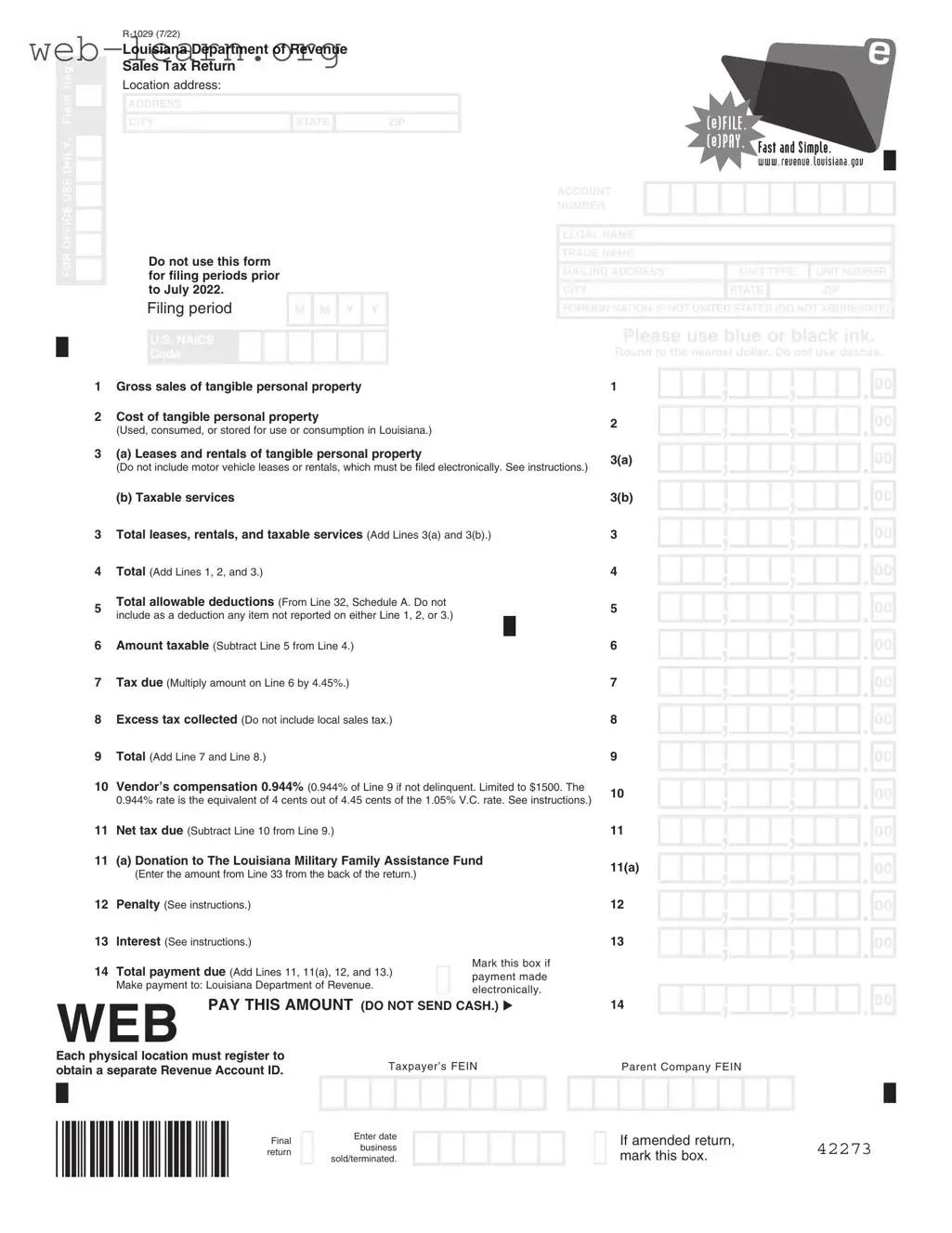

The Louisiana 1029 Sales form is an essential document for businesses operating within the state, designed to facilitate the reporting of sales tax obligations. This form must be used for filing periods beginning in August 2020 and onward, ensuring compliance with state regulations. It requires businesses to report gross sales of tangible personal property, along with costs associated with items used or consumed in Louisiana. In addition to sales, the form also accounts for leases, rentals, and services, excluding motor vehicle transactions, which must be filed electronically. Key calculations on the form include total sales, allowable deductions, and the resulting taxable amount, which is then used to determine the tax due at a rate of 4.45%. Vendors can claim compensation based on the total payment due, with specific limits and conditions outlined. Furthermore, businesses have the opportunity to contribute to the Louisiana Military Family Assistance Fund, providing a way to support local communities while fulfilling tax obligations. Overall, the Louisiana 1029 Sales form serves as a comprehensive tool for businesses to accurately report their sales tax and maintain compliance with state laws.

