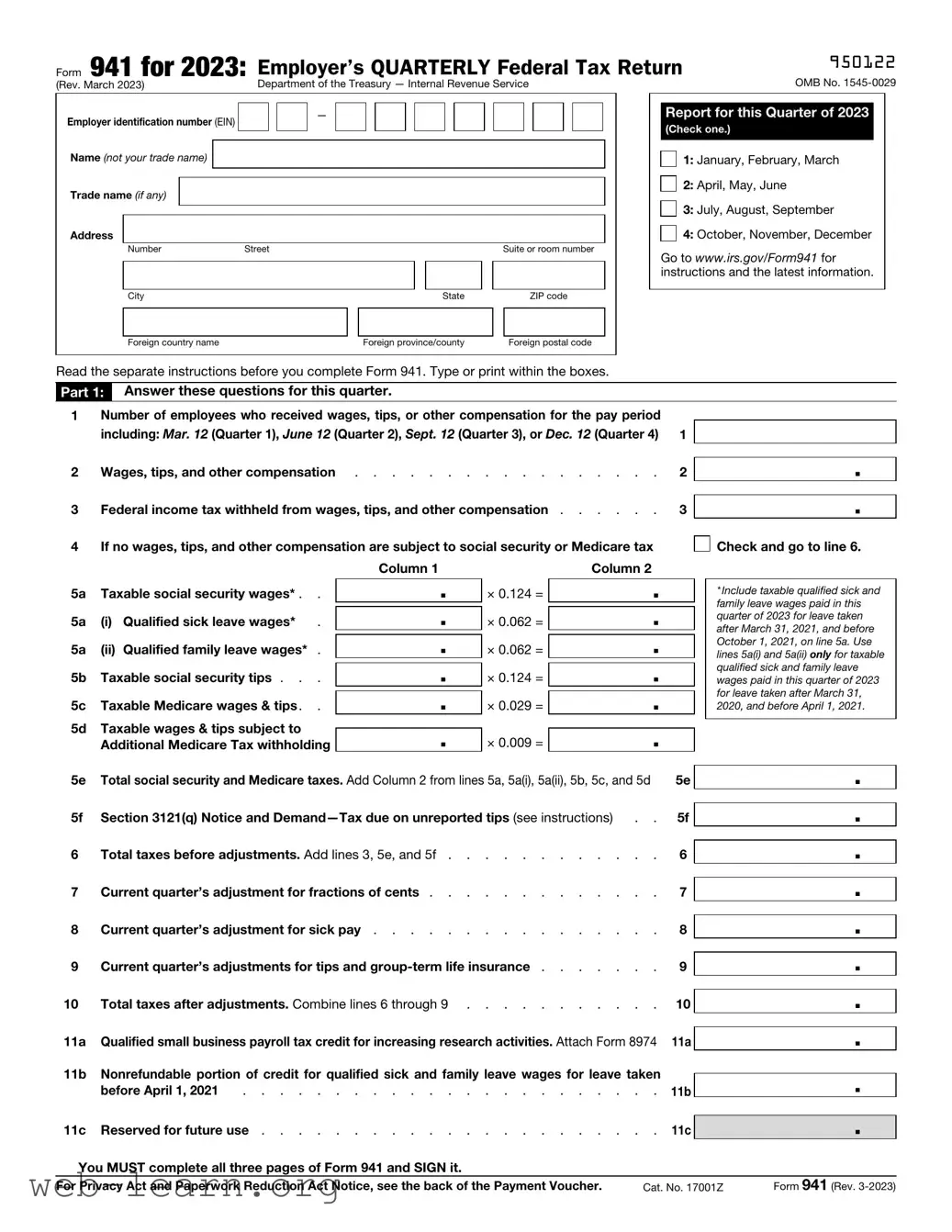

The IRS Form 941, also known as the Employer's Quarterly Federal Tax Return, plays a vital role in managing payroll taxes for businesses across the United States. This form is used to report income taxes, Social Security taxes, and Medicare taxes that employers have withheld from employees' paychecks. Each quarter, businesses must accurately report these figures to ensure compliance with federal tax obligations. Understanding the major sections of Form 941, including the calculation of payroll and adjustments for tax credits, can help employers maintain accuracy and avoid penalties. In addition to reporting withheld taxes, the form captures data about overall employee wages and hours worked, which assists the IRS in tracking employment and ensuring the collection of the appropriate taxes. Filing this form on time is essential, as delays can result in fines or increased scrutiny from the IRS. Being proactive about quarterly updates and understanding the implications of this form can facilitate smoother operations and foster a positive relationship with tax authorities.

| Fact | Details |

|---|---|

| Purpose | The IRS Form 941 is used by employers to report federal income tax, Social Security tax, and Medicare tax withheld from employees' paychecks. |

| Filing Frequency | Employers must file Form 941 quarterly, typically due by the last day of the month following the end of each quarter. |

| Eligibility | This form applies to most employers who pay wages to employees, with few exceptions for certain types of organizations. |

| State-Specific Requirements | In addition to federal requirements, states may have their own payroll tax forms. For example, California requires Form DE-9 for employer payroll taxes. |

| Penalties | Failure to file Form 941 on time or to pay the owed taxes can result in penalties and interest charges. |

| Recordkeeping | Employers are required to maintain records of their employees’ wages, tax withheld, and hours worked, typically for at least four years. |

| Amended Returns | If an error is discovered on a previously filed Form 941, employers can file Form 941-X to amend their original submission. |

Once you have gathered all necessary information, the next step is to carefully fill out IRS Form 941. This form is important for reporting taxes withheld from your employees’ paychecks. Follow these steps to ensure that you complete the form accurately.

After completing the form, keep a copy for your records. This documentation is helpful for future reference and may be necessary for audits or inquiries from the IRS.

IRS Form 941 is used by employers to report income taxes, Social Security tax, and Medicare tax withheld from employees’ wages. This form also indicates the employer's share of Social Security and Medicare taxes. Employers must file this form quarterly.

Employers who pay wages to employees need to file Form 941. This includes businesses, organizations, and any entity that hires staff and withholds federal income, Social Security, and Medicare taxes. If you have no employees during the quarter, you may not need to file.

Form 941 must be filed on a quarterly basis. The due dates for each quarterly return are:

If a due date falls on a weekend or holiday, the next business day becomes the filing deadline.

Form 941 can be filed electronically or by mail. Many employers choose to use IRS e-file for a faster and more efficient process. If filing by mail, send the completed form to the address indicated in the instructions for the form based on your business location.

Form 941 requires several details, including:

Filing Form 941 late can lead to penalties and interest on any unpaid taxes. The IRS imposes a failure-to-file penalty, which starts at 5% of your unpaid tax for each month the return is late, up to a maximum of 25%. It’s important to file on time to avoid these additional costs.

Yes, you can amend Form 941 by submitting Form 941-X, Adjusted Employer’s QUARTERLY Federal Tax Return or Claim for Refund. This form allows you to correct errors in a previously filed Form 941. Be sure to follow the specific guidelines for making corrections to avoid further complications.

Filling out the IRS 941 form can feel daunting, but avoiding common mistakes can make the process smoother. One major error occurs when taxpayers forget to check all necessary boxes. The form requires various sections to be completed based on your specific business situation. If you fail to check the right boxes, you might misreport your payroll taxes. Always double-check to ensure you’ve acknowledged all the relevant sections.

Another frequent mistake is miscalculating employee wages and tax withholdings. Accurate math is crucial, yet many people either add or subtract incorrectly. This error can lead to underpayment or overpayment of taxes, bringing complications and penalties later on. Using a calculator or tax software can help ensure these figures are correct.

An equally significant oversight is neglecting to sign and date the form. Even if all information is accurate, the IRS will not process unsignatured forms. It may feel like a small detail, but without your signature, your form lacks validity. Make sure to date your submission as well to avoid confusion regarding when you filed.

Lastly, not maintaining records of filed forms can lead to serious problems. The IRS expects businesses to keep copies of their filed forms for at least four years. If you ever face an audit, having these records will save you time and stress. Make it a habit to store all your tax documents securely.

The IRS Form 941, also known as the Employer's Quarterly Federal Tax Return, is a crucial document that employers use to report income taxes, Social Security tax, and Medicare tax withheld from employee wages. There are several other forms and documents that are often used in conjunction with Form 941 to ensure comprehensive reporting and compliance with federal tax obligations. Below is a list of related documents that play significant roles in the payroll tax reporting system.

Each of these forms and documents serves a specific purpose in the broader framework of federal tax reporting. Understanding the relationship between Form 941 and these related forms is essential for employers striving to maintain compliance and ensure accurate reporting of payroll taxes.

When filling out the IRS Form 941, it's crucial to get it right to avoid potential penalties and ensure compliance. Here's a helpful list of things to do and things to avoid.

By following these guidelines, you help safeguard your business against common pitfalls associated with IRS Form 941. Always consider keeping a copy of the completed form for your records.

This is not true. Form 941 must be filed by all employers who withhold payroll taxes, regardless of the number of employees. Whether you have one employee or hundreds, if you pay wages and withholding, you’re required to file this form.

In reality, Form 941 is filed quarterly. Employers must submit it four times a year, reflecting the wages paid and taxes withheld during each quarter. Missing a filing deadline can lead to penalties.

This is a common belief, but it's misleading. Any business that pays employees and deducts taxes must submit Form 941, regardless of its size. This includes small businesses and sole proprietorships.

Some assume that once they file the form, they do not need to think about it again until the next tax year. However, Form 941 is an ongoing obligation. Employers must properly keep records and ensure they are accurately filing it each quarter.

The IRS Form 941 is a quarterly tax form used by employers to report income taxes, Social Security tax, and Medicare tax withheld from employee paychecks.

It is crucial to file Form 941 on time to avoid penalties and interest. The due dates for filing are typically the last day of the month following the end of each quarter.

Ensure that all information is accurate. Inaccuracies can lead to complications with the IRS and potential delays in processing.

Employers must fill out specific sections including the number of employees, wages paid, and the amounts withheld for taxes.

If you have more than one business location, you need to report the combined totals on a single Form 941 unless you’re filing for a seasonal employer.

Remember to keep copies of each filed Form 941 for your records. This can assist in future filings and in case of an audit.

Using the Correct Calculation of Taxes is essential. Double-check the tax rates for Social Security and Medicare as they may change from year to year.

If you are unsure about how to fill out the form or what amounts to report, consider seeking assistance from a tax professional.

Health Care Provider Disease Reporting Document - It underscores the need for thorough documentation in health care settings.

Judicial Council Forms - The form can be obtained from the Bureau of Real Estate's website or their offices.

What Is Form 104 Colorado - This form plays a crucial role in your overall tax filing for the year.