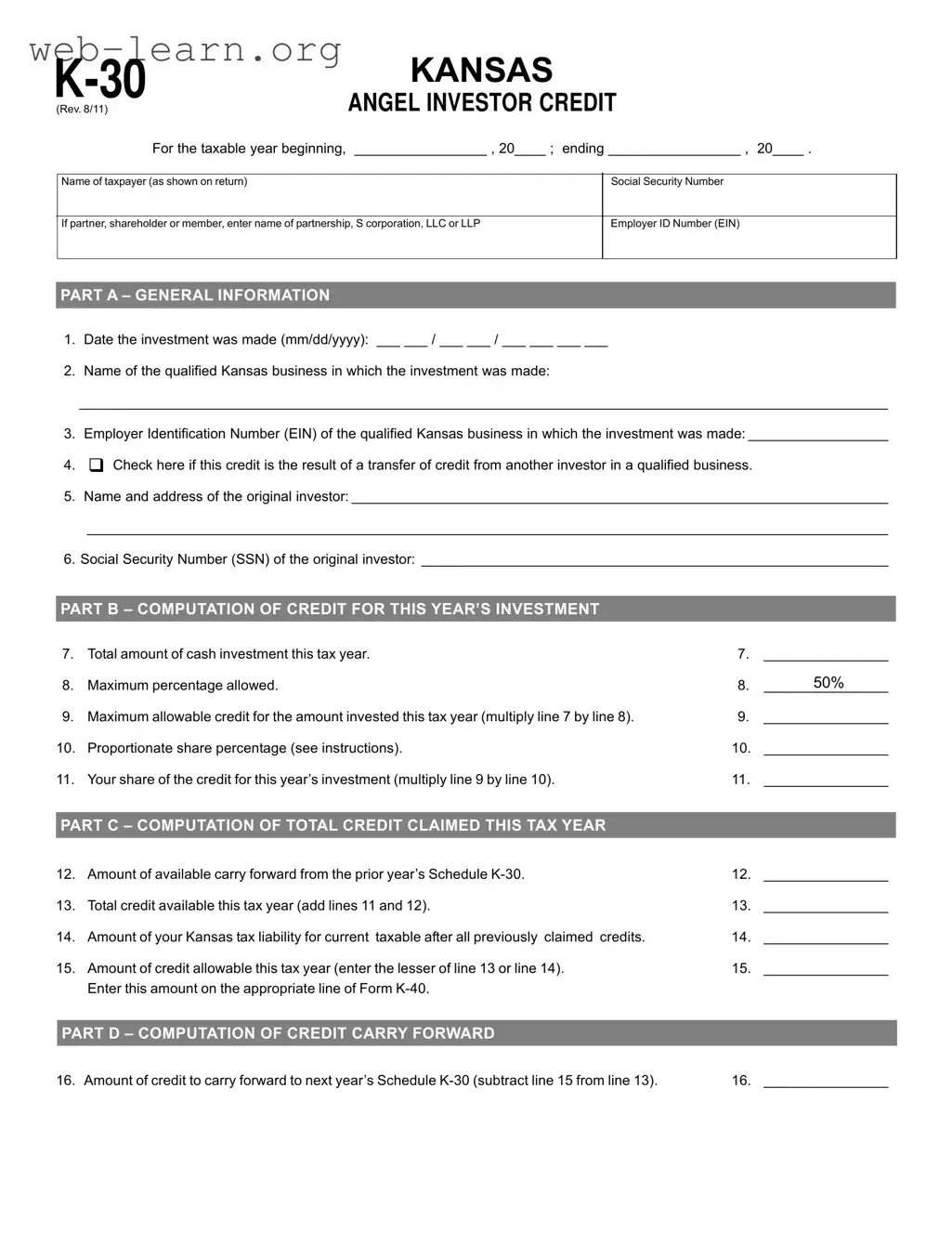

The Kansas K-30 form serves as a crucial instrument for angel investors seeking to capitalize on tax credits available for investments in qualified Kansas businesses. This form facilitates the process of claiming a tax credit against income or premium tax for cash investments made in approved securities of eligible companies. It is essential for investors to provide detailed information, including the date of investment, the name and Employer Identification Number (EIN) of the business, and the total amount of cash invested during the taxable year. The K-30 form also includes sections for computing the allowable credit based on the investment amount, determining the proportionate share for partners or shareholders, and calculating any carry-forward credits from previous years. Notably, the credit is capped at 50% of the cash investment, with specific limits set for individual investors and permitted entities. Additionally, the form requires investors to track their tax liabilities and ensure that the claimed credits do not exceed these obligations. By carefully following the instructions outlined in the K-30 form, investors can effectively navigate the complexities of claiming their tax benefits while supporting the growth of Kansas businesses.

