The Indiana Promissory Note form serves as a critical tool in financial transactions, providing a written agreement between a borrower and a lender. This document outlines the borrower's promise to repay a specific amount of money, along with any applicable interest, within a designated timeframe. Key components of the form include the names and addresses of both parties, the principal amount borrowed, the interest rate, and the repayment schedule. Additionally, it may specify terms regarding late payments, default, and remedies available to the lender in case of non-compliance. The form can be tailored to meet the specific needs of the parties involved, ensuring clarity and mutual understanding. By utilizing this form, individuals and businesses can establish a legally binding commitment that helps protect their financial interests and facilitates smoother transactions.

Indiana Promissory Note Template

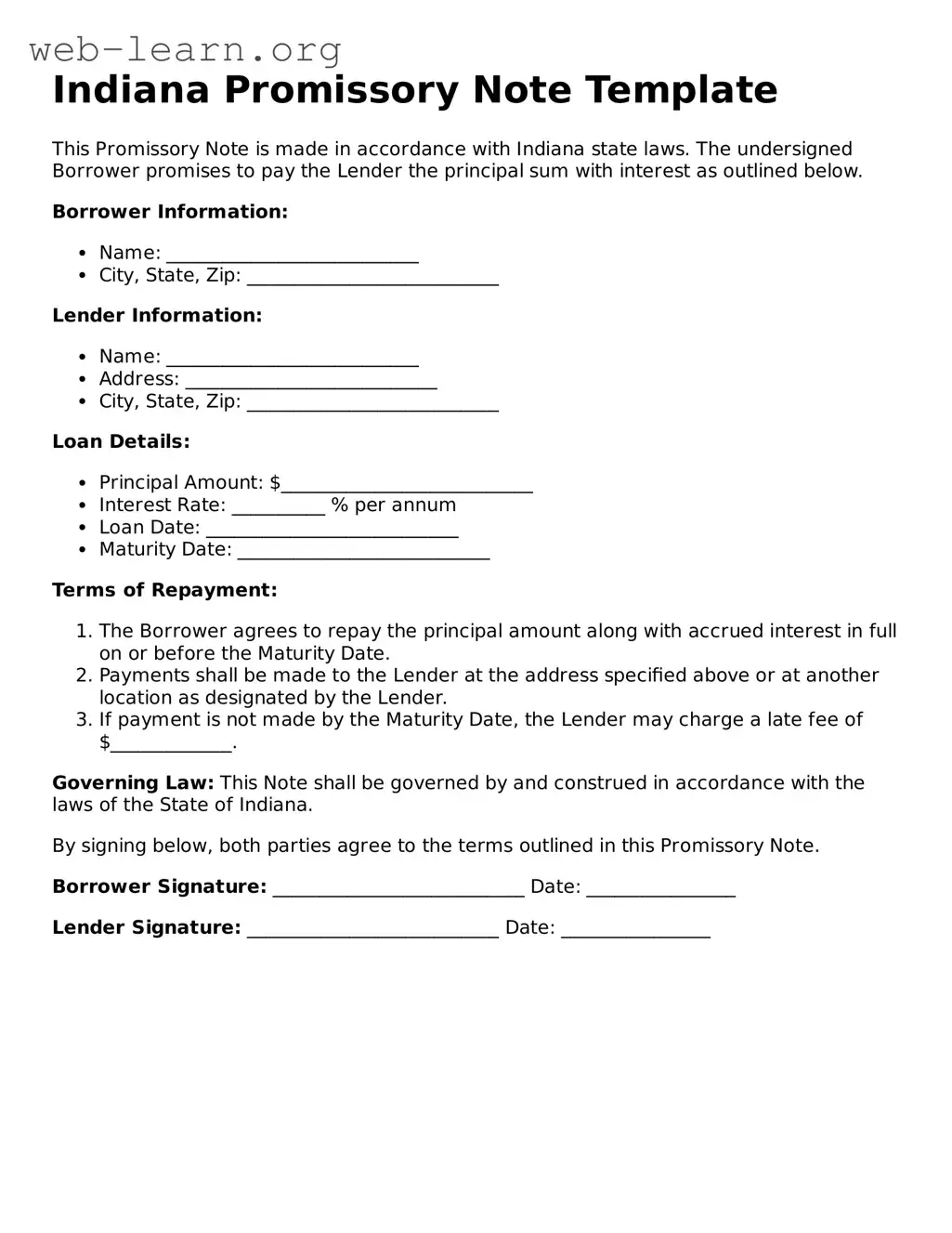

This Promissory Note is made in accordance with Indiana state laws. The undersigned Borrower promises to pay the Lender the principal sum with interest as outlined below.

Borrower Information:

Lender Information:

Loan Details:

Terms of Repayment:

Governing Law: This Note shall be governed by and construed in accordance with the laws of the State of Indiana.

By signing below, both parties agree to the terms outlined in this Promissory Note.

Borrower Signature: ___________________________ Date: ________________

Lender Signature: ___________________________ Date: ________________

| Fact Name | Details |

|---|---|

| Definition | An Indiana Promissory Note is a written promise to pay a specified amount of money to a designated person or entity at a predetermined time. |

| Governing Law | The Indiana Uniform Commercial Code (UCC) governs promissory notes in Indiana, specifically under Article 3, which deals with negotiable instruments. |

| Requirements | To be valid, a promissory note must include the date, the principal amount, the interest rate (if applicable), the payee's name, and the borrower's signature. |

| Types | Indiana recognizes different types of promissory notes, including secured and unsecured notes, each with its own implications for repayment and collateral. |

| Enforceability | If properly executed, a promissory note is legally enforceable in Indiana courts, allowing the payee to seek repayment through legal means if necessary. |

After you have gathered all necessary information, you are ready to fill out the Indiana Promissory Note form. This document will outline the terms of the loan and ensure that both parties understand their obligations. Carefully follow the steps below to complete the form accurately.

What is an Indiana Promissory Note?

An Indiana Promissory Note is a written promise to pay a specific amount of money to a designated person or entity at a specified time or on demand. This document outlines the terms of the loan, including the amount borrowed, interest rate, repayment schedule, and any penalties for late payments. It serves as a legal record of the agreement between the borrower and the lender.

Who can use a Promissory Note in Indiana?

Any individual or business in Indiana can use a Promissory Note. It is commonly utilized by individuals borrowing money from friends or family, as well as by businesses seeking loans from banks or private lenders. The note is beneficial for both parties, as it clarifies the terms of the loan and provides a formal record of the agreement.

What should be included in an Indiana Promissory Note?

An effective Promissory Note should include the following key elements:

Including these details helps prevent misunderstandings and ensures both parties are clear on their obligations.

Is a Promissory Note legally binding in Indiana?

Yes, a Promissory Note is legally binding in Indiana as long as it meets the necessary requirements. It must be in writing, signed by the borrower, and include all essential terms. If the borrower fails to repay the loan as agreed, the lender can take legal action to recover the owed amount. However, it is advisable to consult with a legal professional for specific situations to ensure that the document is enforceable.

Filling out a promissory note can seem straightforward, but many people make common mistakes that can lead to confusion or legal issues down the line. One frequent error is failing to include all necessary parties. A promissory note should clearly identify both the borrower and the lender. Omitting one party's name can create ambiguity about who is responsible for repayment.

Another common mistake is neglecting to specify the loan amount. It may seem obvious, but without a clear figure, the note can be open to interpretation. This lack of clarity can lead to disputes later on regarding how much is actually owed.

People often overlook the importance of detailing the interest rate. If the note does not specify whether the loan is interest-free or includes a specific rate, it can create misunderstandings. It’s essential to state the interest rate explicitly to avoid confusion in the future.

Additionally, many individuals forget to include the repayment terms. This includes when payments are due, how often they should be made, and the method of payment. Without this information, it can be difficult for both parties to understand their obligations.

Another mistake occurs when individuals fail to date the promissory note. A missing date can complicate matters, especially if there are disputes about when the loan was initiated or when payments were supposed to begin. The date provides a clear timeline for the agreement.

Some people make the error of not having the document signed by both parties. A promissory note is only as strong as the agreements made within it. Without signatures, the note may not be enforceable, leaving one party vulnerable.

In addition, individuals sometimes forget to include a clause about default. This clause outlines what happens if the borrower fails to make payments. Including this information can protect the lender’s interests and clarify the consequences for the borrower.

Another oversight is failing to keep copies of the signed promissory note. Both parties should retain a copy for their records. Without this, it can be challenging to prove the terms of the agreement if disputes arise.

People often neglect to consult with a legal professional when drafting a promissory note. While it may seem unnecessary, having legal guidance can help ensure that the note meets all legal requirements and protects both parties involved.

Lastly, individuals may not consider the implications of state laws regarding promissory notes. Each state has its own regulations that can affect the enforceability of the document. It is crucial to understand these laws to avoid potential issues.

When dealing with financial transactions, particularly those involving loans, several important documents accompany the Indiana Promissory Note. Each of these documents serves a specific purpose and helps ensure clarity and legal protection for all parties involved. Below is a list of some commonly used forms and documents.

Understanding these documents is crucial for anyone entering into a loan agreement. Each serves to protect the interests of both the lender and the borrower, fostering a transparent and fair lending process.

When filling out the Indiana Promissory Note form, it is essential to follow certain guidelines to ensure accuracy and compliance. Here are eight important dos and don'ts to consider:

By adhering to these guidelines, individuals can help ensure that their Indiana Promissory Note is completed correctly and effectively serves its purpose.

Understanding the Indiana Promissory Note form is essential for anyone involved in lending or borrowing money. However, several misconceptions can lead to confusion. Here are six common misunderstandings:

Clearing up these misconceptions can help ensure that individuals understand their rights and responsibilities when dealing with promissory notes in Indiana.

Filling out and using the Indiana Promissory Note form can be a straightforward process, but it’s important to understand the key aspects to ensure it serves its purpose effectively. Here are some essential takeaways:

By paying attention to these key aspects, individuals can create a valid and enforceable promissory note that protects the interests of both the borrower and the lender.

Basic Promissory Note - A promissory note typically includes the names of the borrower and lender, the amount borrowed, and the date of repayment.

Online Promissory Note - The document is typically straightforward and easy to understand.

Kansas Promissory Note - It is essential to communicate any changes in financial circumstances to the lender.