When entering into a financial arrangement, understanding the intricacies of a Loan Agreement form is crucial for both borrowers and lenders. This document serves as a binding contract that outlines the terms and conditions governing a loan. Key elements typically included in this form are the loan amount, interest rate, repayment schedule, and any applicable fees. Moreover, both parties must agree on the consequences of late payments or defaults, ensuring transparency and mutual understanding. Additionally, borrowers are often required to provide specific information, such as their financial status and credit history, while lenders may need to disclose their own terms and conditions. The Loan Agreement not only protects the interests of both parties but also provides a clear framework to resolve any potential disputes that may arise during the loan's duration. By carefully reviewing and comprehending each section of this form, individuals can foster a more confident borrowing experience while mitigating the risks associated with lending. Navigating the complexities of a Loan Agreement form does not have to be daunting; instead, it can be an opportunity for both sides to establish a trustworthy financial relationship grounded in clear communication and well-defined expectations.

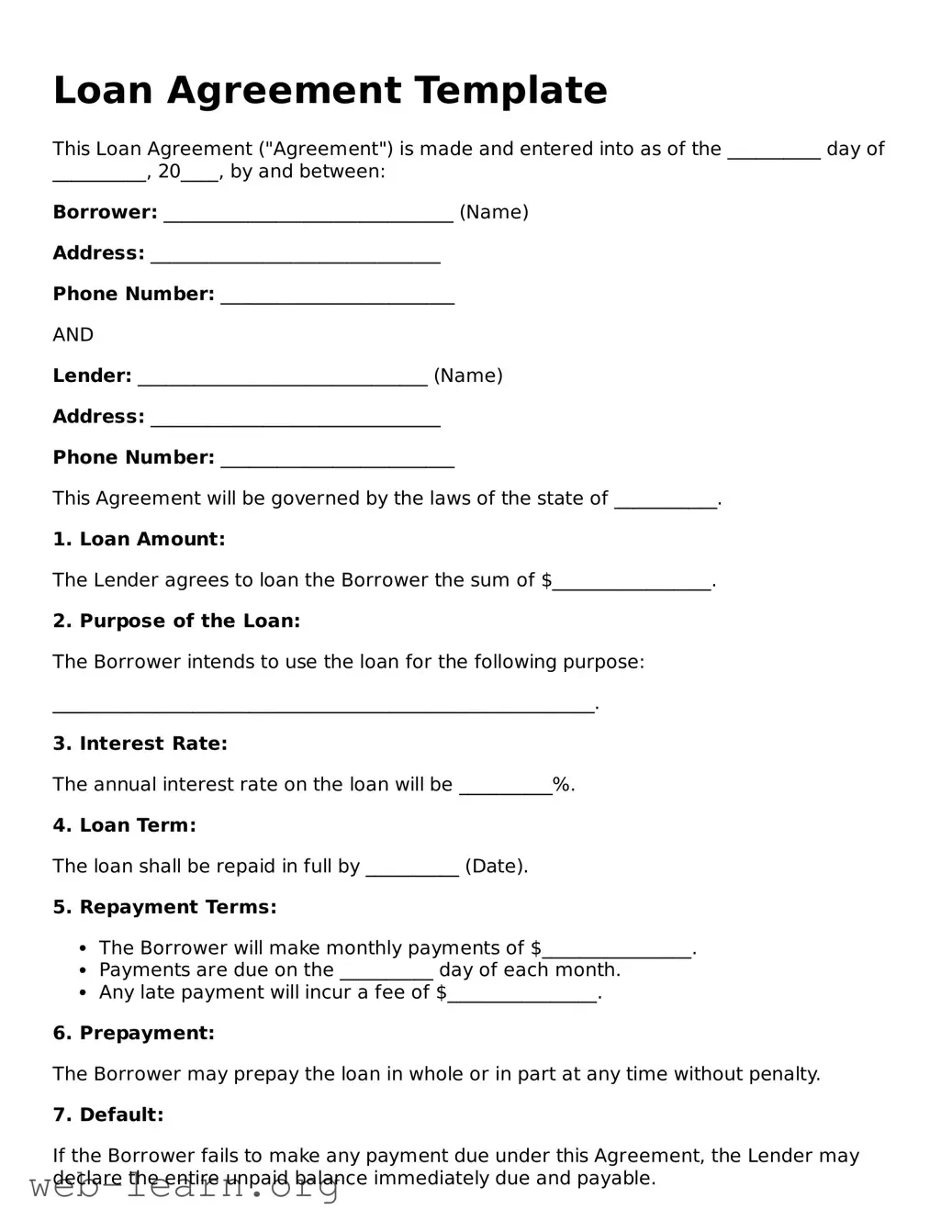

Loan Agreement Template

This Loan Agreement ("Agreement") is made and entered into as of the __________ day of __________, 20____, by and between:

Borrower: _______________________________ (Name)

Address: _______________________________

Phone Number: _________________________

AND

Lender: _______________________________ (Name)

Address: _______________________________

Phone Number: _________________________

This Agreement will be governed by the laws of the state of ___________.

1. Loan Amount:

The Lender agrees to loan the Borrower the sum of $_________________.

2. Purpose of the Loan:

The Borrower intends to use the loan for the following purpose:

__________________________________________________________.

3. Interest Rate:

The annual interest rate on the loan will be __________%.

4. Loan Term:

The loan shall be repaid in full by __________ (Date).

5. Repayment Terms:

6. Prepayment:

The Borrower may prepay the loan in whole or in part at any time without penalty.

7. Default:

If the Borrower fails to make any payment due under this Agreement, the Lender may declare the entire unpaid balance immediately due and payable.

8. Governing Law:

This Agreement shall be governed by the laws of the state of __________.

9. Signatures:

The parties have executed this Loan Agreement as of the date first above written.

Borrower Signature: _______________________________

Date: __________

Lender Signature: _______________________________

Date: __________

| Fact Name | Details |

|---|---|

| Definition | A Loan Agreement is a legal document between a borrower and a lender outlining the terms of a loan. |

| Purpose | This form establishes the responsibilities and rights of both parties involved in the loan transaction. |

| Governing Law | The agreement is typically governed by the laws of the state in which the loan is made. |

| Key Components | It often includes loan amount, interest rate, repayment schedule, and collateral details. |

| Signature Requirement | Both the borrower and lender must sign the agreement for it to be legally binding. |

| Amendments | Any changes to the terms need to be documented in writing and signed by both parties. |

| Dispute Resolution | The agreement may specify how disputes will be handled, including mediation or arbitration procedures. |

Filling out a Loan Agreement form requires careful attention to detail to ensure that all necessary information is correctly provided. Completing the form accurately will facilitate the loan process and clarify the terms of the agreement.

A Loan Agreement is a legal document that outlines the terms under which one party provides a loan to another. It details the amount of the loan, the interest rate, repayment schedule, and any collateral required. This contract protects both the lender and the borrower by ensuring clarity on the obligations involved.

Having a Loan Agreement is crucial for several reasons. It formalizes the lending process, reduces the chances of disputes, and provides legal protection. Without this agreement, misunderstandings can arise regarding repayment terms, interest rates, or consequences for missed payments.

Yes, a Loan Agreement can be modified if both parties agree to the changes. It's essential to document any modifications in writing, ensuring both parties sign the revised agreement. This helps prevent future disputes over altered terms.

A well-drafted Loan Agreement prevents misunderstandings by clearly stating each party's rights and responsibilities. For the lender, it provides assurance that the borrower will repay the loan as agreed. For the borrower, it offers protection against unfair lending practices and unexpected changes to loan terms.

If the borrower defaults, the lender has the right to take specific actions as outlined in the agreement. This might include imposing late fees, demanding full repayment, or taking possession of the collateral if one was required. It’s important for borrowers to understand these consequences before signing.

While it’s not legally required to have a lawyer examine a Loan Agreement, it is highly advisable. An attorney can ensure that the terms are fair, clarify legal implications, and help protect your interests. This can prevent potential conflicts down the line.

Yes, Loan Agreements are typically enforceable in court as long as they adhere to lawful terms and conditions. If a dispute arises and the parties cannot resolve it, the agreement can be presented in court for resolution. This underscores the importance of drafting a comprehensive and clear agreement.

Before signing, take time to carefully read through the entire agreement. Make sure you understand all the terms, ask questions if needed, and consider having a legal professional review it. Always ensure that the agreement reflects what was verbally discussed and agreed upon with the lender.

Filling out a Loan Agreement form can be a straightforward process, but many people make mistakes that could lead to issues down the line. One common mistake is failing to read the entire agreement before signing. Skimming through the document may lead to misunderstanding key terms and conditions, which can result in unwanted surprises after the loan is finalized.

Another frequent error is incorrect personal information. Individuals often overlook entering accurate details such as their name, address, or Social Security number. One small typo can create significant delays in processing and may even raise questions about the borrower's eligibility.

Many applicants also forget to specify the loan amount or miscalculate what they need. This can lead to borrowing more than necessary, resulting in higher interest payments, or less, which might not cover the intended expenses. Being precise is crucial.

In addition to the loan amount, skipping the purpose of the loan can create a negative impression on lenders. Clearly explaining why the money is needed can build trust and demonstrate a borrower’s responsibility. Assumptions about the lender knowing the purpose are misguided.

Failure to include all required documentation is another common pitfall. Lenders often require financial statements, proof of income, and other supporting documents. Not providing these can lead to a denial of the application.

Misunderstanding or misrepresenting income is also a concern. Some people might exaggerate their earnings or neglect to mention additional financial obligations. This can affect the lender's assessment of their ability to repay the loan.

A failure to review the repayment terms can result in confusion regarding monthly payments and interest rates. Borrowers should be clear on when payments are due and what the consequences of late payments are.

People often forget to ask questions before signing the agreement. If there are unclear aspects, it is essential to seek clarification from the lender. Ignoring uncertainties can lead to regret later.

Not keeping a copy of the signed Loan Agreement is a mistake that can haunt borrowers. Documentation is vital for future reference, especially if disputes arise regarding terms or payments.

Finally, many applicants neglect to follow up after submitting the form. It is essential to confirm that the loan application has been received and is being processed. This can prevent unneeded stress and ensure a smooth borrowing experience.

A Loan Agreement is a crucial document for establishing the terms of a financial transaction between a lender and a borrower. However, it often works in tandem with a variety of other forms and documents to ensure the agreement is comprehensive and legally sound. Below is a list of commonly associated documents that may be utilized alongside a Loan Agreement.

Having these documents in place alongside a Loan Agreement can enhance clarity and protection for both parties involved. It is important to review the specific requirements in your area, as local laws may dictate which documents are necessary in each financial transaction.

Promissory Note: This document establishes a borrower's promise to repay a loan. Much like a loan agreement, it specifies the amount borrowed, interest rates, and repayment terms.

Mortgage Agreement: This is a specific type of loan agreement tied to real estate. It outlines the loan terms and includes details about the collateral (the property) securing the loan.

Secured Loan Agreement: In this document, a loan is backed by collateral. Similar to a regular loan agreement, it details the loan amount and repayment schedule, but also specifies the assets at risk if repayment fails.

Interest Rate Lock Agreement: This agreement allows a borrower to lock in a specific interest rate for a set period. It is related to the loan agreement since it directly affects the terms regarding interest payments.

Debt Settlement Agreement: This document is used when negotiating lower payments on an outstanding debt. It shares similarities with a loan agreement as it outlines the terms, but its focus is on settling existing debts rather than new loans.

Loan Modification Agreement: If the terms of an existing loan are altered, this document comes into play. It resembles a loan agreement by detailing the new terms and conditions of the loan.

Personal Guarantee: This is a promise made by someone, often a business owner, to repay a loan if the primary borrower defaults. It closely mirrors a loan agreement in that it specifies obligations and the consequences of non-payment.

Credit Agreement: This agreement outlines the terms for borrowing on a credit line rather than a lump sum. It contains similar terms to a loan agreement regarding interest and repayment, but it pertains to revolving credit.

Funding Agreement: This is often used in business contexts where investors provide funds. Like a loan agreement, it details the terms of funding, repayment expectations, and any interest obligations.

Completing a Loan Agreement form requires careful attention to detail. Here are essential dos and don'ts to consider:

When it comes to loan agreements, many people have misunderstandings that can lead to poor decisions. Here are ten common misconceptions about loan agreements:

Understanding these misconceptions can help individuals engage more effectively in their loan transactions and ensure they are making informed decisions.

When filling out and using a Loan Agreement form, keep the following key takeaways in mind:

Taking these steps can help ensure a smoother borrowing process and minimize potential disputes in the future.

New Employee Paperwork Checklist - The form can be submitted via mail or fax for convenience.

Mobile Home Seller Agreement - The agreement highlights the importance of accurate property descriptions for marketing purposes.