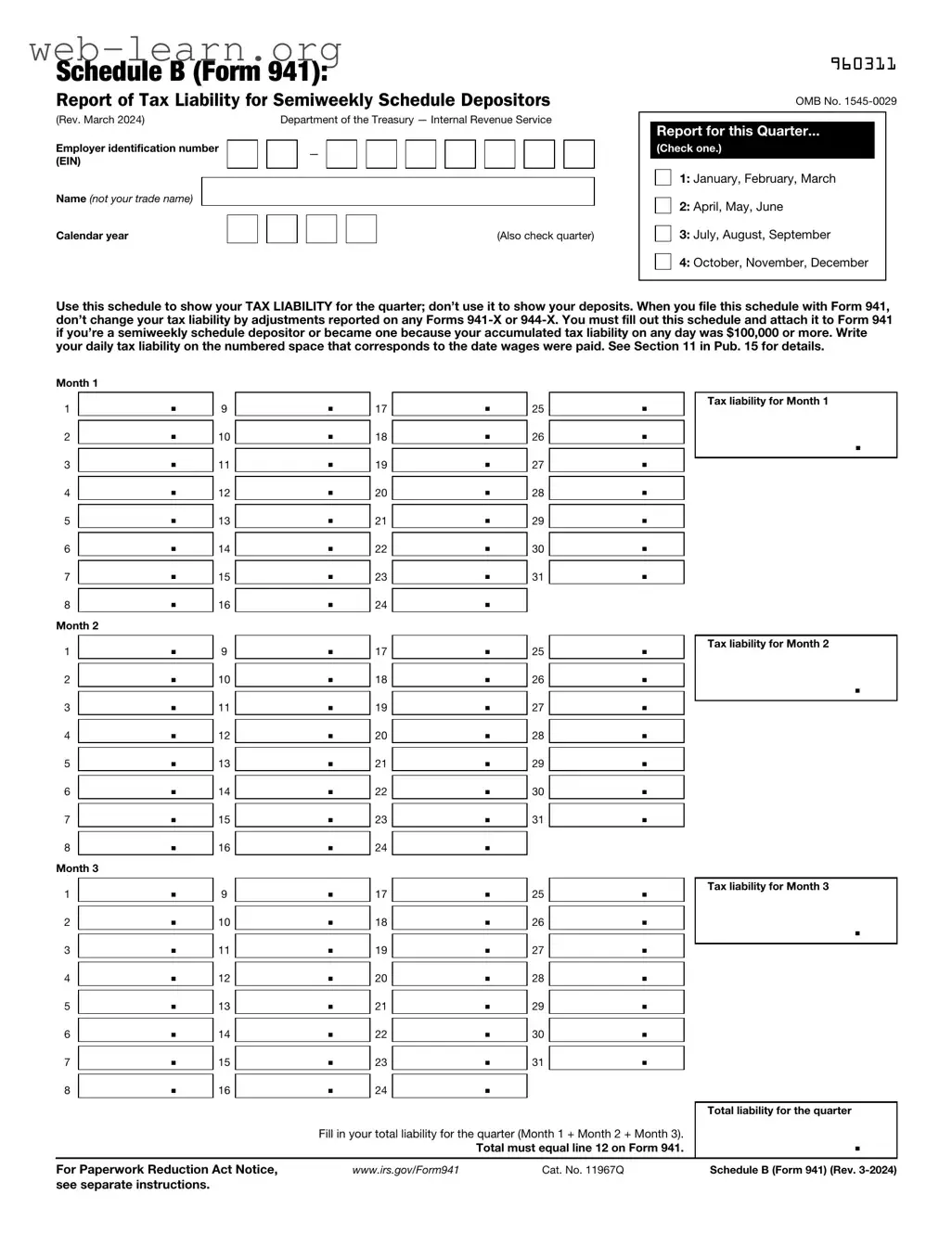

The IRS Schedule B (Form 941) is a critical document for employers, serving as a vital tool in accurately reporting employment taxes. This form specifically tracks the employer's portion of Social Security and Medicare taxes, along with federal income tax withheld from employees' paychecks. Employers must file this form quarterly, ensuring that they remain compliant with federal tax regulations. It captures essential information regarding the total wages paid, tips reported, and the number of employees on payroll. Additionally, Schedule B helps the IRS monitor tax liabilities and ensures that the correct amounts are deposited throughout the year. Missing deadlines or inaccuracies in this form can lead to penalties, making it imperative for employers to understand its requirements thoroughly. As the tax landscape continues to evolve, staying informed about the nuances of Schedule B is crucial for maintaining compliance and avoiding costly mistakes.

Schedule B (Form 941):

Report of Tax Liability for Semiweekly Schedule Depositors

(Rev. March 2024) |

|

|

Department of the Treasury — Internal Revenue Service |

|||||||||||||||||||

Employer identification number |

|

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

(EIN) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name (not your trade name) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Calendar year |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Also check quarter) |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

960311

OMB No.

Report for this Quarter...

(Check one.)

1: January, February, March

2: April, May, June

3: July, August, September

4: October, November, December

Use this schedule to show your TAX LIABILITY for the quarter; don’t use it to show your deposits. When you file this schedule with Form 941, don’t change your tax liability by adjustments reported on any Forms

Month 1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

|

. |

9 |

|

. |

|

17 |

|

. |

25 |

|

. |

|

Tax liability for Month 1 |

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

2 |

|

. |

10 |

|

. |

|

18 |

|

. |

26 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

|

. |

11 |

|

. |

|

19 |

|

. |

27 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

|

. |

12 |

|

. |

|

20 |

|

. |

28 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

|

. |

13 |

|

. |

|

21 |

|

. |

29 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6 |

|

. |

14 |

|

. |

|

22 |

|

. |

30 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

|

. |

15 |

|

. |

|

23 |

|

. |

31 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

|

. |

16 |

|

. |

|

24 |

|

. |

|

|

|

|

|

Month 2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

|

. |

9 |

|

. |

|

17 |

|

. |

25 |

|

. |

|

Tax liability for Month 2 |

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

2 |

|

. |

10 |

|

. |

|

18 |

|

. |

26 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

|

. |

11 |

|

. |

|

19 |

|

. |

27 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

|

. |

12 |

|

. |

|

20 |

|

. |

28 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

|

. |

13 |

|

. |

|

21 |

|

. |

29 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6 |

|

. |

14 |

|

. |

|

22 |

|

. |

30 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

|

. |

15 |

|

. |

|

23 |

|

. |

31 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

|

. |

16 |

|

. |

|

24 |

|

. |

|

|

|

|

|

Month 3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

|

. |

9 |

|

. |

|

17 |

|

. |

25 |

|

. |

|

Tax liability for Month 3 |

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

2 |

|

. |

10 |

|

. |

|

18 |

|

. |

26 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

|

. |

11 |

|

. |

|

19 |

|

. |

27 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

|

. |

12 |

|

. |

|

20 |

|

. |

28 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

|

. |

13 |

|

. |

|

21 |

|

. |

29 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6 |

|

. |

14 |

|

. |

|

22 |

|

. |

30 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

|

. |

15 |

|

. |

|

23 |

|

. |

31 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

|

. |

16 |

|

. |

|

24 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total liability for the quarter |

|

|

|

|

|

Fill in your total liability for the quarter (Month 1 + Month 2 + Month 3). |

|

. |

|||||||

|

|

|

|

|

|

|

|

|

Total must equal line 12 on Form 941. |

|

||||

For Paperwork Reduction Act Notice, |

|

www.irs.gov/Form941 |

|

Cat. No. 11967Q |

|

|

Schedule B (Form 941) (Rev. |

|||||||

see separate instructions. |

|

|

|

|

|

|

|

|

|

|

|

|

||

| Fact Name | Description |

|---|---|

| Purpose | The IRS Schedule B (Form 941) is used by employers to report their share of Social Security and Medicare taxes, as well as income tax withheld from employees' wages. |

| Filing Frequency | This form must be filed quarterly, along with Form 941, which is the Employer's Quarterly Federal Tax Return. |

| State-Specific Forms | Some states require additional forms for reporting state income tax withholding. For example, California requires Form DE 9. |

| Governing Laws | Federal laws governing the use of Schedule B include the Internal Revenue Code (IRC) sections related to employment taxes. |

Completing the IRS Schedule B (Form 941) is essential for employers to report their tax liabilities accurately. After filling out the form, it is crucial to review all information for accuracy before submission to avoid any potential issues with the IRS.

What is IRS Schedule B (Form 941)?

IRS Schedule B (Form 941) is a form used by employers to report their tax liabilities for federal income tax withholding and Social Security and Medicare taxes. It provides a detailed account of the wages paid to employees and the taxes withheld during a specific quarter. This form is an essential part of the quarterly payroll tax return, Form 941.

Who needs to file Schedule B?

Employers who report tax liabilities of $100,000 or more in a single deposit period during the current or previous year must file Schedule B. This applies to both small and large businesses. If your tax liability does not reach this threshold, you do not need to submit Schedule B with your Form 941.

When is Schedule B due?

Schedule B is due at the same time as Form 941. Generally, Form 941 must be filed quarterly, with deadlines falling on the last day of the month following the end of each quarter. For example, for the first quarter ending March 31, the due date is April 30.

How do I complete Schedule B?

To complete Schedule B, you will need to provide information about your tax liabilities for each month in the quarter. This includes:

Follow the instructions provided on the form carefully to ensure accurate reporting.

What happens if I don't file Schedule B when required?

If you are required to file Schedule B but fail to do so, the IRS may impose penalties. These penalties can include fines for late filing and interest on any unpaid taxes. It is crucial to stay compliant to avoid these consequences.

Can I file Schedule B electronically?

Yes, you can file Schedule B electronically if you are filing Form 941 electronically. Many payroll software programs allow for electronic filing, making the process more efficient and reducing the risk of errors.

Where can I find Schedule B?

You can find IRS Schedule B (Form 941) on the IRS website. It is available for download in PDF format, and you can also access instructions for completing the form. Always ensure you are using the most current version of the form.

What if I make a mistake on Schedule B?

If you realize that you made a mistake on Schedule B after submitting it, you should correct it as soon as possible. You can do this by filing an amended Form 941. Be sure to follow the IRS guidelines for making corrections to ensure proper handling of your tax records.

Where do I send Schedule B once it's completed?

The completed Schedule B should be submitted along with Form 941 to the address specified in the form's instructions. The mailing address may vary depending on your location and whether you are enclosing a payment.

Filling out IRS Schedule B (Form 941) can be a straightforward task, but many people make common mistakes that can lead to complications. One frequent error is failing to report all wages accurately. Employers must ensure that the total wages paid during the quarter are correctly reflected. Omitting even a small amount can result in discrepancies that may trigger an audit.

Another mistake is miscalculating the tax liability. Employers need to apply the correct tax rates to the wages reported. If the calculations are off, it could lead to underpayment or overpayment of taxes, which can create issues with the IRS. Keeping detailed records of payroll can help prevent this mistake.

Some individuals neglect to check for updates to tax laws or IRS guidelines. Tax regulations can change frequently, and it is essential to stay informed. Failing to comply with the latest requirements may lead to incorrect filings, which can result in penalties.

Inaccurate reporting of tax credits is another common error. Employers may not realize they qualify for certain credits or may miscalculate the amounts. This oversight can affect the overall tax liability and potentially reduce the benefits available to the employer.

Additionally, many people forget to sign and date the form. An unsigned form is considered incomplete and can lead to delays in processing. It is crucial to review the form thoroughly before submission to ensure all required signatures are present.

Some filers also make the mistake of not keeping copies of submitted forms. Retaining a copy of the Schedule B is essential for record-keeping and can assist in resolving any future discrepancies with the IRS. Without documentation, it becomes challenging to prove compliance.

Lastly, individuals often misinterpret the instructions for completing the form. Each section has specific requirements, and misunderstanding these can lead to errors. Taking the time to read the instructions carefully can help avoid mistakes and ensure accurate reporting.

The IRS Schedule B (Form 941) is an important document for employers, as it provides detailed information about their tax liabilities and payments related to employee wages. Alongside this form, there are several other documents that are commonly used to ensure compliance with federal tax regulations. Below is a list of four such forms and documents, each serving a specific purpose in the overall tax reporting process.

Understanding these forms and their purposes is crucial for employers to maintain compliance with tax obligations. Properly completing and submitting these documents helps avoid penalties and ensures that employees receive accurate information for their own tax filings.

The IRS Schedule B (Form 941) is an important document for employers to report their federal income tax withholding and Social Security and Medicare taxes. Several other forms share similarities with Schedule B in terms of purpose and information required. Here are five documents that are comparable:

When filling out the IRS Schedule B (Form 941), it’s important to be careful and thorough. Here are five things you should and shouldn’t do to ensure accurate completion of the form.

Taking these steps will help you navigate the process smoothly and reduce the risk of errors. If you have questions, seeking professional assistance is advisable.

The IRS Schedule B (Form 941) is an important document for employers. However, there are several misconceptions surrounding it. Here are eight common misunderstandings:

This is not true. Any employer who is required to file Form 941 must also complete Schedule B if they meet certain criteria, regardless of their size.

Some employers believe they can skip Schedule B if they don't have any tax liability. However, if you are required to file Form 941, you must also include Schedule B when applicable.

This form is primarily used to report tax liability for federal income tax withholding and Social Security and Medicare taxes, not just wages.

Completing Schedule B does not ensure a refund. It simply reports your tax liability and any adjustments that may affect your overall tax situation.

Each tax form serves a different purpose. Schedule B is specific to reporting employment tax liabilities, while other forms may focus on different aspects of taxation.

Employers must submit Schedule B for each quarter in which they file Form 941. It is not a one-time requirement.

Any mistakes on Schedule B can lead to penalties or issues with tax compliance. It is crucial to review the form carefully before submission.

Schedule B must be filed along with Form 941. They are interconnected, and one cannot be submitted without the other.

Understanding these misconceptions can help ensure accurate filing and compliance with IRS regulations. Always consider consulting a tax professional for personalized guidance.

Understanding the IRS Schedule B (Form 941) is essential for employers who need to report their payroll taxes accurately. Here are some key takeaways to keep in mind:

By keeping these points in mind, you can navigate the requirements of the IRS Schedule B (Form 941) with greater confidence and accuracy.