The Michigan 4568 form is a crucial document for businesses navigating their tax obligations in the state. This form serves as a summary of nonrefundable credits available under the Michigan Business Tax (MBT), allowing taxpayers to calculate their tax liability after applying these credits. With its various sections, the form outlines specific credits such as the Small Business Alternative Credit, Research and Development Credit, and numerous others that can significantly reduce tax burdens. Each credit has its eligibility criteria and carryforward rules, making it essential for businesses to understand which credits apply to them. Additionally, the form accommodates both standard taxpayers and financial institutions, though insurance companies must use a different form for their credits. By organizing the credits clearly, the Michigan 4568 helps streamline the tax preparation process, ensuring that businesses can efficiently identify and claim all eligible credits. This ultimately supports a smoother filing experience and promotes compliance with state tax regulations.

Michigan Department of Treasury 4568 (Rev.

Attachment 02

2011 MICHIGAN Business Tax Nonrefundable Credits Summary

Issued under authority of Public Act 36 of 2007.

Name |

Federal Employer Identiication Number (FEIN) or TR Number |

|

|

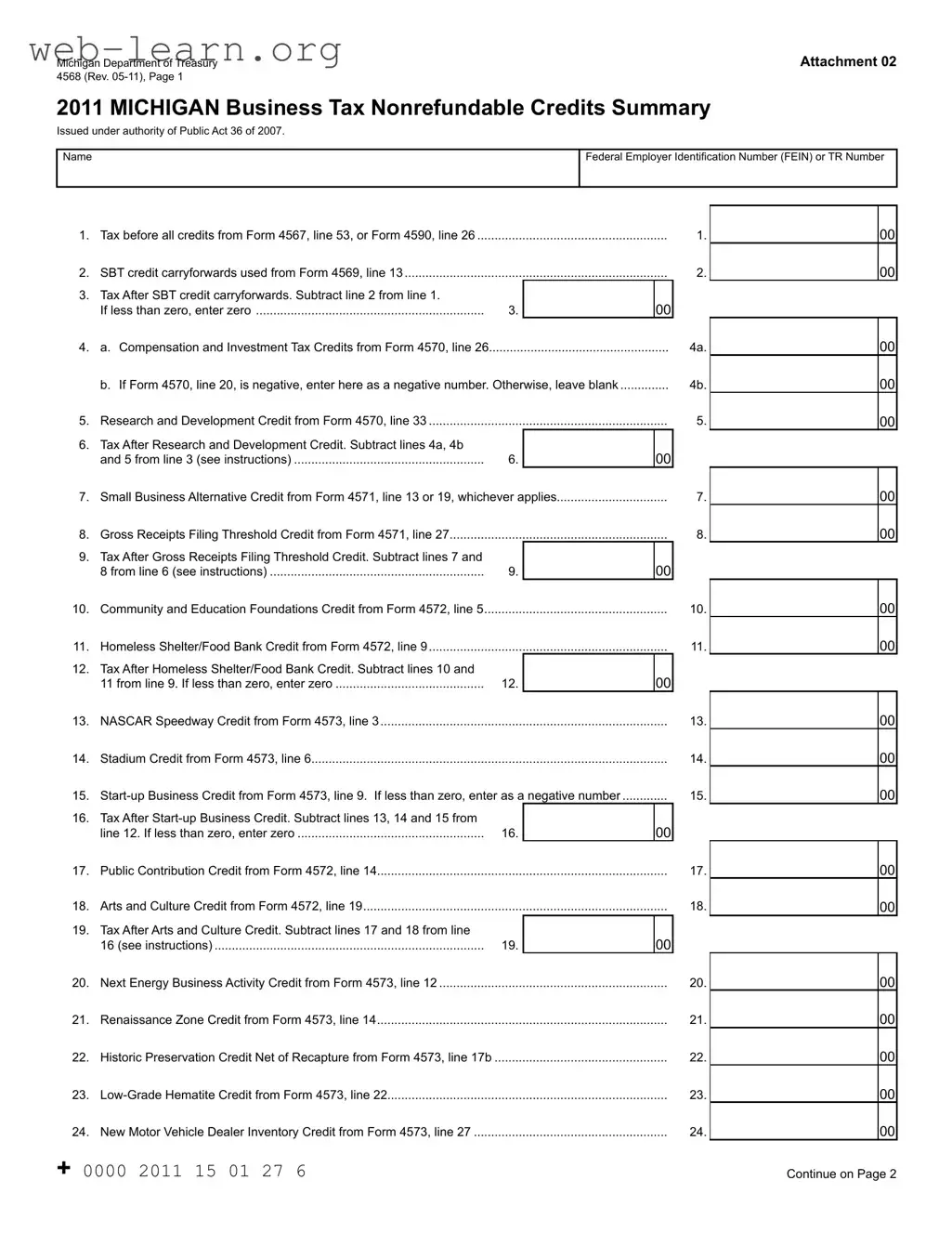

1. |

Tax before all credits from Form 4567, line 53, or Form 4590, line 26 |

1. |

|||

2. |

SBT credit carryforwards used from Form 4569, line 13 |

2. |

|||

3. |

Tax After SBT credit carryforwards. Subtract line 2 from line 1. |

|

|

|

|

|

If less than zero, enter zero |

3. |

|

00 |

|

4. |

a. Compensation and Investment Tax Credits from Form 4570, line 26 |

|

4a. |

||

|

b. If Form 4570, line 20, is negative, enter here as a negative number. Otherwise, leave blank |

|

4b. |

||

5. |

Research and Development Credit from Form 4570, line 33 |

5. |

|||

6. |

Tax After Research and Development Credit. Subtract lines 4a, 4b |

|

|

|

|

|

and 5 from line 3 (see instructions) |

6. |

|

00 |

|

7. |

Small Business Alternative Credit from Form 4571, line 13 or 19, whichever applies |

7. |

|||

8. |

Gross Receipts Filing Threshold Credit from Form 4571, line 27 |

8. |

|||

9. |

Tax After Gross Receipts Filing Threshold Credit. Subtract lines 7 and |

|

|

|

|

|

8 from line 6 (see instructions) |

9. |

|

00 |

|

10. |

Community and Education Foundations Credit from Form 4572, line 5 |

10. |

|||

11. |

Homeless Shelter/Food Bank Credit from Form 4572, line 9 |

11. |

|||

12. |

Tax After Homeless Shelter/Food Bank Credit. Subtract lines 10 and |

|

|

|

|

|

11 from line 9. If less than zero, enter zero |

12. |

|

00 |

|

13. |

NASCAR Speedway Credit from Form 4573, line 3 |

13. |

|||

14. |

Stadium Credit from Form 4573, line 6 |

|

14. |

||

15. |

If less than zero, enter as a negative number |

15. |

|||

16. |

Tax After |

|

|

|

|

|

line 12. If less than zero, enter zero |

16. |

|

00 |

|

17. |

Public Contribution Credit from Form 4572, line 14 |

17. |

|||

18. |

Arts and Culture Credit from Form 4572, line 19 |

|

18. |

||

19. |

Tax After Arts and Culture Credit. Subtract lines 17 and 18 from line |

|

|

|

|

|

16 (see instructions) |

19. |

|

00 |

|

20. |

Next Energy Business Activity Credit from Form 4573, line 12 |

20. |

|||

21. |

Renaissance Zone Credit from Form 4573, line 14 |

21. |

|||

22. |

Historic Preservation Credit Net of Recapture from Form 4573, line 17b |

22. |

|||

23. |

23. |

||||

24. |

New Motor Vehicle Dealer Inventory Credit from Form 4573, line 27 |

24. |

|||

+ 0000 2011 15 01 27 6

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

Continue on Page 2

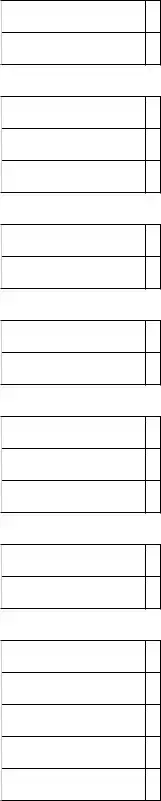

4568, Page 2 |

FEIN or TR Number |

25. |

Large Food Retailer Credit from Form 4573, line 31 |

25. |

26. |

26. |

|

27. |

Bottle Deposit Administration Credit from Form 4573, line 39 |

27. |

28. |

MEGA Federal Contract Credit from Form 4573, line 41 |

28. |

29. |

Biofuel Infrastructure Credit from Form 4573, line 44 |

29. |

30. |

Individual or Family Development Account Credit from Form 4573, line 50 |

30. |

31. |

Bonus Depreciation Credit from Form 4573, line 54 |

31. |

32. |

International Auto Show Credit from Form 4573, line 57 |

32. |

33. |

Brownield Redevelopment Credit from Form 4573, line 59 |

33. |

34. |

Private Equity Fund Credit from Form 4573, line 64 |

34. |

35. |

Film Job Training Credit from Form 4573, line 69 |

35. |

36. |

Film Infrastructure Credit from Form 4573, line 75 |

36. |

37. |

MEGA |

37. |

38. |

Anchor Company Payroll Credit from Form 4573, line 80 |

38. |

39. |

Anchor Company Taxable Value Credit from Form 4573, line 82 |

39. |

40. |

Total Nonrefundable Credits. Add lines 2, 4a, 4b, 5, 7, 8, 10, 11, 13, 14, 15, 17, 18, and 20 through 39. |

