The IRS Power of Attorney (Form 2848) serves as a crucial tool for taxpayers who wish to authorize someone else to represent them before the Internal Revenue Service. This form allows individuals to appoint an attorney, accountant, or other qualified representative to handle specific tax matters on their behalf. By completing this form, taxpayers can ensure that their representatives have the authority to receive confidential information, discuss tax issues, and even sign documents related to their tax affairs. It is important to note that the form must clearly specify the tax matters and the years or periods for which the representation is granted. Additionally, taxpayers can revoke this authorization at any time, providing them with flexibility and control over who manages their tax responsibilities. Understanding the nuances of Form 2848 can help individuals navigate their interactions with the IRS more effectively, making it an essential resource for anyone facing tax-related challenges.

Check Form for Common Errors & Reminders

Form 2848 |

|

Power of Attorney |

For IRS Use Only |

|||||

|

|

|

|

OMB No. |

||||

(Rev. January 2021) |

and Declaration of Representative |

|

|

|

|

|

||

Received by: |

|

|||||||

Department of the Treasury |

|

|

|

|||||

▶ Go to www.irs.gov/Form2848 for instructions and the latest information. |

|

|

|

|

|

|||

Internal Revenue Service |

Name |

|

|

|||||

|

|

|

||||||

Part I |

Power of Attorney |

Telephone |

|

|

||||

|

Caution: A separate Form 2848 must be completed for each taxpayer. Form 2848 will not be honored |

Function |

|

|

||||

|

for any purpose other than representation before the IRS. |

Date |

/ / |

|||||

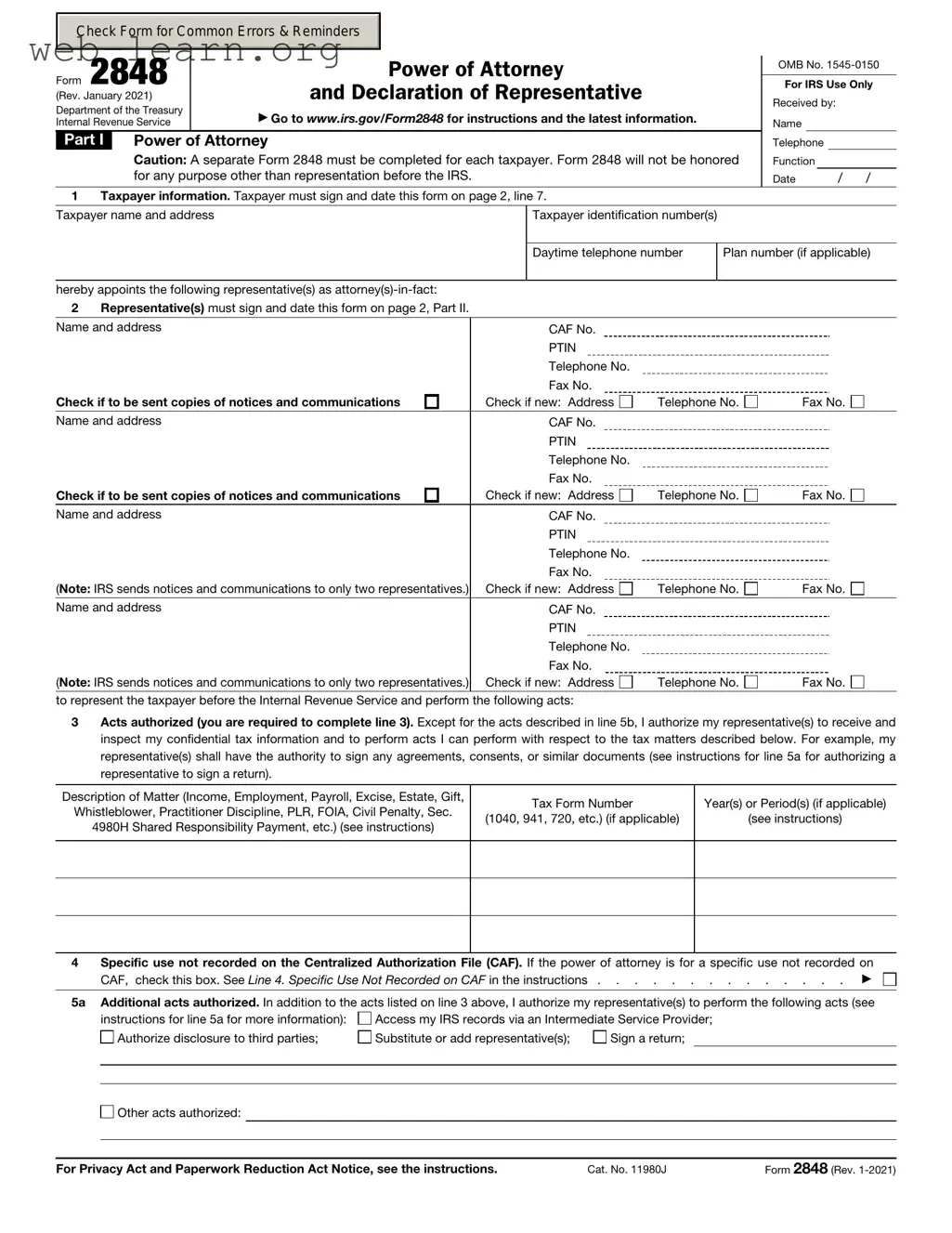

1Taxpayer information. Taxpayer must sign and date this form on page 2, line 7.

Taxpayer name and address |

Taxpayer identification number(s) |

Daytime telephone number

Plan number (if applicable)

Name and address |

CAF No. |

|

|

|

PTIN |

|

|

|

Telephone No. |

|

|

|

Fax No. |

|

|

Check if to be sent copies of notices and communications |

Check if new: Address |

Telephone No. |

Fax No. |

Name and address |

CAF No. |

|

|

|

PTIN |

|

|

|

Telephone No. |

|

|

|

Fax No. |

|

|

Check if to be sent copies of notices and communications |

Check if new: Address |

Telephone No. |

Fax No. |

Name and address |

CAF No. |

|

|

|

PTIN |

|

|

|

Telephone No. |

|

|

|

Fax No. |

|

|

(Note: IRS sends notices and communications to only two representatives.) |

Check if new: Address |

Telephone No. |

Fax No. |

Name and address |

CAF No. |

|

|

|

PTIN |

|

|

|

Telephone No. |

|

|

|

Fax No. |

|

|

(Note: IRS sends notices and communications to only two representatives.) |

Check if new: Address |

Telephone No. |

Fax No. |

to represent the taxpayer before the Internal Revenue Service and perform the following acts:

3Acts authorized (you are required to complete line 3). Except for the acts described in line 5b, I authorize my representative(s) to receive and inspect my confidential tax information and to perform acts I can perform with respect to the tax matters described below. For example, my representative(s) shall have the authority to sign any agreements, consents, or similar documents (see instructions for line 5a for authorizing a representative to sign a return).

Description of Matter (Income, Employment, Payroll, Excise, Estate, Gift, |

Tax Form Number |

Year(s) or Period(s) (if applicable) |

|

Whistleblower, Practitioner Discipline, PLR, FOIA, Civil Penalty, Sec. |

|||

(1040, 941, 720, etc.) (if applicable) |

(see instructions) |

||

4980H Shared Responsibility Payment, etc.) (see instructions) |

|||

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

Specific use not recorded on the Centralized Authorization File (CAF). If the power of attorney is for a specific use not recorded on |

|||

|

CAF, check this box. See Line 4. Specific Use Not Recorded on CAF in the instructions . |

. . . . . . . . . . . . . ▶ |

||

|

|

|

||

5a |

Additional acts authorized. In addition to the acts listed on line 3 above, I authorize my representative(s) to perform the following acts (see |

|||

|

instructions for line 5a for more information): |

Access my IRS records via an Intermediate Service Provider; |

||

|

Authorize disclosure to third parties; |

Substitute or add representative(s); |

Sign a return; |

|

|

|

|

|

|

|

|

|

|

|

Other acts authorized:

For Privacy Act and Paperwork Reduction Act Notice, see the instructions. |

Cat. No. 11980J |

Form 2848 (Rev. |

Form 2848 (Rev. |

Page 2 |

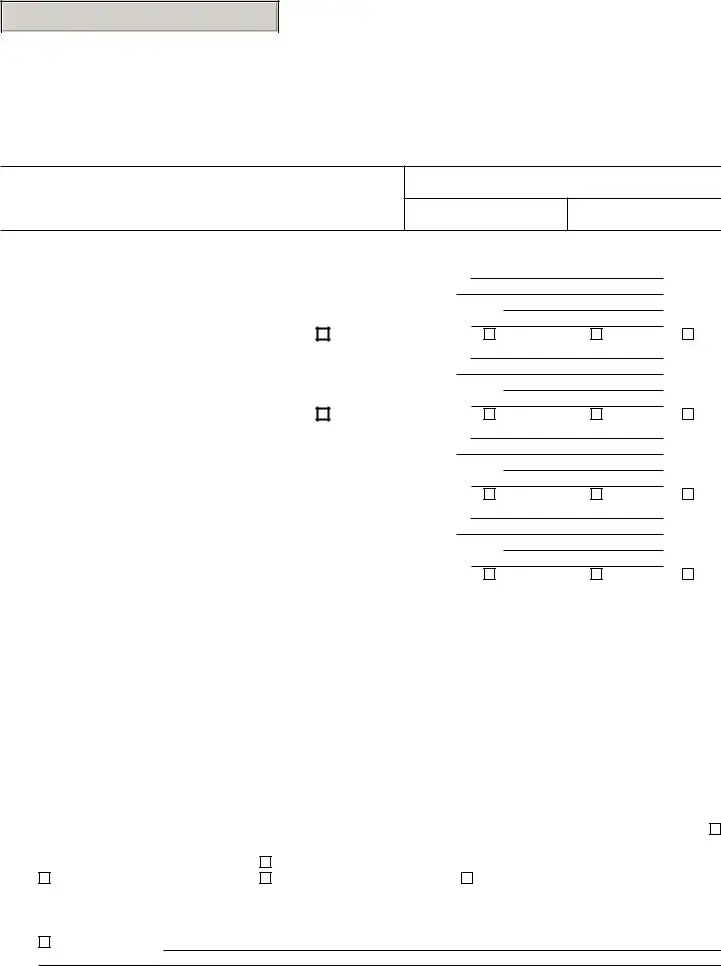

bSpecific acts not authorized. My representative(s) is (are) not authorized to endorse or otherwise negotiate any check (including directing or accepting payment by any means, electronic or otherwise, into an account owned or controlled by the representative(s) or any firm or other entity with whom the representative(s) is (are) associated) issued by the government in respect of a federal tax liability.

List any other specific deletions to the acts otherwise authorized in this power of attorney (see instructions for line 5b):

6Retention/revocation of prior power(s) of attorney. The filing of this power of attorney automatically revokes all earlier power(s) of attorney on file with the Internal Revenue Service for the same matters and years or periods covered by this form. If you do not want to

revoke a prior power of attorney, check here . . . . . . . . . . . . . . . . . . . . . . . . . . . ▶

YOU MUST ATTACH A COPY OF ANY POWER OF ATTORNEY YOU WANT TO REMAIN IN EFFECT.

7Taxpayer declaration and signature. If a tax matter concerns a year in which a joint return was filed, each spouse must file a separate power of attorney even if they are appointing the same representative(s). If signed by a corporate officer, partner, guardian, tax matters partner, partnership representative (or designated individual, if applicable), executor, receiver, administrator, trustee, or individual other than the taxpayer, I certify I have the legal authority to execute this form on behalf of the taxpayer.

▶ IF NOT COMPLETED, SIGNED, AND DATED, THE IRS WILL RETURN THIS POWER OF ATTORNEY TO THE TAXPAYER.

Signature |

Date |

Title (if applicable) |

Print name |

|

Print name of taxpayer from line 1 if other than individual |

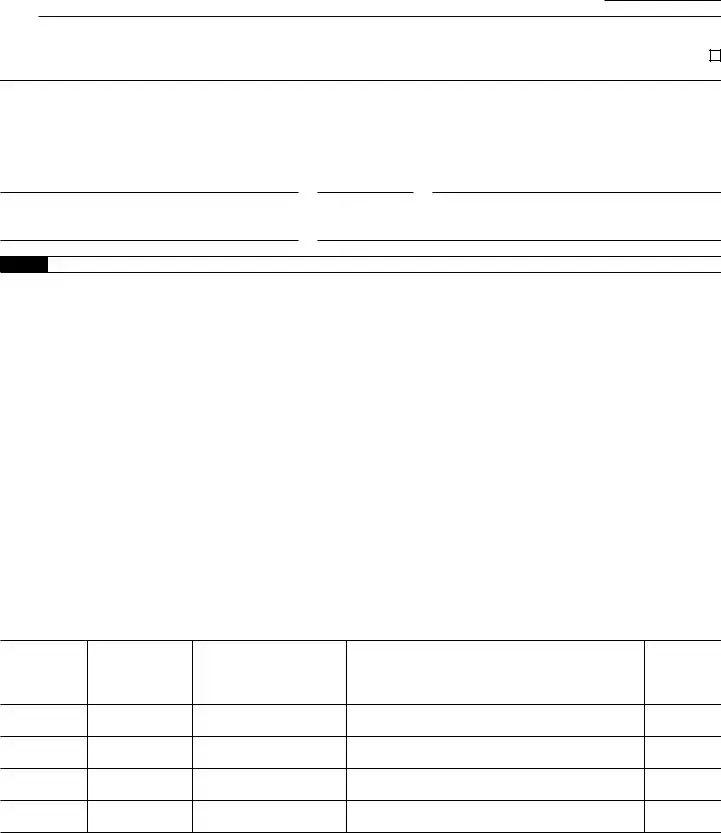

Part II Declaration of Representative

Under penalties of perjury, by my signature below I declare that:

•I am not currently suspended or disbarred from practice, or ineligible for practice, before the Internal Revenue Service;

•I am subject to regulations in Circular 230 (31 CFR, Subtitle A, Part 10), as amended, governing practice before the Internal Revenue Service;

•I am authorized to represent the taxpayer identified in Part I for the matter(s) specified there; and

•I am one of the following:

a

bCertified Public

cEnrolled

d

e

fFamily

gEnrolled

hUnenrolled Return

kQualifying Student or Law

rEnrolled Retirement Plan

▶IF THIS DECLARATION OF REPRESENTATIVE IS NOT COMPLETED, SIGNED, AND DATED, THE IRS WILL RETURN THE POWER OF ATTORNEY. REPRESENTATIVES MUST SIGN IN THE ORDER LISTED IN PART I, LINE 2.

Note: For designations

Designation—

Insert above

letter

Licensing jurisdiction

(State) or other

licensing authority

(if applicable)

Bar, license, certification, registration, or enrollment number (if applicable)

Signature

Date

Form 2848 (Rev.

| Fact Name | Description |

|---|---|

| Purpose | The IRS Power of Attorney (Form 2848) allows an individual to designate someone to represent them before the IRS. |

| Eligibility | Any U.S. citizen or resident can use Form 2848 to appoint a representative, such as a lawyer or accountant. |

| Signature Requirement | The taxpayer must sign the form to grant authority to the designated representative. |

| Scope of Authority | The form specifies the types of tax matters the representative can handle, such as income tax or estate tax. |

| Duration | The authority granted remains in effect until the taxpayer revokes it or the IRS processes a new form. |

| State-Specific Forms | Some states have their own Power of Attorney forms, governed by state law, such as California's Probate Code. |

| Submission | The completed Form 2848 must be submitted to the IRS, either by mail or fax, depending on the situation. |

| Revocation | Taxpayers can revoke the Power of Attorney at any time by submitting a written notice to the IRS. |

Filling out the IRS Power of Attorney (Form 2848) allows you to designate someone to represent you before the IRS. After completing the form, you will submit it to the IRS to grant the designated representative the authority to act on your behalf regarding tax matters.

What is the IRS Power of Attorney (Form 2848)?

The IRS Power of Attorney, officially known as Form 2848, is a document that allows you to appoint someone to represent you before the Internal Revenue Service. This representative can be an attorney, certified public accountant, or enrolled agent. By completing this form, you grant them the authority to discuss your tax matters, receive confidential information, and make decisions on your behalf regarding your tax issues.

What information do I need to provide on Form 2848?

When filling out Form 2848, you will need to provide several key pieces of information:

Make sure all information is accurate to avoid delays in processing your request.

How long is the Power of Attorney valid?

The IRS Power of Attorney remains in effect until you revoke it, the representative withdraws, or the IRS processes a new Form 2848 that supersedes the previous one. If you want to cancel the authorization, you must submit a written notice to the IRS, indicating your desire to revoke the power granted to your representative.

Can I use Form 2848 for state tax matters?

No, Form 2848 is specifically designed for federal tax matters with the IRS. If you need to appoint someone for state tax issues, you will have to check with your state’s tax authority for their specific requirements and forms. Each state has its own rules regarding power of attorney for tax matters.

When filling out the IRS Power of Attorney (Form 2848), individuals often encounter several pitfalls that can lead to complications in their tax matters. One common mistake is failing to provide complete information about the representative. The IRS requires the representative's name, address, and identification number. Omitting any of these details can delay the processing of the form and hinder the representative's ability to act on behalf of the taxpayer.

Another frequent error involves not specifying the exact tax matters for which the power of attorney is granted. The form allows taxpayers to designate specific tax issues, such as income tax or estate tax. If this section is left blank or filled out vaguely, it could lead to confusion regarding the authority granted to the representative.

Additionally, many people neglect to sign and date the form. This may seem like a minor oversight, but without a signature, the IRS will not accept the document. It is crucial for taxpayers to ensure that they sign the form in the appropriate section and include the date to validate the request.

Another mistake is failing to indicate the correct year or period for which the power of attorney is being granted. If a taxpayer intends to authorize representation for a specific tax year but does not specify it, the IRS might interpret the request differently. This can create unnecessary complications and misunderstandings.

Moreover, some individuals mistakenly believe they can submit the form electronically. While the IRS does allow for electronic submission of some forms, the Power of Attorney (Form 2848) must be submitted in paper format. Understanding this requirement is vital to ensure that the form reaches the IRS without delays.

People also frequently overlook the importance of including a phone number for the representative. A contact number can facilitate communication between the IRS and the representative, especially if there are questions or issues that arise during the processing of the form.

Another common error is not updating the form when a representative changes. If a taxpayer decides to appoint a new representative, they must submit a new Form 2848. Failing to do so can result in the previous representative retaining authority, which can complicate matters if the new representative is needed.

In addition, some individuals forget to check the box indicating whether the power of attorney should remain in effect after the taxpayer's death. This decision is crucial, especially for those who want their representatives to continue managing tax matters in the event of their passing.

Lastly, a significant mistake involves not retaining a copy of the completed form. Taxpayers should always keep a copy of any documents submitted to the IRS, including Form 2848. This ensures that they have a record of the authority granted and can refer back to it if needed.

By being aware of these common mistakes, individuals can navigate the process of filling out the IRS Power of Attorney (Form 2848) more effectively. Taking the time to review the form carefully can save significant time and trouble in the long run.

The IRS Power of Attorney (Form 2848) allows taxpayers to authorize an individual to represent them before the IRS. When utilizing this form, there are several other documents that may also be necessary to ensure a smooth process. Below is a list of common forms and documents that often accompany Form 2848.

Understanding these additional forms can help streamline the process when dealing with the IRS. Each document serves a specific purpose and can aid in effectively managing tax-related issues.

The IRS Power of Attorney (Form 2848) allows individuals to designate someone to represent them before the IRS. Several other documents serve similar purposes in different contexts. Below is a list of documents that share characteristics with Form 2848:

When filling out the IRS Power of Attorney (Form 2848), it's essential to follow specific guidelines to ensure your form is accurate and effective. Here are some key dos and don'ts:

The IRS Power of Attorney (Form 2848) is a useful tool for taxpayers who want to authorize someone to represent them in dealings with the IRS. However, there are several misconceptions surrounding this form that can lead to confusion. Here are seven common misunderstandings:

This is not true. The Power of Attorney only allows the designated representative to handle specific tax matters with the IRS. It does not grant them control over your entire financial situation.

In fact, you can revoke a Power of Attorney at any time. You simply need to notify the IRS in writing and submit a new Form 2848 if you wish to appoint someone else.

This is incorrect. You can appoint anyone you trust, including family members or friends, as your representative on the Form 2848, as long as they are willing to act on your behalf.

The authority granted by the Power of Attorney is not permanent. It remains in effect until you revoke it, the representative can no longer act on your behalf, or the IRS closes your case.

Your representative can act on your behalf without your presence. They can communicate with the IRS and receive information as authorized by you on the Form 2848.

This is a common misconception. You do not need to attach the Form 2848 to your tax return. Instead, you submit it directly to the IRS, and it will be processed separately.

Submitting Form 2848 does not mean the IRS will stop contacting you. Your representative will handle communications, but you may still receive notices or requests for information directly.

Understanding these misconceptions can help you make informed decisions about who you choose to represent you and how to manage your tax affairs effectively.

Here are some key takeaways about filling out and using the IRS Power of Attorney (Form 2848):