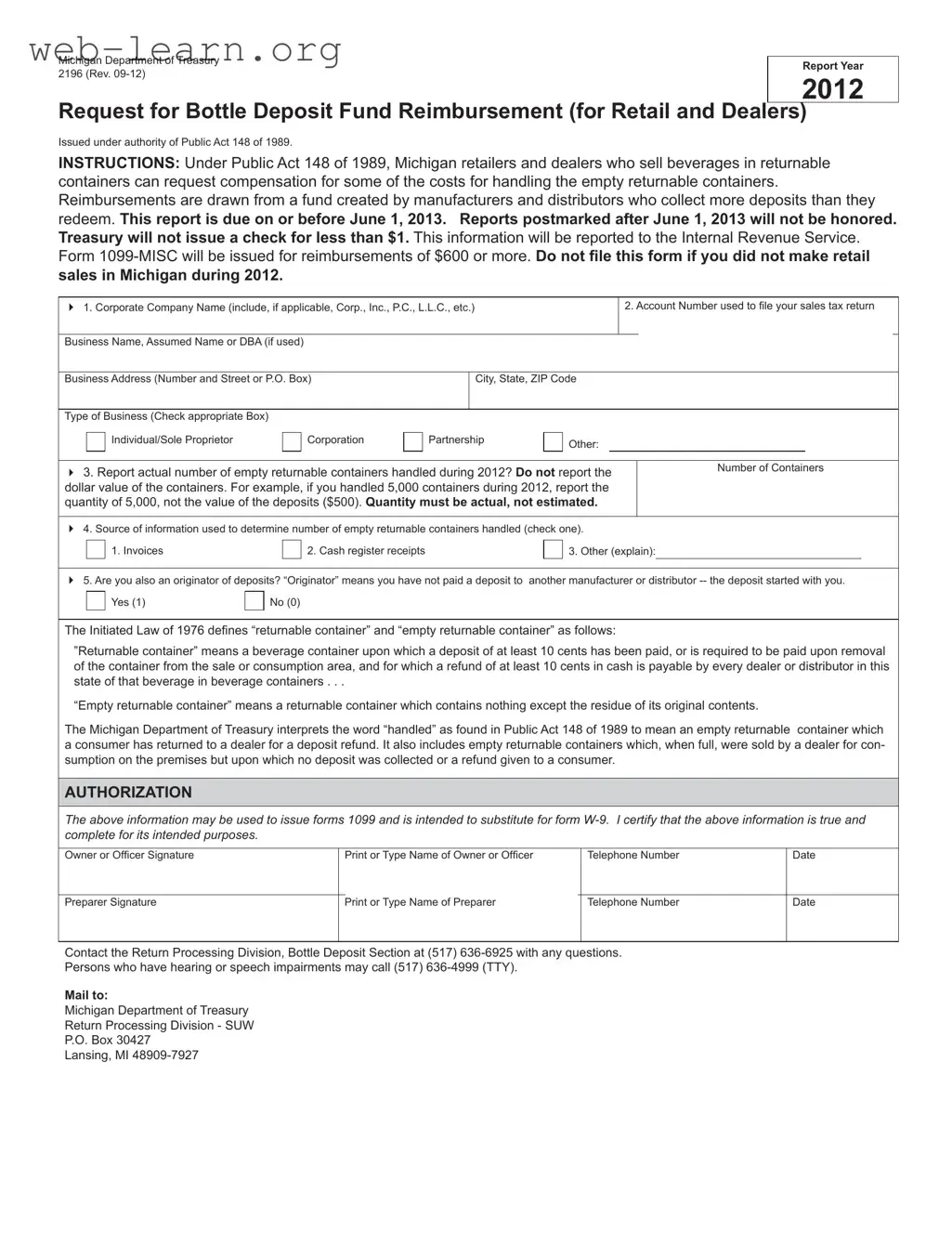

The Michigan 2196 form serves as a crucial tool for retailers and dealers engaged in the sale of beverages in returnable containers. This form allows businesses to request reimbursement for costs associated with handling empty returnable containers, a process supported by the state’s Bottle Deposit Fund. Established under Public Act 148 of 1989, the fund is financed by manufacturers and distributors who collect more deposits than they redeem. To be eligible for reimbursement, retailers must accurately report the number of empty returnable containers handled during the previous year. Key information required includes the corporate name, account number, and business address, along with specifics about the containers processed. The form must be submitted by June 1, 2013, to ensure timely processing, as late submissions will not be honored. Additionally, businesses must be aware that reimbursements below $1 will not be issued, and those exceeding $600 will trigger the issuance of a Form 1099-MISC for tax reporting purposes. Understanding the nuances of the Michigan 2196 form is essential for compliance and maximizing potential reimbursements from the state’s Bottle Deposit Fund.

Michigan Department of Treasury |

Report Year |

|

2196 (Rev. |

||

2012 |

||

|

Request for Bottle Deposit Fund Reimbursement (for Retail and Dealers)

Issued under authority of Public Act 148 of 1989.

INSTRUCTIONS: Under Public Act 148 of 1989, Michigan retailers and dealers who sell beverages in returnable containers can request compensation for some of the costs for handling the empty returnable containers. Reimbursements are drawn from a fund created by manufacturers and distributors who collect more deposits than they redeem. This report is due on or before June 1, 2013. Reports postmarked after June 1, 2013 will not be honored. Treasury will not issue a check for less than $1. This information will be reported to the Internal Revenue Service. Form

1. Corporate Company Name (include, if applicable, Corp., Inc., P.C., L.L.C., etc.) |

|

|

|

|

2. Account Number used to fi le your sales tax return |

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business Name, Assumed Name or DBA (if used) |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Business Address (Number and Street or P.O. Box) |

|

City, State, ZIP Code |

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Type of Business (Check appropriate Box) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

Individual/Sole Proprietor |

|

|

Corporation |

|

|

Partnership |

|

|

Other: |

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. Report actual number of empty returnable containers handled during 2012? Do not report the |

|

|

Number of Containers |

||||||||||||||||||

|

|

|

|

|

|

||||||||||||||||

dollar value of the containers. For example, if you handled 5,000 containers during 2012, report the |

|

|

|

|

|

|

|||||||||||||||

quantity of 5,000, not the value of the deposits ($500). Quantity must be actual, not estimated. |

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

4. Source of information used to determine number of empty returnable containers handled (check one). |

|

|

|

|

|

|

|||||||||||||||

|

|

1. Invoices |

|

|

2. Cash register receipts |

|

|

|

|

3. Other (explain): |

|

|

|||||||||

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

||||||||||||||||

5. Are you also an originator of deposits? “Originator” means you have not paid a deposit to |

another manufacturer or distributor |

||||||||||||||||||||

|

|

Yes (1) |

|

|

No (0) |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

The Initiated Law of 1976 defi nes “returnable container” and “empty returnable container” as follows:

”Returnable container” means a beverage container upon which a deposit of at least 10 cents has been paid, or is required to be paid upon removal of the container from the sale or consumption area, and for which a refund of at least 10 cents in cash is payable by every dealer or distributor in this state of that beverage in beverage containers . . .

“Empty returnable container” means a returnable container which contains nothing except the residue of its original contents.

The Michigan Department of Treasury interprets the word “handled” as found in Public Act 148 of 1989 to mean an empty returnable container which a consumer has returned to a dealer for a deposit refund. It also includes empty returnable containers which, when full, were sold by a dealer for con- sumption on the premises but upon which no deposit was collected or a refund given to a consumer.

AUTHORIZATION

The above information may be used to issue forms 1099 and is intended to substitute for form

Owner or Offi cer Signature |

|

Print or Type Name of Owner or Officer |

|

Telephone Number |

Date |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Preparer Signature |

|

Print or Type Name of Preparer |

|

Telephone Number |

Date |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Contact the Return Processing Division, Bottle Deposit Section at (517)

Persons who have hearing or speech impairments may call (517)

Mail to:

Michigan Department of Treasury

Return Processing Division - SUW

P.O. Box 30427

Lansing, MI

Bottle Deposit Fund Reimbursement Availability

INSTRUCTIONS: Under Public Act 148 of 1989, Michigan retailers and dealers who sell beverages in returnable containers can request compensation for some of the costs for handling the empty returnable containers.

Reimbursements are drawn from a fund created by manufacturers and distributors who collect more deposits than they redeem.

The payment is based on the number of empty returnable containers handled in a calendar year. Payment amounts will be known after Treasury determines how much money is available.

To apply, you must complete and mail a Request for Bottle Deposit Fund Reimbursement (Form 2196) to Treasury. Form 2196 is due on or before June 1, 2013. Use Form 2196 or contact Return Processing Division, Bottle Deposit Section, at (517)

Treasury will begin issuing checks after August 1.

| Fact Name | Fact Description |

|---|---|

| Form Purpose | The Michigan 2196 form is used to request reimbursement from the Bottle Deposit Fund for handling empty returnable containers. |

| Governing Law | This form is issued under the authority of Public Act 148 of 1989. |

| Eligibility | Retailers and dealers who sell beverages in returnable containers can apply for reimbursement. |

| Deadline for Submission | The completed form must be postmarked by June 1, 2013, to be honored. |

| Minimum Payment | Checks will not be issued for amounts less than $1. |

| IRS Reporting | Information from this form will be reported to the Internal Revenue Service. |

| Form 1099-MISC | A Form 1099-MISC will be issued for reimbursements totaling $600 or more. |

| Container Count Requirement | Applicants must report the actual number of empty returnable containers handled, not their dollar value. |

| Source of Information | Applicants must indicate the source of information used to determine the number of containers handled, such as invoices or cash register receipts. |

| Contact Information | For questions, contact the Return Processing Division, Bottle Deposit Section at (517) 636-6925. |

Filling out the Michigan 2196 form is a straightforward process that requires specific information regarding your retail or dealer operations for the year 2012. After completing the form, it should be mailed to the Michigan Department of Treasury by the designated deadline. Ensure all information is accurate to avoid delays in processing your reimbursement request.

What is the Michigan 2196 form?