|

|

Enter total here and carry total to Form 4567, line 54, or Form 4590, line 27 |

40. |

41.Tax After Nonrefundable Credits. Subtract line 40 from line 1. If less than zero, enter zero. (This line must be equal to Form 4567, line 55,

or Form 4590, line 28.) |

41. |

00 |

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

+ 0000 2011 15 02 27 4

Instructions for Form 4568

Michigan Business Tax (MBT) Nonrefundable Credits Summary

Purpose

The purpose of this form is to determine a taxpayer’s tax liability after application of nonrefundable tax credits.

Form 4568 is intended to summarize all applicable nonrefundable credits. Speciic eligibility criteria, including varying credit carryforward life spans, apply to each of the

nonrefundable credits. For more details about each of the

credits, refer to the MBT Act or the instructions for the speciic

forms referenced on this form.

NOTE: This form may be used by both standard taxpayers and inancial institutions. Insurance companies use the

Miscellaneous Credits for Insurance Companies (Form 4596) to claim credits for which they may be eligible. Of the credits listed on this form, inancial institutions may only claim the following:

•Single Business Tax (SBT) Credit Carryforwards

•Compensation Credit

•Renaissance Zone Credit

•Historic Preservation Credit

•Individual or Family Development Account Credit

•Brownield Redevelopment Credit

•Film Infrastructure Credit.

The goal of arranging credits in this fashion is to minimize the need for taxpayers to go through all the available forms before deciding which ones may be applicable to them. Under the present arrangement, taxpayers are able to identify the forms pertaining to them, and eficiently prepare the tax return. Taxpayers should claim all credits for which they are eligible.

Special Instructions for Unitary Business Groups

Credits are earned and calculated on either an

statute.

be attributed an entity type based on the composition of its members.

Complete one Form 4568 for the group.

Further UBG instructions are provided on the forms where the

credits are calculated.

Lines not listed are explained on the form.

NAME AND ACCOUNT NUMBER: Enter name and account number as reported on page 1 of the applicable MBT annual return

(either the MBT Annual Return (Form 4567) for standard taxpayers or the MBT Annual Return for Financial Institutions (Form 4590)).

LINE 6: Although most of the entries on this form are credits that cause tax liability to decrease, if there is an entry on line 4b, subtracting that negative number will cause tax liability to

increase.

The total created by the calculations in this line cannot be less than zero. A total of less than zero is only possible through a

calculation error or an incorrect line entry.

LINE 9: The total created by the calculations in this line cannot be less than zero. A total of less than zero is only possible through a calculation error or an incorrect line entry.

LINE 16: Although most of the entries on this form are credits that cause tax liability to decrease, if there is a negative entry on line 15, subtracting that negative number will cause tax

liability to increase.

LINE 19: The total created by the calculations in this line cannot be less than zero. A total of less than zero is only possible through a calculation error or an incorrect line entry.

Include completed Form 4568 as part of the tax return iling.

| Fact Name | Details |

|---|---|

| Form Purpose | The Michigan 4568 form summarizes nonrefundable tax credits for the Michigan Business Tax. |

| Governing Law | This form is issued under the authority of Public Act 36 of 2007. |

| Eligibility | Both standard taxpayers and financial institutions can use this form, but insurance companies must use Form 4596. |

| Credit Calculation | Taxpayers calculate their tax liability after applying various nonrefundable credits listed on the form. |

| Unitary Business Groups | Unitary Business Groups must complete one Form 4568 for the group, applying credits against the group's tax liability. |

Filling out the Michigan 4568 form involves several steps to ensure that all relevant nonrefundable credits are accurately reported. This process requires careful attention to detail, as the information will ultimately affect your tax liability. Once you have completed the form, it should be included with your tax return filing.

What is the purpose of the Michigan 4568 form?

The Michigan 4568 form is used to summarize nonrefundable tax credits for taxpayers under the Michigan Business Tax (MBT). It helps determine a taxpayer’s tax liability after applying these credits. By summarizing all applicable nonrefundable credits, the form simplifies the process for taxpayers to identify which credits they may qualify for and how to apply them to their tax returns.

Who should use the Michigan 4568 form?

This form is intended for both standard taxpayers and financial institutions. However, insurance companies must use a different form, known as the Miscellaneous Credits for Insurance Companies (Form 4596), to claim their eligible credits. It is crucial for taxpayers to ensure they are using the correct form based on their entity type.

What types of credits can be claimed on the Michigan 4568 form?

The form includes a variety of nonrefundable credits, such as:

Each credit has specific eligibility criteria and varying carryforward life spans. Taxpayers should refer to the MBT Act or the instructions for the specific forms referenced on the Michigan 4568 for detailed information about each credit.

How should taxpayers report their credits on the form?

Taxpayers must complete the form by entering their information in the designated lines. It is important to accurately subtract the credits from the tax before credits to determine the tax liability after applying nonrefundable credits. If any calculations result in a negative number, taxpayers should enter zero instead, as the form does not allow for negative tax liabilities.

What are the instructions for unitary business groups (UBGs) regarding the Michigan 4568 form?

Unitary Business Groups should complete one Form 4568 for the entire group. Credits can be earned and calculated on either an entity-specific or group basis. Intercompany transactions are generally not eliminated in the calculation of most credits. It is essential for UBG members to apply credits against the group's tax liability unless otherwise specified by statute.

What should be done if there is an error in the calculations on the form?

If a total calculation results in a number less than zero, it indicates a potential error in the calculations or incorrect line entry. Taxpayers should review their entries carefully to ensure accuracy. Any discrepancies should be corrected before submitting the form as part of the tax return filing.

Filling out the Michigan 4568 form can be a daunting task, and many individuals make mistakes that can affect their tax credits and overall tax liability. One common mistake is not accurately entering the Federal Employer Identification Number (FEIN) or TR Number. This number is crucial for identifying your business, and any errors can lead to delays or complications in processing your form. Always double-check this information to ensure it matches what is on your other tax documents.

Another frequent error involves the calculation of tax credits. Many people overlook the importance of carefully subtracting the appropriate lines. For example, if there’s a negative entry on line 4b or line 15, subtracting these values can inadvertently increase your tax liability. This is a critical point because the total should never be less than zero. If it is, a calculation error has likely occurred. Taking the time to follow the instructions closely can help avoid this pitfall.

Additionally, some taxpayers fail to include all eligible credits. The Michigan 4568 form lists various nonrefundable credits, and it’s essential to claim every credit for which you qualify. Missing out on a credit can result in paying more tax than necessary. Review the eligibility criteria for each credit and ensure you are capturing all applicable deductions. This thoroughness can make a significant difference in your overall tax outcome.

Lastly, many individuals do not keep track of their calculations throughout the form. It’s easy to lose track of where you are, especially with multiple lines to fill out. Keeping a running total as you complete each section can help ensure accuracy. If you find discrepancies later, it may be challenging to pinpoint where the error occurred. By maintaining clear and organized calculations, you can reduce the likelihood of mistakes and make the filing process smoother.

The Michigan 4568 form is a crucial document for businesses seeking to summarize their nonrefundable tax credits. However, several other forms and documents often accompany it to ensure a comprehensive tax filing. Below is a list of these related forms, each serving a specific purpose in the tax process.

Understanding these forms and their interconnections is vital for maximizing available tax credits and ensuring compliance with Michigan tax regulations. Each document plays a role in the broader tax filing process, making it important to complete them accurately and timely.

The Michigan 4568 form, which summarizes nonrefundable tax credits for businesses, shares similarities with several other tax-related documents. Each of these forms serves to report tax credits or liabilities, ensuring that taxpayers can accurately calculate their tax obligations. Below is a list of documents that resemble the Michigan 4568 form in function and purpose:

Each of these forms plays a crucial role in the broader context of tax reporting and credit utilization within Michigan's tax framework. By summarizing and calculating various credits, they help taxpayers ensure compliance and optimize their tax obligations.

When filling out the Michigan 4568 form, it’s essential to follow specific guidelines to ensure accuracy and compliance. Here’s a helpful list of what to do and what to avoid:

Misconceptions about the Michigan 4568 form can lead to confusion and potential errors in tax reporting. Below are nine common misconceptions along with clarifications to help ensure accurate understanding and use of the form.

Understanding these misconceptions is crucial for accurate tax reporting and compliance with Michigan tax laws. Taxpayers should carefully review the instructions and consult with a tax professional if necessary.

Key Takeaways for Using the Michigan 4568 Form