FOR OFFICE USE ONLY. Field flag

|

|

|

Louisiana Department of Revenue |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

Sales Tax Return |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

Location address: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

ADDRESS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

CITY |

|

|

STATE |

|

|

|

ZIP |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ACCOUNT |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NUMBER |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

LEGAL NAME |

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Do not use this form |

|

|

|

|

|

|

|

TRADE NAME |

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

for filing periods |

prior |

|

|

|

|

|

|

|

MAILING ADDRESS |

UNIT TYPE |

UNIT NUMBER |

||||||||||||||||||

|

|

|

|

to July 2022. |

|

|

|

|

|

|

|

|

|

|

|

|

|

CITY |

|

|

|

|

|

STATE |

|

|

|

ZIP |

|||||

|

|

|

|

Filing period |

|

|

M |

M |

Y |

Y |

|

|

|

|

FOREIGN NATION, IF NOT UNITED STATES (DO NOT ABBREIVATE) |

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Please use blue or black ink. |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

U.S. NAICS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Round to the nearest dollar. Do not use dashes. |

|||||||||||||

1 |

|

Gross sales of tangible personal property |

|

|

|

|

|

|

|

|

1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

2 |

|

Cost of tangible personal property |

|

|

|

|

|

|

|

|

2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

(Used, consumed, or stored for use or consumption in Louisiana.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

3 |

|

(a) Leases and rentals of tangible personal property |

|

|

|

|

3(a) |

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

(Do not include motor vehicle leases or rentals, which must be filed electronically. |

See instructions.) |

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

(b) Taxable services |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3(b) |

|

|

|

|

|

|

|

|

|

|||||||

3 |

|

Total leases, rentals, and taxable services (Add Lines 3(a) and 3(b).) |

|

|

|

3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

4 |

|

Total (Add Lines 1, 2, and 3.) |

|

|

|

|

|

|

|

|

4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

5 |

|

Total allowable deductions (From Line 32, Schedule A. Do not |

|

|

|

|

5 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

include as a deduction any item not reported on either Line 1, 2, or 3.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

6 |

|

Amount taxable (Subtract Line 5 from Line 4.) |

|

|

|

|

|

|

|

|

6 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

7 |

|

Tax due (Multiply amount on Line 6 by 4.45%.) |

|

|

|

|

|

|

|

|

7 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

8 |

|

Excess tax collected (Do not include local sales tax.) |

|

|

|

|

8 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

9 |

|

Total (Add Line 7 and Line 8.) |

|

|

|

|

|

|

|

|

9 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

10 |

Vendor’s compensation 0.944% (0.944% of Line 9 if not delinquent. Limited to $1500. The |

10 |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

0.944% rate is the equivalent of 4 cents out of 4.45 cents of the 1.05% V.C. rate. See instructions.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

11 |

Net tax due (Subtract Line 10 from Line 9.) |

|

|

|

|

|

|

|

|

11 |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

11 |

(a) Donation to The Louisiana Military Family Assistance Fund |

|

|

|

11(a) |

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

|

|

|

(Enter the amount from Line 33 from the back of the return.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

12 |

Penalty (See instructions.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12 |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

13 |

Interest (See instructions.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13 |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

14 |

Total payment due (Add Lines 11, 11(a), 12, and 13.) |

|

|

Mark this box if |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

payment made |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

Make payment to: Louisiana Department of Revenue. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

electronically. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

WEB |

PAY THIS AMOUNT (DO NOT SEND CASH.) u |

14 |

|

|

Each physical location must register to

obtain a separate Revenue Account ID. |

|

|

|

|

Taxpayer’s FEIN |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Final |

|

|

|

Enter date |

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

business |

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

return |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

sold/terminated. |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Parent Company FEIN

If amended return, |

42273 |

|

mark this box. |

||

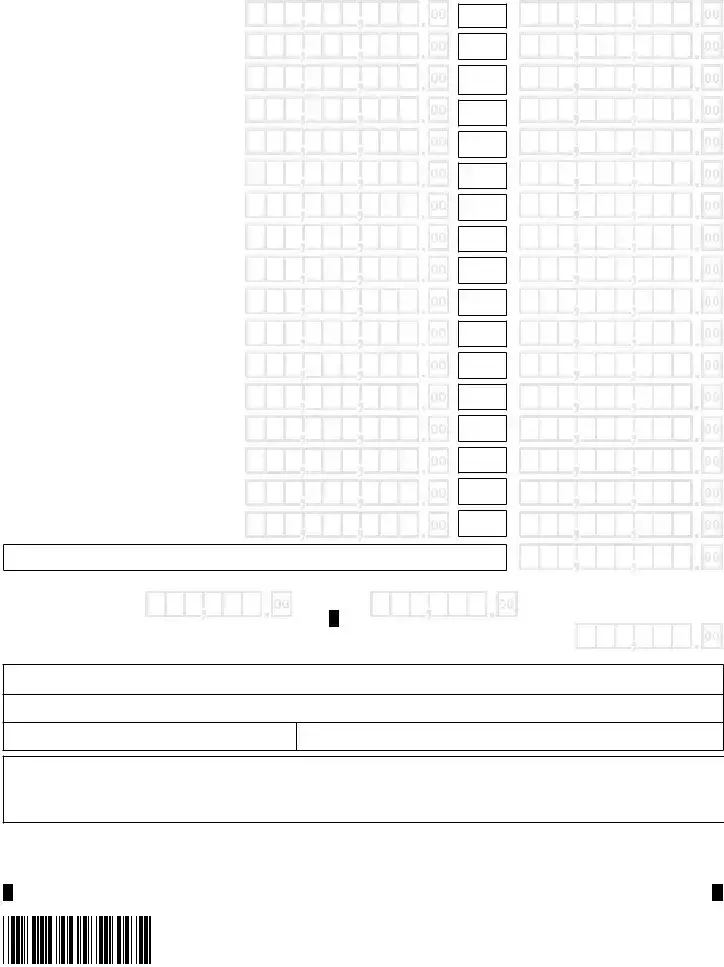

|

Allowable Deductions – Schedule A |

Total Sales |

|||

|

||||

|

|

|

|

|

15 |

Intrastate telecommunication services |

|

|

|

|

(Do not include prepaid telephone cards.) |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

16 |

Interstate telecommunication services |

|

||

|

|

|

|

|

|

|

|

|

|

17 |

Prepaid telephone cards |

|

||

|

|

|

|

|

|

|

|

|

|

18 |

Electricity and natural gas or energy for non- |

|

||

|

residential use |

|

||

|

|

|

|

|

|

|

|

|

|

19 |

Steam and bulk or utility water used for non- |

|

||

|

residential purposes |

|

||

|

|

|

|

|

|

|

|

|

|

20 |

Boiler fuel for nonresidential use |

|

||

|

(See instructions.) |

|

||

|

|

|

|

|

|

|

|

|

|

21 |

Sales/purchase/leases/rentals of manufactur- |

|

||

|

ing machinery or equipment |

|

||

|

|

|

|

|

22 |

Sales to U. S. government and Louisiana |

|

||

|

state and local government agencies |

|

||

|

|

|

|

|

|

|

|

|

|

23 |

Sales of prescription drugs |

|

||

|

|

|

|

|

|

|

|

|

|

24 |

Sales of food for home consumption |

|

||

|

|

|

|

|

|

|

|

|

|

25 |

Electricity, natural gas, and bulk water for |

|

||

|

residential use |

|

||

|

|

|

|

|

|

|

|

|

|

26 |

Sales in interstate commerce |

|

||

|

|

|

|

|

|

|

|

|

|

27 |

Sales for resale |

|

||

|

|

|

|

|

|

|

|

|

|

28 |

Cash discounts, sales returns and |

|

||

|

allowances |

|

||

|

|

|

|

|

29 |

Tangible personal property sold for lease or |

|

||

|

rental (See instructions.) |

|

||

|

|

|

|

|

|

|

|

|

|

30 |

Sales of gasoline, diesel, and motor fuel |

|

||

|

(Sales for resale must be reported on Line 27.) |

|

||

|

|

|

|

|

31 |

Total from SCHEDULE |

|

||

|

(Transactions taxed at 0%.) |

|

||

|

|

|

|

|

Percent Exempt

22.472%

44.944%

22.472%

55.056%

55.056%

55.056%

100%

100%

100%

100%

100%

100%

100%

100%

100%

100%

100%

32 Add Lines 15 through 31; enter here and on Line 5.

33(a) Donation of Vendor’s Compensation |

33(b) Donation in Addition to Tax Due |

|

The Military Family |

|

|

Assistance Fund |

|

|

Worksheet |

|

|

33 Total Donation (Add Lines 33(a) and 33(b)) Enter here and on Line 11(a) on front of return |

33 |

|

Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and belief, they are true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

Signature

Print Name

|

Date (mm/dd/yyyy) |

Title |

Telephone |

|

|

PAID

PREPARER USE ONLY

Print Preparer’s Name |

Preparer’s Signature |

Date (mm/dd/yyyy) |

Check if |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Firm’s Name ➤ |

|

|

|

|

|

|

|

|

|

|

|

|

Firm’s EIN ➤ |

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Firm’s Address ➤ |

|

|

|

|

|

|

|

|

|

|

|

|

Telephone ➤ |

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PTIN, FEIN, or LDR account |

For Office |

number of paid preparer |

Use Only. |

Louisiana Department of Revenue Post Office Box 3138 |

Baton Rouge, LA |

This return is due on or before the 20th day following the taxable period covered and becomes delinquent on |

42274 |

|

the first day thereafter. If the |

due date falls on a weekend or holiday, the return is due the next business day and |

|

becomes delinquent the first |

day thereafter. |

|

| Fact Name | Details |

|---|---|

| Form Purpose | The Louisiana 1029 Sales form is used to report sales tax for tangible personal property and certain services sold in Louisiana. |

| Filing Period | This form should not be used for filing periods prior to August 2020, ensuring compliance with the latest tax regulations. |

| Tax Rate | The sales tax rate applied is 4.45% on the taxable amount calculated on the form. |

| Vendor's Compensation | Vendors may claim compensation of 0.944% of the total payment due, capped at $1,500, provided they are not delinquent. |

| Allowable Deductions | Taxpayers can deduct certain items from their gross sales, including sales to the U.S. government and sales of prescription drugs. |

| Governing Laws | The Louisiana 1029 Sales form is governed by the Louisiana Revised Statutes Title 47, which outlines the state's tax laws. |

Filling out the Louisiana 1029 Sales form is an important task that requires attention to detail. The form must be completed accurately to ensure compliance with state tax regulations. Below are the steps to guide you through the process of filling out this form effectively.

After completing the form, ensure you keep a copy for your records. Submit the form to the Louisiana Department of Revenue by the due date, which is the 20th day following the taxable period. If you have any questions or need further assistance, consider reaching out to a tax professional or the Louisiana Department of Revenue for guidance.

What is the Louisiana 1029 Sales form?

The Louisiana 1029 Sales form is a sales tax return used by businesses to report and remit sales tax to the Louisiana Department of Revenue. It is specifically designed for reporting sales made within the state and is applicable for filing periods starting from August 2020.

Who needs to file the Louisiana 1029 Sales form?

Any business that sells tangible personal property, leases, or provides services in Louisiana must file this form. Each physical location of a business must register separately and obtain a Revenue Account ID.

What information is required to complete the form?

To complete the Louisiana 1029 Sales form, businesses need to provide:

How do I calculate the tax due on the Louisiana 1029 Sales form?

To calculate the tax due, first determine the amount taxable by subtracting the total allowable deductions from the total gross sales. Then, multiply the taxable amount by the sales tax rate of 4.45%. This will give you the tax due before any deductions for vendor compensation.

Are there any allowable deductions I can claim?

Yes, several deductions are allowed on the Louisiana 1029 Sales form. These include sales to government agencies, sales of prescription drugs, sales for resale, and sales of food for home consumption, among others. A complete list of allowable deductions can be found in Schedule A of the form.

What should I do if I need to amend my return?

If you need to amend your return, you should mark the appropriate box on the form. Ensure that you provide the corrected information and submit it to the Louisiana Department of Revenue as soon as possible to avoid penalties.

When is the Louisiana 1029 Sales form due?

The form is due on or before the 20th day following the end of the taxable period covered. If the due date falls on a weekend or holiday, the return is due the next business day. Late submissions will incur penalties.

How can I make a payment for the tax due?

Payments can be made electronically to the Louisiana Department of Revenue. It is important to avoid sending cash. Follow the instructions on the form for the proper payment methods.

What if I have more questions about the form?

If you have further questions about the Louisiana 1029 Sales form, it is advisable to consult the instructions provided with the form or contact the Louisiana Department of Revenue directly for assistance.

Filling out the Louisiana 1029 Sales form can be straightforward, but many make common mistakes that can lead to delays or issues with the submission. One frequent error is not using the correct filing period. This form is only for periods after August 2020. If you mistakenly select an earlier period, your return will be rejected.

Another common mistake involves the use of ink. The instructions clearly state to use blue or black ink. Using any other color can cause problems with processing your form. Additionally, some people forget to round their numbers to the nearest dollar. This is important because cents are not accepted on the form.

Many individuals also overlook the requirement to mark the box if it is an amended return. Failing to do so can lead to confusion and delays in processing. Furthermore, when calculating the total allowable deductions, it’s essential to ensure that only items reported on Lines 1 through 3 are included. Including unrelated deductions can result in incorrect tax calculations.

Some filers neglect to double-check their math. Simple arithmetic errors can lead to significant discrepancies in the tax due. It’s wise to review each line carefully to avoid these mistakes. Similarly, people sometimes forget to sign the form. A missing signature can delay the processing of your return.

Another issue arises when entering the Taxpayer’s FEIN. Ensure that the number is correct and matches the name on the form. Errors in this area can complicate the identification of your account. Additionally, when reporting vendor’s compensation, some forget that it is limited to $1,500. Exceeding this limit can lead to penalties.

Lastly, remember to make the payment electronically and not to send cash. Not following this instruction can result in your payment being rejected. By avoiding these common mistakes, you can ensure a smoother filing process for your Louisiana 1029 Sales form.

The Louisiana 1029 Sales form is a critical document for businesses operating in Louisiana, specifically for reporting sales tax. However, it is often accompanied by other forms and documents that provide additional information or serve specific purposes in the sales tax process. Below is a list of five such documents commonly used alongside the Louisiana 1029 Sales form.

Understanding these accompanying forms and documents is essential for businesses to navigate the sales tax filing process in Louisiana effectively. Proper use of the Louisiana 1029 Sales form and its related documents helps ensure compliance with state tax laws and minimizes the risk of errors in reporting.

The Louisiana 1029 Sales form shares similarities with several other documents used for tax reporting and sales transactions. Here are five documents that are comparable:

When filling out the Louisiana 1029 Sales form, attention to detail is crucial. Here’s a list of practices to follow and avoid to ensure accuracy and compliance.

By adhering to these guidelines, you can navigate the form-filling process more smoothly and reduce the likelihood of errors or delays in processing your return.

This form is specifically designed for filing periods starting from August 2020. Using it for earlier periods is not permitted.

Different types of sales and services are reported on separate lines. For instance, tangible personal property and leases are categorized differently.

Deductions must come from specific lines outlined in the instructions. Items not reported on Lines 1 through 3 cannot be deducted.

Late submissions incur penalties, and it’s important to file on time to avoid these additional costs.

Cash payments are not accepted. Payments must be made electronically or through other specified methods.

The compensation is calculated as a percentage of the total payment due, up to a maximum limit. It varies based on the amount reported.

Each physical location must register for a separate Revenue Account ID. This is crucial for compliance with state regulations.