KANSAS |

|

|

||

|

(Rev. 8/11) |

ANGEL INVESTOR CREDIT |

||

|

|

|

|

|

|

|

For the taxable year beginning, _________________ , 20____ ; |

ending _________________ , 20____ . |

|

|

|

|

|

|

|

Name of taxpayer (as shown on return) |

|

Social Security Number |

|

|

|

|

|

|

|

If partner, shareholder or member, enter name of partnership, S corporation, LLC or LLP |

|

Employer ID Number (EIN) |

|

|

|

|

|

|

PART A – GENERAL INFORMATION

1.Date the investment was made (mm/dd/yyyy): ___ ___ / ___ ___ / ___ ___ ___ ___

2.Name of the qualified Kansas business in which the investment was made:

________________________________________________________________________________________________________

3.Employer Identification Number (EIN) of the qualified Kansas business in which the investment was made: __________________

4.ノ Check here if this credit is the result of a transfer of credit from another investor in a qualified business.

5.Name and address of the original investor: _____________________________________________________________________

_______________________________________________________________________________________________________

6.Social Security Number (SSN) of the original investor: ____________________________________________________________

PART B – COMPUTATION OF CREDIT FOR THIS YEAR’S INVESTMENT

7. Total amount of cash investment this tax year.7. ________________

8. |

Maximum percentage allowed. |

8. |

50% |

________________ |

|||

9. |

Maximum allowable credit for the amount invested this tax year (multiply line 7 by line 8). |

9. |

________________ |

10. |

Proportionate share percentage (see instructions). |

10. |

________________ |

11. |

Your share of the credit for this year’s investment (multiply line 9 by line 10). |

11. |

________________ |

|

|

|

|

PART C – COMPUTATION OF TOTAL CREDIT CLAIMED THIS TAX YEAR |

|

|

|

12. |

Amount of available carry forward from the prior year’s Schedule |

12. |

________________ |

13. |

Total credit available this tax year (add lines 11 and 12). |

13. |

________________ |

14. |

Amount of your Kansas tax liability for current taxable after all previously claimed credits. |

14. |

________________ |

15. |

Amount of credit allowable this tax year (enter the lesser of line 13 or line 14). |

15. |

________________ |

|

Enter this amount on the appropriate line of Form |

|

|

PART D – COMPUTATION OF CREDIT CARRY FORWARD

16. Amount of credit to carry forward to next year’s Schedule |

16. ________________ |

INSTRUCTIONS FOR SCHEDULE

|

GENERAL INSTRUCTIONS |

SPECIFIC LINE INSTRUCTIONS |

||

K.S.A. |

|

|||

PART A |

|

|||

premium tax of any angel investor for a cash investment in the |

LINES 1 through 6 – Complete the information for the qualified |

|||

qualified securities of a qualified Kansas business. |

||||

Kansas business and original investor as requested. |

||||

Before an angel investor may be entitled to receive tax credits, |

||||

|

|

|||

such investor must have made a cash investment in a qualified |

PART B |

|

||

security of a qualified Kansas business. The investment must be |

LINE 7 – Enter total amount of cash investment made this tax year. |

|||

made in a business that has been approved by KTEC (Kansas |

||||

LINE 8 – This percentage determines the maximum credit allowable |

||||

Technology Enterprise Corporation) as a qualified business prior |

||||

as a result of the investment made during this tax year. Do not |

||||

to the date on which the cash investment is made. For information |

||||

make an entry on this line. |

||||

and assistance regarding the approval of a qualified Kansas |

||||

LINE 9 – Multiply line 7 by line 8 and enter the result. This is the |

||||

business, contact KTEC at (785) |

||||

maximum credit allowable. |

||||

The credit is 50% of such investors’ cash investment in any |

||||

LINE 10 – Partners, shareholders or members: Enter the percentage |

||||

qualified Kansas business, subject to the following limitations: |

||||

that represents your proportionate share in the partnership, S |

||||

|

|

|||

• No tax credits will be allowed for more than $50,000 for a single |

corporation, LLC or LLP. All other taxpayers: Enter 100%. |

|||

|

Kansasbusinessoratotalof$250,000intaxcreditsforasingle |

LINE 11 – Multiply line 9 by line 10 and enter result. This is your |

||

|

year per investor who is a natural person or owner of a |

share of the total credit for the amount invested this year. |

||

|

permitted entity investor. |

|

|

|

|

PART C |

|

||

• No tax credits shall be allowed for any cash investments in |

|

|||

LINE 12 – Enter the carry forward amounts available from prior |

||||

|

qualified securities for any year after the year 2016. |

|||

• |

The total amount of tax credits shall not exceed $6,000,000 |

years’ |

||

2010 legislation (SB 430) allows taxpayers that had credits |

||||

|

for tax year 2008 and each tax year thereafter, except that for |

|||

|

earned pursuant to K.S.A. |

|||

|

tax year 2011, the total amount of tax credits shall not exceed |

|||

|

year 2011 any reduction that occurred in tax year 2009 |

|||

|

$5,000,000. |

|||

|

and/or 2010. Enter those amounts here on line 12. |

|||

• |

No investor shall claim a credit for cash investments in Kansas |

|||

LINE 13 – Add lines 11 & 12 and enter the result. |

||||

|

Venture Capital, Inc. |

|||

|

LINE 14 – Enter your total Kansas tax liability for the current tax |

|||

• |

No Kansas venture capital company shall qualify for the tax |

|||

year after all credits other than the credit allowed for |

||||

|

credit for an investment in a fund created by articles 81, 82, |

|||

|

investments made during this tax year. |

|||

|

83 or 84 of chapter 74 of the Kansas Statutes Annotated. |

|||

|

LINE 15 – Enter the lesser of line 13 or line 14. Enter this amount |

|||

If the amount by which that portion of the credit allowed by this |

||||

on the appropriate line of Form |

||||

section exceeds the investors’ liability in any one taxable year, the |

||||

|

|

|||

PART D |

|

|||

remaining portion of the credit may be carried forward until the total |

|

|||

|

|

|||

amount of the credit is used. If the investor is a permitted entity |

LINE 16 – Subtract line 15 from line 13 and enter result. This |

|||

investor, the credit provided by this section shall be claimed by the |

||||

amount cannot be less than zero. Enter this amount on next |

||||

owners of the permitted entity investor in proportion to their |

||||

year’s Schedule |

||||

|

|

|||

ownership share of the permitted entity investor. |

|

|

||

Subject to certain restrictions this credit may be transferred to |

IMPORTANT: Do not send any enclosures with this |

|||

schedule. A copy of the approved KTEC certification |

||||

another taxpayer. Contact KTEC at (785) |

||||

form must be kept with your records. If this is a credit |

||||

information. |

||||

that has been transferred, documentation of the approved transfer |

||||

|

|

|||

“Angel investor’’and ‘‘investor’’meanYXWVUTSRan accredited investor |

||||

|

|

as provided by KDOR (Kansas Department of Revenue) must be |

||

who is a natural person or an owner of a permitted entity investor, |

retained with your records. KDOR reserves the right to request |

|||

who is of high net worth, as defined in 17 C.F.R. 230.501(a) as in |

additional information as necessary. |

|||

effect on the effective date of this act, and who seeks high returns |

|

|

||

through private investments in |

TAXPAYERASSISTANCE |

|||

active involvement in business, such as consulting and mentoring |

For assistance in completing this schedule contact the Kansas |

|||

the entrepreneur. |

||||

Department of Revenue: |

||||

“Cash investment” means money or money equivalent in |

||||

Tax Operations |

||||

consideration for qualified securities. |

||||

Docking State Office Building, 1st fl. |

||||

“Permittedentityinvestor”means any: a) general partnership, |

||||

915 SW Harrison St. |

||||

limited partnership, corporation that has in effect a valid election |

||||

Topeka, KS |

||||

to be taxed as an S corporation under the United States Internal |

||||

Phone: (785) |

||||

Revenue Code, or a limited liability company that has elected to |

||||

Fax: (785) |

||||

be taxed as a partnership under the United States Internal Revenue |

||||

|

|

|||

Code; and, b) that was established and is operated for the sole |

Additional copies of this credit schedule and other tax forms |

|||

purpose of making investments in other entities. |

are available from our web site at: ksrevenue.org |

|||

| Fact Name | Details |

|---|---|

| Form Purpose | The K-30 form is used to claim the Angel Investor Credit in Kansas. |

| Tax Year | This form is applicable for the taxable year specified by the taxpayer. |

| Investment Requirement | Investors must make a cash investment in a qualified Kansas business to qualify for the credit. |

| Maximum Credit | The maximum credit allowed is 50% of the cash investment, subject to certain limits. |

| Carry Forward | Unused credits can be carried forward to future tax years. |

| Governing Law | The credit is governed by K.S.A. 74-8133. |

| Approval Requirement | The business must be approved by KTEC as a qualified business before the investment. |

| Documentation | Taxpayers must keep a copy of the KTEC certification and any transfer documentation. |

Completing the Kansas K-30 form requires careful attention to detail. Ensure that you have all necessary information at hand, including your investment details and tax liability. Follow the steps below to fill out the form accurately.

Once you have completed the form, review all entries for accuracy. Ensure that you retain any necessary documentation and do not send any enclosures with the form. This will help facilitate a smooth processing of your credit claim.

What is the Kansas K-30 form?

The Kansas K-30 form is used to claim the Angel Investor Credit for cash investments made in qualified Kansas businesses. This tax credit allows investors to receive a percentage of their investment back as a credit against their state tax liability.

Who qualifies as an angel investor?

An angel investor is typically an accredited investor who is a natural person or an owner of a permitted entity investor. They seek high returns through private investments in start-up companies and often engage in mentoring or consulting with entrepreneurs.

What are the eligibility requirements for the investment?

The investment must be made in a business that has been approved by the Kansas Technology Enterprise Corporation (KTEC) as a qualified business. It’s essential to verify this status before making any cash investments.

What is the maximum credit I can claim?

For a single Kansas business, the maximum credit is limited to $50,000 per year. However, if you are a natural person or owner of a permitted entity investor, you can claim up to $250,000 in total tax credits per year.

How is the credit calculated?

The credit is calculated by taking the total amount of cash investment made during the tax year and multiplying it by the maximum allowable percentage, which is 50%. This result is then adjusted based on your proportionate share if you are a partner or member of an entity.

Can I carry forward unused credits?

Yes, if the amount of credit exceeds your tax liability for the current year, you can carry forward the unused portion to future tax years until the total credit is utilized.

What if I received the credit through a transfer?

If the credit is a result of a transfer from another investor, you must provide the name, address, and Social Security Number of the original investor on the K-30 form. Documentation of the transfer should also be kept with your records.

What documentation do I need to keep?

It is important to retain a copy of the approved KTEC certification form, as well as any documentation related to credit transfers. The Kansas Department of Revenue may request additional information if necessary.

Where can I get help with the K-30 form?

If you need assistance, you can contact the Kansas Department of Revenue. They provide resources and support for completing the K-30 form and understanding the Angel Investor Credit.

Are there any restrictions on the types of businesses that qualify?

Yes, investments cannot be made in Kansas Venture Capital, Inc. Additionally, no tax credits will be allowed for cash investments in qualified securities for any year after 2016. It’s crucial to ensure that the business meets all eligibility criteria before investing.

Filling out the Kansas K-30 form can be a daunting task, and mistakes can lead to delays or issues with tax credits. Here are ten common errors people often make when completing this form.

First, many individuals forget to include the correct dates for the investment. Line 1 requires the date in a specific format (mm/dd/yyyy). Failing to follow this format can result in confusion and processing delays.

Second, entering an incorrect or incomplete name for the qualified Kansas business can cause problems. Line 2 asks for the name, and if it doesn’t match official records, it may lead to rejection of the credit.

Another frequent mistake involves the Employer Identification Number (EIN). On Line 3, it’s essential to ensure that the EIN is accurate. A simple typo can lead to significant delays in processing the credit.

Some people neglect to check the box on Line 4 if the credit results from a transfer from another investor. This oversight can complicate the processing of the form and may lead to questions from the tax authorities.

Additionally, many individuals fail to provide the original investor's information on Lines 5 and 6. This information is crucial, especially if the credit has been transferred, and missing it can cause the application to be incomplete.

When it comes to the computation sections, mistakes often occur in Line 7, where individuals may not accurately calculate the total cash investment. This figure is vital for determining the allowable credit, so accuracy is key.

Another common error is misunderstanding the maximum allowable credit on Line 9. This amount is calculated by multiplying the investment amount by the maximum percentage allowed. Miscalculating this can lead to claiming less than what you are entitled to.

Line 10 can also be tricky. Some taxpayers don’t correctly determine their proportionate share percentage. This can lead to an incorrect calculation of the credit on Line 11, which is based on this percentage.

In Part C, failing to accurately report the carry forward amounts on Line 12 is a frequent mistake. This amount should reflect any credits from previous years that can still be applied, and missing this can affect the total credit claimed.

Finally, many people overlook the importance of reviewing their entries before submission. Simple arithmetic errors or typos can lead to significant issues. Taking the time to double-check all lines can save a lot of headaches later on.

By being aware of these common mistakes, taxpayers can navigate the Kansas K-30 form more effectively and ensure that they receive the credits they deserve.

The Kansas K-30 form is an essential document for individuals seeking to claim the Angel Investor Credit. However, it is often accompanied by several other forms and documents that help provide additional information or fulfill specific requirements. Below is a list of these related forms and documents, along with a brief description of each.

Understanding these additional forms and documents can help ensure that all necessary information is included when filing for the Angel Investor Credit. Keeping organized records will not only streamline the process but also provide peace of mind should any questions arise from tax authorities.

The Kansas K-30 form is designed for angel investors seeking tax credits for cash investments in qualified Kansas businesses. Several other documents share similarities with the K-30 form, particularly in their purpose and structure. Here are four documents that are comparable to the K-30 form:

These forms, like the K-30, aim to facilitate the reporting of financial activities and the claiming of credits, ensuring compliance with tax regulations while maximizing potential benefits for the investors and businesses involved.

When filling out the Kansas K-30 form, it's important to follow specific guidelines to ensure accuracy and compliance. Below is a list of things you should and shouldn't do during this process.

Following these guidelines can help streamline the process and avoid potential issues with your tax credit claim.

This is not true. The K-30 form is designed for both small and large investors. Any individual or entity that qualifies as an angel investor can utilize this form to claim tax credits for their investments in qualified Kansas businesses.

Credits can only be claimed for investments made in businesses that have been approved by the Kansas Technology Enterprise Corporation (KTEC) as qualified. It is essential to ensure that the business meets these criteria before making an investment.

The K-30 form allows for the carry forward of unused credits to future tax years. If an investor cannot utilize the full credit in one year, they can carry the remainder forward to offset future tax liabilities.

The maximum allowable credit is 50% of the cash investment made during the tax year. However, the total amount of credits claimed is subject to specific limits based on the investor's status and the total investment made.

It is crucial to maintain proper documentation, including the KTEC certification and any records related to the investment. This documentation may be requested by the Kansas Department of Revenue (KDOR) for verification purposes.

Entities such as partnerships, corporations, and limited liability companies (LLCs) can also claim the K-30 credit, provided they meet the necessary qualifications and have made eligible investments.

The form may be revised periodically, and it is essential to use the most current version to ensure compliance with any changes in the law or tax regulations. Always check for updates before filing.

Under certain conditions, K-30 credits may be transferred to another taxpayer. However, this process requires proper documentation and adherence to specific regulations set by KTEC and KDOR.

Here are key takeaways regarding the Kansas K-30 form for angel investor credits: