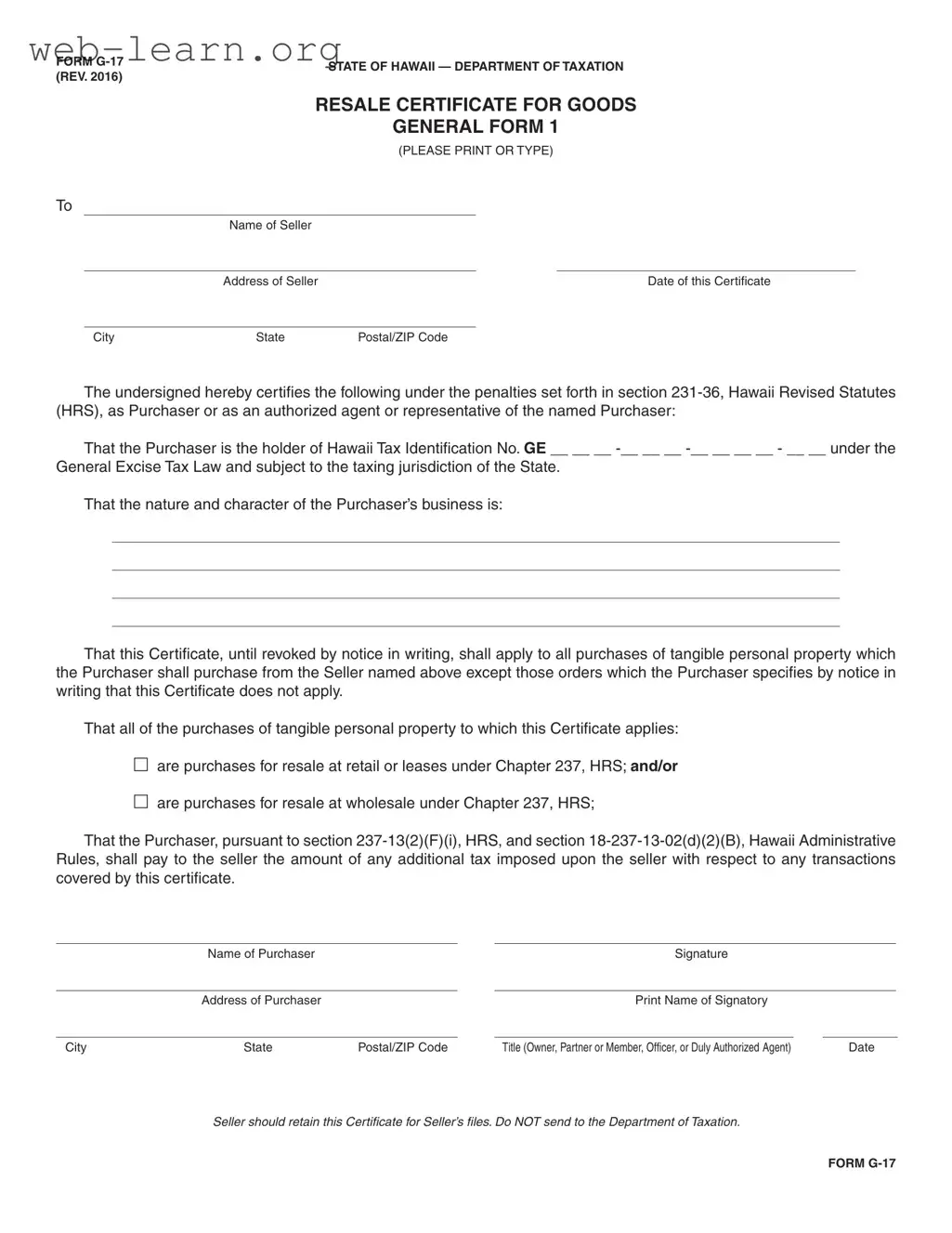

The Hawaii G 17 form serves as a crucial document for businesses engaging in the resale of tangible personal property within the state. This form, officially titled the Resale Certificate for Goods, is issued by the Hawaii Department of Taxation and is essential for ensuring compliance with the General Excise Tax Law. Designed for use by purchasers, it allows them to certify that they hold a valid Hawaii Tax Identification Number and are operating under the jurisdiction of the state’s tax laws. The form requires detailed information about the seller and the purchaser, including their addresses and the nature of the purchaser’s business. Importantly, the G 17 certifies that the purchaser intends to resell the goods rather than use them for personal consumption, which can exempt them from certain taxes at the time of purchase. This certificate remains valid until it is revoked in writing, thereby streamlining transactions between sellers and purchasers. Additionally, the purchaser acknowledges responsibility for any additional taxes that may be imposed on the seller related to these transactions. Overall, the G 17 form plays a vital role in facilitating lawful business operations while ensuring that tax obligations are met.

FORM |

STATE OF HAWAII — DEPARTMENT OF TAXATION |

|

(REV. 2016) |

||

|

RESALE CERTIFICATE FOR GOODS

GENERAL FORM 1

(PLEASE PRINT OR TYPE)

To

Name of Seller

|

Address of Seller |

|

Date of this Certificate |

|

|

|

|

City |

State |

Postal/ZIP Code |

|

The undersigned hereby certifies the following under the penalties set forth in section

That the Purchaser is the holder of Hawaii Tax Identification No. GE __ __ __

That the nature and character of the Purchaser’s business is:

That this Certificate, until revoked by notice in writing, shall apply to all purchases of tangible personal property which the Purchaser shall purchase from the Seller named above except those orders which the Purchaser specifies by notice in writing that this Certificate does not apply.

