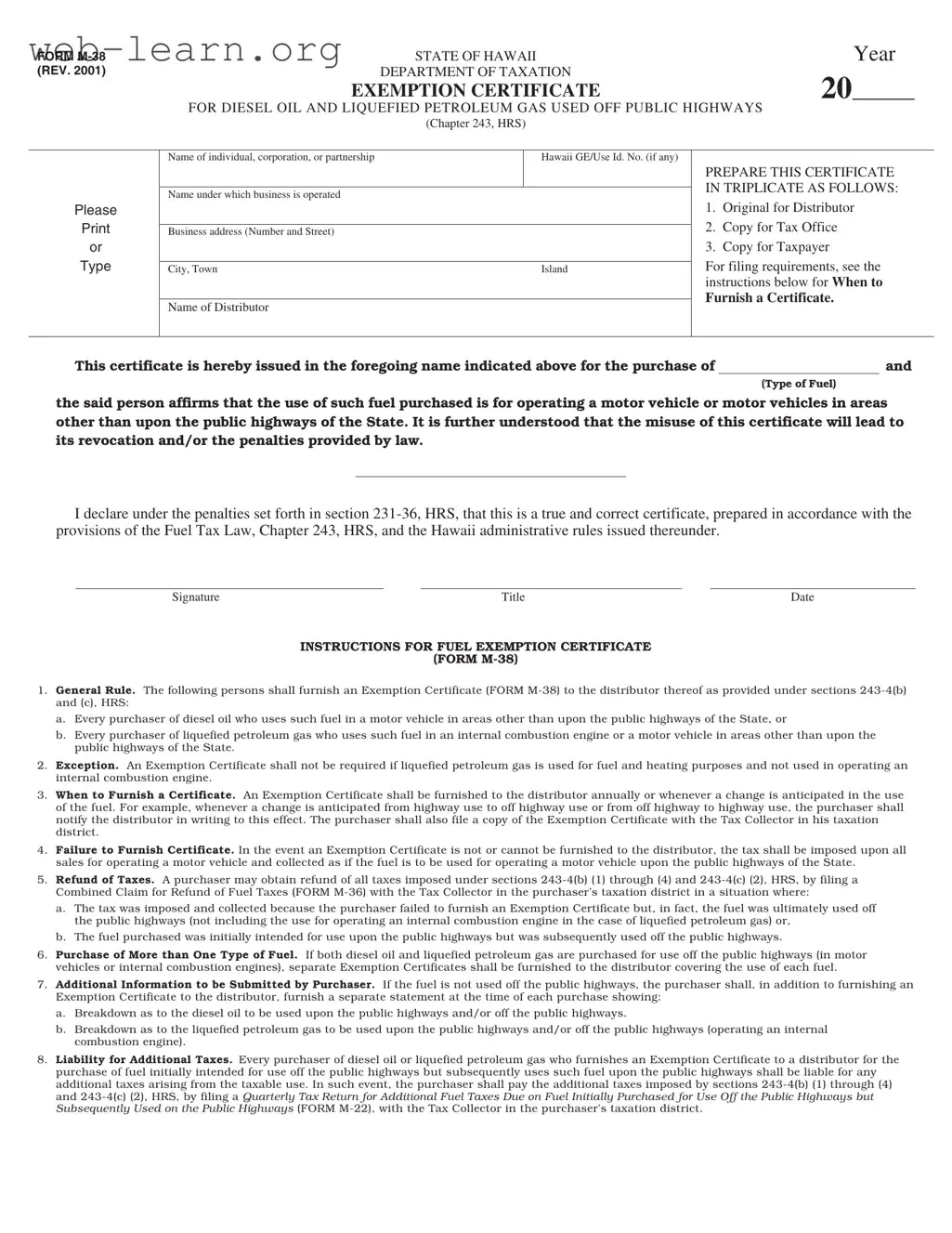

The Hawaii M 38 form serves as an essential tool for individuals and businesses that purchase diesel oil and liquefied petroleum gas (LPG) for use off public highways. This exemption certificate allows purchasers to affirm that the fuel they buy will not be used on public roads, thus avoiding certain taxes associated with highway use. To obtain this exemption, purchasers must fill out the form accurately, providing details such as the name of the individual or business, their tax identification number, and the type of fuel being purchased. The form must be prepared in triplicate, with copies designated for the distributor, the tax office, and the taxpayer. It is crucial for users to understand when to furnish this certificate; it must be provided annually or whenever there is a change in fuel use, such as switching from highway to off-highway applications. Failure to present the form can result in tax liabilities as if the fuel were used on public highways. Additionally, there are specific provisions regarding refunds for taxes imposed when an exemption certificate was not provided but the fuel was ultimately used off the highways. This highlights the importance of compliance with the form's requirements to avoid unnecessary penalties. Overall, the Hawaii M 38 form plays a vital role in regulating fuel use and ensuring that tax obligations are met appropriately.

FORM |

|

STATE OF HAWAII |

|

|

Year |

|

||

(REV. 2001) |

|

DEPARTMENT OF TAXATION |

|

20 |

|

|

|

|

|

EXEMPTION CERTIFICATE |

|

|

|

|

|||

|

FOR DIESEL OIL AND LIQUEFIED PETROLEUM GAS USED OFF PUBLIC HIGHWAYS |

|

||||||

|

|

(Chapter 243, HRS) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of individual, corporation, or partnership |

|

Hawaii GE/Use Id. No. (if any) |

|

|

|

|

|

|

|

|

|

PREPARE THIS CERTIFICATE |

|

|||

|

|

|

|

IN TRIPLICATE AS FOLLOWS: |

|

|||

|

Name under which business is operated |

|

|

|

||||

|

|

|

|

|

|

|

|

|

Please |

|

|

|

1. |

Original for Distributor |

|

||

|

|

|

2. Copy for Tax Office |

|

||||

Business address (Number and Street) |

|

|

|

|||||

or |

|

|

|

3. Copy for Taxpayer |

|

|||

Type |

|

|

|

For filing requirements, see the |

|

|||

City, Town |

|

Island |

|

|||||

|

|

|

|

instructions below for WHEN TO |

|

|||

|

|

|

|

FURNISH A CERTIFICATE. |

|

|||

|

Name of Distributor |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

This certificate is hereby issued in the foregoing name indicated above for the purchase of |

|

|

and |

|

||||

|

|

|

|

|

(Type of Fuel) |

|

||

the said person affirms that the use of such fuel purchased is for operating a motor vehicle or motor vehicles in areas other than upon the public highways of the State. It is further understood that the misuse of this certificate will lead to its revocation and/or the penalties provided by law.

I declare under the penalties set forth in section

Signature |

Title |

Date |

INSTRUCTIONS FOR FUEL EXEMPTION CERTIFICATE

(FORM

1.General Rule. The following persons shall furnish an Exemption Certificate (FORM

a.Every purchaser of diesel oil who uses such fuel in a motor vehicle in areas other than upon the public highways of the State, or

b.Every purchaser of liquefied petroleum gas who uses such fuel in an internal combustion engine or a motor vehicle in areas other than upon the public highways of the State.

2.Exception. An Exemption Certificate shall not be required if liquefied petroleum gas is used for fuel and heating purposes and not used in operating an internal combustion engine.

3.When to Furnish a Certificate. An Exemption Certificate shall be furnished to the distributor annually or whenever a change is anticipated in the use of the fuel. For example, whenever a change is anticipated from highway use to off highway use or from off highway to highway use, the purchaser shall notify the distributor in writing to this effect. The purchaser shall also file a copy of the Exemption Certificate with the Tax Collector in his taxation district.

4.Failure to Furnish Certificate. In the event an Exemption Certificate is not or cannot be furnished to the distributor, the tax shall be imposed upon all sales for operating a motor vehicle and collected as if the fuel is to be used for operating a motor vehicle upon the public highways of the State.

5.Refund of Taxes. A purchaser may obtain refund of all taxes imposed under sections

a.The tax was imposed and collected because the purchaser failed to furnish an Exemption Certificate but, in fact, the fuel was ultimately used off the public highways (not including the use for operating an internal combustion engine in the case of liquefied petroleum gas) or,

b.The fuel purchased was initially intended for use upon the public highways but was subsequently used off the public highways.

6.Purchase of More than One Type of Fuel. If both diesel oil and liquefied petroleum gas are purchased for use off the public highways (in motor vehicles or internal combustion engines), separate Exemption Certificates shall be furnished to the distributor covering the use of each fuel.

7.Additional Information to be Submitted by Purchaser. If the fuel is not used off the public highways, the purchaser shall, in addition to furnishing an Exemption Certificate to the distributor, furnish a separate statement at the time of each purchase showing:

a.Breakdown as to the diesel oil to be used upon the public highways and/or off the public highways.

b.Breakdown as to the liquefied petroleum gas to be used upon the public highways and/or off the public highways (operating an internal combustion engine).

8.Liability for Additional Taxes. Every purchaser of diesel oil or liquefied petroleum gas who furnishes an Exemption Certificate to a distributor for the purchase of fuel initially intended for use off the public highways but subsequently uses such fuel upon the public highways shall be liable for any additional taxes arising from the taxable use. In such event, the purchaser shall pay the additional taxes imposed by sections

| Fact Name | Fact Description |

|---|---|

| Form Title | Exemption Certificate for Diesel Oil and Liquefied Petroleum Gas Used Off Public Highways |

| Governing Law | Chapter 243, Hawaii Revised Statutes (HRS) |

| Purpose | This form certifies that diesel oil or liquefied petroleum gas is used in motor vehicles off public highways. |

| Filing Requirements | It must be prepared in triplicate: one for the distributor, one for the tax office, and one for the taxpayer. |

| Annual Submission | The certificate should be furnished annually or when there is a change in fuel use. |

| Refund Eligibility | Purchasers can claim refunds if taxes were paid without the certificate when fuel was used off public highways. |

| Multiple Fuels | Separate exemption certificates are required for diesel oil and liquefied petroleum gas if both are purchased. |

| Liability for Misuse | Purchasers are liable for additional taxes if fuel intended for off-highway use is used on public highways. |

| Penalties | Misuse of the certificate may result in revocation and penalties as provided by law. |

After completing the Hawaii M 38 form, it should be submitted to the appropriate distributor. It is essential to keep a copy for your records and to provide the necessary documentation to the tax office as required. Ensuring accuracy in the information provided will help avoid any potential penalties or issues with the tax authorities.

The Hawaii M-38 form serves as an Exemption Certificate for diesel oil and liquefied petroleum gas used off public highways. This form allows purchasers to affirm that the fuel will be utilized in areas other than public highways, thereby exempting them from certain taxes associated with highway use.

Any individual, corporation, or partnership purchasing diesel oil or liquefied petroleum gas for use in motor vehicles or internal combustion engines off public highways must complete this form. It is essential for those who want to avoid taxes that apply to fuel used on public roads.

The M-38 form should be furnished to the distributor annually or whenever there is a change in the intended use of the fuel. For instance, if the fuel is to be used on public highways instead of off-road, the purchaser must notify the distributor in writing and provide the updated certificate.

If the Exemption Certificate is not submitted to the distributor, taxes will be imposed on all sales as if the fuel were intended for use on public highways. This can result in unexpected costs for the purchaser.

Yes, a purchaser may obtain a refund for taxes imposed if they can demonstrate that the fuel was ultimately used off public highways, despite not providing an Exemption Certificate at the time of purchase. To claim this refund, the purchaser must file a Combined Claim for Refund of Fuel Taxes using Form M-36.

In cases where both types of fuel are purchased for off-highway use, separate M-38 forms must be completed for each fuel type. This ensures accurate tracking and compliance with tax regulations.

If the fuel is not used off public highways, the purchaser must provide a separate statement detailing the breakdown of diesel oil and liquefied petroleum gas intended for highway versus off-highway use at the time of each purchase.

Purchasers who use diesel oil or liquefied petroleum gas initially intended for off-highway use on public highways will be liable for additional taxes. They must report this usage by filing a Quarterly Tax Return for Additional Fuel Taxes Due using Form M-22 with the Tax Collector in their taxation district.

Filling out the Hawaii M-38 form can be straightforward, but many people make mistakes that can lead to complications. One common error occurs when individuals fail to provide their Hawaii GE/Use ID number. This number is essential for identifying the purchaser and ensuring proper tax processing. Without it, the form may be deemed incomplete, resulting in delays or even penalties. Always double-check that this number is included before submitting the form.

Another frequent mistake is not understanding when to furnish the exemption certificate. Some individuals mistakenly think they only need to submit the form once. However, the form must be provided annually or whenever there is a change in the use of the fuel. For instance, if you switch from using fuel on public highways to off-road use, you must notify your distributor and submit a new certificate. Ignoring this requirement can lead to unnecessary tax liabilities.

People also often overlook the need to submit separate exemption certificates when purchasing more than one type of fuel. If you buy both diesel oil and liquefied petroleum gas for off-highway use, each type of fuel requires its own certificate. Failing to do so can complicate your tax situation and may result in additional taxes being assessed.

Lastly, many purchasers do not realize the importance of keeping accurate records. When fuel is initially intended for off-highway use but is later used on public highways, individuals can be held liable for additional taxes. It’s crucial to maintain documentation that reflects how the fuel was ultimately used. This not only helps in case of an audit but also aids in filing for any refunds if applicable. Being diligent in record-keeping can save you from potential headaches down the line.

The Hawaii M-38 form serves as an Exemption Certificate for diesel oil and liquefied petroleum gas used off public highways. This document is essential for individuals and businesses looking to avoid unnecessary taxes when utilizing fuel in areas not designated as public highways. However, this form is often accompanied by other important documents that help ensure compliance with state regulations. Below is a list of related forms and documents frequently used alongside the Hawaii M-38.

Understanding the various forms associated with the Hawaii M-38 is crucial for anyone involved in the purchase and use of diesel oil and liquefied petroleum gas. By familiarizing oneself with these documents, individuals and businesses can navigate the complexities of fuel taxation and ensure compliance with state laws. This proactive approach can lead to significant savings and a smoother operational process.

The Hawaii M-38 form serves as an exemption certificate for diesel oil and liquefied petroleum gas used off public highways. It shares similarities with other documents that also address tax exemptions or certifications. Here are four documents that are similar to the Hawaii M-38 form:

When filling out the Hawaii M 38 form, it is important to follow certain guidelines to ensure accuracy and compliance. Below is a list of things you should and shouldn't do:

By adhering to these guidelines, you can help ensure that the process goes smoothly and that you remain compliant with the requirements set forth by the State of Hawaii.

Misunderstandings about the Hawaii M 38 form can lead to confusion and potential penalties. Here are nine common misconceptions:

Understanding these misconceptions can help ensure compliance and avoid unnecessary complications. Always consult with a tax professional for personalized guidance.

Filling out the Hawaii M-38 form is essential for individuals and businesses that use diesel oil or liquefied petroleum gas off public highways. Here are key takeaways to consider:

Understanding these key points can help ensure compliance with Hawaii's fuel tax regulations and avoid unnecessary penalties.