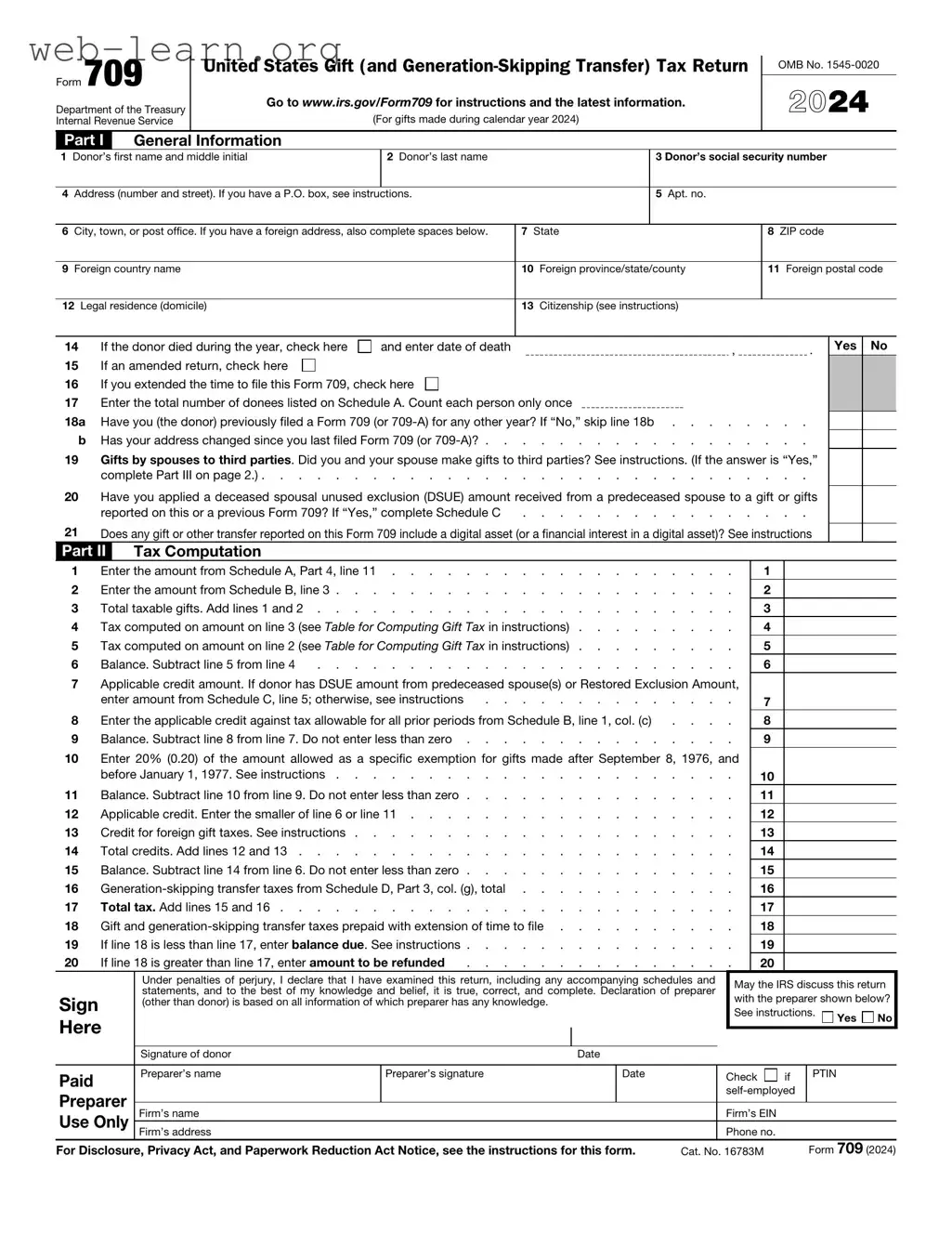

The IRS 709 form, also known as the United States Gift (and Generation-Skipping Transfer) Tax Return, plays a crucial role in the realm of gift taxation. This form is primarily used by individuals who have made gifts exceeding the annual exclusion limit, which is adjusted periodically. Understanding the nuances of this form is essential for anyone who wishes to navigate the complexities of gift giving while staying compliant with federal tax regulations. By filing the 709 form, taxpayers report gifts made during the year, as well as any applicable generation-skipping transfers, which can impact the tax obligations of both the giver and the recipient. Additionally, the form allows individuals to claim the lifetime gift tax exclusion, a significant benefit that can help reduce overall tax liability. Filing this form accurately is important, as it ensures that all taxable gifts are properly accounted for and helps avoid potential penalties from the IRS. Overall, the IRS 709 form serves as a vital tool for managing personal finances and understanding the implications of generous acts.

Form 709 |

United States Gift (and |

|

|

||

Department of the Treasury |

Go to www.irs.gov/Form709 for instructions and the latest information. |

|

(For gifts made during calendar year 2024) |

||

Internal Revenue Service |

Part I General Information

OMB No.

2024

1Donor’s first name and middle initial

2Donor’s last name

3 Donor’s social security number

4Address (number and street). If you have a P.O. box, see instructions.

5Apt. no.

6City, town, or post office. If you have a foreign address, also complete spaces below.

7State

8ZIP code

9Foreign country name

10Foreign province/state/county

11Foreign postal code

12Legal residence (domicile)

13Citizenship (see instructions)

14 |

If the donor died during the year, check here |

and enter date of death |

, |

. |

15 |

If an amended return, check here |

|

|

|

16 |

If you extended the time to file this Form 709, check here |

|

|

|

17Enter the total number of donees listed on Schedule A. Count each person only once

18a |

Have you (the donor) previously filed a Form 709 (or |

b |

Has your address changed since you last filed Form 709 (or |

19Gifts by spouses to third parties. Did you and your spouse make gifts to third parties? See instructions. (If the answer is “Yes,”

complete Part III on page 2.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

20Have you applied a deceased spousal unused exclusion (DSUE) amount received from a predeceased spouse to a gift or gifts

reported on this or a previous Form 709? If “Yes,” complete Schedule C |

. . . . . . . . . . . . . . . . |

21Does any gift or other transfer reported on this Form 709 include a digital asset (or a financial interest in a digital asset)? See instructions

Part II Tax Computation

Yes No

1 |

Enter the amount from Schedule A, Part 4, line 11 |

|

2 |

Enter the amount from Schedule B, line 3 |

|

3 |

Total taxable gifts. Add lines 1 and 2 |

|

4 |

Tax computed on amount on line 3 (see Table for Computing Gift Tax in instructions) |

|

5 |

Tax computed on amount on line 2 (see Table for Computing Gift Tax in instructions) |

|

6 |

Balance. Subtract line 5 from line 4 |

. . . . . . . . . . . . . . . . . . . . . . . |

7Applicable credit amount. If donor has DSUE amount from predeceased spouse(s) or Restored Exclusion Amount,

|

enter amount from Schedule C, line 5; otherwise, see instructions |

. . . . . . . . . . . . . . |

|

8 |

Enter the applicable credit against tax allowable for all prior periods from Schedule B, line 1, col. (c) |

. . . . |

|

9 |

Balance. Subtract line 8 from line 7. Do not enter less than zero |

||

10Enter 20% (0.20) of the amount allowed as a specific exemption for gifts made after September 8, 1976, and

|

before January 1, 1977. See instructions |

|

11 |

Balance. Subtract line 10 from line 9. Do not enter less than zero |

|

12 |

Applicable credit. Enter the smaller of line 6 or line 11 |

|

13 |

Credit for foreign gift taxes. See instructions |

|

14 |

Total credits. Add lines 12 and 13 |

|

15 |

Balance. Subtract line 14 from line 6. Do not enter less than zero |

|

16 |

||

17 |

Total tax. Add lines 15 and 16 |

|

18 |

Gift and |

|

19 |

If line 18 is less than line 17, enter balance due. See instructions |

|

20 |

If line 18 is greater than line 17, enter amount to be refunded |

. . . . . . . . . . . . . . . |

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

|

Under penalties of perjury, I declare that I have examined this return, including any accompanying schedules and |

|

May the IRS discuss this return |

||||||||

|

statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer |

|

|||||||||

Sign |

|

with the preparer shown below? |

|||||||||

(other than donor) is based on all information of which preparer has any knowledge. |

|

|

|

|

|||||||

|

|

|

|

|

See instructions. |

|

|

||||

Here |

|

|

|

|

|

|

Yes |

No |

|||

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Signature of donor |

|

Date |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Paid |

Preparer’s name |

Preparer’s signature |

|

Date |

|

Check |

if |

PTIN |

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|||

Preparer |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

Firm’s name |

|

|

|

|

Firm’s EIN |

|

|

|

|

||

Use Only |

|

|

|

|

|

|

|

|

|||

Firm’s address |

|

|

|

|

Phone no. |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|||

For Disclosure, Privacy Act, and Paperwork Reduction Act Notice, see the instructions for this form. |

Cat. No. 16783M |

|

Form 709 (2024) |

||||||||

Form 709 (2024) |

|

Page 2 |

|

Part III |

Spouse’s Consent on Gifts to Third Parties |

|

|

1 Gifts by spouses to third parties. Do you consent to have the gifts (including |

Yes |

No |

|

|

|

||

by your spouse to third parties during the calendar year considered as made |

|

|

|

answer is “Yes,” the following information must be furnished. If the answer is “No,” skip lines |

|

|

|

2Name of consenting spouse

3SSN of consenting spouse

4 |

Were you married to one another during the entire calendar year? See instructions |

. . . . . . . . . . . . . |

||||

5 |

If line 4 is “No,” check whether |

married |

divorced or |

widowed/deceased, and give date. See instructions |

|

|

6 |

Will a gift tax return for this year be filed by your spouse? If “Yes,” mail both returns in the same envelope |

. . . . . . |

||||

7Consent of Spouse. Have you obtained required spousal consent for gifts made to third parties to be considered as made

Form 709 (2024)

Form 709 (2024) |

Page 3 |

SCHEDULE A Computation of Taxable Gifts (Including transfers in trust) (see instructions)

A |

Does the value of any item listed on Schedule A reflect any valuation discount? If “Yes,” attach explanation |

Yes |

No |

BIf you elect under section 529(c)(2)(B) to treat any transfers made this year to a qualified tuition program as made ratably over a

(a)

Item

number

(b)

Donee’s name and address

(c)

Relationship

to donor

(if any)

(d)

Description of gift

(e)

Donor’s

adjusted basis

of gift

(f) |

(g) |

Date of gift |

Value at |

date of gift

(h) |

(i) |

For split |

Net transfer |

gifts, enter |

(subtract col. |

1/2 of |

(h) from col. |

column (g) |

(g)) |

|

|

Check boxes where applicable

|

(j) |

(k) |

(l) |

(m) |

|

Reserved |

Charitable |

Deductible |

2652(a)(3) |

||

for future |

gift |

gift to |

election |

||

use |

|

spouse |

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gifts made by

Total of Part 1. Add amounts from Part 1, column (i) . . . . . . . . . . . . . . . . . . . . . . . . . . .

(If more space is needed, attach additional statements.)

Form 709 (2024)

Form 709 (2024) |

Page 4 |

SCHEDULE A Computation of Taxable Gifts (Including transfers in trust) (see instructions) (continued)

Part

(a)

Item

number

(b)

Donee’s name and address

(c)

Relationship

to donor (if

any)

(d)

Description of gift

(e) |

(f) |

(g) |

(h) |

Donor’s adjusted |

Date of gift |

Value at date of |

For split gifts, |

basis of gift |

|

gift |

enter 1/2 of |

|

|

|

column (g) |

|

|

|

|

(i) |

Check boxes |

|

Net transfer |

where applicable |

|

(subtract col. (h) |

|

|

(j) |

||

from col. (g)) |

||

|

2632(b) |

|

|

election out |

|

|

|

Gifts made by

Total of Part 2. Add amounts from Part 2, column (i) |

|

(If more space is needed, attach additional statements.) |

Form 709 (2024) |

Form 709 (2024) |

Page 5 |

SCHEDULE A Computation of Taxable Gifts (Including transfers in trust) (see instructions) (continued)

Part

(a)

Item

number

(b)

Donee’s name and address

(c)

Relationship

to donor (if

any)

(d)

Description of gift

(e)

Donor’s

adjusted basis

of gift

(f) |

(g) |

(h) |

(i) |

Date of gift |

Value at |

For split |

Net transfer |

|

date of gift |

gifts, enter |

(subtract col. |

|

|

1/2 of |

(h) from col. |

|

|

column (g) |

(g)) |

|

|

|

|

Check boxes where applicable

|

(j) |

(k) |

|

(l) |

(m) |

(n) |

||||||

Reserved |

Charitable |

Deductible |

2652(a)(3) |

2632(c) |

||||||||

for future |

gift |

gift to |

election |

election |

||||||||

use |

|

|

|

spouse |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gifts made by

Total of Part 3. Add amounts from Part 3, column (i) . . . . . . . . . . . . . . . . . . . . . . . .

(If more space is needed, attach additional statements.)

Form 709 (2024)

Form 709 (2024) |

Page 6 |

SCHEDULE A Computation of Taxable Gifts (Including transfers in trust) (see instructions) (continued)

Part

1 |

Total value of gifts of donor. Add totals from column (i) of Parts 1, 2, and 3 |

2 |

Total annual exclusions for gifts listed on line 1 (see instructions) |

3Total included amount of gifts. Subtract line 2 from line 1 . . . . . . . . . . . . . . . . . . . . . . . . .

Deductions (see instructions)

4Gifts of interests to spouse for which a marital deduction will be claimed. Enter the total value of items on Parts 1 and 3 of Schedule A for which the box in column (l) is checked . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

5 |

Exclusions attributable to gifts on line 4 |

6 |

Marital deduction. Subtract line 5 from line 4 |

7Charitable deduction. Enter the total value of items on Parts 1 and 3 of Schedule A for which the box in column (k) is checked, less

|

exclusions |

8 |

Total deductions. Add lines 6 and 7 |

9 |

Subtract line 8 from line 3 |

10 |

|

11 |

Taxable gifts. Add lines 9 and 10. Enter here and on page 1, Part |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

4

5

6

7

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

1

2

3

8

9

10

11

Qualified Terminable Interest Property (QTIP) Marital Deduction (See instructions for Schedule A, Part 4, line 4.)

If a trust (or other property) meets the requirements of qualified terminable interest property under section 2523(f), and: a. The trust (or other property) is listed on Schedule A; and

b. The value of the trust (or other property) is entered in whole or in part as a deduction on Schedule A, Part 4, line 4, then the donor shall be deemed to have made an election to have such trust (or other property) treated as qualified terminable interest property under section 2523(f).

If less than the entire value of the trust (or other property) that the donor has included in Parts 1 and 3 of Schedule A is entered as a deduction on line 4, the donor shall be considered to have made an election only as to a fraction of the trust (or other property). The numerator of this fraction is equal to the amount of the trust (or other property) deducted on Schedule A, Part 4, line 6. The denominator is equal to the total value of the trust (or other property) listed in Parts 1 and 3 of Schedule A.

If you make the QTIP election, the terminable interest property involved will be included in your spouse’s gross estate upon your spouse’s death (section 2044). See instructions for line 4 of Schedule A. If your spouse disposes (by gift or otherwise) of all or part of the qualifying life income interest, your spouse will be considered to have made a transfer of the entire property that is subject to the gift tax. See Transfer of Certain Life Estates Received From Spouse in the instructions.

12Election Out of QTIP Treatment of Annuities

Check here if you elect under section 2523(f)(6) not to treat as qualified terminable interest property any joint and survivor annuities that are reported on Schedule A and would otherwise be treated as qualified terminable interest property under section 2523(f). See instructions. Enter the item numbers from Schedule A for the annuities for which you are making this election.

Form 709 (2024)

Form 709 (2024) |

Page 7 |

SCHEDULE B Gifts From Prior Periods

If you answered “Yes” on line 18a of page 1, Part I, see the instructions for completing Schedule B. If you answered “No,” skip to Part II, Tax Computation on page 1 (or Schedule C or D, if applicable). Complete Schedule A before beginning Schedule B. See instructions for recalculation of the column (c) amounts. Attach calculations.

(a)

Calendar year or calendar quarter (see instructions)

(b)

Internal Revenue office

where prior return was filed

(c)

Amount of applicable credit (unified credit) against gift tax for periods after December 31, 1976

(d)

Amount of specific exemption for prior periods ending before January 1, 1977

(e)

Amount of

taxable gifts

1 |

Totals for prior periods |

|

1 |

|

2 |

Amount, if any, by which total specific exemption, line 1, column (d), is more than $30,000 . . . |

. . . . . . . . . . . . . . . . |

2 |

|

3Total amount of taxable gifts for prior periods. Add amount on line 1, column (e), and amount, if any, on line 2. Enter here and on page 1, Part

Computation, line 2 |

3 |

(If more space is needed, attach additional statements.) |

Form 709 (2024) |

Form 709 (2024) |

Page 8 |

SCHEDULE C Deceased Spousal Unused Exclusion (DSUE) Amount and Restored Exclusion

Provide the following information to determine the DSUE amount and applicable credit received from prior spouses. Complete Schedule A before beginning Schedule C.

(a) |

|

(b) |

|

(c) |

(d) |

(e) |

(f) |

|

Name of deceased spouse |

|

Date of death |

Portability election made? |

If “Yes,” DSUE |

DSUE amount applied by |

Date of gift(s) (enter as |

||

(dates of death after December 31, 2010, only) |

|

|

|

|

|

amount received |

donor to lifetime gifts (list |

mm/dd/yy for Part 1 and |

|

|

|

|

|

|

from spouse |

current |

as yyyy for Part 2) |

|

|

|

Yes |

|

No |

|

and prior gifts) |

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

Part |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Part |

|

|

|

|

|

|

|

|

TOTAL (for all DSUE amounts applied from column (e) for Part 1 and Part 2. Enter here and on line 2 below) |

|

|

|

1 |

Donor’s basic exclusion amount (see instructions) |

1 |

|

2 |

Total from column (e), Parts 1 and 2 |

2 |

|

3 |

Restored Exclusion Amount (see instructions) |

3 |

|

4 |

Add lines 1, 2, and 3 |

4 |

|

5 |

Applicable credit on amount on line 4 (see Table for Computing Gift Tax in the instructions). Enter here and on line 7, Part |

5 |

|

(If more space is needed, attach additional statements.) |

|

Form 709 (2024) |

|

Form 709 (2024) |

Page 9 |

SCHEDULE D Computation of

Note: Inter vivos direct skips that are completely excluded by the GST exemption must still be fully reported (including value and exemptions claimed) on Schedule D.

Part

(a) |

(b) |

(c) |

(d) |

(e) |

Item number (from |

Description |

Value (from Schedule A, Part 2, |

Nontaxable portion of transfer |

Net transfer (subtract |

Schedule A, Part 2, col. (a), |

(only for ETIP transfers) |

col. (i), or close of ETIP |

|

col. (d) from col. (c)) |

then ETIP transfers, if any) |

|

described in col. (b)) |

|

|

1

Gifts made by spouse (for gift splitting only)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(If more space is needed, attach additional statements.) |

|

|

Form 709 (2024) |

|

Form 709 (2024) |

Page 10 |

||

SCHEDULE D |

Computation of |

|

|

Part |

|

||

Complete items |

|

||

1 |

Maximum allowable exemption (see instructions) |

1 |

|

2 |

Total exemption used for periods before filing this return |

2 |

|

3 |

Exemption available for this return. Subtract line 2 from line 1 |

3 |

|

4 |

Exemption claimed on this return from Part 3, column (c), total below |

4 |

|

5Automatic allocation of exemption to transfers reported on Schedule A, Part 3. To opt out of the automatic allocation rules, you must attach an “Election Out”

|

statement. See instructions |

5 |

6 |

Exemption allocated to transfers not shown on line 4 or line 5 above. You must attach a “Notice of Allocation.” See instructions |

6 |

7 |

Add lines 4, 5, and 6 |

7 |

8 |

Exemption available for future transfers. Subtract line 7 from line 3 |

8 |

Part

(a) |

(b) |

(c) |

(d) |

(e) |

(f) |

(g) |

Item number |

Net transfer |

GST exemption allocated |

Divide col. (c) |

Inclusion ratio |

Applicable rate |

|

(from Schedule D, |

(from Schedule D, |

|

by col. (b) |

(subtract col. (d) |

(multiply col. (e) |

transfer tax |

Part 1) |

Part 1, col. (e)) |

|

|

from 1.000) |

by 40% (0.40)) |

(multiply col. (b) |

|

|

|

|

|

|

by col. (f)) |

|

|

|

|

|

|

|

1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gifts made by spouse (for gift splitting only)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total exemption claimed. Enter here and on Part |

|

|

|

|

|

|

2, line 4, above. May not exceed Part 2, line 3, |

|

Total |

|

|||

above |

|

10; and on page 1, Part |

|

|||

|

|

|

|

|

|

|

(If more space is needed, attach additional statements.) |

|

|

|

Form 709 (2024) |

||

| Fact Name | Details |

|---|---|

| Purpose | The IRS Form 709 is used to report gifts that exceed the annual exclusion limit and to allocate the lifetime gift tax exemption. |

| Filing Requirement | Individuals must file Form 709 if they give gifts totaling more than $17,000 (as of 2023) to any one person in a calendar year. |

| Due Date | Form 709 is due on April 15th of the year following the gift, unless an extension is filed. |

| Lifetime Exemption | The lifetime gift tax exemption is $12.92 million (as of 2023), allowing individuals to give gifts without incurring tax until they exceed this amount. |

| State-Specific Forms | Some states have their own gift tax forms. For example, California does not have a gift tax, while New York requires its own form under the New York Estate Tax Law. |

| Joint Gifts | Married couples can combine their annual exclusions, allowing them to give up to $34,000 to one person without triggering a gift tax. |

| Educational Expenses | Payments made directly to educational institutions for someone else's tuition do not count as taxable gifts and do not require Form 709. |

| Medical Expenses | Similar to educational expenses, payments made directly to medical providers for someone else's medical expenses are not considered gifts. |

| Penalties | Failure to file Form 709 when required can result in penalties, including fines and interest on unpaid taxes. |

Filling out the IRS Form 709 can seem daunting, but with a clear plan, it becomes manageable. After completing the form, you'll submit it to the IRS, which will help them track any gifts you've made that may affect your tax obligations. Here’s how to fill it out step by step.

IRS Form 709 is the United States Gift (and Generation-Skipping Transfer) Tax Return. It is used to report gifts made during the year that exceed the annual exclusion amount, which is set by the IRS. This form is essential for individuals who give substantial gifts to ensure they comply with federal tax regulations.

Anyone who makes gifts that exceed the annual exclusion limit must file Form 709. In 2023, the annual exclusion amount is $17,000 per recipient. If you give more than this amount to any one person in a calendar year, you must report it on this form. Additionally, if you make gifts to multiple recipients that collectively exceed the exclusion amount, you will also need to file.

Form 709 covers a variety of gifts, including:

Essentially, any gift that exceeds the annual exclusion limit must be reported.

The deadline for filing Form 709 is typically April 15 of the year following the year in which you made the gifts. If you need additional time, you can file for an extension, which will give you until October 15. However, it's important to note that an extension to file does not extend the time to pay any taxes owed.

Yes, there are several exemptions and deductions that can apply when filing Form 709. For instance, gifts made to spouses who are U.S. citizens are generally exempt from gift tax. Additionally, payments made directly to educational or medical institutions on behalf of someone else do not count as taxable gifts. Always check the latest IRS guidelines for any updates on exemptions.

Failing to file Form 709 when required can lead to penalties and interest on any unpaid taxes. The IRS may impose a failure-to-file penalty, which can add up quickly. It's crucial to stay compliant to avoid these financial repercussions.

As of now, Form 709 cannot be filed electronically. You must complete the form and mail it to the IRS. Be sure to keep copies of all documents for your records.

You can find IRS Form 709 on the official IRS website. The form is available for download, along with instructions that can help you complete it accurately. Always use the most current version to ensure compliance with tax laws.

Filling out the IRS Form 709, which is used for reporting gifts and generation-skipping transfers, can be a daunting task for many individuals. One common mistake people make is failing to report all taxable gifts. It’s essential to remember that not just large gifts need to be reported; even gifts that exceed the annual exclusion amount should be included. Omitting any gifts can lead to penalties or complications in future tax filings.

Another frequent error is miscalculating the value of the gifts. The IRS requires that gifts be reported at their fair market value at the time of the transfer. People sometimes underestimate or overestimate this value, leading to inaccuracies on the form. It’s crucial to have a clear understanding of how to determine fair market value, as this will affect the overall tax implications.

Many filers also neglect to consider the implications of joint gifts. If two individuals give a gift together, they may be eligible for a combined annual exclusion. However, if this is not properly documented on the form, it can result in confusion and potential tax liabilities. Ensuring that both parties are accounted for correctly is vital to avoiding issues with the IRS.

Another mistake that can occur is not filing the form on time. The IRS has specific deadlines for filing Form 709, and missing these deadlines can lead to penalties. People often forget that the form is due on April 15 of the year following the gift, unless an extension is filed. Keeping track of these important dates is essential for compliance.

Lastly, many individuals fail to seek professional advice when needed. Tax laws can be complex and ever-changing. Relying solely on personal knowledge or online resources may lead to mistakes. Consulting with a tax professional can provide clarity and ensure that the form is filled out accurately, minimizing the risk of errors and potential audits.

The IRS Form 709, also known as the United States Gift (and Generation-Skipping Transfer) Tax Return, is an important document for individuals who make significant gifts during the tax year. Several other forms and documents often accompany Form 709 to ensure proper reporting and compliance with tax laws. Below is a list of these related documents.

Understanding these forms and documents is essential for anyone involved in significant gifting or estate planning. Proper preparation and submission can help avoid potential issues with the IRS and ensure compliance with tax obligations.

The IRS Form 709, also known as the United States Gift (and Generation-Skipping Transfer) Tax Return, is a key document for reporting gifts made during the tax year. It shares similarities with several other tax-related forms. Here are five documents that are comparable to Form 709:

When filling out the IRS 709 form, it’s essential to follow specific guidelines to ensure accuracy and compliance. Here’s a list of things you should and shouldn’t do:

By following these guidelines, you can help ensure that your IRS 709 form is filled out correctly and submitted on time.

The IRS Form 709, also known as the United States Gift (and Generation-Skipping Transfer) Tax Return, is often misunderstood. Here are nine common misconceptions about this form, clarified for better understanding.

This is not true. While high-value gifts are more likely to trigger the need to file, anyone who gives gifts exceeding the annual exclusion amount must file the form, regardless of their overall wealth.

Filing the form does not automatically mean you owe taxes. The form is used to report gifts, and you only pay tax if your gifts exceed the lifetime exemption limit.

Gifts of any kind, including property, stocks, and even services, can necessitate filing. The form covers a wide range of gifts, not just monetary ones.

This is misleading. Form 709 can report gifts made over multiple years, and it allows you to apply your annual exclusion to each gift in the year it was given.

While it may seem complex, gift splitting allows married couples to combine their annual exclusions, effectively doubling the amount they can give without tax implications.

Form 709 must be filed by the tax return deadline, typically April 15 of the following year. Missing this deadline can result in penalties.

This is incorrect. If you discover an error after filing, you can amend the form. Corrections can be made to ensure accurate reporting.

This form also applies to gifts made to trusts and charities. Gifts to these entities can also trigger reporting requirements.

For those who exceed the annual exclusion amount, filing is mandatory. Failing to file can lead to penalties and complications in future tax matters.

Understanding these misconceptions can help individuals navigate their gifting strategies more effectively and comply with tax regulations.

The IRS Form 709, also known as the United States Gift (and Generation-Skipping Transfer) Tax Return, is an important document for individuals who make gifts exceeding certain thresholds. Understanding how to fill out and use this form can help ensure compliance with tax regulations. Here are some key takeaways:

By keeping these takeaways in mind, individuals can navigate the process of filling out and using the IRS Form 709 more effectively.