That all of the purchases of tangible personal property to which this Certificate applies:

are purchases for resale at retail or leases under Chapter 237, HRS; AND/OR

are purchases for resale at wholesale under Chapter 237, HRS;

That the Purchaser, pursuant to section

|

Name of Purchaser |

|

|

Signature |

|

|

|

|

|

|

|

|

|

|

|

|

Address of Purchaser |

|

|

Print Name of Signatory |

|

|

|

|

|

|

|

|

|

|

|

City |

State |

Postal/ZIP Code |

|

Title (Owner, Partner or Member, Officer, or Duly Authorized Agent) |

|

Date |

|

Seller should retain this Certificate for Seller’s files. Do NOT send to the Department of Taxation.

FORM

| Fact Name | Details |

|---|---|

| Form Title | Resale Certificate for Goods General Form 1 |

| Governing Law | Hawaii Revised Statutes (HRS) sections 231-36 and 237-13 |

| Purpose | This form certifies that a purchaser is exempt from paying sales tax on goods purchased for resale. |

| Tax Identification | The purchaser must hold a Hawaii Tax Identification Number under the General Excise Tax Law. |

| Validity | The certificate remains valid until revoked by the purchaser through written notice. |

| Retention Requirement | Sellers must retain this certificate for their records; it should not be submitted to the Department of Taxation. |

Completing the Hawaii G 17 form is essential for ensuring compliance with state tax regulations. This form serves as a resale certificate, allowing purchasers to buy goods without paying sales tax under certain conditions. Follow the steps below to fill out the form accurately.

Once completed, the seller should retain this certificate for their records. It is important not to send the form to the Department of Taxation. Ensure that all information is accurate to avoid any compliance issues.

What is the Hawaii G 17 form?

The Hawaii G 17 form is a Resale Certificate for Goods. It is used by businesses in Hawaii to certify that they are purchasing tangible personal property for resale. This means that the buyer will not pay general excise tax on these purchases, as they intend to sell the items to customers.

Who needs to fill out the G 17 form?

Any business or individual who holds a Hawaii Tax Identification Number and is purchasing goods for resale should complete this form. It is important that the purchaser is either the owner or an authorized agent of the business.

What information is required on the G 17 form?

The form requires the following information:

How long is the G 17 form valid?

The G 17 form remains valid until it is revoked by the purchaser. The purchaser must provide written notice to the seller if they wish to revoke the certificate.

What should the seller do with the G 17 form?

The seller should keep the completed G 17 form on file for their records. It is not necessary to send the form to the Hawaii Department of Taxation.

What happens if the G 17 form is not used correctly?

If the form is misused or if the purchaser does not qualify for the exemption, the seller may be held responsible for any unpaid taxes. It is crucial to ensure that the form is filled out accurately and that the purchases qualify for resale.

Can the G 17 form be used for all types of purchases?

No, the G 17 form is specifically for tangible personal property that is intended for resale. If the purchaser is buying items for personal use or consumption, they should not use this form.

Where can I obtain a G 17 form?

The G 17 form can be downloaded from the Hawaii Department of Taxation's website. It is also available at various business offices and tax service providers throughout Hawaii.

Filling out the Hawaii G-17 form can seem straightforward, but many people make common mistakes that can lead to complications. One frequent error is failing to provide the correct Hawaii Tax Identification Number. This number is essential for identifying the purchaser's business within the state's tax system. If the number is incorrect or missing, it could invalidate the certificate and create issues during tax audits.

Another mistake is neglecting to specify the nature and character of the business. This section is crucial for the seller to understand the purpose of the purchases. If this information is vague or omitted, it may raise questions about the legitimacy of the resale certificate, potentially leading to disputes or penalties.

Additionally, some individuals forget to check the appropriate boxes regarding the type of purchases. The form requires purchasers to indicate whether their purchases are for retail or wholesale resale. Failing to check these boxes can lead to confusion and misinterpretation of the certificate's intent, which could result in unexpected tax liabilities.

Another common oversight involves the signature and title of the signatory. The form must be signed by an authorized individual, and their title should be clearly stated. If the signature is missing or the title is not included, the form may not hold up under scrutiny, which could jeopardize the purchaser's tax-exempt status.

Finally, many people forget to retain a copy of the completed form for their records. Although the seller is responsible for keeping the certificate on file, it is wise for the purchaser to maintain their own copy as well. This practice ensures that they have documentation on hand in case of any future inquiries or audits.

The Hawaii G-17 form is a resale certificate used by purchasers to certify that they are buying goods for resale. This form is crucial for ensuring compliance with Hawaii's General Excise Tax Law. Various other forms and documents often accompany the G-17 to facilitate transactions and maintain accurate records. Below is a list of related documents frequently utilized in conjunction with the G-17 form.

Each of these forms plays a vital role in ensuring compliance with Hawaii's tax laws. Businesses and individuals should familiarize themselves with these documents to navigate the state's tax system effectively.

The Hawaii G 17 form, known as the Resale Certificate for Goods, serves a specific purpose in the realm of taxation and business transactions. It allows purchasers to certify that they are buying goods for resale, which can exempt them from certain taxes. Several other documents share similarities with the G 17 form in terms of their function and the information they require. Below are five such documents:

When completing the Hawaii G 17 form, it is important to follow specific guidelines to ensure accuracy and compliance. Below is a list of recommended practices and common mistakes to avoid.

Following these guidelines will help ensure that the form is filled out correctly, minimizing the risk of issues with tax compliance.

Misconceptions about the Hawaii G 17 form can lead to confusion and potential issues for both purchasers and sellers. Here are seven common misconceptions, along with clarifications to help ensure proper understanding.

Understanding these misconceptions can help ensure compliance with Hawaii's tax laws and facilitate smoother transactions between buyers and sellers.

The Hawaii G-17 form serves as a resale certificate for goods and is an important document for businesses engaging in the sale of tangible personal property. Here are some key takeaways regarding its completion and use: