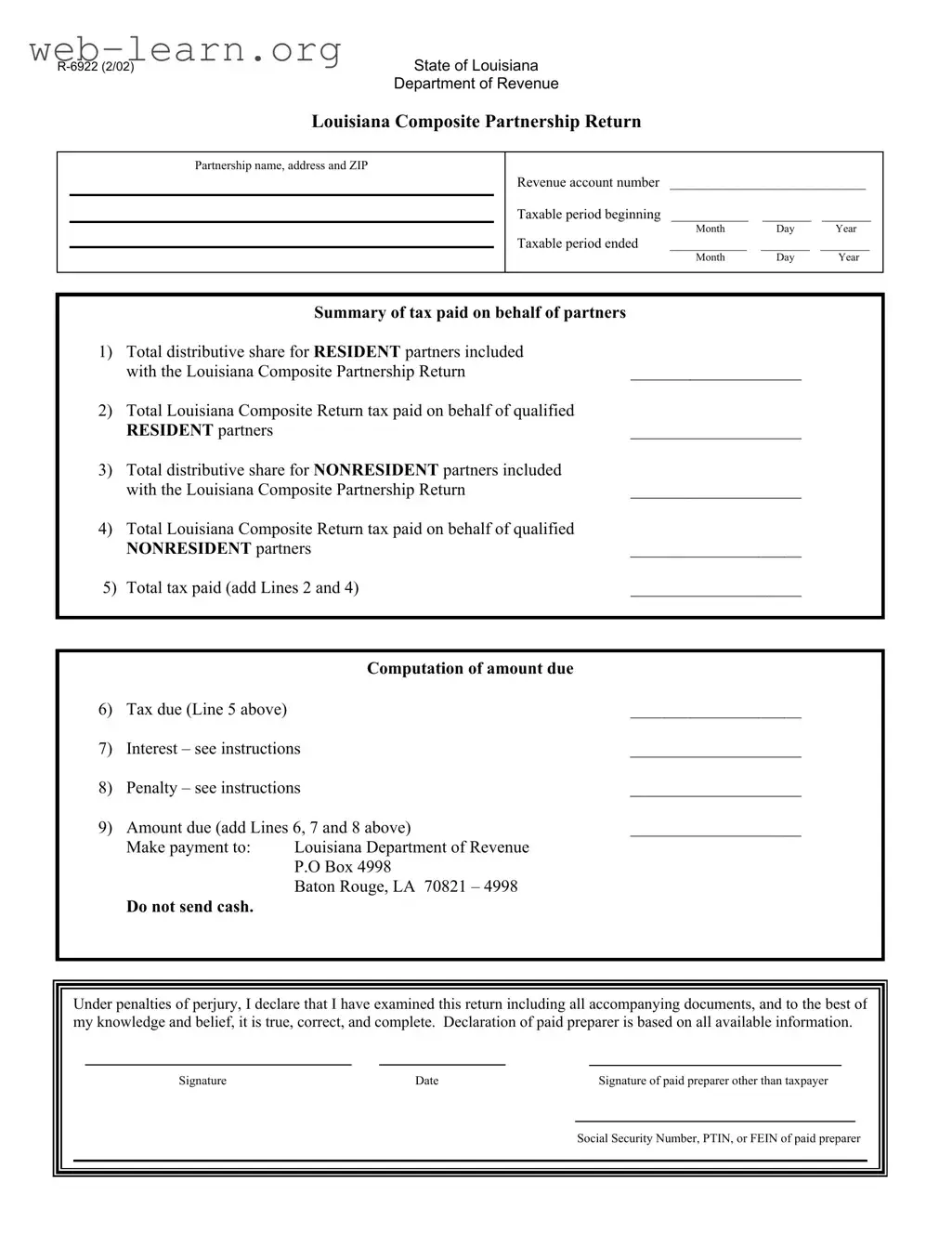

The Louisiana R 6922 form serves as a crucial document for partnerships operating within the state, facilitating the reporting of income and tax obligations for both resident and nonresident partners. This form is designed to streamline the tax process by allowing partnerships to file a composite return, thereby simplifying the tax responsibilities of individual partners. Key elements of the R 6922 include sections for detailing the partnership's name, address, and revenue account number, as well as specific taxable periods. It requires a summary of tax payments made on behalf of partners, distinguishing between resident and nonresident partners. Additionally, the form outlines the total distributive shares and the corresponding taxes paid, providing a clear breakdown of tax liabilities. The computation of the total amount due, including any interest or penalties, is also an essential part of the form. Finally, the R 6922 mandates a declaration of accuracy under penalties of perjury, ensuring accountability and compliance with Louisiana tax regulations.

State of Louisiana |

|

|

|

|

|||||

|

|

|

Department of Revenue |

|

|

|

|

||

|

|

|

Louisiana Composite Partnership Return |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

Partnership name, address and ZIP |

|

|

|

|

|

||

|

|

|

|

|

Revenue account number |

____________________________ |

|||

|

|

|

|

|

Taxable period beginning |

___________ |

_______ |

_______ |

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

Month |

Day |

Year |

|

|

|

|

|

Taxable period ended |

___________ |

_______ |

_______ |

|

|

|

|

|

|

|

|

Month |

Day |

Year |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

Summary of tax paid on behalf of partners |

|

|

|

|

||

1) |

Total distributive share for RESIDENT partners included |

|

|

|

|

||||

|

|

with the Louisiana Composite Partnership Return |

____________________ |

|

|||||

2) |

Total Louisiana Composite Return tax paid on behalf of qualified |

|

|

|

|

||||

|

|

RESIDENT partners |

|

|

|

____________________ |

|

||

3) |

Total distributive share for NONRESIDENT partners included |

|

|

|

|

||||

|

|

with the Louisiana Composite Partnership Return |

____________________ |

|

|||||

4) |

Total Louisiana Composite Return tax paid on behalf of qualified |

|

|

|

|

||||

|

|

NONRESIDENT partners |

|

|

|

____________________ |

|

||

5) |

Total tax paid (add Lines 2 and 4) |

____________________ |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

Computation of amount due |

|

6) |

Tax due (Line 5 above) |

|

____________________ |

7) |

Interest – see instructions |

____________________ |

|

8) |

Penalty – see instructions |

____________________ |

|

9) |

Amount due (add Lines 6, 7 and 8 above) |

____________________ |

|

|

Make payment to: |

Louisiana Department of Revenue |

|

|

|

P.O Box 4998 |

|

|

|

Baton Rouge, LA 70821 – 4998 |

|

Do not send cash.

Under penalties of perjury, I declare that I have examined this return including all accompanying documents, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of paid preparer is based on all available information.

Signature |

Date |

Signature of paid preparer other than taxpayer |

Social Security Number, PTIN, or FEIN of paid preparer

State of Louisiana

Department of Revenue

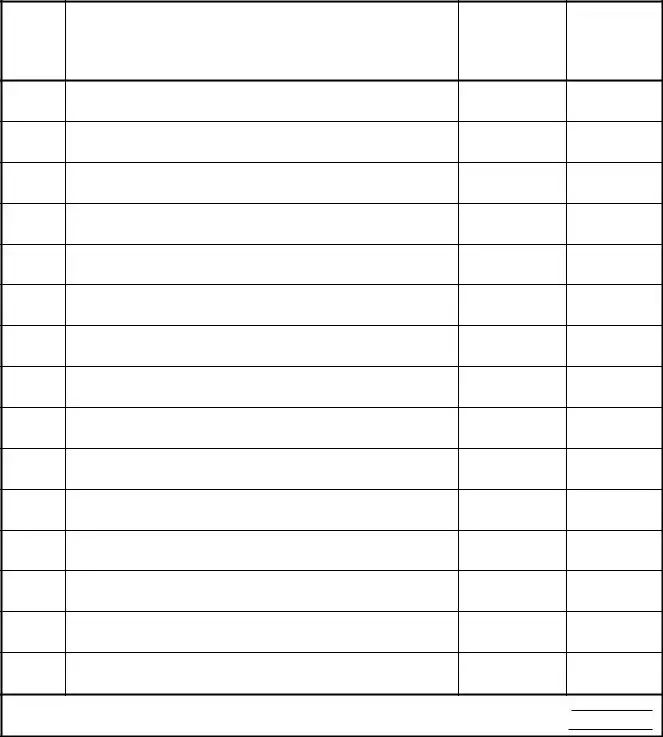

Louisiana Resident Composite Tax Return Schedule

Partnership name ____________________________ |

Page _____ of _____ |

Revenue account number______________________ |

|

Partner Number

Name and address of partner

Partner ID

number

Distributable

share

Total distributive share for resident partners included with the Louisiana Composite Return…………………

Total LA Composite Return Tax paid on behalf of qualified resident partners included with the LA Composite Return…..

State of Louisiana

Department of Revenue

Louisiana Nonresident Composite Tax Return Schedule

Partnership name ____________________________ |

|

Page ____ of ____ |

|||||||

Revenue account number______________________ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Non- |

|

|

|

Partner |

Name and address of partner |

Partner ID |

Distributable |

|

|

resident |

Included in |

||

Number |

number |

share |

|

|

partner |

Composite |

|||

|

|

agreement |

Return |

||||||

|

|

|

|

|

|||||

|

|

|

|

|

|

filed |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total distributive share for nonresident partners included with the Louisiana Composite Return………………. |

|

|

|

|

|

||||

Total LA Composite Return Tax paid on behalf of qualified nonresident partners included with the LA Composite Return…. |

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

| Fact Name | Details |

|---|---|

| Form Purpose | The Louisiana R 6922 form is used to file a composite partnership return for both resident and nonresident partners. |

| Governing Law | This form is governed by the Louisiana Revised Statutes, specifically Title 47, which pertains to taxation. |

| Tax Period | The form requires the taxable period to be specified, including the beginning and ending dates. |

| Payment Instructions | Payments must be made to the Louisiana Department of Revenue, and cash is not accepted. |

| Declaration Requirement | Taxpayers must declare under penalties of perjury that the return is true, correct, and complete. |

Completing the Louisiana R 6922 form requires attention to detail and accuracy. Once the form is filled out, it must be submitted to the Louisiana Department of Revenue along with any necessary payments. Below are the steps to guide you through the process.

What is the Louisiana R 6922 form?

The Louisiana R 6922 form is a tax document used by partnerships to report income and tax obligations for both resident and non-resident partners. This form allows partnerships to file a composite return, which simplifies the tax process for partners who may not be required to file individual returns in Louisiana.

Who needs to file the R 6922 form?

Partnerships operating in Louisiana that have both resident and non-resident partners are required to file the R 6922 form. This includes partnerships that wish to pay the tax on behalf of their partners, thus relieving them of the obligation to file separately.

What information is required on the R 6922 form?

To complete the R 6922 form, the following information is needed:

How do I calculate the tax due on the R 6922 form?

The tax due is calculated by adding the total tax paid on behalf of qualified resident partners and the total tax paid on behalf of qualified non-resident partners. This total will be found on Line 5 of the form. Additionally, any interest or penalties should be included to determine the final amount due.

Where do I send the completed R 6922 form?

The completed R 6922 form should be mailed to the Louisiana Department of Revenue at the following address:

P.O. Box 4998

Baton Rouge, LA 70821 – 4998

It is important to note that cash should not be sent with the form.

What happens if I don’t file the R 6922 form?

Failing to file the R 6922 form can result in penalties and interest charges. The Louisiana Department of Revenue may impose fines for late filing or non-filing, which can increase the overall tax liability for the partnership.

Can a paid preparer assist with the R 6922 form?

Yes, a paid preparer can assist with completing the R 6922 form. The preparer must sign the form and provide their identification number. Their declaration is based on the information provided to them, ensuring accuracy and compliance with tax laws.

Filling out the Louisiana R 6922 form can be straightforward, but several common mistakes can lead to issues. One frequent error is neglecting to include the correct revenue account number. This number is essential for the Louisiana Department of Revenue to process the return accurately. Without it, the form may be delayed or rejected.

Another common mistake involves the taxable period dates. Taxpayers often enter incorrect beginning or ending dates. It is crucial to ensure these dates align with the specific tax year being reported. Incorrect dates can result in penalties or additional interest charges.

Many people also fail to accurately calculate the total distributive shares for both resident and nonresident partners. This includes not only the amounts but also ensuring that the totals match the supporting documentation. Discrepancies can raise red flags during processing and may lead to audits.

Additionally, some filers overlook the interest and penalty calculations. These amounts are based on specific instructions provided with the form. Ignoring these details can lead to underpayment and subsequent penalties, making it essential to follow the guidelines closely.

Finally, signatures are often missing or incorrectly filled out. The declaration of the taxpayer and the paid preparer must be signed and dated. A missing signature can result in the return being considered incomplete, causing further delays in processing.

The Louisiana R-6922 form serves as the Louisiana Composite Partnership Return, a crucial document for partnerships operating within the state. This form is often accompanied by several other documents that help clarify the partnership's tax obligations and provide necessary details about its partners. Below are five commonly used forms and documents that frequently accompany the R-6922.

Each of these documents plays a vital role in ensuring that partnerships and their partners meet their tax obligations accurately. Together, they provide a comprehensive picture of the partnership's financial dealings and facilitate compliance with both state and federal tax laws.

The Louisiana R 6922 form serves a specific purpose in the realm of partnership taxation. Several other documents share similarities with it, particularly in their function and structure. Below is a list detailing these related documents:

When filling out the Louisiana R 6922 form, it's important to follow specific guidelines to ensure accuracy and compliance. Here’s a list of things you should and shouldn't do.

Misconceptions about the Louisiana R 6922 form can lead to confusion for those involved in partnership taxation. Here are six common misunderstandings:

When filling out the Louisiana R 6922 form, there are several important points to keep in mind. This form is essential for partnerships operating in Louisiana and ensures proper tax compliance. Here are key takeaways to consider:

By following these guidelines, you can ensure that the Louisiana R 6922 form is filled out correctly and submitted without issues. If you have questions, consider seeking assistance to clarify any uncertainties.