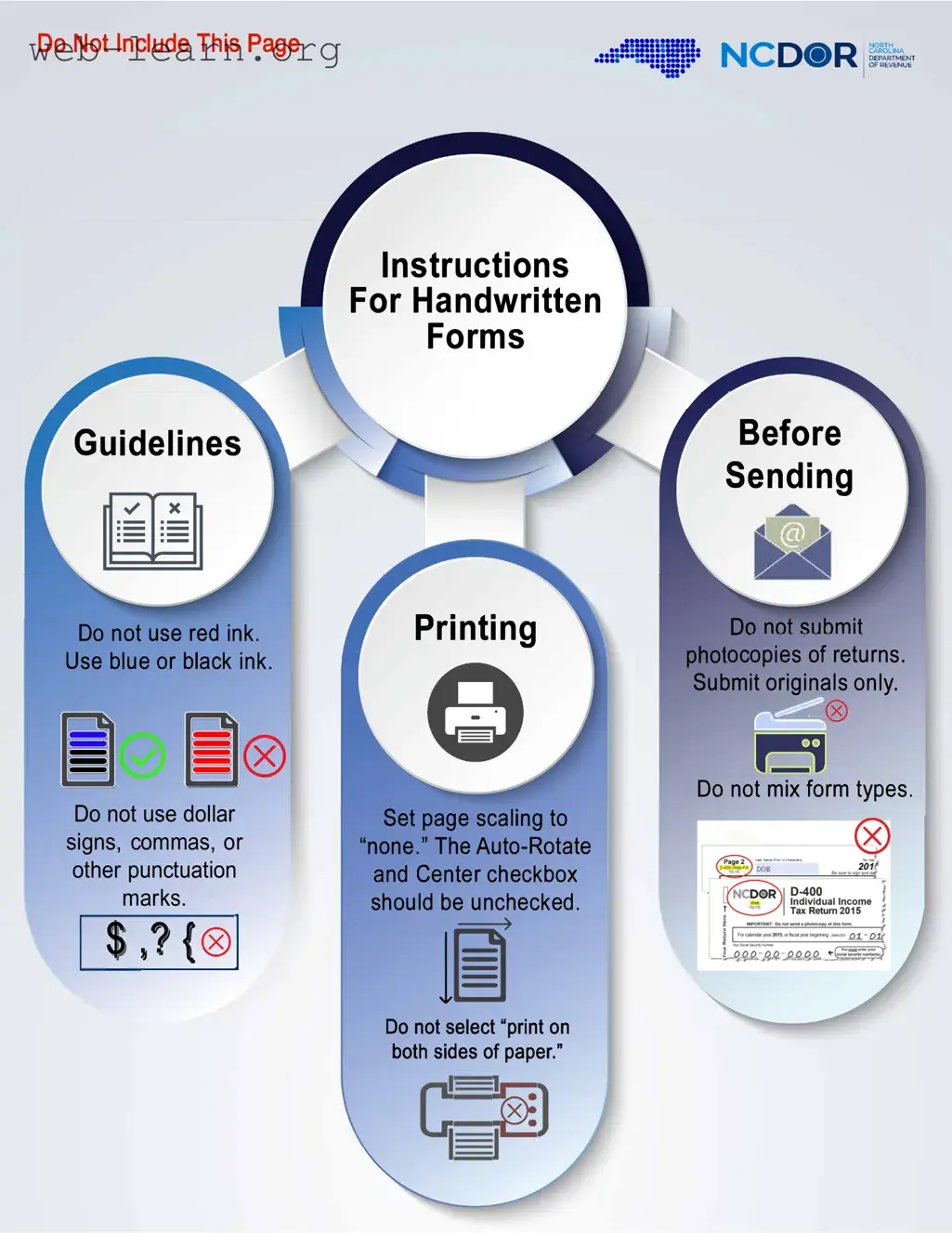

Do Not Include This Page

Guidelines

::::==·

. •• ··=!!!:::!:•

Instructions

For Handwritten

Forms

NCD(i)• R

Before Sending

I NORTH CAROLINA DEPARTMENT OF REVENUE

Do not use red ink. Use blue or black ink.

®

Do not use dollar signs, commas, or other punctuation

marks.

, 1 t®I

Printing

Set page scaling to

"none." The

1�

ocopies of returns. Submit originals only.

,,___(8)

Do not mix form types.

Do not select "print on bothc;sides of paper."

