The IRS W-2 form plays a crucial role in the annual income tax process for employees and employers alike. Issued by employers, this form summarizes the earnings, tips, and other compensations an employee received throughout the year. It also includes details about federal, state, and other taxes withheld from the employee's wages. For many, this document serves as the foundation for accurately completing tax returns. Recipients should pay close attention to the various boxes on the form, which disclose not only total wages but also any contributions made to retirement plans and health care benefits. Understanding the W-2 form is essential for ensuring that individuals report their income correctly and take advantage of potential deductions or credits they may qualify for. Moreover, both employees and employers have specific responsibilities regarding the accuracy and submission of this important form, which plays a significant role in the overall tax system.

| Fact Name | Details |

|---|---|

| Purpose | The W-2 form reports an employee's annual wages and the amount of taxes withheld from their paycheck. |

| Who Receives It | Employers must provide a W-2 form to each employee who earned wages during the year. |

| Filing Deadline | Employers must file W-2 forms with the Social Security Administration by January 31 of the following year. |

| Tax Purposes | The W-2 form is essential for employees to complete their federal and state tax returns accurately. |

| State-Specific Forms | Many states also require a similar form called the W-2, governed by state employment laws. |

| Copies Provided | Employers typically provide copies of the W-2 form to employees, the IRS, and state tax agencies. |

| Deductions Included | The W-2 form includes deductions for federal income tax, social security, and Medicare. |

| Corrections | If mistakes occur, employers must issue a corrected W-2 form, known as Form W-2c. |

| Digital Versions | Employers may offer electronic W-2 forms, but employees must consent to receive them this way. |

| Identification Numbers | The W-2 form contains important identifiers, including the employer's EIN (Employer Identification Number) and the employee's Social Security Number. |

Once you have all the necessary information at hand, filling out the IRS W-2 form correctly is important for both you and your employees. Make sure to double-check all entries for accuracy to avoid any potential issues with tax filings. Below are the steps required to complete the form.

Once the W-2 form is filled out, ensure that you distribute copies to your employee and file the appropriate copy with the IRS. Keeping accurate records is vital for both your business and the employees you support.

