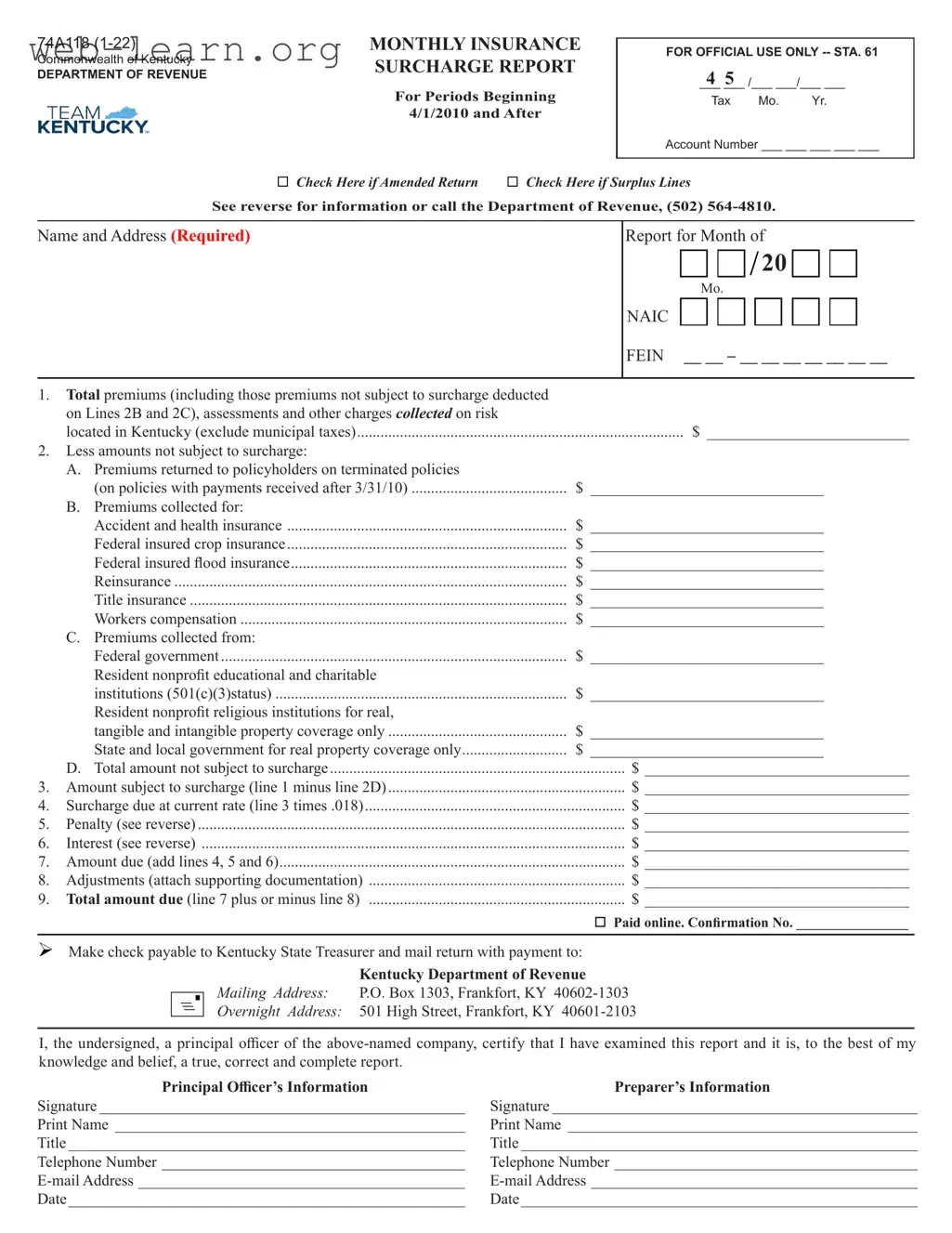

The Kentucky 74A118 form, also known as the Monthly Insurance Surcharge Report, plays a crucial role in the state's insurance framework. This form is designed for insurers operating within Kentucky, and it serves as a means to report and remit the insurance premium surcharge that is mandated by Kentucky law. The surcharge applies to various premiums, assessments, and other charges collected from policyholders, with specific exclusions for certain types of insurance. Insurers must complete the form on a monthly basis, detailing total premiums collected, as well as any amounts that are exempt from the surcharge. Additionally, the form requires the calculation of the surcharge due, along with any applicable penalties and interest for late submissions. It is important to note that insurers are responsible for collecting this surcharge from policyholders at the time of premium collection. Failure to file or pay the surcharge by the deadline can result in penalties, making timely submission essential. The form also includes sections for adjustments and certifications by a principal officer, ensuring accountability and accuracy in reporting. Understanding the nuances of the 74A118 form is vital for compliance and for maintaining the integrity of the insurance industry in Kentucky.

74A118 |

MONTHLY INSURANCE |

Commonwealth of Kentucky |

SURCHARGE REPORT |

DEPARTMENT OF REVENUE |

|

|

For Periods Beginning |

|

4/1/2010 and After |

FOR OFFICIAL USE ONLY

___4 ___5 /___ ___/___ ___

Tax Mo. Yr.

Account Number ___ ___ ___ ___ ___

Check Here if Amended Return |

Check Here if Surplus Lines |

See reverse for information or call the Department of Revenue, (502)

Name and Address (Required)

Report for Month of

/ 20

Mo.

NAIC

FEIN __ __ – __ __ __ __ __ __ __

1.Total premiums (including those premiums not subject to surcharge deducted on Lines 2B and 2C), assessments and other charges collected on risk

located in Kentucky (exclude municipal taxes) |

$ __________________________ |

2.Less amounts not subject to surcharge:

A. Premiums returned to policyholders on terminated policies

|

(on policies with payments received after 3/31/10) |

$ |

______________________________ |

B. |

Premiums collected for: |

|

|

|

Accident and health insurance |

$ |

______________________________ |

|

Federal insured crop insurance |

$ |

______________________________ |

|

Federal insured flood insurance |

$ |

______________________________ |

|

Reinsurance |

$ |

______________________________ |

|

Title insurance |

$ |

______________________________ |

|

Workers compensation |

$ |

______________________________ |

C. |

Premiums collected from: |

|

|

|

Federal government |

$ |

______________________________ |

|

Resident nonprofit educational and charitable |

|

|

|

institutions (501(c)(3)status) |

$ |

______________________________ |

|

Resident nonprofit religious institutions for real, |

|

|

|

tangible and intangible property coverage only |

$ |

______________________________ |

|

State and local government for real property coverage only |

$ |

______________________________ |

|

D. Total amount not subject to surcharge |

$ __________________________________ |

3. |

Amount subject to surcharge (line 1 minus line 2D) |

$ __________________________________ |

4. |

Surcharge due at current rate (line 3 times .018) |

$ __________________________________ |

5. |

Penalty (see reverse) |

$ __________________________________ |

6. |

Interest (see reverse) |

$ __________________________________ |

7. |

Amount due (add lines 4, 5 and 6) |

$ __________________________________ |

8. |

Adjustments (attach supporting documentation) |

$ __________________________________ |

9. |

Total amount due (line 7 plus or minus line 8) |

$ __________________________________ |

Paid online. Confirmation No. ________________

Make check payable to Kentucky State Treasurer and mail return with payment to:

Kentucky Department of Revenue

Mailing Address: P.O. Box 1303, Frankfort, KY

Overnight Address: 501 High Street, Frankfort, KY

I, the undersigned, a principal officer of the

Principal Officer’s Information |

Preparer’s Information |

Signature _______________________________________________ |

Signature _______________________________________________ |

Print Name _____________________________________________ |

Print Name _____________________________________________ |

Title ___________________________________________________ |

Title ___________________________________________________ |

Telephone Number _______________________________________ |

Telephone Number _______________________________________ |

Date___________________________________________________ |

Date___________________________________________________ |

GENERAL INFORMATION

KRS 136.392 requires that every domestic, foreign and alien insurer, other than life and health insurers, which is subject to or exempted from Kentucky insurance premiums taxes as levied pursuant to the provisions of either KRS 136.350, 136.370 or 136.390, shall charge and collect a surcharge at the current rate upon each $100 of premium, assessments or other charges, except for whether the charges are designated as premiums, assessments or otherwise.

Every insurer is required to file for each period, whether filing monthly or annually, even if no premiums were collected.

The insurance premium surcharge shall be collected by the insurer from its policyholders at the same time and in the same manner that its premium or other charge for the insurance coverage is collected. When claiming a deduction for premiums returned to a policyholder, the surcharge must also be returned to the policyholder.

No insurer or its agent shall be entitled to any portion of any premium surcharge as a fee or commission for its collection.

On or before the 20th day of each month, each insurer shall report and remit to the Department of Revenue, on the required forms, all premium surcharge monies collected during the preceding monthly accounting period less any monies returned to policyholders on policies terminated by either the insured or the insurer. Insurers with an annual liability of less than $1,000 for each of the previous two calendar years may report and remit to the Department of Revenue all premium surcharge monies collected on a calendar year basis on or before the 20th day of January of the following year.

Account Number For Surplus Lines

•

•Single

The penalty for failure to file an insurance premium surcharge report by the due date is 2 percent of the surcharge due for each 30 days or fraction thereof that the report is late (maximum 20 percent). The minimum penalty is $10. (KRS 131.180 (1))

The penalty for failure to pay the insurance premium surcharge by the due date is 2 percent of the surcharge due for each 30 days or fraction thereof that the payment is overdue (maximum 20 percent). The minimum penalty is $10. (KRS 131.180 (2))

Interest at the “tax increase rate” is applied to all insurance premium surcharge liabilities not paid by the original due date of the report. The computation period is from the original due date of the report to the date of payment. (KRS 131.183 (1))

Report on line 1 only those premiums that have been collected.

NOTE: Refunds or credits can only be taken on premiums returned to policy holders on terminated policies, not on exempt premiums such as worker’s compensation insurance. Refund requests must be made in writing.

Types of Policyholders Exempt or Partially Exempt from the Insurance Premium Surcharge pursuant to KRS 136.392(5):

•The federal government;

•Resident educational and charitable institutions qualifying under Section 501(c)(3) of the Internal Revenue Code;

•Resident nonprofit religious institutions for real, tangible, and intangible property coverage only;

•State government for coverage of real property; or

•Local governments for coverage of real property.

Also, Exempt from the Insurance Premium Surcharge:

•Premiums received by life and health insurers pursuant to KRS 136.392(1);

•Municipal premium taxes pursuant to KRS 136.392(1);

•Premiums received for accident and health insurance;

•Premiums received for federal insured crop insurance;

•Premiums received for federal insured flood insurance;

•Premiums received for reinsurance;

•Premiums received for title insurance; or

•Premiums received for workers’ compensation insurance.

Premiums collected for surety and bonds on public works projects are subject to the surcharge if the contractor is the policyholder. The fact that a governmental entity may be the obligee has no bearing on the application of the surcharge.

| Fact Name | Description |

|---|---|

| Form Number | 74A118 |

| Purpose | This form is used to report monthly insurance surcharge amounts collected by insurers operating in Kentucky. |

| Governing Law | KRS 136.392 outlines the requirements for the insurance premium surcharge. |

| Filing Frequency | Insurers must file this form monthly, even if no premiums were collected during the period. |

| Due Date | The completed form and payment are due on or before the 20th day of each month. |

| Penalty for Late Filing | A penalty of 2% of the surcharge due applies for each 30 days the report is late, with a maximum of 20%. |

| Interest on Late Payments | Interest is charged at the "tax increase rate" for unpaid surcharge liabilities from the original due date. |

| Exemptions | Certain entities, like federal government and nonprofit organizations, may be exempt from the surcharge. |

| Contact Information | For assistance, call the Kentucky Department of Revenue at (502) 564-4810. |

After completing the Kentucky 74A118 form, it is essential to ensure that all information is accurate before submission. This form must be filed with the Kentucky Department of Revenue by the 20th of each month for the previous month's premiums collected. If there are any adjustments or supporting documentation, attach them accordingly. The form can be submitted online or mailed to the appropriate address provided.

The Kentucky 74A118 form is a monthly insurance surcharge report required by the Commonwealth of Kentucky. It is used by insurers to report premiums, assessments, and other charges collected on risks located in Kentucky. This form is essential for compliance with Kentucky Revised Statutes (KRS) regarding insurance premium taxes.

Every domestic, foreign, and alien insurer, except for life and health insurers, must file the 74A118 form. This requirement applies regardless of whether the insurer is subject to or exempt from Kentucky insurance premium taxes. Even if no premiums were collected, insurers must still submit the form.

The form must be submitted to the Kentucky Department of Revenue on or before the 20th day of each month. This deadline applies to all insurers reporting on a monthly basis. Insurers with an annual liability of less than $1,000 for the previous two years can file annually by the 20th day of January of the following year.

The form requires several key pieces of information, including:

If the 74A118 form is not filed by the due date, a penalty of 2% of the surcharge due will be applied for each 30 days or fraction thereof that the report is late, up to a maximum of 20%. The minimum penalty is $10. Similar penalties apply for late payments of the surcharge.

Yes, certain policyholders are exempt or partially exempt from the surcharge. These include:

Payments for the surcharge should be made by check payable to the Kentucky State Treasurer. The completed form, along with the payment, should be mailed to the Kentucky Department of Revenue at the specified address. If preferred, payments can also be made online.

Filling out the Kentucky 74A118 form can be a straightforward process, but many people make common mistakes that can lead to complications. One significant error is failing to report the correct total premiums collected. Line 1 requires you to include all premiums, assessments, and other charges collected on risks located in Kentucky. If you mistakenly omit certain premiums, you may face penalties or interest charges later.

Another frequent mistake involves miscalculating the amounts not subject to the surcharge. Lines 2A through 2C list specific categories, such as premiums returned to policyholders and certain types of insurance. If you don’t carefully review these categories, you might incorrectly calculate the total amount not subject to the surcharge, leading to an inaccurate amount subject to surcharge on Line 3.

People often neglect to check the appropriate boxes for amended returns or surplus lines. If your report is an amendment or pertains to surplus lines, it’s crucial to indicate that clearly. Failing to do so can cause confusion and delays in processing your form, resulting in potential penalties.

Inaccurate or incomplete information in the principal officer’s section can also create issues. Ensure that the signature, print name, title, and contact information are all correctly filled out. An incomplete signature or missing information may lead to the rejection of your form, requiring you to resubmit it and possibly incurring late fees.

Additionally, many individuals forget to attach necessary supporting documentation when making adjustments. Line 8 asks for adjustments, and if you claim any, you must provide the relevant documentation. Without this, your adjustments may not be accepted, which can affect the total amount due on Line 9.

Finally, not keeping a copy of the submitted form can be a costly oversight. Always retain a copy of your completed 74A118 form and any correspondence with the Kentucky Department of Revenue. This practice can save you time and trouble if questions or disputes arise regarding your submission.

When dealing with the Kentucky 74A118 form, there are several other documents and forms that may be required or helpful in the process. These documents help ensure compliance with state regulations and provide necessary information for accurate reporting. Below is a list of commonly used forms and documents associated with the Kentucky 74A118 form.

Understanding these forms and their purposes can simplify the reporting process and ensure compliance with Kentucky's insurance premium tax regulations. Always consult with a professional if you have questions about specific requirements or need assistance with the documentation process.

The Kentucky 74A118 form is a specific document used for reporting insurance surcharges in the state of Kentucky. Several other forms serve similar purposes in various contexts, ensuring compliance with tax and reporting obligations. Here’s a list of five documents that share similarities with the Kentucky 74A118 form:

When filling out the Kentucky 74A118 form, it is essential to follow specific guidelines to ensure accuracy and compliance. Below is a list of things you should and shouldn't do.

Following these guidelines will help ensure that your submission is accurate and timely. If you have any questions or need assistance, consider reaching out to the Department of Revenue for clarification.

Understanding the Kentucky 74A118 form is essential for insurers operating in the state. However, several misconceptions can lead to confusion. Here are four common misunderstandings:

This is not true. All insurers, regardless of size, must complete the Kentucky 74A118 form. This includes domestic, foreign, and alien insurers, as well as those exempt from certain insurance premiums taxes. Even small insurers with minimal premiums collected are required to file.

In reality, the form requires reporting of all premiums collected, including those not subject to the surcharge. Insurers must detail the total premiums and then subtract the amounts not subject to the surcharge to arrive at the correct figure.

This is a misunderstanding. Insurers must file the Kentucky 74A118 form for each reporting period, even if no premiums were collected. Compliance is necessary to avoid penalties.

This is incorrect. The surcharge collected from policyholders must be remitted to the state. Insurers are not entitled to any portion of the surcharge as a fee or commission for its collection.

Filling out the Kentucky 74A118 form is an essential task for insurers operating in the state. Here are some key takeaways to keep in mind:

Understanding these aspects of the Kentucky 74A118 form can help ensure compliance and avoid penalties. Always refer to the latest guidelines from the Kentucky Department of Revenue for any updates or changes.