;�1

Web

Employee’s Withholding Allowance Certificate

PURPOSE - Complete Form

FORM

FORM

FORM

including the N.C. Child Deduction Amount, N.C. itemized deductions, and N.C. tax credits. However, you may claim fewer allowances than

you are entitled to if you wish to increase the tax withheld during the tax year. If your withholding allowances decrease, you must file a new

When an individual ceases to be “Head of Household” after maintaining the household for the major portion of the year, a new

TWO OR MORE JOBS - If you have more than one job, determine the total number of allowances you are entitled to claim on all jobs using one Form

“Multiple Jobs Table” to determine the additional amount to be withheld on Line 2 of Form

NONWAGE INCOME - If you have a large amount of nonwage income, such as interest or dividends, you should consider making estimated tax

payments using Form

ncdor.gov.

HEAD OF HOUSEHOLD - Generally you may claim “Head of Household” filing status on your tax return only if you are unmarried and pay more than 50% of the costs of keeping up a home for yourself and your dependent(s)

or other qualifying individuals.

SURVIVING SPOUSE - You may claim “Surviving Spouse” filing status only if your spouse died in either of the two preceding tax years and you meet the following requirements:

1.Your home is maintained as the main household of a child or stepchild for whom you can claim a federal exemption; and

2.You were entitled to file a joint return with your spouse in the year of your spouse’s death.

MARRIED TAXPAYERS - For married taxpayers, both spouses must agree as to whether they will complete the

the filing status, “Married Filing Jointly” or “Married Filing Separately.”

•Married taxpayers who complete the worksheet based on the filing status, “Married Filing Jointly” should consider the sum of both spouses’ income, federal and State adjustments to income, and State tax credits to determine the number of allowances.

•Married taxpayers who complete the worksheet based on the filing status, “Married Filing Separately” should consider only his or her portion of income, federal and State adjustments to income, and State tax credits to determine the number of allowances.

All

CAUTION: If you furnish an employer with an Employee’s Withholding Allowance Certificate that contains information which has no reasonable basis and results in a lesser amount of tax being withheld than would have been withheld had you furnished reasonable information, you are subject to a penalty of 50% of the amount not properly withheld.

Cut here and give this certificate to your employer. Keep the top portion for your records.

WebEmployee’s Withholding Allowance Certificate

1.Total number of allowances you are claiming

(Enter zero (0), or the number of allowances from Page 2, Line 17 of the

2. Additional amount, if any, withheld from each pay period (Enter whole dollars)

,.00

Social Security Number

Filing Status |

|

|

Single or Married Filing Separately |

Head of Household |

Married Filing Jointly or Surviving Spouse |

First Name (USE CAPITAL LETTERS FOR YOUR NAME AND ADDRESS) |

M.I. |

|

|

Last Name |

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

County (Enter first five letters) |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

|

State |

Zip Code (5 Digit) |

|

|

Country (If not U.S.) |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Employee’s Signature |

Date |

I certify, under penalties provided by law, that I am entitled to the number of withholding allowances claimed on Line 1 above.

|

|

|

|

|

PART I |

||

|

Answer all of the following questions for your filing status. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Single - |

|

|

|

|

|

|

|

1. |

Will your N.C. itemized deductions from Page 3, Schedule 1 exceed $13,249? |

Yes |

o |

No |

o |

|

|

2. |

Will your N.C. Child Deduction Amount from Page 3, Schedule 2 exceed $2,499? |

Yes |

o |

No |

o |

|

|

3. |

Will you have federal adjustments or State deductions from income? |

Yes |

o |

No |

o |

|

|

4. |

Will you be able to claim any N.C. tax credits or tax credit carryovers? |

Yes |

o |

No |

o |

|

|

If you answered “No” to all of the above, STOP HERE and enter ZERO (0) as total allowances on Form |

|

|||||

|

If you answered “Yes” to any of the above, you may choose to go to Page 2, Part II to determine if you qualify for |

|

|||||

|

additional allowances. Otherwise, enter ZERO (0) on Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Married Filing Jointly - |

|

|

|

|

|

|

|

1. |

Will your N.C. itemized deductions from Page 3, Schedule 1 exceed $23,999? |

Yes |

o |

No |

o |

|

|

2. |

Will your N.C. Child Deduction Amount from Page 3, Schedule 2 exceed $2,499? |

Yes |

o |

No |

o |

|

|

3. |

Will you have federal adjustments or State deductions from income? |

Yes |

o |

No |

o |

|

|

4. |

Will you be able to claim any N.C. tax credits or tax credit carryovers? |

Yes |

o |

No |

o |

|

|

5. |

Will your spouse receive combined wages and taxable retirement benefits of |

|

|

|

|

|

|

|

less than $8,250 or only retirement benefits not subject to N.C. income tax? |

Yes |

o |

No |

o |

|

|

If you answered “No” to all of the above, STOP HERE and enter ZERO (0) as total allowances on Form |

|

|||||

|

If you answered “Yes” to any of the above, you may choose to go to Page 2, Part II to determine if you qualify for |

|

|||||

|

additional allowances. Otherwise, enter ZERO (0) on Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Married Filing Separately - |

|

|

|

|

|

|

|

1. |

Will your portion of N.C. itemized deductions from Page 3, Schedule 1 exceed $13,249? |

Yes |

o |

No |

o |

|

|

2. |

Will your N.C. Child Deduction Amount from Page 3, Schedule 2 exceed $2,499? |

Yes |

o |

No |

o |

|

|

3. |

Will you have federal adjustments or State deductions from income? |

Yes |

o |

No |

o |

|

|

4. |

Will you be able to claim any N.C. tax credits or tax credit carryovers? |

Yes |

o |

No |

o |

|

|

If you answered “No” to all of the above, STOP HERE and enter ZERO (0) as total allowances on Form |

|

|||||

|

If you answered “Yes” to any of the above, you may choose to go to Page 2, Part II to determine if you qualify for |

|

|||||

|

additional allowances. Otherwise, enter ZERO (0) on Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Head of Household- |

|

|

|

|

|

|

|

1. |

Will your N.C. itemized deductions from Page 3, Schedule 1 exceed $18,624? |

Yes |

o |

No |

o |

|

|

2. |

Will your N.C. Child Deduction Amount from Page 3, Schedule 2 exceed $2,499? |

Yes |

o |

No |

o |

|

|

3. |

Will you have federal adjustments or State deductions from income? |

Yes |

o |

No |

o |

|

|

4. |

Will you be able to claim any N.C. tax credits or tax credit carryovers? |

Yes |

o |

No |

o |

|

|

If you answered “No” to all of the above, STOP HERE and enter ZERO (0) as total allowances on Form |

|

|||||

|

If you answered “Yes” to any of the above, you may choose to go to Page 2, Part II to determine if you qualify for |

|

|||||

|

additional allowances. Otherwise, enter ZERO (0) on Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Page 1

Surviving Spouse - |

|

|

|

|

|

1. |

Will your N.C. itemized deductions from Page 3, Schedule 1 exceed 23,999? |

Yes |

o |

No |

o |

2. |

Will your N.C. Child Deduction Amount from Page 3, Schedule 2 exceed $2,499? |

Yes |

o |

No |

o |

3. |

Will you have federal adjustments or State deductions from income? |

Yes |

o |

No |

o |

4. |

Will you be able to claim any N.C. tax credits or tax credit carryovers? |

Yes |

o |

No |

o |

If you answered “No” to all of the above, STOP HERE and enter FOUR (4) as total allowances on Form |

|||||

If you answered “Yes” to any of the above, you may choose to go to Part II to determine if you qualify for additional |

|||||

allowances. Otherwise, enter FOUR (4) on Form |

|

|

|

|

|

1. |

Enter your total estimated N.C. itemized deductions from Page 3, Schedule 1 |

..................................................... |

1. |

_______________________$ |

. |

|||

|

|

|

||||||

2. |

Enter the applicable |

{ |

$10,750 if Single |

|

|

|

|

|

|

N.C. standard deduction |

$21,500 if Married Filing Jointly or Surviving Spouse |

|

|

|

|||

|

based on your filing status. |

$10,750 if Married Filing Separately |

|

|

|

_______________________$ |

. |

|

|

|

$16,125 if Head of Household |

|

2. |

||||

3. |

Subtract Line 2 from Line 1. If Line 1 is less than Line 2, enter ZERO (0) |

|

3. |

_______________________$ |

. |

|||

|

|

|||||||

4. |

Enter an estimate of your total N.C. Child Deduction Amount from Page 3, Schedule 2 |