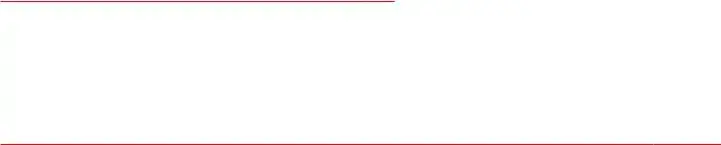

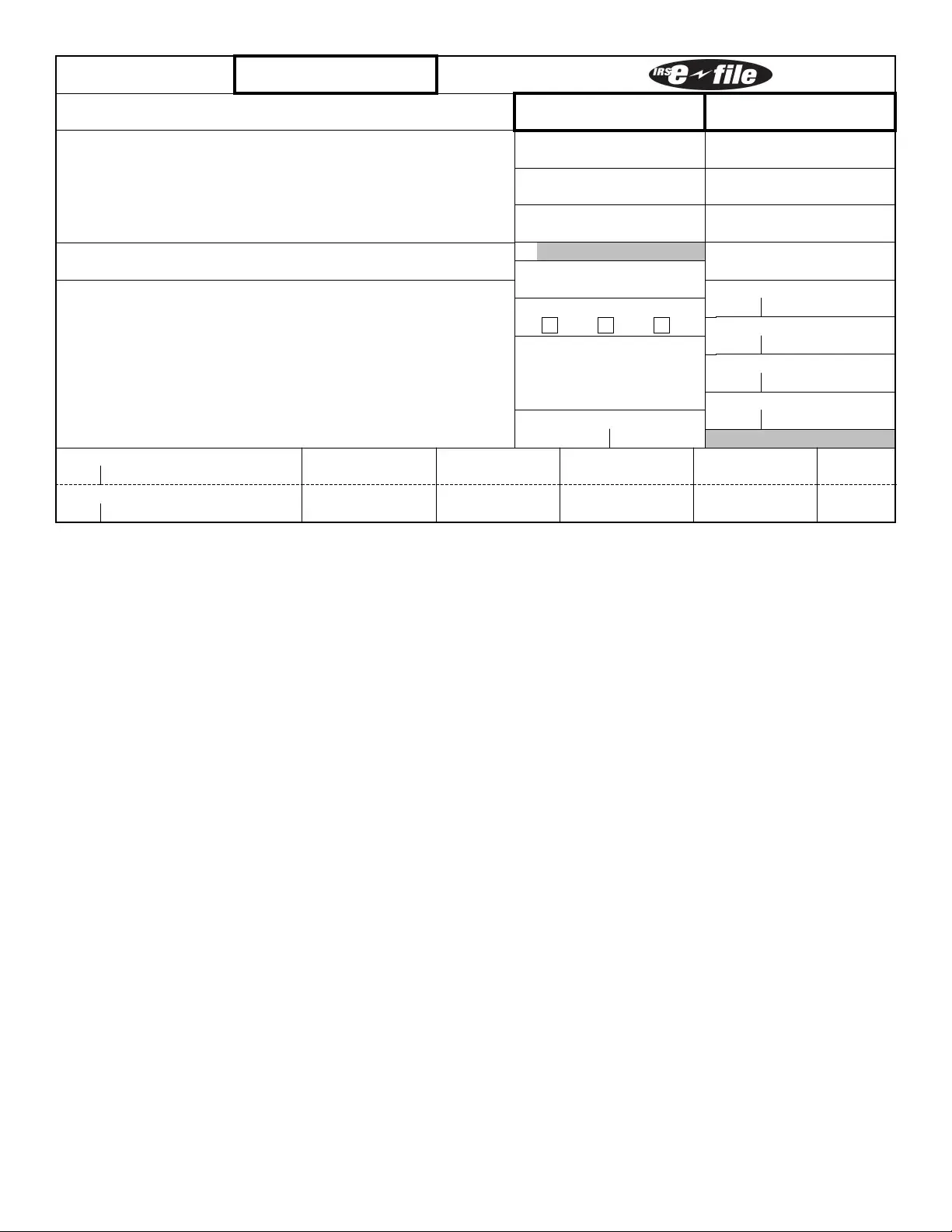

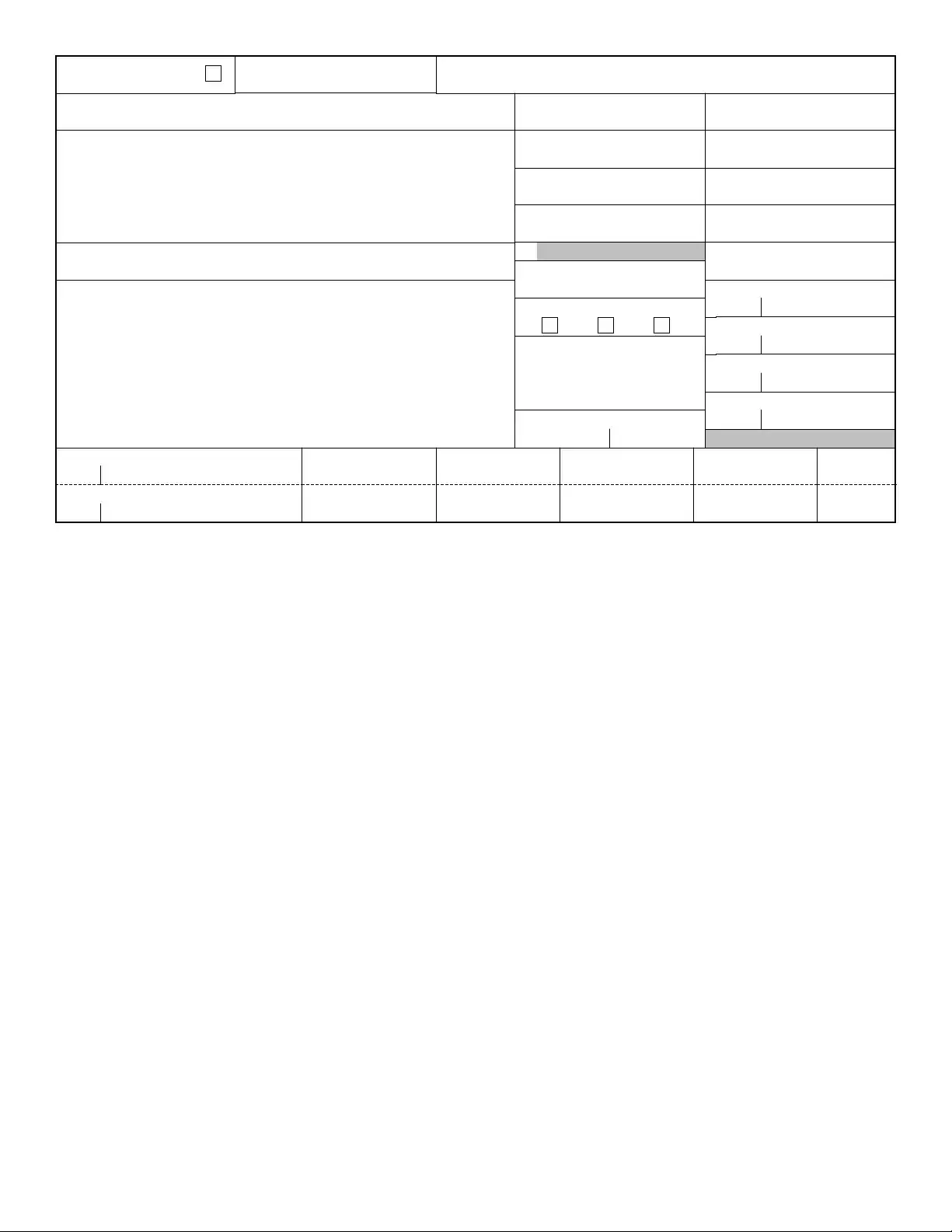

The W-2 form, officially known as the Wage and Tax Statement, is a document that employers in the United States must provide to their employees. This form reports an employee's annual wages and the taxes withheld from their paycheck. Employees use the information on their W-2 to complete their tax returns.

Any employee who receives a salary or wages from an employer typically receives a W-2 form at the end of each tax year. This includes full-time employees, part-time workers, and some contracted workers who meet specific criteria. However, some independent contractors may receive a different form known as the 1099.

Employers are required to send out W-2 forms by January 31 of each year. You should receive your W-2 in the mail or electronically if your employer offers that option. If you haven’t received your form by mid-February, you should reach out to your employer’s payroll department.

A W-2 form includes several important pieces of information:

Each of these elements is crucial for accurately filing your tax returns.

If you notice any mistakes on your W-2, such as incorrect earnings or wrong Social Security numbers, it’s important to address this as soon as possible. Contact your employer and request a corrected W-2, known as a W-2c. This corrected form will help ensure that your tax return is accurate and reflects your true earnings.

Technically, you can file your taxes without a W-2, but it is not recommended. If you haven’t received your W-2 by the time you need to file, you can estimate your income based on your pay stubs. However, you may need to file an extension until you receive the correct form, and it’s essential to amend your tax return later if the numbers change.

The W-2 is a crucial document for tax filing because it provides the IRS with detailed information about your earnings and the taxes you have already paid. This helps determine whether you owe additional taxes or are eligible for a refund. Accurate reporting of income and taxes is vital for complying with federal tax laws.

Filling out the IRS W-2 form correctly is crucial for both employers and employees. Unfortunately, there are several common mistakes that can occur during this process. One such mistake is failing to provide accurate personal information. Employees must ensure that their names and Social Security numbers are entered correctly. Any discrepancies can lead to delays in processing the tax return.

Another frequent error is not reporting all taxable wages. Employers might overlook additional income such as tips or bonuses, resulting in an underreported income. This can lead to complications when the employee files their taxes. It’s essential for both parties to keep detailed records to ensure accuracy.

Some employers may incorrectly classify employees as independent contractors on the W-2 form. This misclassification can cause problems for employees, especially when it comes to tax deductions and responsibilities. Proper classification ensures that workers receive the appropriate tax documents, either a W-2 or a 1099, based on their employment status.

Omitting or misreporting withholdings is another mistake that often occurs. Employees might not realize that various withholdings like federal income tax, Social Security, and Medicare tax need to be detailed accurately. If any withholdings are incorrect, the employee may owe money when filing their taxes or risk overpaying.

Some people also fail to retain a copy of their W-2 forms for their records. Keeping these documents is vital for future reference and for any potential audits. Losing this paperwork can complicate the tax filing process and lead to unnecessary stress.

Not checking for errors after the form is completed can lead to problems down the line. Even if the form appears correct, it's wise to double-check for typos or omissions. These small mistakes can create significant issues with the IRS.

Another pitfall lies in the submission method. Employees must ensure that forms are submitted on time and to the correct IRS office. Missing the deadline or submitting to the wrong location can result in penalties or complications with tax processing.

Lastly, misunderstanding the additional details required on the form can be problematic. For instance, employees may not realize they need to report other types of compensation, such as health insurance premiums deducted directly from their paychecks. Understanding all components of the W-2 form is essential for accurate reporting.

The IRS W-2 form plays a crucial role in the tax reporting process for employees and employers alike. It summarizes an employee's earnings and the taxes withheld throughout the year. However, several other documents often accompany the W-2 form, making the tax filing process more comprehensive. Here are four important forms and documents that you might frequently encounter alongside the W-2 form.

Understanding the context and purpose of these documents can simplify the tax filing process. When preparing your taxes, ensure you have all the necessary forms to meet reporting requirements efficiently and accurately.

The IRS W-2 form is well-known for summarizing an employee's annual wages and the taxes withheld. Several other documents serve similar purposes in the realm of taxation, employment, and income reporting. Below are ten documents that share similarities with the W-2:

Understanding the similarities among these forms can help individuals navigate their tax obligations more efficiently. Each document, while unique, plays an important role in providing a clear picture of one’s financial landscape for tax purposes.

Filling out your IRS W-2 form correctly is important for ensuring proper tax reporting. Below is a helpful list of what you should and shouldn't do when completing this form.

By following these guidelines, you'll help ensure that your W-2 is accurately completed, aiding in a smoother tax process.

The IRS W-2 form is an important document for both employees and employers, yet there are several misconceptions surrounding it. Here’s a breakdown to help clarify some common myths.

This is not true. The W-2 form is required for any employee who receives wages, regardless of their work hours or employment type, as long as they are classified as an employee.

All employers are legally required to provide a W-2 form to their employees who earn wages. This ensures that employees can accurately report their income on their tax returns.

The information on the W-2 is crucial. Employees must use it to complete their tax returns, as it reflects their earnings and the taxes withheld throughout the year.

Employees need the W-2 form for all tax filings. Even if they receive a refund, the information on the W-2 is necessary to properly report income.

While it’s important to have accurate information, employees should address any discrepancies with their employer. Penalties are typically not incurred by employees for incorrect W-2 forms; the responsibility lies with the employer to correct and reissue the form.

Technically, you can file without a W-2, but it is not advised. You risk underreporting your income, leading to potential penalties. It’s best to ensure you have the W-2 before filing.

The W-2 provides more than just your annual income. It includes information about federal and state taxes withheld, Social Security, and Medicare contributions, which are all important for tax calculations.

Understanding these common misconceptions about the W-2 form can help employees better navigate their tax responsibilities and ensure they are prepared for filing their income tax returns.

The IRS W-2 form is crucial for both employers and employees. Understanding it will ensure accurate reporting of income and taxes. Here are key takeaways about filling out and using the W-2 form:

Understanding the W-2 form will aid in proper tax filing and compliance with IRS requirements.

Il Vehicle Registration - The form is an integral part of the vehicle registration and licensing process.

Az 5005 Form - Common exemptions include property for leasing in licensed businesses.

Identity Verification Form Template - It is important to bring the appropriate identification when signing.