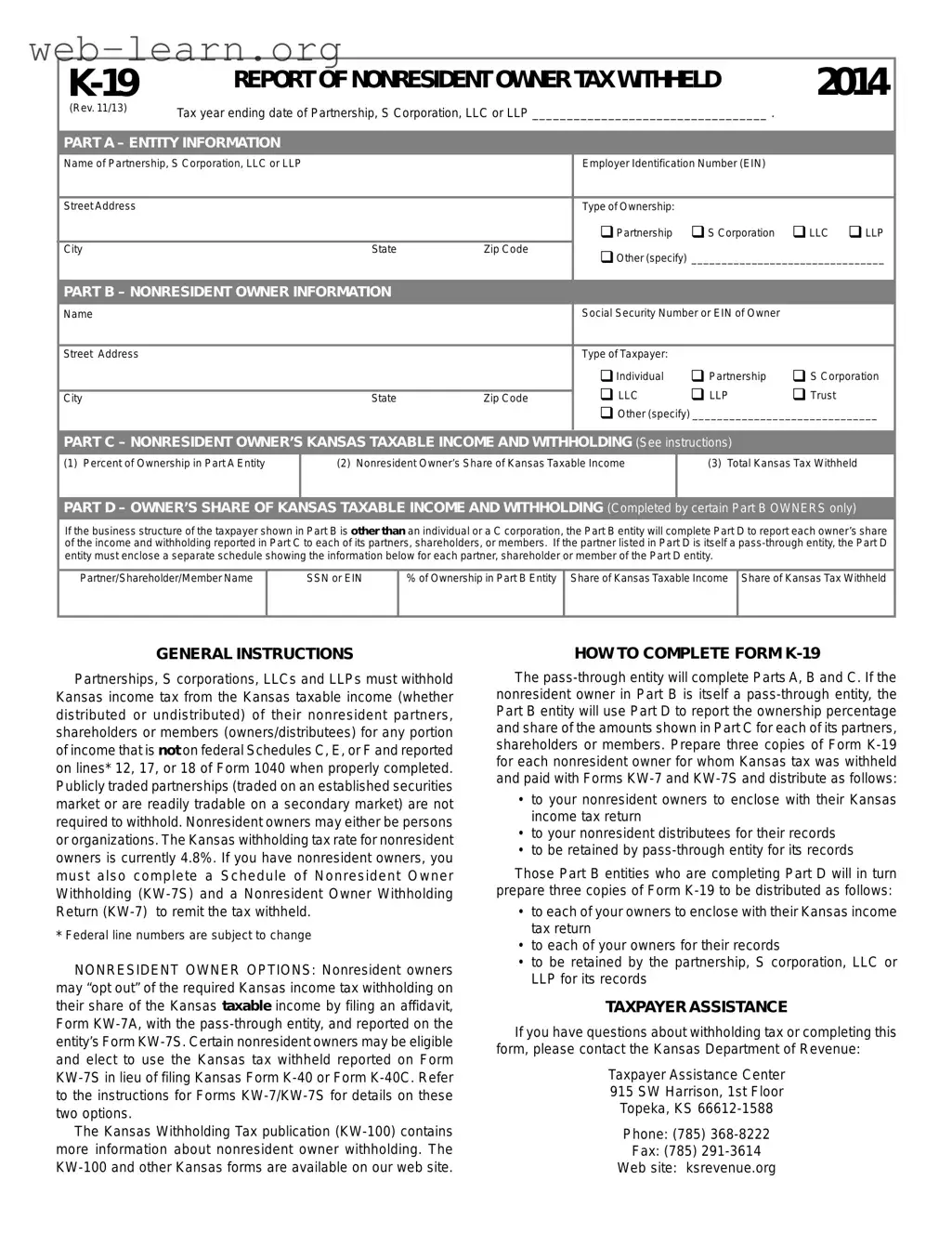

The Kansas K-19 form serves as a crucial document for partnerships, S corporations, limited liability companies (LLCs), and limited liability partnerships (LLPs) that need to report the withholding of state income tax from nonresident owners. This form is specifically designed to capture essential information about the entity itself, including its name, Employer Identification Number (EIN), and ownership structure. Additionally, it gathers details about the nonresident owners, such as their names, Social Security Numbers or EINs, and the nature of their ownership—whether they are individuals, partnerships, or other types of entities. The K-19 form also outlines the nonresident owner's share of Kansas taxable income and the corresponding amount of tax withheld, which is currently set at a rate of 4.9%. For certain entities, there is a provision to report the income and withholding for each owner separately in a designated section of the form. Notably, nonresident owners have options to opt out of withholding under specific circumstances, which can be documented through an affidavit. Completing the K-19 form accurately is vital for compliance, as it ensures that all parties involved can properly report and manage their tax obligations in Kansas.

