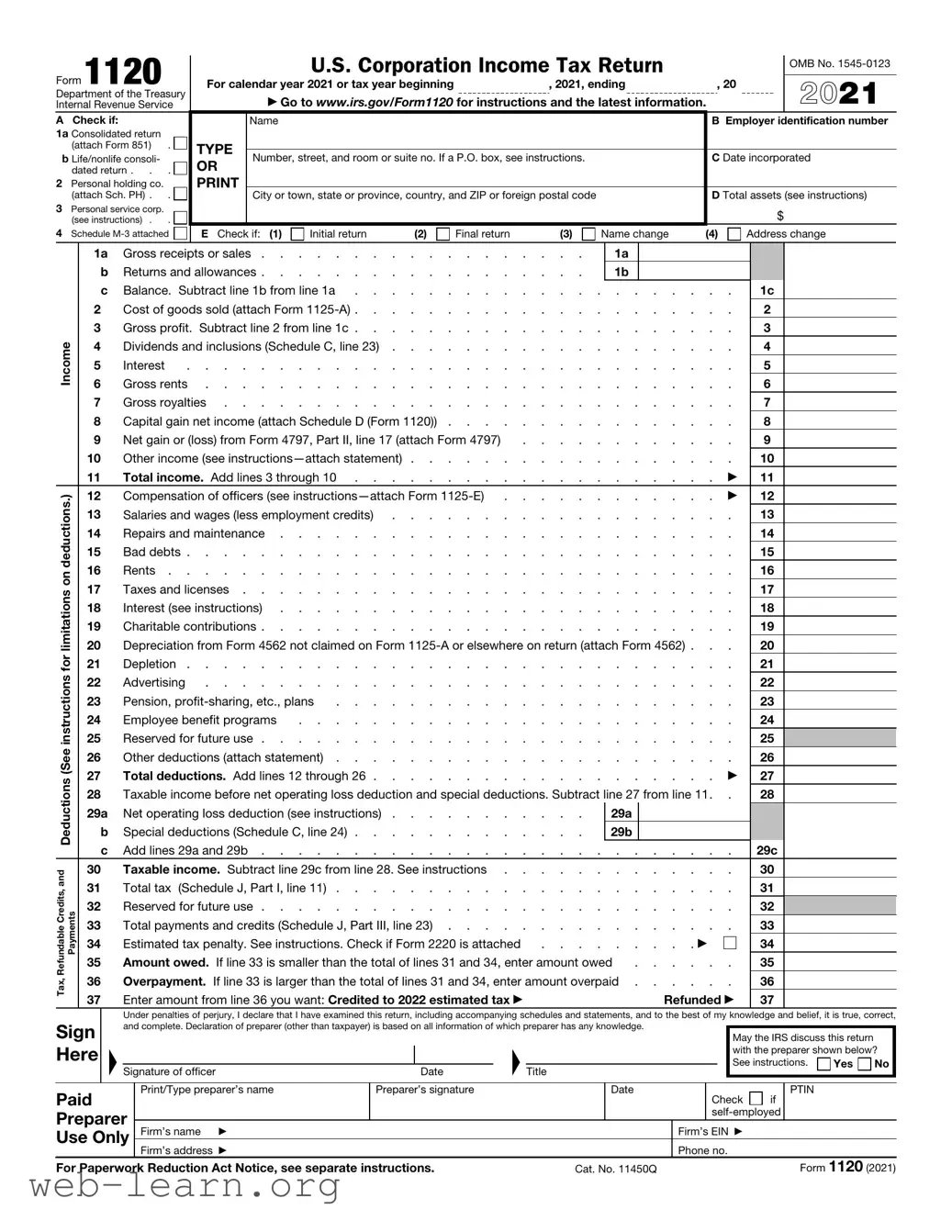

The IRS Form 1120 is a crucial component for corporations operating within the United States, serving as the official vehicle for reporting income, gains, losses, deductions, and credits, as well as calculating tax liability. Corporations submit this form to detail their financial performance and tax obligations for a given tax year. Beyond simply reporting income, the 1120 form requires various supporting schedules that delve into the specifics of company operations, including details about assets, liabilities, and shareholders. A significant aspect of this form is its role in facilitating compliance with federal tax requirements, and understanding it can be essential for ensuring fiscal responsibility. Additionally, proper completion can help corporations take advantage of deductions and credits that may significantly lower their tax burden. It is vital for business owners and financial managers to be aware of the deadlines associated with filing, typically set for the 15th day of the fourth month following the end of the corporation’s tax year, and the repercussions of failing to file accurately and on time can be severe. Overall, mastering the nuances of Form 1120 ensures that corporations not only comply with IRS regulations but also optimize their financial standing.

| Fact Name | Description |

|---|---|

| Form Purpose | The IRS Form 1120 is used by corporations to report income, gains, losses, deductions, and credits to the federal government. |

| Filing Frequency | This form must be filed annually, typically by the 15th day of the fourth month after the end of the corporation's tax year. |

| Corporate Structure | Form 1120 is primarily for C corporations. S corporations use Form 1120-S instead. |

| Tax Rate | The corporate tax rate is a flat 21% on taxable income, as set by the Tax Cuts and Jobs Act of 2017. |

| Deductions | Corporations can deduct business expenses, including cost of goods sold, salaries, and operational costs, to lower taxable income. |

| State-Specific Forms | Many states require separate forms for corporate taxes. For example, New York requires Form CT-3, governed by New York Tax Law. |

| Extensions | If additional time is needed, corporations can file Form 7004 to request a six-month extension for filing. |

| Estimated Payments | Corporations must make estimated tax payments if they expect to owe $500 or more in tax for the year. |

| Filing Methods | Form 1120 can be filed electronically or by mail. Electronic filing is encouraged for faster processing. |

After gathering the necessary information, you're ready to fill out the IRS Form 1120. This process involves various sections requiring specific details about your business. It is essential to ensure accuracy and completeness to avoid complications or potential penalties from the IRS.

What is IRS Form 1120?

IRS Form 1120 is used by corporations to report their income, gains, losses, deductions, and credits. Essentially, it's the corporate income tax return. Corporations must file this form annually to the Internal Revenue Service (IRS) to detail their financial activities during the tax year. This includes both regular C corporations and certain other types of corporations, like those that have elected to be treated as such for tax purposes.

Who must file IRS Form 1120?

Any corporation that is organized in the U.S. is required to file Form 1120. This includes corporations that have been formed under U.S. state laws and even foreign corporations doing business in the U.S. However, some corporations may qualify to file different forms, such as S corporations, which instead use Form 1120S.

When is the filing deadline for Form 1120?

The deadline for filing Form 1120 is generally the 15th day of the fourth month after the end of the corporation’s tax year. For corporations operating on a calendar year basis, this means the due date falls on April 15. If the due date falls on a weekend or holiday, the deadline extends to the next business day. Extensions are available, allowing corporations additional time to file, but they must still pay any taxes owed by the original deadline to avoid penalties and interest.

What are the consequences of not filing Form 1120?

If a corporation fails to file Form 1120, it may face significant penalties. The IRS can impose a penalty for each month the return is late, calculated based on the number of shareholders. Additionally, any taxes due will accrue interest, and prolonged failure to file can lead to further complications, including legal issues. Staying compliant is crucial for avoiding these potential problems.

How can I file Form 1120?

Filing Form 1120 can be done electronically or via mail. Many corporations opt to use tax software or hire a tax professional to navigate the process. This choice can simplify calculations and ensure accuracy. If you choose to file by mail, send your completed form to the address specified in the instructions, depending on your corporation's location and whether you are making a payment.

Filling out the IRS 1120 form can be a complex process, and mistakes are common. One frequent error occurs in the reporting of income. Taxpayers sometimes overlook or incorrectly report certain forms of income, such as taxable interest or dividends. It's essential to carefully review all sources of income to ensure accuracy. Failure to report income correctly can lead to penalties and additional interest owed.

Another common mistake involves deductions. Corporations can take various deductions, but people sometimes either miss out on available deductions or incorrectly calculate them. This can happen due to a lack of clarity regarding which expenses qualify. Consulting IRS guidelines may help clarify which expenses can be deducted, ensuring that all eligible deductions are claimed.

Some individuals struggle with the proper classification of expenses. Misclassifying expenses can lead to discrepancies in the financial statements of a corporation. For instance, a personal expense claimed as a business expense can raise red flags during an audit. Keeping personal and business finances separate is crucial to avoid these complications.

Another mistake involves the accuracy of the corporate tax rate applied. Tax rates can change, and taxpayers might inadvertently use an outdated rate. Corporations can be subject to different rates based on their size and type. Always verify the current tax rates to ensure compliance and avoid over- or underpayment of taxes.

Finally, many taxpayers fail to complete the form on time. Timeliness is essential to avoid penalties. Filing for an extension is an option, but it still requires an estimate of taxes owed. Even with an extension, it’s best to adhere to deadlines to maintain compliance and avoid unnecessary financial burdens.

The IRS Form 1120 is essential for domestic corporations to report their income, gains, losses, deductions, and credits. However, there are several other documents often submitted alongside it to provide a complete picture of a corporation's financial situation. Here’s a list of five forms commonly associated with IRS Form 1120:

These documents enhance the information provided in Form 1120, offering clarity on the corporation's overall financial health and tax obligations. Be sure to gather all necessary forms to ensure accurate filing and compliance with tax laws.

The IRS Form 1120 is used by corporations to report their income, deductions, and credits. Several other forms serve similar purposes for different types of entities or situations. Below is a list of documents that share similarities with Form 1120:

Filling out the IRS 1120 form can seem daunting, but understanding what to do—and what to avoid—can make the process smoother. Below are some key points to keep in mind as you prepare your submission.

By adhering to these guidelines, you can navigate the intricacies of the IRS 1120 form with greater ease and confidence.

The IRS Form 1120 is an essential document for corporations in the United States, but various misconceptions surround it. Here are seven common misunderstandings that can lead to confusion.

Understanding these misconceptions is crucial for ensuring compliance and optimizing business finances. Properly addressing these points can help corporations navigate the complexities of tax obligations effectively.

Here are key takeaways for filling out and using the IRS 1120 form:

What Is a Test Requisition - Be aware of the laboratory's hours for specimen drop-off and collection.

Ono Hawaiian Bbq Careers - Understand that employment offers are contingent on verification of identity.