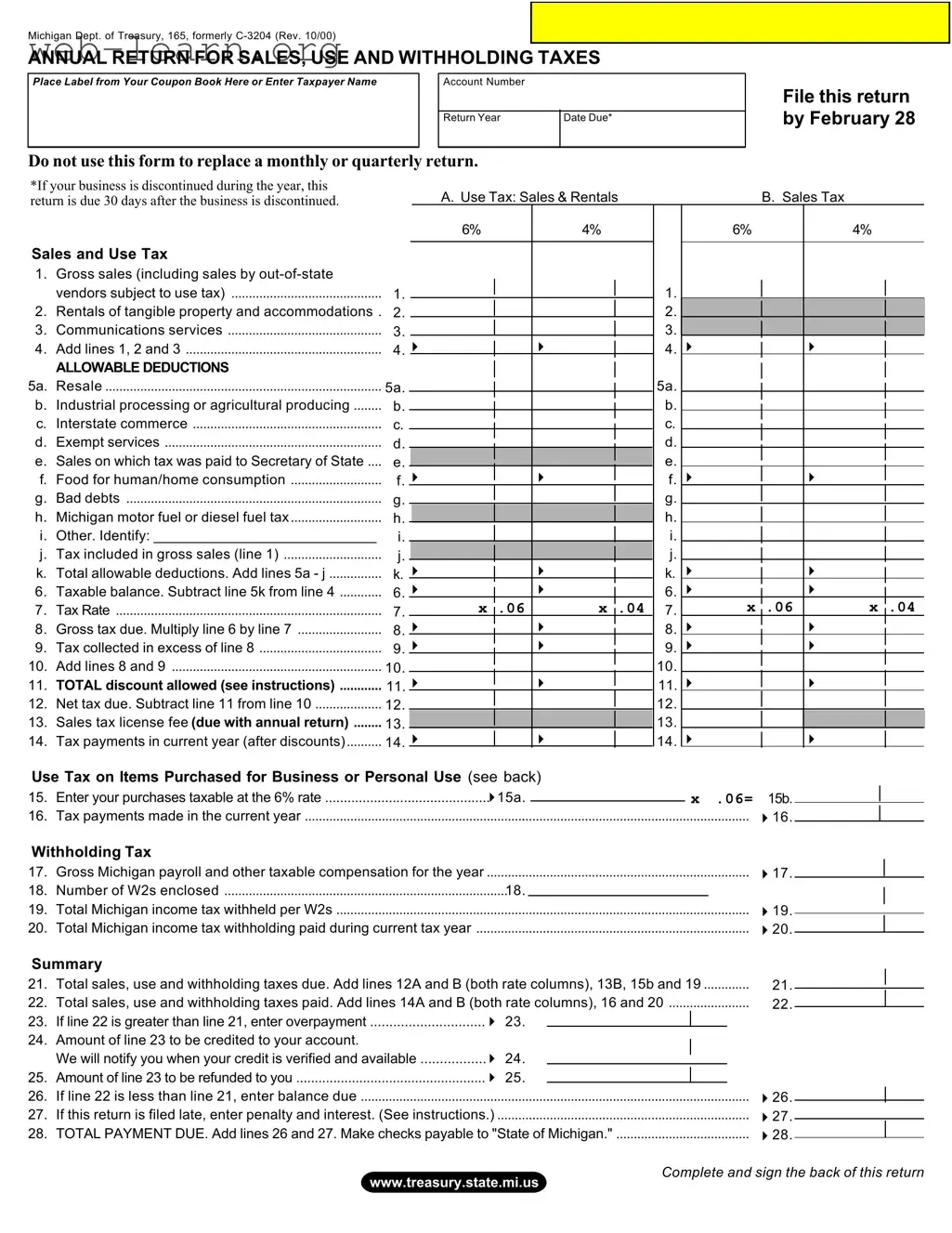

The Michigan C 3204 form serves as the Annual Return for Sales, Use, and Withholding Taxes, a crucial document for businesses operating within the state. This form must be filed annually by February 28, or within 30 days if a business is discontinued during the year. It captures essential information regarding gross sales, rentals, and communications services, allowing businesses to report their taxable transactions accurately. The form also includes sections for allowable deductions, enabling taxpayers to subtract specific expenses from their gross sales. This can include items like resale, industrial processing, and food for human consumption. Furthermore, the C 3204 calculates the gross tax due based on the taxable balance and applicable tax rates. Businesses must also report their withholding tax obligations, including total Michigan income tax withheld. By completing this form, businesses not only fulfill their tax obligations but also ensure compliance with state regulations, making it a vital aspect of financial management in Michigan.

Michigan Dept. of Treasury, 165, formerly

ANNUAL RETURN FOR SALES, USE AND WITHHOLDING TAXES

Place Label from Your Coupon Book Here or Enter Taxpayer Name |

|

Account Number |

|

|

|

|

|

|

|

Return Year |

Date Due* |

|

|

|

|

Do not use this form to replace a monthly or quarterly return.

File this return by February 28

*If your business is discontinued during the year, this |

|

|

|

A. Use Tax: Sales & Rentals |

|

|

|

|

|

|

B. Sales Tax |

|

|

|

|

|||||||||||

return is due 30 days after the business is discontinued. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

6% |

|

|

|

4% |

|

|

|

6% |

|

|

|

|

|

4% |

|

|

|

||||

Sales and Use Tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

1. |

Gross sales (including sales by |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

vendors subject to use tax) |

1. |

|

|

|

|

|

|

|

|

|

|

1. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

2. |

Rentals of tangible property and accommodations . |

2. |

|

|

|

|

|

|

|

|

|

|

2. |

|

|

|

|

|

|

|

|

|

|

|

|

|

3. |

Communications services |

3. |

|

|

|

|

|

|

|

|

|

|

3. |

|

|

|

|

|

|

|

|

|

|

|

|

|

4. |

Add lines 1, 2 and 3 |

4. |

4 |

|

|

|

|

4 |

|

|

4. |

4 |

|

|

|

|

|

|

4 |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

ALLOWABLE DEDUCTIONS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5a. |

Resale |

5a. |

|

|

|

|

|

|

|

|

|

|

5a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

b. |

Industrial processing or agricultural producing |

b. |

|

|

|

|

|

|

|

|

|

|

b. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

c. |

Interstate commerce |

c. |

|

|

|

|

|

|

|

|

|

|

c. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

d. |

Exempt services |

d. |

|

|

|

|

|

|

|

|

|

|

d. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

e. |

Sales on which tax was paid to Secretary of State .... |

e. |

|

|

|

|

|

|

|

|

|

|

e. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

|

|

|

|

4 |

|

|

4 |

|

|

|

|

|

|

4 |

|

|

|

|

||||||

f. |

Food for human/home consumption |

f. |

|

|

|

|

|

|

f. |

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

g. |

Bad debts |

g. |

|

|

|

|

|

|

|

|

|

|

g. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

h. |

Michigan motor fuel or diesel fuel tax |

h. |

|

|

|

|

|

|

|

|

|

|

h. |

|

|

|

|

|

|

|

|

|

|

|

|

|

i. |

Other. Identify: ____________________________ |

i. |

|

|

|

|

|

|

|

|

|

|

i. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

j. |

Tax included in gross sales (line 1) |

j. |

|

|

|

|

|

|

|

|

|

|

j. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

|

|

|

|

4 |

|

|

4 |

|

|

|

|

|

|

4 |

|

|

|

|

||||||

k. |

Total allowable deductions. Add lines 5a - j |

k. |

|

|

|

|

|

|

k. |

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

6. |

Taxable balance. Subtract line 5k from line 4 |

6. |

4 |

|

|

|

|

4 |

|

|

6. |

4 |

|

|

|

|

|

|

4 |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

X |

|

.06 |

|

X |

|

.04 |

|

|

|

X |

|

.06 |

|

X |

|

.04 |

||||||||

7. |

Tax Rate |

7. |

|

|

|

|

|

7. |

|

|

|

|

|

|

||||||||||||

8. |

Gross tax due. Multiply line 6 by line 7 |

8. |

4 |

|

|

|

|

4 |

|

|

8. |

4 |

|

|

|

|

|

|

4 |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

4 |

|

|

|

|

4 |

|

|

4 |

|

|

|

|

|

|

4 |

|

|

|

|

|||||||

9. |

Tax collected in excess of line 8 |

9. |

|

|

|

|

|

|

9. |

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

10. |

Add lines 8 and 9 |

10. |

|

|

|

|

|

|

|

|

|

|

10. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

11. |

TOTAL discount allowed (see instructions) |

11. |

4 |

|

|

|

|

4 |

|

|

11. |

4 |

|

|

|

|

|

|

4 |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

12. |

Net tax due. Subtract line 11 from line 10 |

12. |

|

|

|

|

|

|

|

|

|

|

12. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

13. |

Sales tax license fee (due with annual return) |

13. |

|

|

|

|

|

|

|

|

|

|

13. |

|

|

|

|

|

|

|

|

|

|

|

|

|

14. |

Tax payments in current year (after discounts) |

14. |

4 |

|

|

|

|

4 |

|

|

14. |

4 |

|

|

|

|

|

|

4 |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Use Tax on Items Purchased for Business or Personal Use (see back) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

15. |

Enter your purchases taxable at the 6% rate |

|

|

415a. |

|

|

|

|

|

|

X .06= |

|

|

15b. |

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

16. |

Tax payments made in the current year |

|

|

|

|

................................................................. |

|

|

|

|

|

|

|

|

|

416. |

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Withholding Tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

17. |

...........................................................................Gross Michigan payroll and other taxable compensation for the year |

|

|

|

|

|

|

|

|

|

417. |

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

18. |

Number of W2s enclosed |

|

|

|

18. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

19. |

Total Michigan income tax withheld per W2s |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

419. |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

20. |

Total Michigan income tax withholding paid during current tax year |

|

|

|

|

|

|

|

|

|

420. |

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

Summary |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

21. |

Total sales, use and withholding taxes due. Add lines 12A and B (both rate columns), 13B, 15b and 19 |

21. |

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|||||||||||||||||||||

22. |

Total sales, use and withholding taxes paid. Add lines 14A and B (both rate columns), 16 and 20 |

|

|

|

|

22. |

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

23. |

If line 22 is greater than line 21, enter overpayment |

|

|

4 23. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

24. |

Amount of line 23 to be credited to your account. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

We will notify you when your credit is verified and available |

4 24. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

25. |

Amount of line 23 to be refunded to you |

|

|

4 25. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

26. |

If line 22 is less than line 21, enter balance due |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

426. |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

27. |

If this return is filed late, enter penalty and interest. (See instructions.) |

|

|

|

|

|

|

|

|

|

427. |

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

28. |

TOTAL PAYMENT DUE. Add lines 26 and 27. Make checks payable to "State of Michigan." |

|

|

|

|

|

428. |

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

Complete and sign the back of this return

www.treasury.state.mi.us

Type of Business Ownership (check one only)

Individual

Husband - Wife

Partnership

Registered Partnership, Agreement Date:

Limited Partnership

Limited Liability Company

Domestic (Michigan)

Professional

Foreign

Michigan Corporation

Subchapter S

Professional

Trust or Estate (Fiduciary)

Joint Stock Club or Investment Company Social Club or Fraternal Organization Other (Explain)

Signature

I declare, under penalty of perjury, that this return is true and complete to the best of my knowledge.

I authorize Treasury to discuss my return with my preparer. Do not discuss my return with my preparer.

Taxpayer's Signature

Taxpayer's Social Security Number |

Telephone Number |

|

|

( |

) |

|

|

|

Taxpayer's Title |

Date |

|

|

|

|

I declare, under penalty of perjury, that this return is based on all information of which I have any knowledge.

Preparer's Signature, Address and Phone and ID Number

If you are enclosing payment with your return, MAIL TO: Sales, Use and Withholding Taxes

Michigan Department of Treasury

Lansing, MI 48922

If your return is for a refund, credit or has no tax due, MAIL TO: Sales, Use and Withholding Taxes

Michigan Department of Treasury

Lansing, MI 48930

*Use Tax on Items Purchased for Business or Personal Use

Use lines 15 and 16 to report purchases made for use in your business or for items removed from your inventory for personal use. Do not repeat the amounts from Column A, lines 1 - 4 here.

| Fact Name | Fact Description |

|---|---|

| Form Purpose | The Michigan C 3204 form is used for reporting annual sales, use, and withholding taxes. |

| Filing Deadline | This return must be filed by February 28 of each year. |

| Discontinued Business | If a business is discontinued, the return is due 30 days after the discontinuation. |

| Tax Rates | The applicable tax rates are 6% for sales and use tax, and 4% for certain rentals. |

| Allowable Deductions | Taxpayers can claim various deductions, including resale and bad debts. |

| Tax Calculation | Taxable balance is calculated by subtracting total allowable deductions from gross sales. |

| Overpayment Procedure | If the total taxes paid exceed the total taxes due, taxpayers can claim a refund or credit. |

| Governing Law | This form is governed by Michigan Compiled Laws, specifically MCL 205.51 et seq. |

| Signature Requirement | Taxpayers must sign the form, declaring under penalty of perjury that the information is accurate. |

| Mailing Instructions | Returns with payments should be mailed to Lansing, MI 48922; others to Lansing, MI 48930. |

Completing the Michigan C 3204 form requires careful attention to detail. This form is essential for reporting your sales, use, and withholding taxes. After filling it out, ensure that you submit it by the due date to avoid penalties. Below are the steps to guide you through the process of filling out the form.

What is the Michigan C 3204 form?

The Michigan C 3204 form is the Annual Return for Sales, Use, and Withholding Taxes. Businesses use this form to report their tax liabilities for the year, including sales tax, use tax, and withholding tax. It must be filed annually by February 28, or within 30 days if the business is discontinued during the year.

Who needs to file the C 3204 form?

Any business operating in Michigan that collects sales tax, use tax, or withholding tax is required to file this form. This includes sole proprietors, partnerships, corporations, and other business entities. If your business has no tax liability, you may still need to file to report that status.

What information do I need to complete the form?

You will need to provide details about your gross sales, rentals, and communications services. Additionally, you must list any allowable deductions and calculate the taxable balance. Information about your withholding tax, including the total Michigan income tax withheld, is also required.

How do I calculate my tax due?

To calculate your tax due, follow these steps:

What happens if I file my C 3204 form late?

If you file the C 3204 form after the due date, you may incur penalties and interest. It is important to file on time to avoid these additional charges. The form provides a section to calculate any penalties and interest that may apply.

Can I claim a refund on this form?

Yes, if you have overpaid your taxes, you can claim a refund. The form allows you to enter the amount of overpayment and specify how much you would like credited to your account or refunded to you. Be sure to keep accurate records of your payments.

What should I do if my business is discontinued?

If your business is discontinued during the year, you must file the C 3204 form within 30 days of the business closure. This ensures that you report any final tax liabilities and avoid potential penalties for late filing.

Where do I send my completed form?

If you are enclosing payment with your return, mail it to the Michigan Department of Treasury at Lansing, MI 48922. If your return is for a refund or has no tax due, send it to Lansing, MI 48930. Make sure to check the instructions on the form for any specific mailing requirements.

Is there a fee associated with filing this form?

Yes, there is a sales tax license fee that is due with the annual return. This fee is included in the calculations on the form. Be sure to review the instructions for the exact amount and any other fees that may apply.

Filling out the Michigan C 3204 form can be straightforward, but several common mistakes can lead to errors or delays in processing. One frequent error is failing to include the correct taxpayer name and account number. This information is crucial for the Michigan Department of Treasury to properly identify the business and ensure that the return is applied to the correct account. Omitting or miswriting these details can result in complications that may require additional follow-up.

Another mistake often made is misunderstanding the due date. The form states that it is due by February 28, or within 30 days if the business has been discontinued during the year. Some individuals misinterpret this information, leading to late submissions. Late filings can incur penalties and interest, which could have been avoided with careful attention to the deadlines.

Inaccurate calculations of taxable sales and allowable deductions are also common pitfalls. Taxpayers may miscalculate their gross sales or fail to include all applicable deductions. For instance, it is essential to correctly identify and sum allowable deductions, such as resale or bad debts. Errors in these calculations can lead to overpayment or underpayment of taxes, prompting further scrutiny from tax authorities.

Additionally, neglecting to sign the form is a mistake that can halt the processing of the return. Both the taxpayer and preparer must sign the document, affirming that the information provided is accurate. Without these signatures, the form may be considered incomplete, resulting in delays or the return being rejected.

Lastly, many individuals overlook the requirement to check the type of business ownership. This section must be completed accurately, as it helps the Department of Treasury categorize the business correctly. Failing to do so can lead to misclassification and potential issues with compliance. Ensuring that all sections of the form are filled out completely and accurately is essential for a smooth filing process.

The Michigan C 3204 form is an essential document for businesses to report their annual sales, use, and withholding taxes. However, several other forms and documents are often used in conjunction with it to ensure compliance with state tax regulations. Below is a list of these related documents, each serving a specific purpose.

Understanding these forms and their purposes can greatly assist businesses in navigating the complexities of tax reporting. Properly completing and submitting these documents ensures compliance with state and federal regulations, ultimately leading to smoother operations and fewer headaches down the road.

The Michigan C 3204 form is essential for reporting sales, use, and withholding taxes. Several other forms serve similar purposes, focusing on tax reporting and compliance. Here’s a look at five documents that share similarities with the Michigan C 3204 form:

When completing the Michigan C 3204 form, attention to detail is crucial. Here’s a guide outlining ten important dos and don’ts to ensure your submission is accurate and timely.

By following these guidelines, you can help ensure that your Michigan C 3204 form is filled out correctly and submitted on time, minimizing the risk of penalties or delays in processing.

Misconceptions about the Michigan C 3204 form can lead to confusion for taxpayers. Here are seven common misunderstandings:

Understanding these misconceptions can help ensure compliance with tax obligations and avoid unnecessary penalties.

Key Takeaways for Filling Out and Using the Michigan C 3204 Form: