The Michigan 4816 form is an essential document for county and local treasurers dealing with Principal Residence Exemption (PRE) denials. This form is specifically designed to request that the Michigan Department of Treasury bill a seller for any additional taxes, interest, and penalties that arise from a PRE denial when the property has been sold to a bona fide purchaser. It is crucial to complete this form accurately and attach all required documentation, including the denial notice and proof of property transfer, to avoid delays in processing. The form is divided into several parts, gathering property information, details about the PRE denial, and billing information. Each property must be submitted on a separate form, and any incomplete submissions can lead to inaccuracies in billing. Understanding the nuances of this form helps ensure that the correct parties are held accountable for any tax liabilities associated with the denial of the PRE. Properly navigating this process can save time and prevent potential financial pitfalls for both sellers and purchasers.

Michigan Department of Treasury 4816

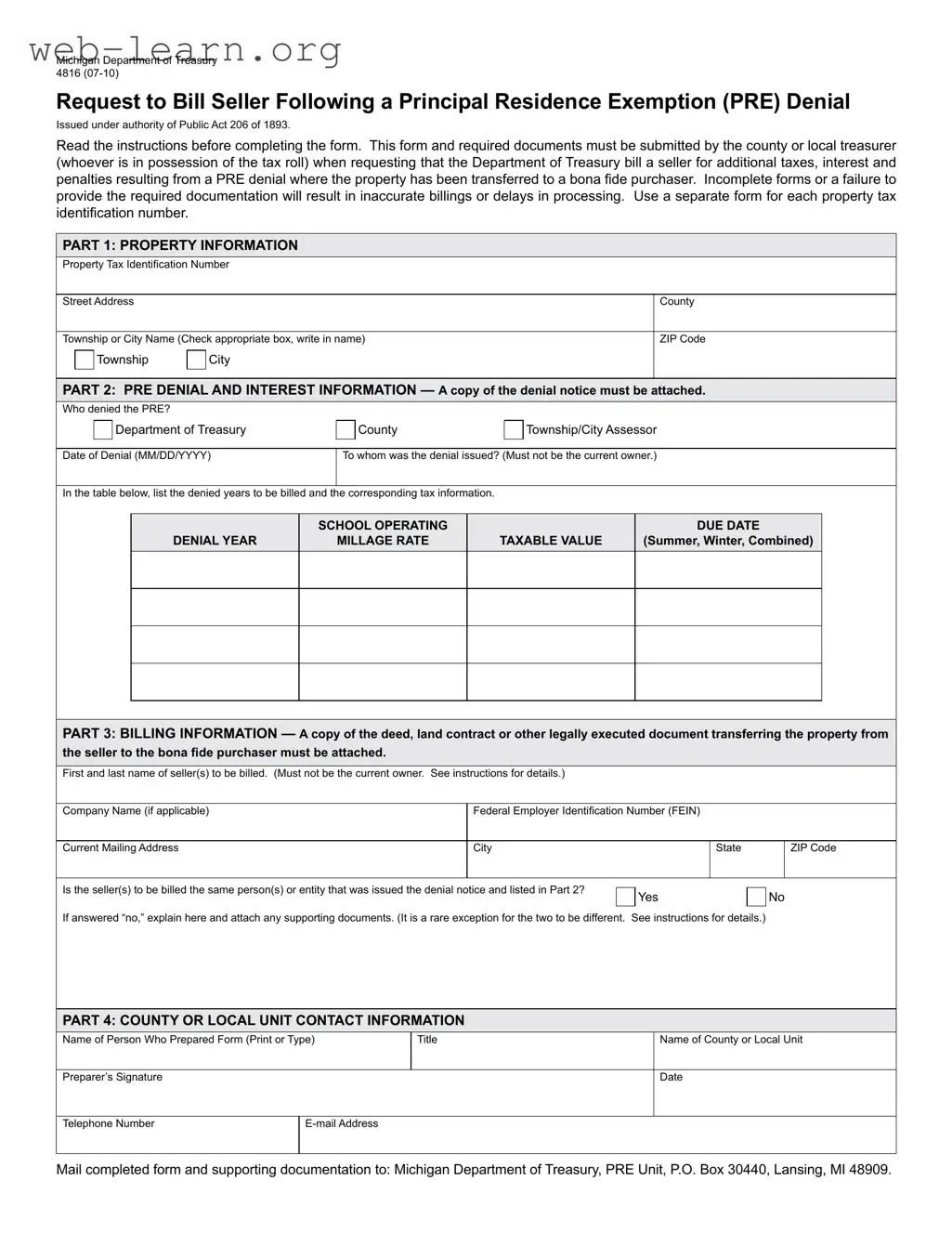

Request to Bill Seller Following a Principal Residence Exemption (PRE) Denial

Issued under authority of Public Act 206 of 1893.

Read the instructions before completing the form. This form and required documents must be submitted by the county or local treasurer

(whoever is in possession of the tax roll) when requesting that the Department of Treasury bill a seller for additional taxes, interest and penalties resulting from a PRE denial where the property has been transferred to a bona ide purchaser. Incomplete forms or a failure to

provide the required documentation will result in inaccurate billings or delays in processing. Use a separate form for each property tax identiication number.

PART 1: PROPERTY INFORMATION

Property Tax Identiication Number

Street Address |

|

|

County |

||

|

|

||||

Township or City Name (Check appropriate box, write in name) |

ZIP Code |

||||

|

|

Township |

|

City |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

PART 2: PRE DENIAL AND INTEREST INFORMATION — A copy of the denial notice must be attached.

Who denied the PRE?

Department of Treasury

County

Township/City Assessor

Date of Denial (MM/DD/YYYY) |

To whom was the denial issued? (Must not be the current owner.) |

|

|

In the table below, list the denied years to be billed and the corresponding tax information.

DENIAL YEAR

SchOOL OPERATINg

MILLAgE RATE

TAxABLE vALuE

DuE DATE

(Summer, Winter, combined)

PART 3: BILLINg INFORMATION — A copy of the deed, land contract or other legally executed document transferring the property from the seller to the bona ide purchaser must be attached.

First and last name of seller(s) to be billed. (Must not be the current owner. See instructions for details.)

Company Name (if applicable)

Federal Employer Identiication Number (FEIN)

Current Mailing Address

City

State

ZIP Code

Is the seller(s) to be billed the same person(s) or entity that was issued the denial notice and listed in Part 2?

Yes

No

If answered “no,” explain here and attach any supporting documents. (It is a rare exception for the two to be different. See instructions for details.)

PART 4: cOuNTY OR LOcAL uNIT cONTAcT INFORMATION

Name of Person Who Prepared Form (Print or Type)

Title

Name of County or Local Unit

Preparer’s Signature

Date

Telephone Number

Mail completed form and supporting documentation to: Michigan Department of Treasury, PRE Unit, P.O. Box 30440, Lansing, MI 48909.

4816, Page 2

Instructions for Form 4816

Request to Bill Seller Following a Principal Residence Exemption (PRE) Denial

This form must be submitted by the county or local treasurer (whoever is in possession of the tax roll) when requesting that the

Department of Treasury (Department) bill a seller for additional taxes, interest and penalties resulting from a PRE denial where the property has been transferred to a bona ide purchaser. Speciically, Subsections 6, 8 and 11 of Michigan Compiled Laws 211.7cc state that “if the property has been transferred to a bona ide purchaser before additional taxes were billed to the seller as a result of the

denial of a claim for exemption, the taxes, interest, and penalties shall not be a lien on the property and shall not be billed to the bona

ide purchaser ….” The local tax collecting unit in possession of the tax roll then notiies the Department, which “shall then assess the

owner who claimed the exemption under this section for the tax, interest, and penalties accruing as a result of the denial of the claim for exemption ….” In other words, the seller (the person denied) is responsible for all additional taxes, interest and penalties due for

the years up to and including the year of the sale if the purchaser is a “bona ide purchaser.” The PRE is not removed in these bona ide purchaser situations.

A “bona ide purchaser” is one who purchases in good faith for valuable consideration. Therefore, a person who receives property

through an inheritance, foreclosure or one who receives property through a quit claim without valuable consideration, would not qualify as a bona ide purchaser. If the new owner is not a bona ide purchaser, the taxes are added back to the tax roll and the purchaser is responsible for the additional taxes, interest and penalties which become a lien on the property.

There are rare situations, however, where the person(s) or entity that was denied the PRE lost the property in a foreclosure or some other circumstance to an “acquiring entity,” which then subsequently sold the property to a bona ide purchaser. In these situations, the “acquiring entity” that sold the property would be responsible for the additional taxes, interest and penalties although the denial notice was issued to the prior owner. In these unusual circumstances, since the property was not acquired for valuable consideration, the transfer to the “acquiring entity” is not considered a bona ide purchase. As a result, the “acquiring entity” is responsible for the additional taxes, interest and penalties. If this rare situation occurs, explain in Part 3 the circumstances involved and attach any supporting documents. If the “acquiring entity” has not sold the property to a bona ide purchaser, the billing of additional taxes, interest and penalties must occur at the county or local unit level (whichever is in possession of the tax roll) since the transfer was not a bona ide purchase.

In order for the Department to process a request to bill the seller (the person or entity who was issued the denial notice) for additional taxes, interest and penalties in a bona ide purchaser situation, this form must be completed with the required documents attached. Upon

review of the completed form and supporting documents, the Department will process and issue a bill, which will include additional taxes and applicable interest and penalties, to the person(s) or entity listed in Part 3.

PART 1: PROPERTY INFORMATION

All of the information in Part 1 must be provided to the Department to process the request. Use a separate form for each property tax identiication number.

PART 2: PRE DENIAL INFORMATION

A copy of the PRE denial notice relating to the property in Part 1 must be submitted with this form. The date of the denial notice must be listed on the form along with the person(s) or entity that issued the denial notice. If the denial notice was issued to the current owner of

the property, the billing of additional taxes, interest and penalties must occur at the county or local unit level (whichever is in possession of the tax roll) and does not qualify as a bona ide purchaser situation. In addition, if the purchaser is not a “bona ide purchaser,” as described earlier, the billing also must occur at the county or local level.

For each year the PRE was denied, requiring the Department to bill the seller, list the school operating millage rate, taxable value, and the due date of the school operating taxes (summer, winter, or combined summer/winter).

PART 3: BILLINg INFORMATION

A copy of the deed, land contract or other legally executed document transferring the property from the seller to the bona ide purchaser must be submitted with this form. Each seller to be billed must be listed including a current mailing address (if the mailing address is available). If the seller is a company, the complete company name, address, and Federal Employer Identiication Number (FEIN), if available, must be provided.

PART 4: cOuNTY OR LOcAL uNIT cONTAcT INFORMATION

Complete the contact information in the event the Department has a question or needs clariication. The completed form and supporting documents must be mailed to the address at the bottom of the form. Failure to provide complete information or adequate supporting documentation will result in delays in processing.

If you have any questions, call the PRE Unit at (517)

| Fact Name | Description |

|---|---|

| Form Purpose | The Michigan 4816 form is used to request that the Department of Treasury bill a seller for additional taxes, interest, and penalties after a Principal Residence Exemption (PRE) denial. |

| Governing Law | This form is issued under the authority of Public Act 206 of 1893 and is governed by Subsections 6, 8, and 11 of Michigan Compiled Laws 211.7cc. |

| Submission Requirement | County or local treasurers must submit this form along with required documents when a property has been transferred to a bona fide purchaser after a PRE denial. |

| Documentation Needed | A copy of the PRE denial notice and a deed or land contract transferring the property must accompany the form. |

| Consequences of Incomplete Submission | Submitting an incomplete form or failing to include necessary documentation can lead to inaccurate billings or delays in processing. |

| Contact Information | The completed form should be mailed to the Michigan Department of Treasury, PRE Unit, and contact details for clarification must be included. |

Filling out the Michigan 4816 form is a crucial step in the process of requesting that the Department of Treasury bill a seller for additional taxes, interest, and penalties following a Principal Residence Exemption (PRE) denial. It is important to ensure that all required information is accurate and complete, as any omissions may lead to delays or inaccuracies in billing. Follow the steps below carefully to complete the form correctly.

Once the form and supporting documents are submitted, the Department will review them. If everything is in order, they will process the request and issue a bill for the additional taxes, interest, and penalties to the appropriate seller(s). It is essential to keep copies of all submitted documents for your records.

The Michigan 4816 form is used to request that the Department of Treasury bill a seller for additional taxes, interest, and penalties that arise from a Principal Residence Exemption (PRE) denial. This form must be submitted by the county or local treasurer when the property has been transferred to a bona fide purchaser. It ensures that the seller, who was denied the PRE, is held responsible for the additional charges.

The county or local treasurer, who has possession of the tax roll, is responsible for completing the Michigan 4816 form. Each form must be filled out for a separate property tax identification number. It's essential that the form is filled out completely to avoid delays or inaccuracies in billing.

When submitting the Michigan 4816 form, several documents must be included:

These documents are crucial for the Department of Treasury to process the request accurately.

If the Michigan 4816 form is incomplete or lacks the required documentation, it may result in inaccurate billings or delays in processing. It's important to double-check all information and ensure that all necessary documents are attached before submission to avoid these issues.

Filling out the Michigan 4816 form can be a straightforward process, but many people make common mistakes that can lead to delays or inaccuracies. One frequent error is neglecting to read the instructions thoroughly before starting. The instructions provide essential guidance that can help avoid missteps. Skipping this step often results in incomplete forms, which can complicate the billing process.

Another common mistake is failing to attach the required documents. For instance, a copy of the PRE denial notice must accompany the form. Without this crucial piece of information, the Department of Treasury cannot process the request. Similarly, individuals often forget to include the deed or land contract that verifies the property transfer. Omitting these documents can lead to unnecessary delays in billing.

People sometimes confuse the roles of the seller and the current owner. The form specifically requires the seller to be the person or entity that was denied the PRE, not the current owner. Misidentifying the seller can lead to incorrect billing and further complications. Additionally, some individuals mistakenly use the same form for multiple properties. Each property tax identification number requires a separate form, and failing to do so can result in processing issues.

In Part 2 of the form, individuals often overlook the need to list the denied years and corresponding tax information accurately. This section is crucial for determining the amount owed. Errors in the taxable value or due dates can lead to significant discrepancies in billing. Furthermore, people sometimes forget to provide their contact information in Part 4. This information is vital for the Department to reach out if there are questions or clarifications needed.

Another mistake involves answering the question about whether the seller to be billed is the same as the person issued the denial notice. If the answer is “no,” it is essential to provide an explanation and attach any supporting documents. Failing to do this can complicate the billing process and may lead to additional inquiries from the Department.

Lastly, individuals often underestimate the importance of checking for accuracy before submitting the form. Simple typographical errors, such as incorrect addresses or misspelled names, can cause significant delays. Taking the time to review the form carefully can save a lot of hassle in the long run. By being mindful of these common mistakes, individuals can ensure a smoother experience when completing the Michigan 4816 form.

The Michigan 4816 form is an important document used when a property owner faces a denial of their Principal Residence Exemption (PRE). When submitting this form, it is often necessary to include additional documents to ensure a smooth process. Below are some forms and documents that are commonly used alongside the Michigan 4816 form.

Including these additional documents with the Michigan 4816 form can help prevent delays and ensure that the process is handled efficiently. It is always advisable to double-check that all required paperwork is complete and accurate before submission.

The Michigan 4816 form is important for handling tax matters related to Principal Residence Exemption (PRE) denials. Several other documents serve similar purposes in various contexts. Here are eight documents that share similarities with the Michigan 4816 form:

When filling out the Michigan 4816 form, it's important to follow specific guidelines to ensure a smooth process. Here’s a list of things you should and shouldn't do:

This is not true. The form is specifically designed to bill sellers for additional taxes, interest, and penalties after a Principal Residence Exemption (PRE) denial. It applies to sellers who are not the current owners of the property, meaning that the property must have been transferred to a bona fide purchaser.

In reality, submitting the form without the required supporting documents will lead to delays or inaccurate billings. Essential documents include a copy of the PRE denial notice and the deed or land contract transferring the property.

This is a common misunderstanding. If the property has been transferred to a bona fide purchaser before additional taxes were billed, the seller is responsible for the taxes, interest, and penalties only for the years up to the sale. If the new owner is not a bona fide purchaser, the taxes will revert to the property and be billed accordingly.

This is incorrect. The Michigan 4816 form must be completed for each property tax identification number separately. Each property requires its own form to ensure accurate processing.

This is misleading. If the PRE denial notice is issued to the current owner, the billing must occur at the county or local unit level, not through the Michigan 4816 form. The seller must be someone other than the current owner for the form to be applicable.

When dealing with the Michigan 4816 form, it’s important to follow specific guidelines to ensure a smooth process. Here are some key takeaways to keep in mind:

By keeping these points in mind, you can navigate the process of completing and submitting the Michigan 4816 form more effectively.