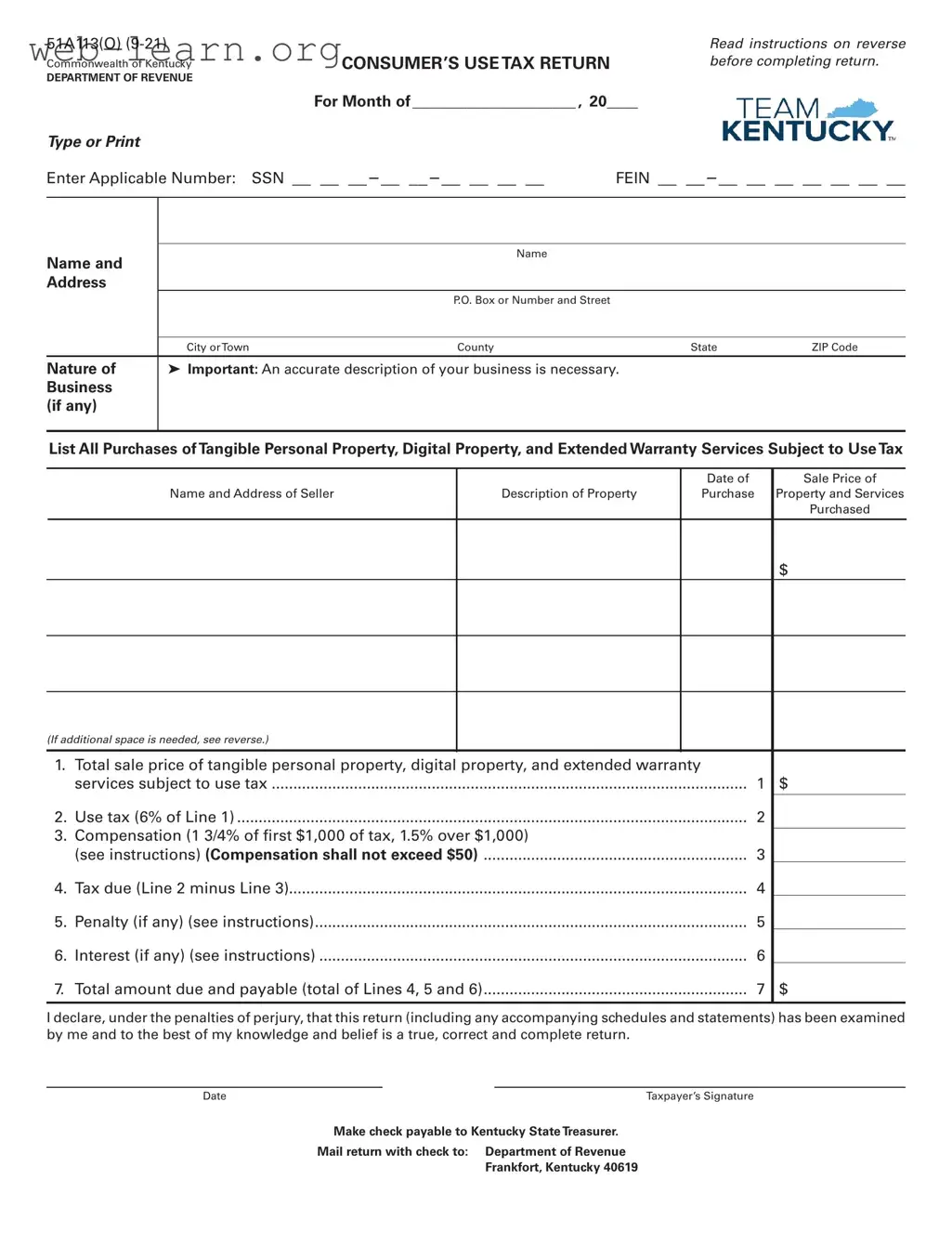

The Kentucky 51A113 form is an essential document for individuals and businesses that owe consumer use tax in the state of Kentucky. This form is specifically designed for those who are not registered as consumers or retailers, and it helps ensure compliance with state tax regulations. When completing the form, you will need to provide detailed information about your purchases of tangible personal property, digital property, and extended warranty services that are subject to use tax. The form requires you to list each item purchased, including the date of sale, the price, and the seller's information. The use tax rate is set at 6% of the total sale price of these items. Additionally, the form outlines penalties for late filing and payment, ensuring that taxpayers understand the importance of timely submissions. By accurately completing the 51A113, you can fulfill your tax obligations while avoiding potential fines and interest charges. Remember, this form must be filed within 20 days after the month in which the purchases were made, and it should be sent to the Department of Revenue along with any payment due. Understanding how to properly fill out this form is crucial for maintaining good standing with the state and ensuring that you meet your tax responsibilities.

51A113(O) |

|

Read instructions on reverse |

Commonwealth of Kentucky |

CONSUMER’S USE TAX RETURN |

before completing return. |

DEPARTMENT OF REVENUE |

|

|

|

For Month of _____________________ , 20____ |

|

Type or Print |

|

|

Enter Applicable Number: |

SSN __ __ __ – __ __ – __ __ __ __ |

FEIN __ __ – __ __ __ __ __ __ __ |

|

|

|

|

|

Name and |

|

Name |

|

|

|

|

|

|

|

Address |

|

|

|

|

|

|

P.O. Box or Number and Street |

|

|

|

|

|

|

|

|

City or Town |

County |

State |

ZIP Code |

|

|

|

|

|

Nature of |

Important: An accurate description of your business is necessary. |

|

|

|

Business |

|

|

|

|

(if any) |

|

|

|

|

|

|

|

|

|

List All Purchases of Tangible Personal Property, Digital Property, and Extended Warranty Services Subject to Use Tax

|

|

|

|

|

Date of |

|

Sale Price of |

|

Name and Address of Seller |

|

Description of Property |

|

Purchase |

|

Property and Services |

|

|

|

|

|

|

|

Purchased |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(If additional space is needed, see reverse.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1. |

Total sale price of tangible personal property, digital property, and extended warranty |

|

|

|

|||

|

services subject to use tax |

|

|

1 |

$ |

||

2. |

Use tax (6% of Line 1) |

|

|

2 |

|

||

|

|

|

|||||

3. |

Compensation (1 3/4% of first $1,000 of tax, 1.5% over $1,000) |

|

|

|

|||

|

|

|

|||||

|

(see instructions) (Compensation shall not exceed $50) |

............................................................. |

|

|

3 |

|

|

4. |

Tax due (Line 2 minus Line 3) |

|

|

4 |

|

||

5. |

Penalty (if any) (see instructions) |

|

|

5 |

|

||

6. |

Interest (if any) (see instructions) |

|

|

6 |

|

||

7. |

Total amount due and payable (total of Lines 4, 5 and 6) |

............................................................. |

|

|

7 |

$ |

|

|

|

|

|

|

|

|

|

I declare, under the penalties of perjury, that this return (including any accompanying schedules and statements) has been examined by me and to the best of my knowledge and belief is a true, correct and complete return.

Date |

Taxpayer’s Signature |

Make check payable to Kentucky State Treasurer.

Mail return with check to: Department of Revenue

Frankfort, Kentucky 40619

NOTICE

This form is to be filed only by persons or firms liable for use tax who are not: (1) registered consumers or (2) registered retailers. Registered consumers and retailers must use returns mailed to them by the Department, or filed electronically.

INSTRUCTIONS

Time and Place for

Tax

Sale

Tangible Personal Property, Digital Property, and Extended Warranty

Completing the

Penalties and

The penalty for failure to pay the tax within the time prescribed is 2 percent of the tax not timely paid for each 30 days payment is

Additional Space for Listing Tangible Personal Property, Digital Property, and

Extended Warranty Services Subject to Use Tax

Name and Address of Seller

Description of Property

Date of

Purchase

Sale Price of

Property and Services

Purchased

$

Subtotal: Sale price of purchases (include in total on Line 1, front page) .............................................

$

| Fact Name | Details |

|---|---|

| Purpose of Form | The Kentucky 51A113 form is used to report and pay the consumer's use tax on purchases of tangible personal property, digital property, and extended warranty services for which sales tax has not been paid. |

| Governing Law | This form is governed by Kentucky Revised Statutes (KRS) 139 and KRS 138.460, which outline the state's sales and use tax regulations. |

| Tax Rate | The use tax rate is set at 6% of the total sales price of the taxable items purchased without sales tax. |

| Filing Deadline | The completed form must be filed within 20 days following the month in which the purchase was made. |

| Penalties for Late Filing | A penalty of 2% of the tax owed is applied for each 30-day period the return is late, with a maximum penalty of 20% of the tax owed. |

| Compensation for Filing | Taxpayers may receive compensation of 1.75% on the first $1,000 of tax due, and 1.5% on amounts over $1,000, capped at $50. |

Once you have gathered all necessary information, you can begin filling out the Kentucky 51A113 form. This process involves entering your personal details, listing your purchases, and calculating the tax due. Make sure to double-check your entries for accuracy before submitting the form.

The Kentucky 51A113 form is a Consumer’s Use Tax Return. It is used by individuals or businesses that have purchased tangible personal property, digital property, or extended warranty services without paying Kentucky sales tax. This form allows taxpayers to report and remit the use tax owed on these purchases.

This form is specifically for those who are not registered consumers or retailers in Kentucky. If you have made purchases subject to use tax and have not paid sales tax at the time of purchase, you are required to file this form. Registered consumers and retailers should use the returns provided by the Department of Revenue instead.

The form must be filed within 20 days following the month in which the purchase was made. For example, if you made a purchase in January, the form is due by February 20. It is important to submit the form along with any payment due to avoid penalties and interest.

The use tax rate is 6% of the total sale price of the items purchased. To determine the amount owed, you will first need to total the sale prices of all applicable purchases on Line 1 of the form. Then, multiply that total by 0.06 to find the use tax due.

If you fail to file the return by the due date, you may incur penalties. The penalty is 2% of the tax for each 30 days or fraction thereof that the return is late, up to a maximum of 20%. Additionally, interest will apply to any late payments, which can add to the total amount owed.

Use tax applies to tangible personal property, digital property, and extended warranty services. Tangible personal property includes items like furniture, clothing, and tools. Digital property encompasses items such as digital books, music, and video games. Extended warranty services are applicable if the service agreement was sold or extended after July 1, 2018, and the related property is taxable.

To complete the form, you will need to list all applicable purchases, including the date of sale, price, and description of the property or services. After calculating the total sale price, fill in the corresponding lines for use tax, compensation, penalties, and interest as necessary. Finally, sign and date the form before mailing it to the Department of Revenue with your payment.

Filling out the Kentucky 51A113 form can be a straightforward process, but many people make common mistakes that can lead to delays or complications. One frequent error is failing to provide an accurate description of the business. This form requires a clear description to ensure that the tax is applied correctly. Omitting this information or being vague can lead to questions from the Department of Revenue, which could slow down the processing of your return.

Another common mistake is not listing all purchases subject to use tax. It's crucial to include every item, whether tangible personal property, digital property, or extended warranty services. If you miss even one purchase, it could result in underpayment of taxes, leading to penalties and interest. Take the time to review your purchases carefully before submitting the form.

Many individuals also overlook the importance of calculating the use tax correctly. The form specifies a tax rate of 6% on the total sale price of the items purchased. Errors in this calculation can lead to either overpayment or underpayment, both of which can create issues down the line. Double-check your math and ensure that you are applying the correct rate to the total amount.

Another mistake often made is neglecting to sign and date the form. This step may seem minor, but without a signature, your return is not valid. It's a simple oversight that can lead to significant delays. Always remember to review the form for a signature before mailing it.

Lastly, many people fail to pay attention to the deadline for filing the return. The Kentucky 51A113 form is due 20 days after the end of the month in which the purchases were made. Missing this deadline can result in penalties that accumulate over time. Mark your calendar and set reminders to ensure that you submit your return on time.

When filing the Kentucky 51A113 form, there are several other forms and documents that may be helpful or necessary to accompany your submission. Understanding these related documents can streamline your tax reporting process and ensure compliance with state regulations.

Being familiar with these forms and documents can simplify the tax filing process. Ensuring you have the right paperwork in order will help you meet your obligations while minimizing any potential issues with the Kentucky Department of Revenue.

The Kentucky 51A113 form, used for reporting consumer’s use tax, shares similarities with several other tax-related documents. Below is a list of ten forms that have comparable purposes or structures, along with brief explanations of how they relate to the Kentucky 51A113.

When filling out the Kentucky 51A113 form, it is essential to follow specific guidelines to ensure accuracy and compliance. Below are six important do's and don'ts to consider:

This form is designed for both individuals and businesses. If you made purchases of tangible personal property, digital property, or extended warranty services without paying sales tax, you need to file this form, regardless of your business status.

If you purchased items that are subject to Kentucky use tax and did not pay Kentucky sales tax at the time of purchase, you are required to file the 51A113 form. This is true even if you paid sales tax in another state.

The use tax rate in Kentucky is the same as the sales tax rate, which is currently 6%. Therefore, when calculating your use tax, you should apply this rate to the total sale price of your purchases.

All purchases of tangible personal property, digital property, and extended warranty services that were not taxed at the time of sale must be reported. This includes both large and small purchases, so it’s crucial to list everything accurately.

The Kentucky 51A113 form is essential for individuals and businesses who owe use tax on certain purchases. Below are key takeaways regarding the completion and use of this form.