REPORT OF NONRESIDENT OWNER TAX WITHHELD |

2014 |

||||

(Rev. 11/13) |

Tax year ending date of Partnership, S Corporation, LLC or LLP __________________________________ . |

|

|||

|

|

||||

|

|

|

|

|

|

PART A – ENTITY INFORMATION |

|

|

|

|

|

Name of Partnership, S Corporation, LLC or LLP |

|

Employer Identification Number (EIN) |

|

||

|

|

|

|

|

|

Street Address |

|

|

Type of Ownership: |

|

|

|

|

|

Partnership |

S Corporation |

LLC LLP |

City |

State |

Zip Code |

Other (specify) ________________________________ |

||

|

|

|

|||

|

|

|

|

|

|

PART B – NONRESIDENT OWNER INFORMATION |

|

|

|

|

|

Name |

|

|

Social Security Number or EIN of Owner |

|

|

|

|

|

|

|

|

Street Address |

|

|

Type of Taxpayer: |

|

|

|

|

|

Individual |

Partnership |

S Corporation |

|

|

|

LLC |

LLP |

Trust |

City |

State |

Zip Code |

|||

|

|

|

Other (specify) ______________________________ |

||

|

|

|

|

|

|

PART C – NONRESIDENT OWNER’S KANSAS TAXABLE INCOME AND WITHHOLDING (See instructions)

(1) Percent of Ownership in Part A Entity

(2) Nonresident Owner’s Share of Kansas Taxable Income

(3) Total Kansas Tax Withheld

PART D – OWNER’S SHARE OF KANSAS TAXABLE INCOME AND WITHHOLDING (Completed by certain Part B OWNERS only)

If the business structure of the taxpayer shown in Part B is other than an individual or a C corporation, the Part B entity will complete Part D to report each owner’s share of the income and withholding reported in Part C to each of its partners, shareholders, or members. If the partner listed in Part D is itself a

Partner/Shareholder/Member Name

SSN or EIN

% of Ownership in Part B Entity

Share of Kansas Taxable Income

Share of Kansas Tax Withheld

GENERAL INSTRUCTIONS

Partnerships, S corporations, LLCs and LLPs must withhold Kansas income tax from the Kansas taxable income (whether distributed or undistributed) of their nonresident partners, shareholders or members (owners/distributees) for any portion of income that is not on federal Schedules C, E, or F and reported on lines* 12, 17, or 18 of Form 1040 when properly completed. Publicly traded partnerships (traded on an established securities market or are readily tradable on a secondary market) are not required to withhold. Nonresident owners may either be persons or organizations. The Kansas withholding tax rate for nonresident owners is currently 4.8%. If you have nonresident owners, you must also complete a Schedule of Nonresident Owner Withholding

*Federal line numbers are subject to change

NONRESIDENT OWNER OPTIONS: Nonresident owners may “opt out” of the required Kansas income tax withholding on their share of the Kansas taxable income by filing an affidavit, Form

The Kansas Withholding Tax publication

HOW TO COMPLETE FORM

The

•to your nonresident owners to enclose with their Kansas income tax return

•to your nonresident distributees for their records

•to be retained by

Those Part B entities who are completing Part D will in turn prepare three copies of Form

•to each of your owners to enclose with their Kansas income tax return

•to each of your owners for their records

•to be retained by the partnership, S corporation, LLC or LLP for its records

TAXPAYER ASSISTANCE

If you have questions about withholding tax or completing this form, please contact the Kansas Department of Revenue:

Taxpayer Assistance Center

915 SW Harrison, 1st Floor

Topeka, KS

Phone: (785)

Fax: (785)

Web site: ksrevenue.org

| Fact Name | Details |

|---|---|

| Form Title | K-19 Report of Nonresident Owner Tax Withheld |

| Revision Date | Rev. 11/13 |

| Tax Year Requirement | Must indicate the tax year ending date for the entity. |

| Entity Types | Applicable for Partnerships, S Corporations, LLCs, and LLPs. |

| Withholding Rate | The current Kansas withholding tax rate is 4.9% for nonresident owners. |

| Nonresident Owner Options | Owners may opt out of withholding by filing Form KW-7A. |

| Governing Law | Kansas Statutes, specifically related to income tax withholding for nonresidents. |

| Taxpayer Assistance | Contact the Kansas Department of Revenue for help with the form. |

Completing the Kansas K-19 form is essential for reporting nonresident owner tax withheld. Follow these steps carefully to ensure accurate submission.

After completing the form, ensure all information is accurate and legible. Proper distribution of the copies will help nonresident owners with their tax filings. If any questions arise during the process, consider reaching out to the Kansas Department of Revenue for assistance.

What is the purpose of the Kansas K-19 form?

The Kansas K-19 form is used to report the Kansas income tax withheld from nonresident owners of partnerships, S corporations, LLCs, or LLPs. This form captures essential information about the entity, the nonresident owner, and the taxable income that has been withheld. It ensures compliance with Kansas tax regulations regarding nonresident owners and helps facilitate the correct remittance of withheld taxes to the state.

Who needs to complete the K-19 form?

Partnerships, S corporations, LLCs, and LLPs that have nonresident owners must complete the K-19 form. If the nonresident owner is itself a pass-through entity, additional reporting in Part D is required. Each entity must accurately report the ownership percentage, share of Kansas taxable income, and the total Kansas tax withheld for each nonresident owner. It is crucial to ensure that all relevant information is provided to avoid penalties or delays in processing.

How is the Kansas tax withheld calculated for nonresident owners?

The withholding tax rate for nonresident owners is currently set at 4.9% of their share of Kansas taxable income. This income may be either distributed or undistributed. Entities must calculate the total Kansas tax withheld based on the share of income reported for each nonresident owner. It is important to complete Parts C and D of the K-19 form accurately to reflect these calculations.

What should be done with the completed K-19 form?

Once the K-19 form is completed, three copies should be prepared for each nonresident owner. These copies are to be distributed as follows:

For those completing Part D, similar distribution rules apply for the owners listed in that section. Proper handling of these forms is essential for compliance with Kansas tax laws.

Filling out the Kansas K-19 form can be straightforward, but many make common mistakes that can lead to issues. One frequent error is failing to provide complete information in Part A. The name of the partnership, S corporation, LLC, or LLP, along with the Employer Identification Number (EIN), must be accurate and fully filled out. Omitting any detail or providing incorrect information can delay processing and create complications for both the entity and the nonresident owners.

Another common mistake occurs in Part B, where individuals often misidentify the type of taxpayer. Selecting the wrong option, such as marking “Partnership” instead of “LLC,” can lead to incorrect tax calculations and potential penalties. It is essential to review the options carefully and ensure that the correct taxpayer type is chosen to avoid confusion down the line.

In Part C, many people overlook the importance of accurately reporting the nonresident owner’s share of Kansas taxable income. This section requires precise calculations. Errors in the percentage of ownership or the taxable income can result in incorrect withholding amounts. It’s crucial to double-check these figures to ensure compliance with Kansas tax laws.

Lastly, some filers forget to prepare and distribute the required copies of the K-19 form as outlined in the instructions. Not providing copies to the nonresident owners, or failing to retain a copy for the entity's records, can lead to issues during tax season. Each entity must ensure that they follow the distribution guidelines to avoid complications later.

The Kansas K-19 form is a crucial document for reporting nonresident owner tax withholding for partnerships, S corporations, LLCs, and LLPs. Alongside this form, several other documents play an essential role in ensuring compliance with Kansas tax regulations. Below is a list of these documents, each accompanied by a brief description.

Understanding these documents is essential for compliance with Kansas tax laws. Each form serves a specific purpose in the overall process of reporting and remitting taxes for nonresident owners, ensuring that both entities and individuals meet their tax obligations accurately and efficiently.

The Kansas K-19 form, used for reporting tax withheld from nonresident owners, shares similarities with several other documents that facilitate tax reporting and compliance. Here are nine documents that are comparable to the K-19 form, each serving a unique purpose in the tax reporting landscape:

Each of these documents plays a crucial role in the broader context of tax compliance and reporting, ensuring that both entities and individuals meet their obligations while navigating the complexities of tax law.

When filling out the Kansas K-19 form, it is important to follow specific guidelines to ensure accuracy and compliance. Here are six things to do and avoid:

By adhering to these guidelines, you can help ensure a smoother process when dealing with the Kansas K-19 form.

Understanding the Kansas K-19 form can be challenging, and there are many misconceptions surrounding it. Here are nine common misunderstandings:

Understanding the Kansas K-19 form is crucial for ensuring compliance with state tax regulations. Here are key takeaways to help navigate the process:

By keeping these points in mind, you can navigate the K-19 form process with greater confidence and accuracy.