The Michigan 2196 form is a request for reimbursement from the Bottle Deposit Fund, specifically designed for retailers and dealers who sell beverages in returnable containers. This form allows these businesses to seek compensation for the costs associated with handling empty returnable containers, as outlined in Public Act 148 of 1989.

Who is eligible to file the Michigan 2196 form?

Eligibility to file this form is granted to Michigan retailers and dealers who made retail sales of beverages in returnable containers during the specified reporting year. If you did not engage in such sales, you should not submit the form.

What is the deadline for submitting the Michigan 2196 form?

The completed Michigan 2196 form must be postmarked on or before June 1, 2013. Late submissions will not be honored, so it’s crucial to adhere to this deadline to ensure eligibility for reimbursement.

What information is required on the form?

When filling out the Michigan 2196 form, you will need to provide:

How is the reimbursement amount calculated?

The reimbursement amount is based on the actual number of empty returnable containers handled by the business during the calendar year. However, the total payment will depend on the funds available in the Bottle Deposit Fund, which is supported by manufacturers and distributors.

What happens if the reimbursement amount is less than $1?

The Michigan Department of Treasury will not issue checks for amounts less than $1. Therefore, if your calculated reimbursement falls below this threshold, you will not receive a payment.

Will I receive a tax form for my reimbursement?

Yes, if your total reimbursement amount is $600 or more, the Treasury will issue a Form 1099-MISC. This form will report the income to the Internal Revenue Service, so it’s important to keep accurate records of your reimbursements.

What should I do if I have questions about the form?

If you have any questions regarding the Michigan 2196 form or the reimbursement process, you can contact the Return Processing Division, Bottle Deposit Section at (517) 636-6925. For individuals with hearing or speech impairments, a TTY service is available at (517) 636-4999.

Where do I send the completed form?

Once you have completed the Michigan 2196 form, mail it to the following address:

Michigan Department of Treasury

Return Processing Division - SUW

P.O. Box 30427

Lansing, MI 48909-7927

What if I need assistance with filling out the form?

If you require assistance in completing the Michigan 2196 form, it may be beneficial to consult with a tax professional or a legal advisor who is familiar with Michigan's beverage deposit laws. They can provide guidance tailored to your specific situation.

Filling out the Michigan 2196 form can be straightforward, but mistakes can lead to delays or even denials of reimbursement requests. One common error is failing to provide the correct Corporate Company Name. This section requires the full legal name of the business, including designations like Corp., Inc., or LLC. Omitting this information or using an informal name can result in the form being rejected.

Another frequent mistake involves the Account Number. Many people either forget to include it or enter an incorrect number. This account number is essential for linking the reimbursement request to the appropriate sales tax filings. Without it, the processing team may struggle to verify your eligibility.

Accurate reporting of the number of empty returnable containers handled is crucial. Some individuals mistakenly report a dollar value instead of the actual quantity. For instance, if you handled 5,000 containers, you must write “5,000” rather than the monetary equivalent of the deposits. This misstep can lead to significant issues in processing your claim.

Additionally, many applicants fail to properly identify the source of information used to determine the number of containers handled. This section must be completed accurately, indicating whether invoices, cash register receipts, or another source was used. Leaving this blank or providing vague information can cause confusion and delay.

Another common oversight is not indicating whether the business is an originator of deposits. This question is crucial for understanding the nature of your transactions. If you are unsure about your status, it’s better to seek clarification rather than leaving the question unanswered.

Lastly, many people overlook the importance of signatures. Both the owner or officer and the preparer must sign the form. Failing to include these signatures can lead to the form being considered incomplete. Double-checking for signatures before submission can save time and prevent unnecessary complications.

The Michigan 2196 form is essential for retailers and dealers seeking reimbursement for handling empty returnable containers. Along with this form, several other documents are often required to ensure a smooth reimbursement process. Here are four important forms and documents that you may encounter:

Having these documents ready when submitting your Michigan 2196 form can streamline the reimbursement process. Each document plays a vital role in ensuring that your request is processed efficiently and accurately. Stay organized, and you can navigate the process with confidence.

The Michigan 2196 form is important for retailers and dealers involved in the beverage industry, specifically those handling returnable containers. Several other documents serve similar purposes in different contexts. Here are five documents that share similarities with the Michigan 2196 form:

When filling out the Michigan 2196 form, it is essential to follow certain guidelines to ensure your application is processed smoothly. Below is a list of things you should and shouldn't do when completing this form.

By following these guidelines, you can increase the likelihood of a successful submission. If you have any questions, don't hesitate to reach out to the Return Processing Division for assistance.

Understanding the Michigan 2196 form is crucial for retailers and dealers who handle returnable containers. However, several misconceptions can lead to confusion. Here are ten common misunderstandings about this form:

Being aware of these misconceptions can help ensure that you complete the Michigan 2196 form accurately and on time. If you have questions, consider reaching out to the Michigan Department of Treasury for clarification.

Here are some key takeaways regarding the Michigan 2196 form, which is used for requesting reimbursement from the Bottle Deposit Fund:

Following these guidelines will help ensure a smoother reimbursement process and compliance with state regulations.