4. |

_______________________$ |

. |

||||

|

||||||||

5. |

Enter an estimate of your total federal adjustments to income and State deductions from |

|

_______________________$ |

. |

||||

|

federal adjusted gross income |

................................................................................................................................ |

|

|

5. |

|||

|

|

|

|

|

|

|||

6. |

Add Lines 3, 4, and 5 |

|

|

|

6. |

_______________________$ |

. |

|

|

|

|

|

|||||

7. |

Enter an estimate of your nonwage income (such as dividends or interest) |

7. |

$_____________________ |

. |

|

|

||

|

|

|

||||||

8.Enter an estimate of your State additions to federal adjusted gross

|

income |

8. |

$ |

. |

|

|

|

|

|

|

|||

9. |

Add Lines 7 and 8 |

|

9. |

$ |

. |

|

|

|

|||||

10. |

Subtract Line 9 from Line 6 (Do not enter less than zero) |

|

10. |

$ |

. |

|

|

|

|||||

11. |

Divide the amount on Line 10 by $2,500 . Round down to whole number |

|

11. |

_______________________ |

||

|

Ex. $3,900 ÷ $2,500 = 1.56 rounds down to 1 |

|

|

|

|

|

12. |

Enter the amount of your estimated N.C. tax credits |

12. |

$ |

. |

|

|

|

|

|

||||

13. |

Divide the amount on Line 12 by $134. Round down to whole number |

|

13. |

_______________________ |

||

|

Ex. $200 ÷ $134 = 1.49 rounds down to 1 |

|

|

|

|

|

14. If filing as Single, Head of Household, or Married Filing Separately, enter zero (0) on this line. If filing as Surviving Spouse, enter 4.

If filing as Married Filing Jointly, enter the appropriate number from either (a), (b), (c), (d), or (e) below.

(a)Your spouse expects to have combined wages and taxable retirement benefits of $0 for N.C. purposes, enter 4. (Taxable retirement benefits do not include: Bailey, Social Security, and Railroad retirement)

(b)Your spouse expects to have combined wages and taxable retirement benefits of more than $0 but less than or equal to $3,250, enter 3.

(c)Your spouse expects to have combined wages and taxable retirement benefits of more than $3,250 but less than or equal to $5,750, enter 2.

(d)Your spouse expects to have combined wages and taxable retirement benefits of more than $5,750 but less than or equal to $8,250, enter 1.

(e)Your spouse expects to have combined wages and taxable retirement benefits of more than

$8,250, enter 0 |

14. |

_______________________ |

|

|

15. Add Lines 11, 13, and 14, and enter the total here |

15. |

_______________________ |

|

|

16. If you completed this worksheet on the basis of Married Filing Jointly, the total number of allowances determined |

|

|

|

|

on Line 15 may be split between you and your spouse, however, you choose. Enter the number of allowances |

|

|

|

|

from Line 15 that your spouse plans to claim |

16. |

_______________________ |

|

|

17. Subtract Line 16 from Line 15 and enter the total number of allowances here and on Line 1 of your |

|

|

|

|

Form |

17. |

_______________________ |

|

|

|

|

|

|

|

|

|

Page |

|

2 |

|

|

|

|

|

Important: If you cannot reasonably estimate the amount to enter in the schedules below, you should enter ZERO (0) on Line 1,

Schedule 1 |

Estimated N.C. Itemized Deductions |

|

|

|

Qualifying mortgage interest |

$ |

. |

|

|

Real estate property taxes |

$ |

. |

|

. |

Total qualifying mortgage interest and real estate property taxes* |

$ |

|||

Charitable Contributions (Same as allowed for federal purposes) |

$ |

. |

||

Medical and Dental Expenses (Same as allowed for federal purposes) |

$ |

. |

||

Total estimated N.C. itemized deductions. Enter on Page 2, Part II, Line 1 |

|

$ |

. |

|

*The sum of your qualified mortgage interest and real estate property taxes may not exceed $20,000. For married taxpayers, the $20,000 limitation applies to the combined total of qualified mortgage interest and real estate property

taxes claimed by both spouses, rather than to each spouse separately.

Schedule 2 |

Estimated N.C. Child Deduction Amount |

A taxpayer who is allowed a federal child tax credit under section 24 of the Internal Revenue Code is allowed a deduction for each dependent child unless adjusted gross income exceeds the threshold amount shown below.

