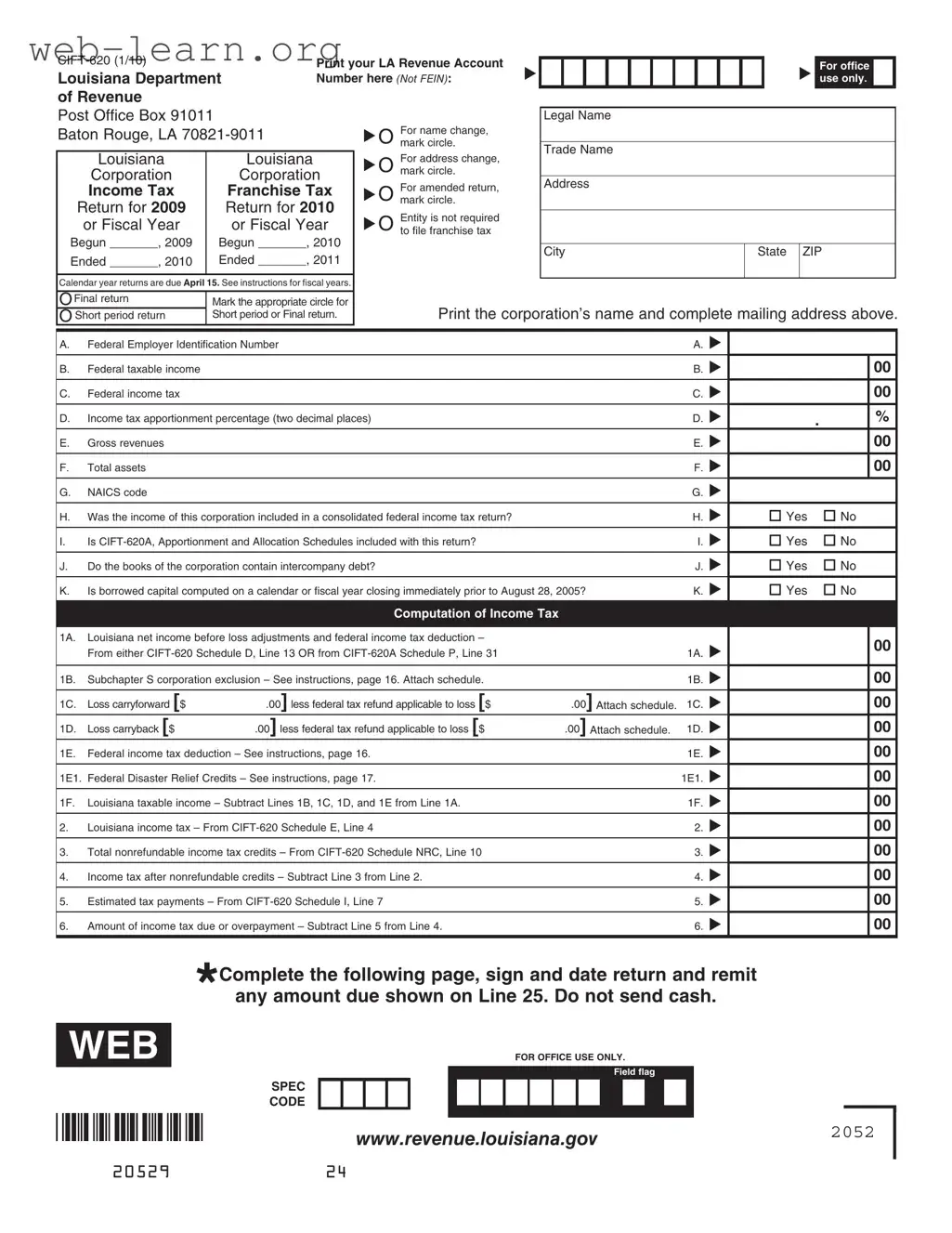

The Louisiana CIFT 620 form is an essential document for corporations operating within the state, serving as a comprehensive tax return for both income and franchise taxes. This form captures critical financial information, including federal taxable income, gross revenues, and total assets, which are pivotal for calculating the corporation's tax obligations. It also requires entities to indicate their status, such as whether they are filing an amended return or making a final submission. The form includes sections for income tax computation, detailing deductions and adjustments that affect taxable income, as well as credits that can reduce the overall tax liability. Additionally, it addresses franchise tax requirements, necessitating the reporting of capital stock and surplus, among other financial metrics. Corporations must complete various schedules associated with the CIFT 620, ensuring all relevant data is accurately reported. Timely submission is crucial, with calendar year returns due by April 15, emphasizing the importance of understanding and correctly filling out this form to remain compliant with Louisiana tax regulations.

Print your LA Revenue Account |

u |

|

|

|

|

|

|

|

|

|

|

|

Louisiana Department |

|

|

|

|

|

|

|

|

|

|

||

Number here (NOT FEIN): |

|

|

|

|

|

|

|

|

|

|

|

|

of Revenue |

|

|

|

|

|

|

|

|

|

|

|

|

u

For office use only.

Post Office Box 91011

Baton Rouge, LA

uO |

For name change, mark circle.

Legal Name

Trade Name

Louisiana

Corporation

Income Tax

Return for 2009

or Fiscal Year

Begun _______, 2009

Ended _______, 2010

Louisiana

Corporation

Franchise Tax Return for 2010 or Fiscal Year

Begun _______, 2010

Ended _______, 2011

uO |

uO |

uO |

For address change, mark circle.

For amended return, mark circle.

Entity is not required to ile franchise tax

Address

City |

State |

ZIP |

|

|

|

Calendar year returns are due April 15. See instructions for iscal years.

OFinal return |

Mark the appropriate circle for |

O Short period return |

Short period or Final return. |

Print the corporation’s name and complete mailing address above.

A. |

Federal Employer Identiication Number |

|

A. u |

|

|

|

||

|

|

|

|

|

|

|

|

|

B. |

Federal taxable income |

|

|

B. u |

|

|

00 |

|

|

|

|

|

|

|

|

|

|

C. |

Federal income tax |

|

|

C. u |

|

|

00 |

|

|

|

|

|

|

|

|

||

D. |

Income tax apportionment percentage (two decimal places) |

|

D. u |

. |

|

% |

||

E. |

Gross revenues |

|

|

E. u |

|

|

00 |

|

F. |

Total assets |

|

|

F. u |

|

|

00 |

|

G. |

NAICS code |

|

|

G. u |

|

|

|

|

|

|

|

|

|

|

|||

H. |

Was the income of this corporation included in a consolidated federal income tax return? |

|

H. u |

o Yes |

o No |

|||

I. |

Is |

|

I. u |

o Yes |

o No |

|||

J. |

Do the books of the corporation contain intercompany debt? |

|

J. u |

o Yes |

o No |

|||

K. |

Is borrowed capital computed on a calendar or iscal year closing immediately prior to August 28, 2005? |

K. u |

o Yes |

o No |

||||

|

|

Computation of Income Tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1A. |

Louisiana net income before loss adjustments and federal income tax deduction – |

|

|

u |

|

|

00 |

|

|

From either |

|

1A. |

|

|

|||

|

|

|

|

|

|

|

|

|

1B. |

Subchapter S corporation exclusion – See instructions, page 16. Attach schedule. |

|

1B. |

u |

|

|

00 |

|

|

|

|

|

|

|

|

|

|

1C. |

Loss carryforward [$ |

.00] less federal tax refund applicable to loss [$ |

.00] Attach schedule. |

1C. |

u |

|

|

00 |

1D. |

Loss carryback [$ |

.00] less federal tax refund applicable to loss [$ |

.00] Attach schedule. |

1D. |

u |

|

|

00 |

1E. |

Federal income tax deduction – See instructions, page 16. |

|

1E. |

u |

|

|

00 |

|

|

|

|

|

|

|

|

|

|

1E1. |

Federal Disaster Relief Credits – See instructions, page 17. |

|

1E1. |

u |

|

|

00 |

|

1F. |

Louisiana taxable income – Subtract Lines 1B, 1C, 1D, and 1E from Line 1A. |

|

1F. |

u |

|

|

00 |

|

2. |

Louisiana income tax – From |

|

2. |

u |

|

|

00 |

|

|

|

|

|

|

|

|

|

|

3. |

Total nonrefundable income tax credits – From |

|

3. |

u |

|

|

00 |

|

|

|

|

|

|

|

|

|

|

4. |

Income tax after nonrefundable credits – Subtract Line 3 from Line 2. |

|

4. |

u |

|

|

00 |

|

|

|

|

|

|

|

|

|

|

5. |

Estimated tax payments – From |

|

5. |

u |

|

|

00 |

|

|

|

|

|

|

|

|

|

|

6. |

Amount of income tax due or overpayment – Subtract Line 5 from Line 4. |

|

6. |

u |

|

|

00 |

|

|

|

|

|

|

|

|

|

|

*Complete the following page, sign and date return and remit

any amount due shown on Line 25. Do not send cash.

WEB

FOR OFFICE USE ONLY.

Field lag

SPEC

CODE

www.revenue.louisiana.gov2052

2052924

Print your LA Revenue Account Number here. u _____________________________

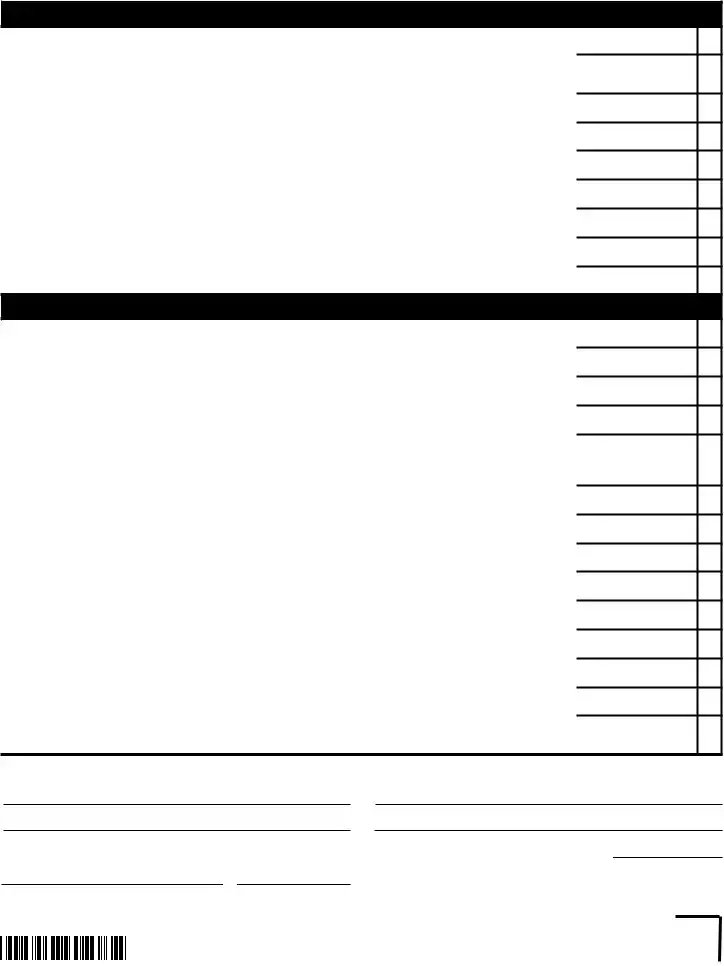

Computation of Franchise Tax

7A. |

Total capital stock, surplus, undivided proits, & borrowed capital – From |

7A. |

u |

|

|

|

|

|

|

7B. |

Franchise tax apportionment percentage – From |

|

|

|

|

Percentage must be carried out to 2 decimal places. Do not exceed 100.00%. |

7B. |

u |

. |

|

|

|

|

|

7C. |

Franchise taxable base – Multiply Line 7A by Line 7B. |

7C. |

u |

|

|

|

|

|

|

8. |

Amount of assessed value of real and personal property in Louisiana in 2009 |

8. |

u |

|

|

|

|

|

|

9. |

Louisiana franchise tax – From |

9. |

u |

|

|

|

|

|

|

10. |

Total nonrefundable franchise tax credits – From |

10. |

u |

|

|

|

|

|

|

11. |

Franchise tax after nonrefundable credits – Subtract Line 10 from Line 9. |

11. |

u |

|

|

|

|

|

|

12. |

Previous payments |

12. u |

|

|

|

|

|

|

|

13. |

Amount of franchise tax due or overpayment – Subtract Line 12 from Line 11. |

13. |

u |

|

|

Net Amount Due |

|

|

|

|

|

|

|

|

00

%

00

00

00

00

00

00

00

14. |

Total income and franchise tax due or overpayment – Add Lines 6 and 13. |

14. u |

|

|

|

|

|

15. |

Louisiana Citizens Insurance Credit – See instructions, page 17. |

15. |

u |

|

|

||

15A. Other refundable credits – From |

15A. u |

||

|

|

|

|

15B. Subtotal – Add Lines 15 and 15A and print the result. |

15B. |

u |

|

|

|

|

|

16. |

Net income and franchise taxes overpayment. If Line 14 is equal to Line 15B, print zero on |

|

|

|

Lines 16 through 23 and go to Line 24. If Line 14 is less than Line 15B, subtract Line 14 from |

|

|

|

Line 15B and print the result here. If Line 14 is greater than Line 15B, print zero on Lines 16 |

|

u |

|

through 19 and go to Line 20. – See instructions, page 17. |

16. |

|

17. |

Amount of overpayment you want to donate to The Military Family Assistance Fund |

17. |

u |

|

|

|

|

18. |

Amount of overpayment you want Refunded |

18. u |

|

|

|

|

|

19. |

Amount of overpayment you want Credited to 2010 |

19. u |

|

|

|

|

|

20. |

Amount due – If Line14 is greater than Line 15B, subtract Line 15B from Line 14 and print the result. |

20. |

u |

|

|

|

|

21. |

Delinquent iling penalty – See instructions, page 17. |

21. |

u |

|

|

|

|

22. |

Delinquent payment penalty – See instructions, page 17. |

22. |

u |

|

|

|

|

23. |

Interest – See instructions, page 17. |

23. |

u |

|

|

|

|

24. |

Additional donation to The Military Family Assistance Fund |

24. |

u |

|

|

|

|

25. |

Total amount due – Add Lines 20 through 24. |

25. |

u |

|

Make payment to Louisiana Department of Revenue. DO NOT SEND CASH. |

||

|

|

|

|

|

|

|

|

00

00

00

00

00

00

00

00

00

00

00

00

00

00

Under the penalties of perjury, I declare that I have examined this return, including all accompanying documents, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which he has any knowledge.

Print name of officer

Signature of oficer

Signature of preparer

Firm name

|

( |

) |

|

Title of oficer |

|

|

Telephone |

Date

()

Telephone

Date

WEB |

2053 |

Print your LA Revenue Account Number here. u _____________________________

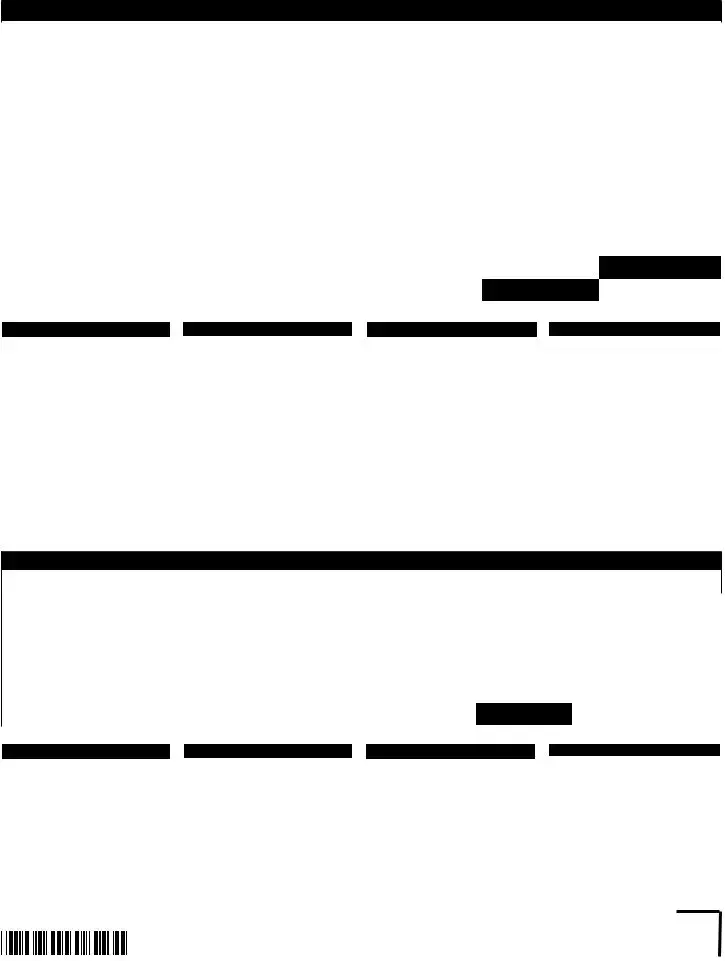

Schedule NRC – Nonrefundable Tax Credits, Exemptions, and Rebates

|

Description |

|

Code |

Corporation |

|

Corporation |

||

|

|

|

|

|

Franchise Tax (B) |

|||

|

|

|

|

Income Tax (A) |

|

|||

|

|

|

|

|

|

|

|

|

1. |

|

u |

|

|

|

00 |

|

00 |

|

|

|

|

|

|

|

|

|

2. |

|

u |

|

|

|

00 |

|

00 |

|

|

|

|

|

|

|

|

|

3. |

|

u |

|

|

|

00 |

|

00 |

|

|

|

|

|

|

|

|

|

4. |

|

u |

|

|

|

00 |

|

00 |

|

|

|

|

|

|

|

|

|

5. |

|

u |

|

|

|

00 |

|

00 |

|

|

|

|

|

|

|

|

|

6. |

|

u |

|

|

|

00 |

|

00 |

|

|

|

|

|

|

|

|

|

7. |

|

u |

|

|

|

00 |

|

00 |

|

|

|

|

|

|

|

|

|

8. |

|

u |

|

|

|

00 |

|

00 |

|

|

|

|

|

|

|

|

|

9. |

|

u |

|

|

|

00 |

|

00 |

|

|

|

|

|

|

|

|

|

10. |

Total Income Tax Credits: Add credit amounts in Column A. Print here and on |

|

|

00 |

|

|

||

|

|

|

|

|

|

|

||

11. |

Total Franchise Tax Credits: Add credit amounts in Column B. Print here and on |

|

|

|

|

00 |

||

|

|

|

|

|

|

|

|

|

For further information about these credits, please see instructions beginning on page 18.

Description |

Code |

|

Premium Tax |

100 |

|

|

|

|

Bone Marrow |

120 |

|

|

|

|

Nonviolent Offenders |

140 |

|

|

|

|

Qualiied Playgrounds |

150 |

|

|

|

|

Debt Issuance |

155 |

|

|

|

|

Contributions to |

160 |

|

Educational Institutions |

||

|

||

Donations to |

170 |

|

Public Schools |

||

|

Description |

Code |

Donations of Materials, |

|

Equipment, Advisors, |

175 |

Instructors |

|

Other |

199 |

|

|

Atchafalaya Trace |

200 |

|

|

Previously Unemployed |

208 |

|

|

Recycling Credit |

210 |

|

|

Basic Skills Training |

212 |

|

|

Dedicated Research |

220 |

|

|

New Jobs Credit |

224 |

|

|

Refunds by Utilities |

226 |

|

|

Description |

Code |

|

Eligible |

228 |

|

Neighborhood Assistance |

230 |

|

|

|

|

Cane River Heritage Area |

232 |

|

|

|

|

La Community Economic Dev |

234 |

|

Apprenticeship |

236 |

|

|

|

|

Ports of Louisiana Investor |

238 |

|

|

|

|

Ports of Louisiana Import |

240 |

|

Export Cargo |

||

|

||

Motion Picture Investment |

251 |

|

Research and Development |

252 |

|

|

|

|

Historic Structures |

253 |

|

|

|

|

Digital Interactive Media |

254 |

Description |

Code |

Motion Picture Resident |

256 |

Capital Company |

257 |

LCDFI Credit |

258 |

New Markets |

259 |

Brownields Investor |

260 |

Motion Picture Infrastructure |

261 |

Other |

299 |

Biomed/University Research |

300 |

Tax Equalization |

305 |

Manufacturing Establishments |

310 |

Enterprise Zone |

315 |

Other |

399 |

Schedule RC – Refundable Tax Credits and Rebates

|

Description |

|

Code |

Amount of Credit Claimed |

|

|

|

|

|

|

|

1. |

|

u |

F |

|

00 |

|

|

|

|

|

|

2. |

|

u |

F |

|

00 |

|

|

|

|

|

|

3. |

|

u |

F |

|

00 |

|

|

|

|

|

|

4. |

|

u |

F |

|

00 |

|

|

|

|

|

|

5. |

|

u |

F |

|

00 |

|

|

|

|

|

|

6. |

Total: Add lines 1 through 5. Print the result here and on Line 15A. |

u |

|

|

00 |

|

|

|

|

|

|

For further information about these credits, please see instructions beginning on page 20.

Description |

Code |

|

Inventory Tax |

50F |

|

Ad Valorem Natural Gas |

51F |

|

Ad Valorem Offshore Vessels |

52F |

|

Telephone Company |

54F |

|

Property |

||

|

||

|

|

|

Prison Industry Enhancement |

55F |

|

|

|

|

Urban Revitalization |

56F |

Description |

Code |

|

57F |

||

|

|

|

Milk Producers |

58F |

|

|

|

|

Technology |

59F |

|

Commercialization |

||

|

||

Angel Investor |

61F |

|

|

|

|

Musical and Theatrical |

62F |

|

Production |

||

|

||

|

|

Description |

Code |

|

Wind and Solar Energy |

64F |

|

Systems |

||

|

||

|

|

|

School Readiness Child |

65F |

|

Care Provider |

||

|

||

|

|

|

School Readiness Business |

67F |

|

- Supported Child Care |

|

|

School Readiness Fees |

|

|

and Grants to Resource |

68F |

|

and Referral Agencies |

|

Description |

Code |

|

Sugarcane Trailer Conversion |

69F |

|

|

|

|

Retention and Modernization |

70F |

|

|

|

|

Conversion of Vehicle to |

71F |

|

Alternative Fuel |

||

|

||

Research and Development |

72F |

|

|

|

|

Other Refundable |

80F |

|

|

|

WEB2054

Print your LA Revenue Account Number here. u _____________________________

All applicable schedules must be completed.

Schedule A – Balance Sheet

ASSETS |

1. Beginning of year |

2. End of year |

1.Cash

2.Trade notes and accounts receivable

3. |

Reserve for bad debts |

( |

) |

( |

) |

4. |

Inventories |

|

|

|

|

|

|

|

|

|

|

5. |

Investment in United States government obligations |

|

|

|

|

|

|

|

|

|

|

6. |

Other current assets – Attach schedule. |

|

|

|

|

|

|

|

|

|

|

7. |

Loans to stockholders |

|

|

|

|

|

|

|

|

|

|

8. |

Stock and obligations of subsidiaries |

|

|

|

|

|

|

|

|

|

|

9. |

Other investments – Attach schedule. |

|

|

|

|

|

|

|

|

|

|

10. Buildings and other ixed depreciable assets |

|

|

|

|

|

|

|

|

|

|

|

11. Accumulated amortization and depreciation |

( |

) |

( |

) |

|

12. Depletable assets |

|

|

|

|

|

|

|

|

|

|

|

13. Accumulated depletion |

( |

) |

( |

) |

|

14. Land |

|

|

|

|

|

|

|

|

|

|

|

15. Intangible assets |

|

|

|

|

|

|

|

|

|

|

|

16. Accumulated amortization |

( |

) |

( |

) |

|

17. Other assets – Attach schedule. |

|

|

|

|

|

|

|

|

|

|

|

18. Excessive reserves or undervalued assets – Attach schedule. |

|

|

|

|

|

|

|

|

|

|

|

19. Totals – Add Lines 1 through 18. |

|

|

|

|

|

Liabilities and Capital

20. Accounts payable

21. Mortgages, notes, and bonds payable one year old or less at balance sheet date and having a maturity of one year or less from original date incurred

22. Other current liabilities – Attach schedule.

23. Loans from stockholders – Attach schedule.

24. Due to subsidiaries and affiliates

25. Mortgages, notes, and bonds payable more than one year old at balance sheet date or having a maturity of more than one year from original date incurred

26. Other liabilities – Attach schedule.

27. Capital stock: a. Preferred stock

b. Common stock

28.

29. Surplus reserves – Attach schedule.

30. Earned surplus and undivided proits

31. Excessive reserves or undervalued assets

32. Totals – Add Lines 20 through 31.

WEB |

2055 |

| Fact Name | Fact Description |

|---|---|

| Form Purpose | The Louisiana CIFT 620 form is used for filing the Corporation Income Tax Return and the Corporation Franchise Tax Return for corporations operating in Louisiana. |

| Filing Deadlines | For calendar year returns, the due date is April 15. Fiscal year returns have different deadlines, which should be verified based on the specific fiscal year end. |

| Governing Laws | This form is governed by Louisiana Revised Statutes Title 47, which outlines the tax obligations for corporations within the state. |

| Required Information | Corporations must provide various financial details, including federal taxable income, gross revenues, and total assets, among others. |

| Amendments | If a corporation needs to amend its return, it can indicate this on the form. This allows for corrections to previously submitted information. |

| Nonrefundable Credits | The form allows corporations to claim nonrefundable income and franchise tax credits, which can help reduce their overall tax liability. |

Filling out the Louisiana CIFT 620 form requires careful attention to detail. Each section of the form must be completed accurately to ensure compliance with state tax regulations. Once the form is filled out, it should be signed and submitted along with any payment due.

What is the Louisiana CIFT 620 form?

The Louisiana CIFT 620 form is the state’s Corporation Income and Franchise Tax Return. Corporations operating in Louisiana must file this form to report their income and calculate their tax obligations for the state. This includes both income tax and franchise tax for the specified tax year.

Who needs to file the CIFT 620 form?

Any corporation that is registered or doing business in Louisiana is required to file the CIFT 620 form. This includes both domestic and foreign corporations. If a corporation meets certain thresholds for income or assets, it must file this form regardless of its tax liability.

When is the CIFT 620 form due?

For calendar year filers, the CIFT 620 form is due on April 15 of the following year. For fiscal year filers, the due date is the 15th day of the fourth month following the end of the fiscal year. It is important to file on time to avoid penalties and interest.

What information is required on the CIFT 620 form?

The form requires various pieces of information, including:

Additionally, the form includes sections for calculating income tax and franchise tax, as well as any applicable credits.

What if I need to amend my CIFT 620 form?

If you discover an error after filing, you can amend your CIFT 620 form. You should mark the appropriate circle on the form to indicate that it is an amended return. Be sure to provide corrected information and any necessary schedules.

Are there penalties for late filing?

Yes, there are penalties for late filing of the CIFT 620 form. If the form is not filed by the due date, the corporation may face penalties and interest on any unpaid tax amounts. It is advisable to file even if you cannot pay the full amount owed to minimize penalties.

Can I make payments online?

Yes, corporations can make tax payments online through the Louisiana Department of Revenue’s website. It is recommended to keep a record of any payments made for your records.

Where do I send the completed CIFT 620 form?

The completed CIFT 620 form should be sent to the Louisiana Department of Revenue at the address provided on the form. It is important to ensure that the form is mailed to the correct address to avoid delays in processing.

Filling out the Louisiana CIFT 620 form can be a complex task. Many individuals make common mistakes that can lead to delays or issues with their tax filings. Understanding these mistakes can help ensure a smoother process.

One frequent error is failing to enter the correct Louisiana Revenue Account Number. This number is essential for identifying the corporation and ensuring that the return is processed correctly. Omitting or incorrectly entering this number can result in significant delays.

Another common mistake is neglecting to check the appropriate boxes for name or address changes. If there have been any changes, marking the correct circle is crucial. Failing to do so can lead to confusion and miscommunication with the Louisiana Department of Revenue.

Many filers also forget to include required schedules, such as the CIFT-620A Apportionment and Allocation Schedules. This omission can lead to incomplete submissions, resulting in penalties or additional inquiries from the tax authority.

Incorrectly calculating the federal taxable income is another mistake that often occurs. It is vital to ensure that this figure is accurate, as it directly impacts the corporation’s tax liability. Errors in this calculation can lead to overpayment or underpayment of taxes.

Some individuals make the mistake of not providing the correct apportionment percentage. This percentage must be expressed to two decimal places. An incorrect entry can affect the corporation’s tax obligations and lead to further complications.

Additionally, filers sometimes forget to sign and date the return. This step is crucial, as an unsigned return may be considered invalid. It is essential to ensure that all required signatures are included before submission.

Another common error is not reviewing the instructions thoroughly. Each section of the form has specific requirements and guidelines. Overlooking these can result in incomplete or incorrect filings.

Finally, failing to keep a copy of the submitted form for personal records is a mistake that can have long-term consequences. Having a copy can be invaluable for future reference or in case of any disputes with the tax authority.

By avoiding these common mistakes, individuals can enhance the accuracy of their Louisiana CIFT 620 form submissions and minimize the risk of complications with their tax filings.

The Louisiana CIFT 620 form is an important document for corporations filing their income tax returns in Louisiana. Along with this form, several other documents may be required to ensure compliance with state tax regulations. Below is a list of forms and documents that are often used in conjunction with the CIFT 620 form.

These additional forms and schedules provide crucial information needed to accurately complete the CIFT 620 form and ensure compliance with Louisiana tax laws. It is important for corporations to gather all necessary documents before filing to avoid any issues with their tax returns.

When filling out the Louisiana CIFT 620 form, there are several important considerations to keep in mind. Here’s a list of things you should and shouldn’t do:

The Louisiana CIFT 620 form is essential for corporations operating in Louisiana, but several misconceptions often lead to confusion. Here are ten common misunderstandings about this form:

Understanding these misconceptions can help corporations navigate their tax obligations more effectively and avoid potential pitfalls associated with the CIFT 620 form.

Here are key takeaways for filling out and using the Louisiana CIFT 620 form: