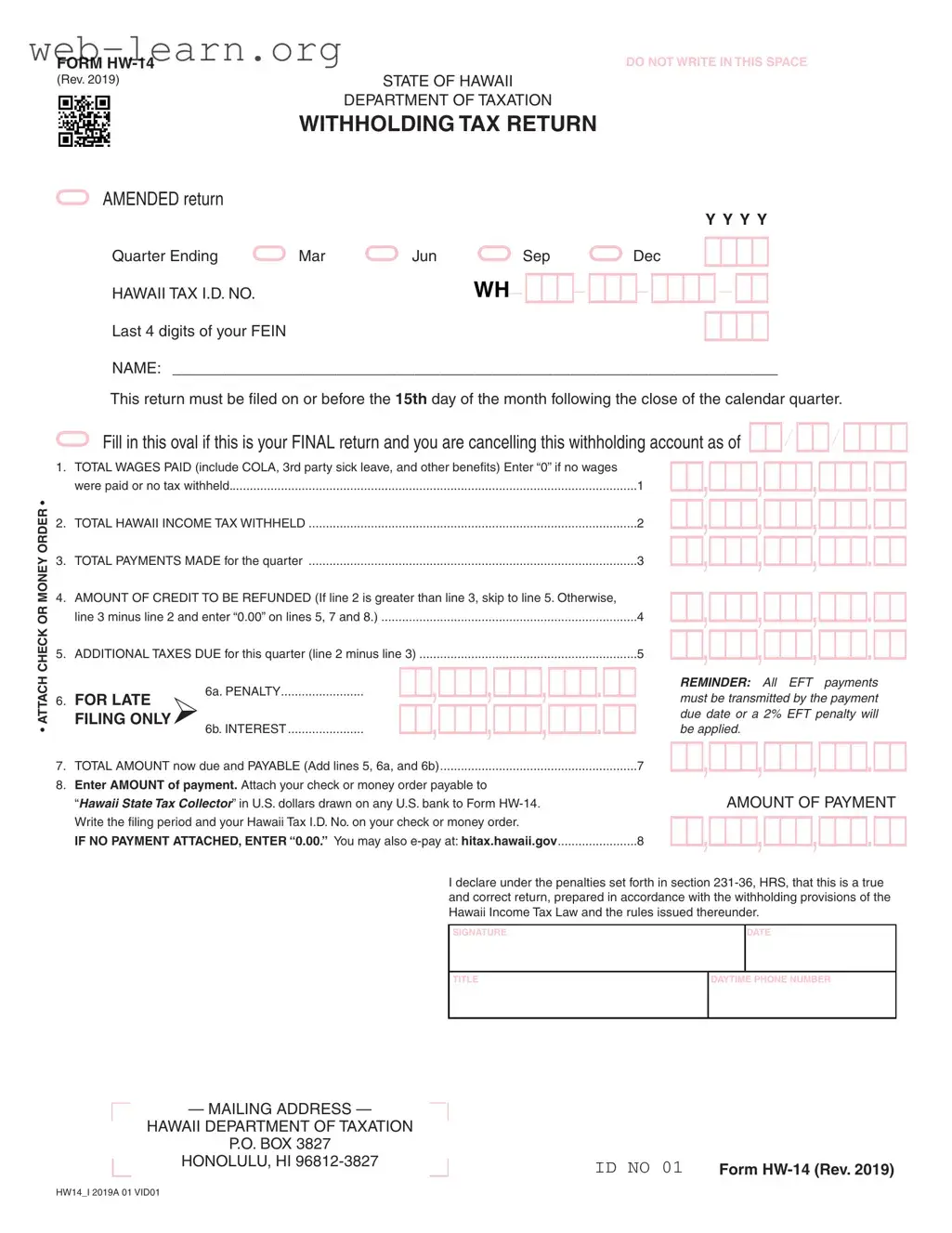

The Hawaii HW-14 form serves as a critical tool for employers and businesses operating within the state, ensuring compliance with local withholding tax obligations. Each quarter, employers must submit this form to report wages paid and the corresponding income tax withheld from employees. The form is structured to capture essential information, such as the total wages paid, the total amount of Hawaii income tax withheld, and any payments made during the quarter. Notably, it also addresses the potential for refunds or additional taxes due, depending on the calculations of tax withheld versus payments made. Employers are reminded of the importance of timely submission, as the form must be filed by the 15th day of the month following the close of the quarter. Failure to comply can result in penalties and interest charges, underscoring the need for accuracy in reporting. Furthermore, the form provides a clear avenue for final returns, allowing businesses to officially cancel their withholding accounts when necessary. Completing the HW-14 requires careful attention to detail, as it must be prepared in accordance with the Hawaii Income Tax Law and its accompanying regulations, ensuring that all information is truthful and accurate.

FORM |

|

|

|

|

(Rev. 2019) |

|

STATE OF HAWAII |

|

|

|

|

DEPARTMENT OF TAXATION |

|

|

|

WITHHOLDING TAX RETURN |

|

||

AMENDED return |

|

|

|

|

|

|

|

|

Y Y Y Y |

Quarter Ending |

Mar |

Jun |

Sep |

Dec |

HAWAII TAX I.D. NO. |

|

WH |

|

|

Last 4 digits of your FEIN |

|

|

|

|

NAME: ______________________________________________________________________

This return must be filed on or before the 15th day of the month following the close of the calendar quarter.

• ATTACH CHECK OR MONEY ORDER •

Fill in this oval if this is your FINAL return and you are cancelling this withholding account as of

1. |

TOTAL WAGES PAID (include COLA, 3rd party sick leave, and other benefits) Enter “0” if no wages |

|

|

|

were paid or no tax withheld |

1 |

|

2. |

TOTAL HAWAII INCOME TAX WITHHELD |

2 |

|

3. |

TOTAL PAYMENTS MADE for the quarter |

3 |

|

4. |

AMOUNT OF CREDIT TO BE REFUNDED (If line 2 is greater than line 3, skip to line 5. Otherwise, |

|

|

|

line 3 minus line 2 and enter “0.00” on lines 5, 7 and 8.) |

4 |

|

5. |

ADDITIONAL TAXES DUE for this quarter (line 2 minus line 3) |

5 |

|

|

|

|

REMINDER: All EFT payments |

|

|

6a. PENALTY |

|

6. |

FOR LATE |

|

must be transmitted by the payment |

|

|

|

due date or a 2% EFT penalty will |

|

FILING ONLY6b. INTEREST |

be applied. |

|

7. |

TOTAL AMOUNT now due and PAYABLE (Add lines 5, 6a, and 6b) |

7 |

|

8. |

Enter AMOUNT of payment. Attach your check or money order payable to |

|

|

|

“HAWAII STATE TAX COLLECTOR” in U.S. dollars drawn on any U.S. bank to Form |

AMOUNT OF PAYMENT |

|

|

Write the filing period and your Hawaii Tax I.D. No. on your check or money order. |

|

|

|

IF NO PAYMENT ATTACHED, ENTER “0.00.” You may also |

8 |

|

I declare under the penalties set forth in section

— MAILING ADDRESS —

HAWAII DEPARTMENT OF TAXATION

P.O. BOX 3827

HONOLULU, HI

ID NO 01 |

Form |

HW14_I 2019A 01 VID01

| Fact Name | Description |

|---|---|

| Form Purpose | The HW-14 form is used to report withholding tax for employees in Hawaii. |

| Filing Deadline | This form must be filed by the 15th day of the month following the end of each calendar quarter. |

| Final Return Option | Taxpayers can indicate if this is their final return by filling in the designated oval on the form. |

| Tax Identification | Each filer must include their Hawaii Tax I.D. number and the last four digits of their Federal Employer Identification Number (FEIN). |

| Payment Requirements | A check or money order must be attached if there is a payment due. Payments can also be made electronically. |

| Governing Law | The HW-14 form is governed by the Hawaii Income Tax Law, specifically under section 231-36, HRS. |

| Penalties for Late Filing | Filing late may result in penalties, including a 2% EFT penalty for electronic payments not submitted by the due date. |

Completing the Hawaii HW-14 form is an essential step for businesses that need to report their withholding tax. After filling out the form, it must be submitted to the Hawaii Department of Taxation by the specified deadline. Ensure that all information is accurate to avoid any potential penalties or delays.

What is the Hawaii HW-14 form?

The Hawaii HW-14 form is a withholding tax return that employers in Hawaii must file to report the income tax withheld from employees' wages. It is essential for ensuring compliance with state tax regulations.

When is the HW-14 form due?

This form must be filed on or before the 15th day of the month following the end of each calendar quarter. For example, if the quarter ends in March, the form is due by April 15th.

What information is required on the HW-14 form?

What should I do if I did not pay any wages?

If no wages were paid or no tax was withheld, you should enter “0” in the total wages paid section. It is still important to file the form even if no wages were reported.

How do I make a payment with the HW-14 form?

You can attach a check or money order made payable to “HAWAII STATE TAX COLLECTOR.” Ensure that you write the filing period and your Hawaii Tax ID No. on the payment. Alternatively, you may also make an electronic payment at hitax.hawaii.gov.

What if I need to amend my HW-14 form?

If you need to make changes after filing, you can submit an amended return using the HW-14 form. Be sure to indicate that it is an amended return by checking the appropriate box on the form.

What happens if I file late?

Filing the HW-14 form late may result in penalties and interest charges. A penalty is assessed for late filing, and interest may accrue on any unpaid taxes. It's important to file on time to avoid these additional costs.

Can I cancel my withholding account?

Yes, if you are closing your business or no longer need to withhold taxes, you can cancel your withholding account. Be sure to indicate this on the HW-14 form by filling in the designated oval for a final return.

Where do I send the HW-14 form?

The completed HW-14 form should be mailed to the Hawaii Department of Taxation at the following address:

HAWAII DEPARTMENT OF TAXATION

P.O. BOX 3827

HONOLULU, HI 96812-3827

What if I have further questions about the HW-14 form?

If you have additional questions or need assistance, you can contact the Hawaii Department of Taxation directly or consult their website for more resources and guidance.

Filling out the Hawaii HW-14 form can seem straightforward, but many people stumble over common mistakes that can lead to delays or penalties. One frequent error is forgetting to include the correct Hawaii Tax I.D. number. This number is crucial for identifying your account with the state. If it’s missing or incorrect, your return may be rejected, causing unnecessary headaches.

Another common mistake is neglecting to check the box indicating whether the return is final. If you are closing your withholding account, it’s essential to mark this clearly. Failing to do so can result in continued tax obligations and confusion about your account status.

Many filers also overlook the importance of accurate wage reporting. When entering the total wages paid, it’s vital to include all applicable amounts, such as cost-of-living adjustments and third-party sick leave. Omitting these figures can lead to underreporting, which may trigger audits or additional tax liabilities.

Similarly, errors in calculating the total Hawaii income tax withheld can create significant problems. Double-check your math to ensure that the amounts entered in line 2 are accurate. If you report a higher tax withheld than what was actually paid, it could result in complications down the line.

Another mistake is not properly calculating the amounts due. When determining the amount of credit to be refunded or additional taxes owed, it’s crucial to follow the instructions carefully. Miscalculating these figures can lead to incorrect payments or refunds, which can complicate your tax situation.

Many people also forget to attach their payment, if applicable. The form requires that you include a check or money order, or indicate “0.00” if no payment is due. Leaving this blank can delay processing and may incur penalties.

Lastly, failing to file the return on time is a common pitfall. Remember that the HW-14 must be submitted by the 15th day of the month following the close of the quarter. Late filings can incur penalties and interest, which can add up quickly. Keeping track of deadlines is essential for maintaining compliance and avoiding unnecessary costs.

The Hawaii HW-14 form is essential for employers in Hawaii who need to report withholding tax for their employees. However, several other forms and documents may accompany it to ensure compliance with state tax laws. Below is a list of these related documents, each serving a specific purpose in the tax filing process.

Understanding these forms can help employers navigate the complexities of tax compliance in Hawaii. Each document plays a vital role in ensuring accurate reporting and timely payments, ultimately contributing to a smooth tax filing experience.

The Hawaii HW-14 form is similar to several other tax-related documents. Each of these forms serves a specific purpose in the context of tax reporting and withholding. Below is a list of documents that share similarities with the HW-14 form:

When filling out the Hawaii HW-14 form, it’s important to follow certain guidelines to ensure accuracy and compliance. Here are seven things you should and shouldn't do:

Following these guidelines can help avoid delays or penalties. Take your time and ensure everything is filled out correctly.

Understanding the Hawaii HW-14 form is essential for anyone involved in withholding taxes in Hawaii. However, several misconceptions can lead to confusion. Here are seven common misconceptions about the HW-14 form, along with clarifications:

Clarifying these misconceptions can help ensure compliance with Hawaii's tax laws and prevent unnecessary penalties. Understanding the requirements of the HW-14 form is crucial for anyone responsible for withholding taxes in Hawaii.

When it comes to filing the Hawaii HW-14 form, there are several important points to keep in mind. Understanding these key takeaways can simplify the process and ensure compliance with Hawaii’s tax regulations.

By keeping these points in mind, you can navigate the HW-14 form with greater ease and ensure that your tax filings are accurate and timely.