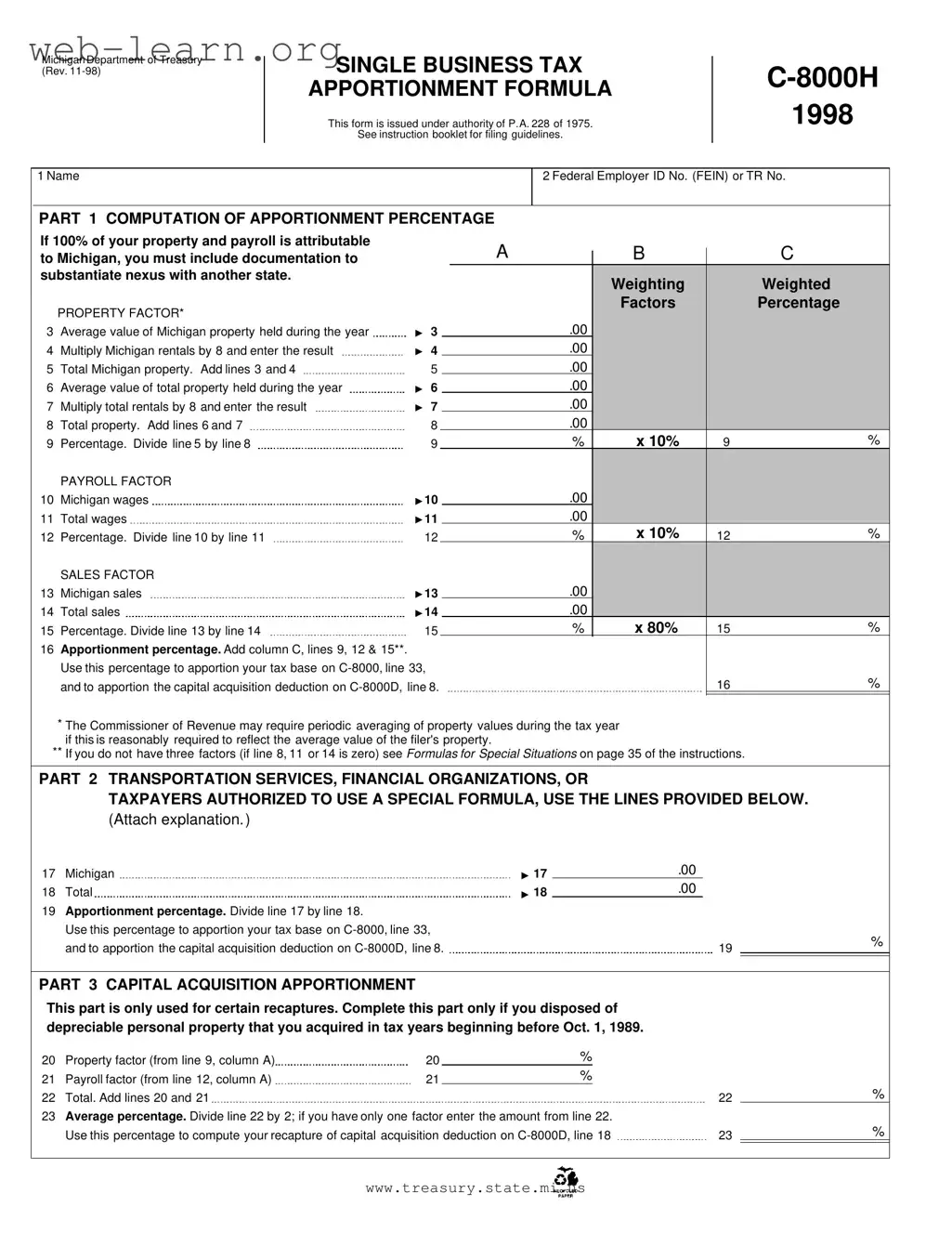

The Michigan C 8000H form is a crucial document for businesses operating within the state, particularly for those navigating the complexities of the Single Business Tax. This form is designed to help determine the apportionment percentage, which is essential for accurately calculating the tax base owed by a business. It requires detailed information about a company's property, payroll, and sales, all of which contribute to the overall apportionment calculation. By breaking down these factors, the C 8000H form allows businesses to allocate their tax responsibilities fairly based on their economic presence in Michigan versus other states. The form includes sections for computing the property factor, payroll factor, and sales factor, each weighted differently to reflect their importance in the overall apportionment process. Additionally, there are provisions for businesses in specific sectors, such as transportation services or financial organizations, to use a special formula for their calculations. Understanding how to fill out the C 8000H form correctly can significantly impact a business's tax obligations, making it a vital tool for compliance and financial planning.

Michigan Department of Treasury (Rev.

SINGLE BUSINESS TAX APPORTIONMENT FORMULA

This form is issued under authority of P.A. 228 of 1975.

See instruction booklet for filing guidelines.

1998

1 Name

2 Federal Employer ID No. (FEIN) or TR No.

PART 1 COMPUTATION OF APPORTIONMENT PERCENTAGE

If 100% of your property and payroll is attributable |

|

|

|

|

A |

|

B |

|

C |

|

to Michigan, you must include documentation to |

|

|

|

|

|

|

||||

substantiate nexus with another state. |

|

|

|

|

|

|

Weighting |

|

Weighted |

|

|

|

|

|

|

|

|

|

|

||

|

PROPERTY FACTOR* |

|

|

|

|

|

|

Factors |

|

Percentage |

|

|

|

|

|

|

|

|

|

|

|

3 |

Average value of Michigan property held during the year |

▼ |

3 |

|

|

|

.00 |

|

|

|

4 |

Multiply Michigan rentals by 8 and enter the result |

▼ |

4 |

|

|

|

.00 |

|

|

|

5 |

Total Michigan property. Add lines 3 and 4 |

|

5 |

|

|

|

.00 |

|

|

|

6 |

Average value of total property held during the year |

▼ |

6 |

|

|

|

.00 |

|

|

|

7 |

Multiply total rentals by 8 and enter the result |

▼ |

7 |

|

|

|

.00 |

|

|

|

8 |

Total property. Add lines 6 and 7 |

|

8 |

|

|

|

.00 |

|

|

|

9 |

Percentage. Divide line 5 by line 8 |

|

9 |

|

|

|

% |

x 10% |

9 |

% |

|

PAYROLL FACTOR |

|

|

|

|

|

|

|

|

|

10 |

Michigan wages |

▼ |

10 |

|

|

|

.00 |

|

|

|

11 |

Total wages |

▼ |

11 |

|

|

|

.00 |

|

|

|

12 |

Percentage. Divide line 10 by line 11 |

|

12 |

|

|

|

% |

x 10% |

12 |

% |

|

SALES FACTOR |

|

|

|

|

|

|

|

|

|

13 |

Michigan sales |

▼ |

13 |

|

|

|

.00 |

|

|

|

14 |

Total sales |

▼ |

14 |

|

|

|

.00 |

|

|

|

15 |

Percentage. Divide line 13 by line 14 |

|

15 |

|

|

|

% |

x 80% |

15 |

% |

16 |

Apportionment percentage. Add column C, lines 9, 12 & 15**. |

|

|

|

|

|

|

|

|

|

|

Use this percentage to apportion your tax base on |

|

|

|

|

|||||

|

and to apportion the capital acquisition deduction on |

|

|

16 |

% |

|||||

|

|

|

|

|

|

|

|

|

|

|

*The Commissioner of Revenue may require periodic averaging of property values during the tax year if this is reasonably required to reflect the average value of the filer's property.

**If you do not have three factors (if line 8, 11 or 14 is zero) see Formulas for Special Situations on page 35 of the instructions.

PART 2 TRANSPORTATION SERVICES, FINANCIAL ORGANIZATIONS, OR

TAXPAYERS AUTHORIZED TO USE A SPECIAL FORMULA, USE THE LINES PROVIDED BELOW.

(Attach explanation. )

17 Michigan

▼

17

.00

18Total

19Apportionment percentage. Divide line 17 by line 18.

Use this percentage to apportion your tax base on

▼

18

.00

19 |

% |

|

PART 3 CAPITAL ACQUISITION APPORTIONMENT

This part is only used for certain recaptures. Complete this part only if you disposed of depreciable personal property that you acquired in tax years beginning before Oct. 1, 1989.

20 |

Property factor (from line 9, column A) |

20 |

% |

|

|

|

21 |

Payroll factor (from line 12, column A) |

21 |

% |

|

|

|

22 |

Total. Add lines 20 and 21 |

|

|

|

22 |

% |

23 |

Average percentage. Divide line 22 by 2; if you have only one factor enter the amount from line 22. |

|

|

|||

|

Use this percentage to compute your recapture of capital acquisition deduction on |

23 |

% |

|||

www.treasury.state.mi.us

| Fact Name | Description |

|---|---|

| Governing Law | The Michigan C 8000H form is issued under the authority of Public Act 228 of 1975. |

| Purpose | This form is used for the apportionment of the Single Business Tax in Michigan. |

| Filing Guidelines | Detailed filing guidelines can be found in the accompanying instruction booklet. |

| Apportionment Percentage | The apportionment percentage is calculated based on property, payroll, and sales factors. |

| Special Situations | If certain factors are zero, taxpayers should refer to the “Formulas for Special Situations” section in the instructions. |

| Capital Acquisition | Part 3 of the form is specifically for capital acquisition apportionment related to depreciable personal property. |

Filling out the Michigan C 8000H form is an important step for businesses seeking to calculate their apportionment percentage for tax purposes. This form requires specific financial information about your property, payroll, and sales. Completing it accurately ensures compliance with state tax regulations.

What is the Michigan C 8000H form?

The Michigan C 8000H form is a Single Business Tax Apportionment Formula used by businesses operating in Michigan. It helps determine the apportionment percentage of a business's income that is taxable in Michigan, based on property, payroll, and sales factors.

Who needs to file the C 8000H form?

Businesses that have a presence in Michigan and are subject to the Single Business Tax must file this form. If a business operates in multiple states, it must apportion its income to determine how much is taxable in Michigan.

What factors are used to calculate the apportionment percentage?

The apportionment percentage is calculated using three main factors:

How do I calculate the Property Factor?

The Property Factor is calculated by taking the average value of Michigan property held during the year, adding it to the total of Michigan rentals multiplied by 8, and then dividing by the total property held during the year, which also includes total rentals multiplied by 8.

What if my business has no property, payroll, or sales in Michigan?

If your business does not have any property, payroll, or sales in Michigan, you may need to refer to the "Formulas for Special Situations" section in the instructions for guidance. In such cases, alternative methods for apportionment may apply.

What is the purpose of the apportionment percentage?

The apportionment percentage is crucial for determining how much of a business's income is subject to tax in Michigan. This percentage is applied to the tax base on the C-8000 form and is also used for capital acquisition deductions on the C-8000D form.

Can I use a special formula for apportionment?

Yes, if your business is involved in transportation services, financial organizations, or qualifies under specific conditions, you may be authorized to use a special formula. You will need to provide an explanation and complete the designated lines on the form.

What should I do if I disposed of depreciable personal property?

If you disposed of depreciable personal property acquired in tax years before October 1, 1989, you must complete Part 3 of the C 8000H form. This part helps compute the recapture of capital acquisition deductions based on your property and payroll factors.

How do I submit the C 8000H form?

After completing the C 8000H form, you should submit it along with your main tax return, typically the C-8000 form. Ensure that all required documentation is attached, especially if you claim nexus with another state.

Where can I find additional resources or assistance?

For more information, you can visit the Michigan Department of Treasury's website. They provide detailed instructions and resources related to the C 8000H form and other tax-related inquiries.

Filling out the Michigan C 8000H form can be a complex process, and several common mistakes can lead to errors that may affect tax calculations. One frequent error occurs in the calculation of property factors. Taxpayers often miscalculate the average value of Michigan property held during the year. This miscalculation can stem from not accurately averaging property values or failing to include all relevant properties. The result is an incorrect property factor that can skew the overall apportionment percentage.

Another common mistake involves inaccurate reporting of payroll figures. Taxpayers may mistakenly report total wages instead of Michigan wages. This error not only affects the payroll factor but can also lead to a misrepresentation of the business's tax liability. Ensuring that only Michigan wages are reported is essential for an accurate calculation.

Additionally, errors in sales factor calculations can occur. Taxpayers sometimes confuse Michigan sales with total sales, leading to an inaccurate sales percentage. This mistake can significantly impact the apportionment percentage, as the sales factor is weighted heavily in the overall calculation. It is crucial to distinguish between sales made within Michigan and those made outside the state.

Many individuals overlook the importance of documentation. If a business claims 100% of its property and payroll is attributable to Michigan, it must provide documentation to substantiate nexus with other states. Failing to include this documentation can lead to complications or even penalties during audits.

Another mistake involves neglecting to follow instructions. The C 8000H form comes with specific guidelines, and failure to adhere to these can result in incomplete or incorrect submissions. It is vital to read the instruction booklet carefully and ensure that all required sections are completed accurately.

Finally, not reviewing calculations before submission can lead to errors. Simple arithmetic mistakes can occur during the process, and these can have significant implications for tax liability. Taking the time to double-check all calculations can help avoid unnecessary issues with the Michigan Department of Treasury.

The Michigan C 8000H form is used for the apportionment of the Single Business Tax. It helps determine how much of a business's tax liability is attributable to Michigan based on property, payroll, and sales factors. Along with this form, several other documents may be required to ensure accurate reporting and compliance with state tax regulations.

These forms and documents work together to provide a comprehensive view of a business's tax obligations in Michigan. Proper completion and submission of each are essential for compliance and to avoid potential penalties.

The Michigan C 8000H form is a specific document used for calculating the apportionment percentage for the Single Business Tax. Several other documents serve similar purposes in different contexts or jurisdictions. Below are seven documents that share similarities with the C 8000H form:

When filling out the Michigan C 8000H form, it is essential to approach the process with care. Here are some important dos and don’ts to keep in mind:

Following these guidelines can help ensure a smoother filing process and reduce the risk of errors that could lead to complications or delays.

Understanding the Michigan C 8000H form can be challenging, and there are several misconceptions that often arise. Here’s a breakdown of seven common misunderstandings:

Being aware of these misconceptions can help businesses navigate the filing process more effectively and ensure compliance with Michigan tax laws.

When filling out the Michigan C 8000H form, consider the following key points to ensure accurate completion and compliance:

By following these takeaways, you can navigate the C 8000H form more effectively and ensure compliance with Michigan tax regulations.