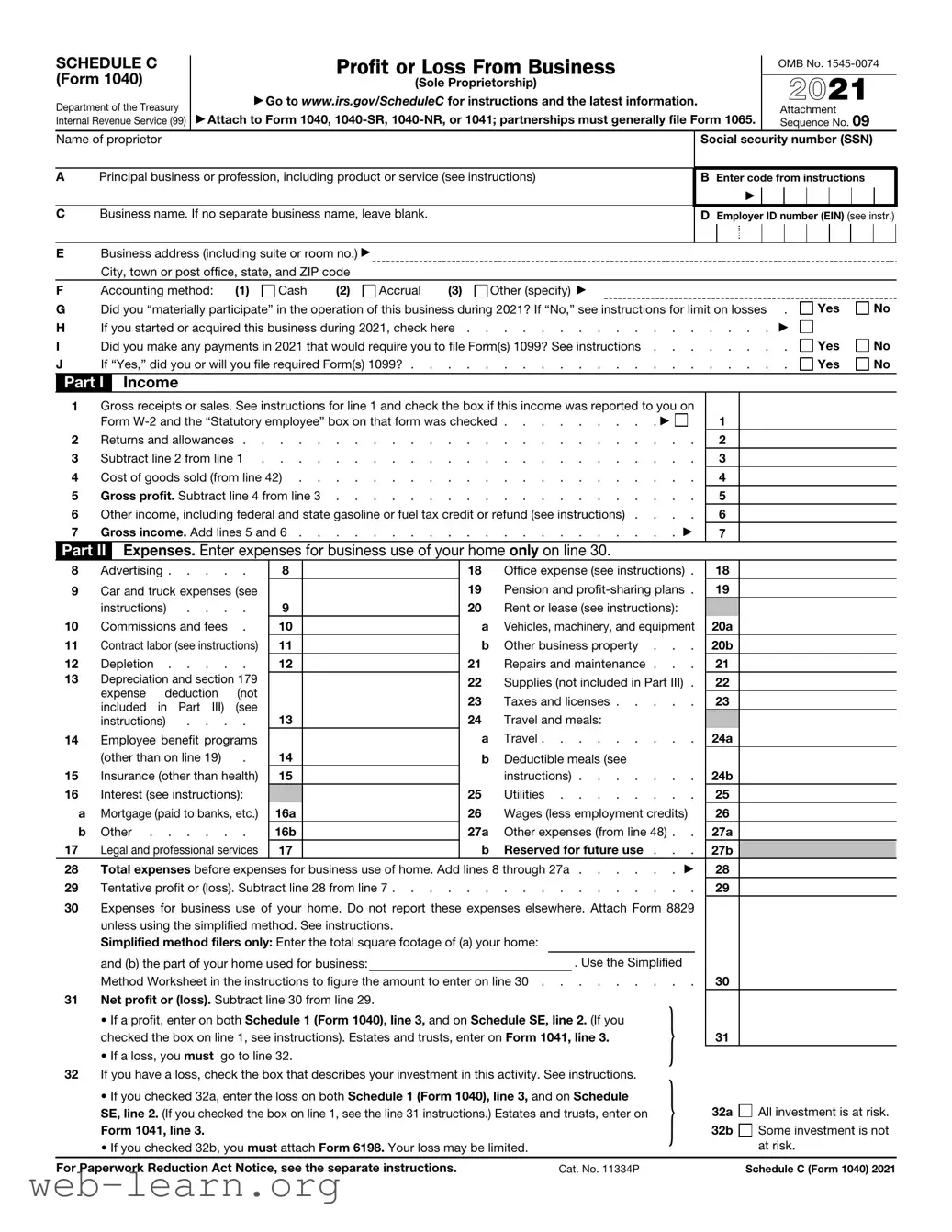

The IRS Schedule C (Form 1040) plays a crucial role for self-employed individuals and business owners. This form is designed to report income and expenses from a sole proprietorship, providing the IRS with a clear overview of your business's financial activity. Notably, it captures a variety of income types, reflecting everything from sales revenues to service fees. In addition to income reporting, Schedule C allows for detailed expense documentation, such as costs related to advertising, office supplies, and travel. Understanding how to accurately complete this form is essential, as it not only affects tax liability but also establishes the foundation for future financial planning and business assessments. With its combination of straightforward reporting and the opportunity for deductions, it is a vital element in managing a self-employed person’s financial responsibilities. Properly filling out Schedule C can help maximize eligible deductions, ultimately impacting the overall financial health of one's business.

| Fact Name | Description |

|---|---|

| Purpose | IRS Schedule C, also known as "Profit or Loss from Business," is used by sole proprietors to report income and expenses from their business activities. |

| Eligibility | This form is specifically for individuals who operate a business as a sole proprietor. Partnerships and corporations use different forms. |

| Filing Requirement | Individuals must file Schedule C if they earn at least $400 in net earnings from self-employment during the tax year. |

| Deadline | Schedule C must be submitted along with IRS Form 1040 by the tax filing deadline, typically April 15. |

| Income Reporting | All business income must be reported, including cash, checks, and credit card payments. This total is reported on Line 1 of the form. |

| Expense Deductions | Expenses such as operating costs, supplies, and other business-related deductions can be reported on the form, reducing taxable income. |

| Self-Employment Tax | Self-employed individuals must also calculate and pay self-employment tax based on net earnings, which is reported on Schedule SE. |

| Record-Keeping | Detailed records of income and expenses are crucial for accurate reporting on Schedule C and for potential audits. |

| State Variations | Some states require additional forms for reporting business income, governed by state-specific tax laws that may include income tax or franchise tax regulations. |

| Importance of Accuracy | Filling out Schedule C accurately is essential to avoid errors that may lead to penalties or increased scrutiny from the IRS. |

Completing the IRS Schedule C (Form 1040) is an essential part of reporting income for self-employed individuals. This process will guide you through the steps to ensure accurate and complete information. Take your time to gather the necessary documentation and fill out each section methodically.

Following these steps will equip you to fill out the IRS Schedule C with confidence. Ensure that you keep copies of everything for your records, as this may be helpful in the future. Reach out to a tax professional if you need further assistance or clarification.

IRS Schedule C is a form used by sole proprietors to report income or loss from their business. It is part of the Form 1040 tax return. If you have a business that is not organized as a corporation, you'll typically need to file a Schedule C. By doing so, you detail the income your business generated as well as the expenses incurred in running it.

Individuals who earn income from self-employment, freelancing, or running a business as a sole proprietor are required to file Schedule C. This includes anyone who is a contractor or has a side business, even if you only did it part-time. If your net profit from your business is $400 or more, you must file this schedule.

You should report any income related to your business activities on Schedule C. This can include:

Make sure to keep accurate records of all income received so that you can accurately report it.

Many business-related expenses are deductible, which can help lower your taxable income. Some common examples include:

It's important to maintain receipts and records to substantiate these deductions.

Your net profit or loss is calculated by subtracting your total business expenses from your total business income. If your expenses exceed your income, you will have a net loss. Conversely, if your income exceeds your expenses, you will show a profit. This figure is then reported on your Form 1040.

Yes, there are a few key considerations:

Filling out the IRS Schedule C (Form 1040) can be tricky. Many people make common mistakes that can affect their tax filings. One major error occurs when individuals do not report all their income. Whether it’s cash payments or income from side gigs, every dollar counts. Missing even a small amount can cause issues with the IRS.

Another frequent mistake is claiming incorrect business expenses. Many people confuse personal expenses with business-related expenses. It’s vital to keep business and personal finances separate. This distinction ensures that only legitimate business costs are deducted, which can prevent potential audits.

People also often fail to keep adequate records. The IRS requires proof of income and expenses. Without receipts and documentation, it becomes challenging to support the claimed amounts. Good records not only simplify the filling process but also strengthen the validity of your claims if questioned.

Some taxpayers neglect to use the correct accounting method. Depending on the nature of the business, the cash basis or accrual basis accounting may be more appropriate. Selecting the wrong method can complicate tax calculations and lead to incorrect tax liability.

A common oversight is not filling in all required sections. Each part of the Schedule C has its purpose. Omitting information may not only result in processing delays but can also trigger an audit. It’s crucial to ensure that every applicable section is completed correctly.

Another mistake is misunderstanding the implications of self-employment tax. Many people are surprised to learn that self-employment income incurs additional taxes. Failing to anticipate these taxes can lead to unexpected liabilities come tax time.

Lastly, some who fill out Schedule C make mistakes while calculating their net profit or loss. Errors in addition or subtraction can have significant consequences. Taking the time to double-check calculations can help avoid unnecessary complications later.

Being aware of these common pitfalls can help smooth the Schedule C filing process. By paying careful attention to details and keeping organized records, taxpayers can better navigate their obligations and maximize their deductions.

The IRS Schedule C 1040 form is utilized by sole proprietors to report income or losses from a business operated or a profession practiced. Along with this form, there are several other documents that are commonly used to provide necessary information and support for tax reporting. The following is a list of some of those relevant forms and documents.

These documents and forms provide essential support and context when filing taxes related to a business. Properly organizing and submitting them alongside the Schedule C 1040 form can lead to a smoother tax-filing process.

IRS Form 1065: This form is used by partnerships to report income, deductions, gains, losses, and other information about the business. Like Schedule C, it provides a comprehensive overview of the entity's financial performance, but it pertains to multi-member businesses.

IRS Form 1120: Corporations use this form to report their income tax. Similar to Schedule C, Form 1120 requires detailed descriptions of income and expenses. However, it specifically addresses corporate rather than individual business activities.

IRS Form 1120-S: This form is for S corporations and allows pass-through taxation. It shares similarities with Schedule C in its analysis of income and expenses, reflecting how both structures report their financial results to the IRS.

IRS Schedule E: Often used for reporting supplemental income or losses, Schedule E is similar in that it records income and related expenses, particularly from rental properties or partnerships. However, it focuses more on passive income streams.

IRS Schedule F: This form is for farmers. It closely resembles Schedule C as both document farming income and expenses. The major difference lies in the specific types of deductions and credits applicable in agricultural contexts.

IRS Form 1040: The 1040 is the individual income tax return form that summarizes all income sources. While Schedule C is attached to it for sole proprietors, both forms work in tandem to calculate overall tax obligations based on personal earnings.

IRS Form 4797: This form is used for reporting the sale of business property. It parallels Schedule C in its focus on business operations and financial performance but targets the sale and disposition of assets instead of ongoing business income.

IRS Form 8606: This form reports non-deductible contributions to traditional IRAs and distributions from Roth IRAs. Although it does not focus on business income, like Schedule C, it is critical for tracking financial investments and tax responsibilities for specific individual situations.

When completing the IRS Schedule C Form 1040, it is essential to approach the task with attention, as this form is used to report income or losses from a business you operated as a sole proprietor. Below is a list of helpful tips detailing what to do and what to avoid during this process.

Things to Do:

Things to Avoid:

Understanding IRS Schedule C (Form 1040) can be confusing. Many people hold misconceptions about this important tax form used by sole proprietors to report income or loss from their business. Here are four common misconceptions that often arise.

Recognizing and correcting these misconceptions can help ensure that business owners navigate their tax responsibilities effectively and with greater confidence.

Understanding the IRS Schedule C (Form 1040) is crucial for anyone operating a sole proprietorship. Here are some key takeaways to help you navigate this essential document.

Be proactive in addressing these elements when filling out Schedule C. Your diligence can pave the way for a smoother tax season and help you maximize your benefits as a business owner.

Pre Lien Form - Contractors must ensure that this notice is properly completed and served to protect their interests.

2023 Form Il-1040 - Subtracting Line 2 from Line 1 gives you a starting point for your nonrefundable credit calculation.

Affidavit of Heirship California - The form serves as an official record of the deceased's heirs.