The N.C. Child Deduction Amount can be claimed only for a child who is under 17 years of age on the last day of the year.

|

|

|

Deduction |

|

|

|

No. of |

Amount per |

Estimated |

Filing Status |

Adjusted Gross Income |

Children |

Qualifying Child |

Deduction |

Single |

Up to |

$ |

20,000 |

|

Over |

$ |

20,000 |

|

Over |

$ |

30,000 |

|

Over |

$ |

40,000 |

|

Over |

$ |

50,000 |

|

Over |

$ |

60,000 |

MFJ or SS |

Up to |

$ |

40,000 |

|

Over |

$ |

40,000 |

|

Over |

$ |

60,000 |

|

Over |

$ |

80,000 |

|

Over |

$ |

100,000 |

|

Over |

$ |

120,000 |

HOH |

Up to |

$ |

30,000 |

|

Over |

$ |

30,000 |

|

Over |

$ |

45,000 |

|

Over |

$ |

60,000 |

|

Over |

$ |

75,000 |

|

Over |

$ |

90,000 |

MFS |

Up to |

$ |

20,000 |

|

Over |

$ |

20,000 |

|

Over |

$ |

30,000 |

|

Over |

$ |

40,000 |

|

Over |

$ |

50,000 |

|

Over |

$ |

60,000 |

|

|

|

_____________ |

$ |

2,500 |

______________ |

Up to |

$ |

30,000 |

_____________ |

$ |

2,000 |

______________ |

Up to |

$ |

40,000 |

_____________ |

$ |

1,500 |

______________ |

Up to |

$ |

50,000 |

_____________ |

$ |

1,000 |

______________ |

Up to |

$ |

60,000 |

_____________ |

$ |

500 |

______________ |

|

|

|

_____________ |

$ |

- |

______________ |

|

|

|

_____________ |

$ |

2,500 |

______________ |

Up to |

$ |

60,000 |

_____________ |

$ |

2,000 |

______________ |

Up to |

$ |

80,000 |

_____________ |

$ |

1,500 |

______________ |

Up to |

$ |

100,000 |

_____________ |

$ |

1,000 |

______________ |

Up to |

$ |

120,000 |

_____________ |

$ |

500 |

______________ |

|

|

|

_____________ |

$ |

- |

______________ |

|

|

|

_____________ |

$ |

2,500 |

______________ |

Up to |

$ |

45,000 |

_____________ |

$ |

2,000 |

______________ |

Up to |

$ |

60,000 |

_____________ |

$ |

1,500 |

______________ |

Up to |

$ |

75,000 |

_____________ |

$ |

1,000 |

______________ |

Up to |

$ |

90,000 |

_____________ |

$ |

500 |

______________ |

|

|

|

_____________ |

$ |

- |

______________ |

|

|

|

_____________ |

$ |

2,500 |

______________ |

Up to |

$ |

30,000 |

_____________ |

$ |

2,000 |

______________ |

Up to |

$ |

40,000 |

_____________ |

$ |

1,500 |

______________ |

Up to |

$ |

50,000 |

_____________ |

$ |

1,000 |

______________ |

Up to |

$ |

60,000 |

_____________ |

$ |

500 |

______________ |

|

|

|

_____________ |

$ |

- |

______________ |

Page 3

Multiple Jobs Table

Find the amount of your estimated annual wages from your lowest paying job(s) in the left hand column. Follow across to find the amount of additional tax to be withheld for each pay period. Enter the additional amount to be withheld on Line 2 of your Form

Additional Withholding for Single, Married, or Surviving Spouse with Multiple Jobs

Estimated Annual Wages |

|

Payroll Period |

|

||

At Least |

But Less Than |

Monthly |

Semimonthly |

Biweekly |

Weekly |

|

|

|

|

|

|

0 |

1000 |

2 |

1 |

1 |

1 |

1000 |

2000 |

7 |

3 |

3 |

2 |

|

|

|

|

|

|

2000 |

3000 |

11 |

6 |

5 |

3 |

|

|

|

|

|

|

3000 |

4000 |

16 |

8 |

7 |

4 |

|

|

|

|

|

|

4000 |

5000 |

20 |

10 |

9 |

5 |

|

|

|

|

|

|

5000 |

6000 |

25 |

12 |

11 |

6 |

|

|

|

|

|

|

6000 |

7000 |

29 |

14 |

13 |

7 |

7000 |

8000 |

33 |

17 |

15 |

8 |

|

|

|

|

|

|

8000 |

9000 |

38 |

19 |

17 |

9 |

9000 |

10000 |

42 |

21 |

20 |

10 |

10000 |

10750 |

46 |

23 |

21 |

11 |

|

|

|

|

|

|

10750 |

Unlimited |

48 |

24 |

22 |

11 |

Additional Withholding for Head of Household Filers with Multiple Jobs

Estimated Annual Wages |

|

Payroll Period |

|

||

At Least |

But Less Than |

Monthly |

Semimonthly |

Biweekly |

Weekly |

|

|

|

|

|

|

0 |

1000 |

2 |

1 |

1 |

1 |

|

|

|

|

|

|

1000 |

2000 |

7 |

3 |

3 |

2 |

2000 |

3000 |

11 |

6 |

5 |

3 |

|

|

|

|

|

|

3000 |

4000 |

16 |

8 |

7 |

4 |

4000 |

5000 |

20 |

10 |

9 |

5 |

5000 |

6000 |

25 |

12 |

11 |

6 |

6000 |

7000 |

29 |

14 |

13 |

7 |

7000 |

8000 |

33 |

17 |

15 |

8 |

8000 |

9000 |

38 |

19 |

17 |

9 |

9000 |

10000 |

42 |

21 |

20 |

10 |

10000 |

11000 |

47 |

23 |

22 |

11 |

11000 |

12000 |

51 |

26 |

24 |

12 |

12000 |

13000 |

56 |

28 |

26 |

13 |

13000 |

14000 |

60 |

30 |

28 |

14 |

14000 |

15000 |

65 |

32 |

30 |

15 |

15000 |

16000 |

69 |

35 |

32 |

16 |

16000 |

Unlimited |

71 |

36 |

33 |

16 |

Page 4

| Fact Name | Details |

|---|---|

| Purpose of NC-4 | The NC-4 form is used by employees to inform their employers of the correct amount of state income tax to withhold from their paychecks. |

| Filing Status Impact | If an employee does not submit an NC-4, the employer must withhold taxes as if the employee is single with zero allowances, which may result in higher withholding. |

| Form Variants | There are different versions of the NC-4, including NC-4 EZ for those claiming the N.C. Standard Deduction or Child Deduction, and NC-4 NRA for nonresident aliens. |

| Withholding Allowances | Employees can determine their withholding allowances using the NC-4 Allowance Worksheet, which takes into account various deductions and credits. |

| Change in Allowances | Employees must file a new NC-4 within 10 days if their withholding allowances change, except in certain circumstances such as ceasing to be "Head of Household." |

| Multiple Jobs | For those with more than one job, it is advised to claim all allowances on the NC-4 for the higher paying job to ensure accurate withholding. |

| Estimated Tax Payments | Individuals with significant nonwage income should consider making estimated tax payments using Form NC-40 to avoid underpayment penalties. |

| Penalties for Incorrect Information | Providing inaccurate information on the NC-4 that leads to insufficient tax withholding can result in a penalty of 50% of the underwithheld amount. |

| Governing Law | The NC-4 form is governed by the North Carolina General Statutes, specifically those related to state income tax withholding. |

Completing the NC-4 form is an important step to ensure that your employer withholds the correct amount of state income tax from your pay. Follow these steps carefully to fill out the form accurately.

Once you have completed the NC-4 form, submit it to your employer. Keep a copy for your records. If your situation changes, such as a change in your number of allowances, you may need to fill out a new NC-4 within 10 days.

What is the purpose of the NC-4 form?

The NC-4 form is used to help your employer withhold the correct amount of state income tax from your paycheck. If you do not submit this form, your employer will withhold taxes based on a “Single” filing status with zero allowances, which may not reflect your actual tax situation.

Who should complete the NC-4 form?

Anyone who is employed in North Carolina and wants to ensure the correct amount of state income tax is withheld should complete the NC-4 form. This includes residents, nonresident aliens, and those claiming specific deductions or credits.

What happens if I don’t submit an NC-4 form?

If you do not submit the NC-4 form, your employer will withhold taxes as if you are single with zero allowances. This could result in more taxes being withheld than necessary, which may affect your take-home pay.

Can I claim more allowances than I am entitled to?

You can choose to claim fewer allowances than you are entitled to. This may be beneficial if you want to increase the amount of tax withheld during the year. However, claiming more allowances than you qualify for can lead to penalties.

What should I do if my situation changes?

If your withholding allowances decrease, you must file a new NC-4 form with your employer within 10 days. An exception exists for individuals who stop being “Head of Household” after maintaining that status for most of the year; they do not need to file a new form until the next tax year.

What if I have multiple jobs?

If you work more than one job, you should complete one NC-4 form to determine your total allowances. It’s usually best to claim all your allowances on the NC-4 for your highest-paying job and claim zero on the others. This helps ensure the correct amount of tax is withheld.

What if I have nonwage income?

If you receive a significant amount of nonwage income, like interest or dividends, consider making estimated tax payments using Form NC-40. This can help you avoid underpayment penalties at tax time.

When filling out the NC-4 form, individuals often make several common mistakes that can lead to incorrect withholding amounts. One frequent error involves the use of inappropriate ink colors. It is important to use only blue or black ink, as red ink is not accepted. This simple oversight can cause delays in processing the form.

Another common mistake is the inclusion of dollar signs, commas, or other punctuation marks. The instructions clearly state that such symbols should not be used. Omitting these can help ensure that the form is processed without complications.

People also tend to mix different types of forms. Each type of form serves a specific purpose, and using the wrong one can lead to incorrect tax withholding. It is essential to use the NC-4 form specifically designed for employee withholding allowances.

Many individuals fail to accurately complete the NC-4 Allowance Worksheet. This worksheet is crucial for determining the correct number of withholding allowances. Neglecting to fill it out correctly can result in claiming too many or too few allowances, which can affect tax liability.

Some filers overlook the requirement to submit only original forms. Photocopies are not accepted, and submitting them can lead to processing delays. Keeping track of the original form is vital.

Another mistake is not updating the form when there are changes in personal circumstances, such as a change in marital status or the number of dependents. A new NC-4 must be filed within ten days of such changes to ensure accurate withholding.

Additionally, individuals often miscalculate their allowances when they have multiple jobs. It is advisable to claim all allowances on the form submitted to the higher-paying job, while filing zero allowances for the others. This strategy helps in achieving more accurate withholding.

People sometimes neglect to consider nonwage income, such as dividends or interest. If there is a significant amount of nonwage income, it may be necessary to make estimated tax payments using Form NC-40. Failing to account for this can lead to underpayment penalties.

Lastly, some individuals incorrectly claim a filing status. For instance, the status of “Head of Household” can only be claimed if specific criteria are met, such as being unmarried and providing more than half of the household expenses. Misunderstanding these requirements can lead to inaccuracies in tax withholding.

The NC-4 form is crucial for ensuring that your employer withholds the correct amount of state income tax from your paycheck. However, there are several other forms and documents that often accompany the NC-4 to help clarify your tax situation. Here’s a brief overview of these additional forms.

Understanding these forms can make a significant difference in your tax experience. Properly completing and submitting them ensures that your tax withholdings align with your financial situation, helping you avoid surprises when tax season arrives.

When filling out the NC-4 form, it is important to follow specific guidelines to ensure accuracy and compliance. Here’s a helpful list of what you should and shouldn’t do:

By following these guidelines, you can help ensure that your NC-4 form is completed correctly, which will assist in the proper withholding of state income tax from your paychecks.

Understanding the NC-4 form can be challenging, and several misconceptions often arise. Here are nine common misunderstandings related to this important document:

In reality, submitting the NC-4 form is essential. Without it, employers must withhold taxes based on the “Single” filing status with zero allowances, which may lead to higher tax withholding than necessary.

The NC-4 EZ form is only available for those claiming the N.C. Standard Deduction or N.C. Child Deduction Amount without any other deductions or credits. Not everyone qualifies.

This is incorrect. Nonresident aliens must specifically use the NC-4 NRA form to ensure proper tax withholding.

Changes in circumstances, such as a decrease in withholding allowances, require a new NC-4 to be submitted within 10 days of the change.

Married couples must agree on how to complete the NC-4 Allowance Worksheet, considering their combined income and deductions.

While claiming more allowances can increase take-home pay, it may lead to under-withholding, resulting in a tax bill when filing returns.

The NC-4 form affects withholding throughout the year, impacting each paycheck. It’s important to consider its implications regularly.

Only blue or black ink should be used. Using red ink can lead to processing issues with the form.

While employers may be required to send the form, it is not done automatically for every submission. Employers need to ensure compliance with state regulations.

Filling out the NC-4 form correctly is crucial for ensuring proper state income tax withholding. Here are key takeaways to keep in mind:

By understanding these points, you can ensure compliance and avoid unnecessary tax issues. Always keep a copy of your submitted form for your records.