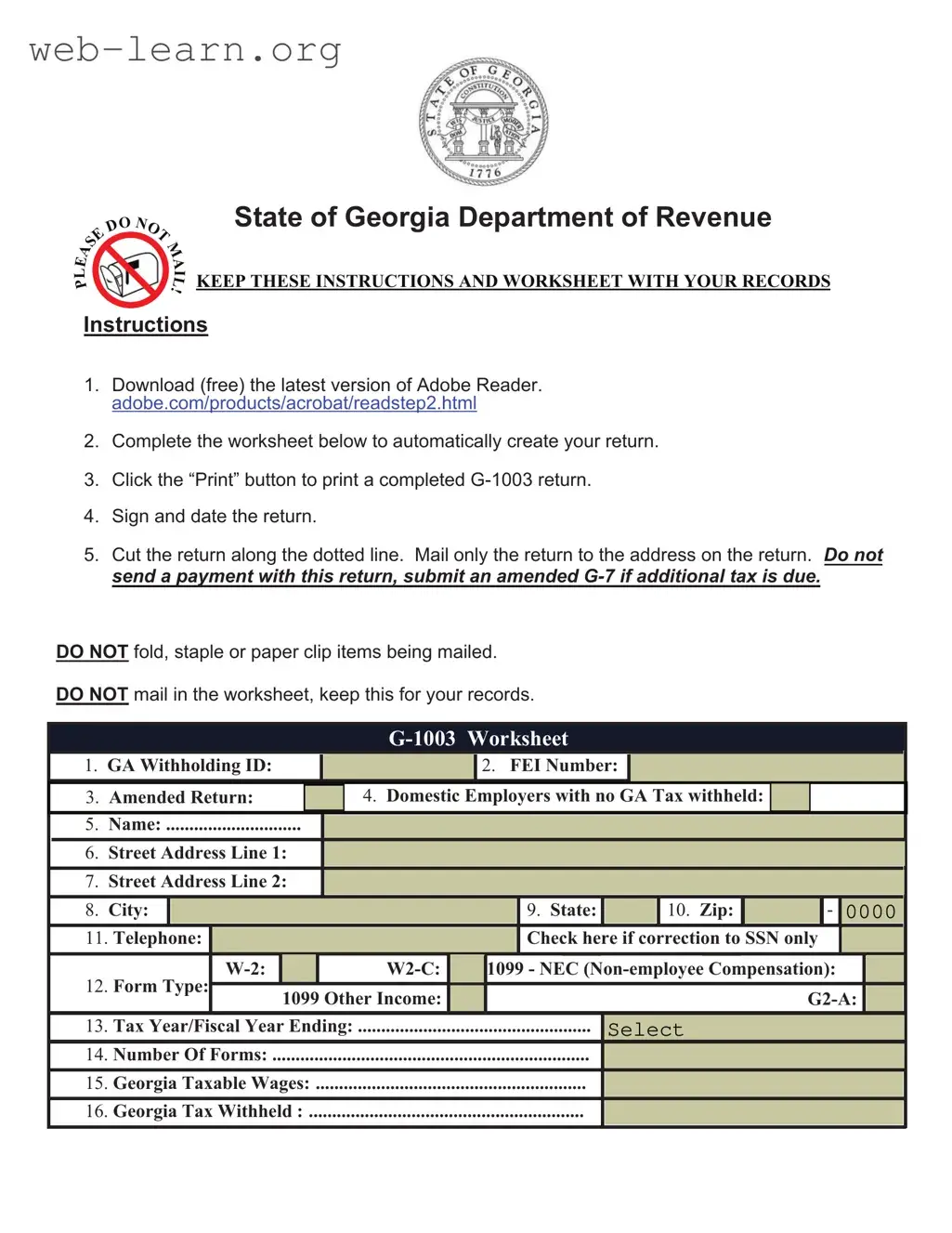

The Georgia G 1003 form plays a crucial role in the state's tax reporting process for employers. It is primarily used to report income statements such as W-2s and 1099s, ensuring that the appropriate Georgia taxes are withheld and reported accurately. Employers must complete the form carefully, including essential details such as the Georgia Withholding ID, FEI number, and the type of forms being submitted. This form is particularly significant for those who are required to file electronically, as it streamlines the reporting process. The due dates for submitting these forms vary based on the type of income statement, with W-2s and 1099-NEC due by January 31, while other 1099s have a February 28 deadline. Employers should be aware of the penalties for late submissions, which can accumulate quickly. It is important to follow the instructions provided, including mailing only the return without any additional documents or payments. Understanding the G 1003 form is essential for compliance and accurate tax reporting in Georgia.

| Fact Name | Fact Description |

|---|---|

| Form Purpose | The G-1003 form is used to report Georgia tax withheld from employees and other payments. |

| Filing Requirement | Employers must file the G-1003 if they have withheld Georgia taxes from wages or payments. |

| Deadline | W-2 and 1099-NEC forms are due by January 31st, while other 1099 forms are due by February 28th. |

| Electronic Filing | Filing electronically is required for certain taxpayers, including those mandated by federal law. |

| Penalty for Late Filing | Late submissions incur penalties, starting at $10 per statement if filed within 30 days. |

| Submission Address | Forms should be mailed to the Georgia Department of Revenue, PO Box 105685, Atlanta, GA 30348-5685. |

| Form Type Options | Options include W-2, W2-C, 1099-NEC, and 1099-Other Income. |

| Correction Procedure | Corrections to W-2s or 1099s must be submitted with copies of the corrected forms. |

| Governing Law | The G-1003 form is governed by Georgia Regulation 560-7-8-.33. |

After completing the Georgia G-1003 form, you will need to print it, sign, and date it before mailing it to the designated address. Ensure that you do not include any payment with this return and keep a copy for your records.

What is the Georgia G-1003 form?

The Georgia G-1003 form is an income statement return used by employers to report Georgia taxable wages and tax withheld from employees. It is particularly important for domestic employers who have withheld Georgia state taxes from their employees' wages.

Who needs to file the G-1003 form?

Employers who have withheld Georgia income tax from their employees must file the G-1003 form. This includes those who issue W-2s or 1099 forms that report Georgia taxable wages. If you are a domestic employer, this form is necessary for compliance with state tax regulations.

When is the G-1003 form due?

The G-1003 form is due by January 31st for W-2 and 1099-NEC forms. Other 1099 income statements are due by February 28th. If the due date falls on a weekend or holiday, the form is due the next business day.

How do I complete the G-1003 form?

To complete the G-1003 form, follow these steps:

Can I file the G-1003 form electronically?

Yes, if you file and pay electronically, or if you are required to file income statements electronically, you must submit the G-1003 form electronically. This is also true for those who file Form G2-FL. Even if not required, you may choose to file electronically.

What happens if I miss the deadline for filing?

If you miss the deadline for filing the G-1003 form, you may incur penalties. Late penalties can range from $10 to $50 per statement, depending on how late the filing is. The total penalties can accumulate up to $200,000 based on the duration of the delay.

What should I do if I need to amend my G-1003 form?

If you need to amend your G-1003 form, you must submit an amended G-7 form if additional tax is due. Ensure that you also include copies of any corrected W-2s or 1099s with your amended return.

Where do I send the completed G-1003 form?

Mail the completed G-1003 form to the following address:

Processing Center

Georgia Department of Revenue

PO Box 105685

Atlanta, GA 30348-5685

Remember to only mail the return and not the entire page. Cut along the dotted line before mailing.

Are there specific forms that can be filed with the G-1003?

The G-1003 can be filed with W-2s, W-2-Cs, and 1099-NEC forms. However, other form types must be filed separately. For instance, G2-As for nonresident members should not be included with other forms.

What should I keep for my records?

It is important to keep the worksheet and any copies of submitted forms for your records. Do not mail the worksheet; retain it for your documentation.

Completing the Georgia G-1003 form can be straightforward, but many individuals make critical mistakes that can lead to delays or penalties. One common error is failing to provide the correct GA Withholding ID. This identification number is essential for processing your return accurately. Double-check that you have entered the correct ID, as any discrepancies can result in your submission being rejected.

Another frequent mistake involves the Form Type selection. Many filers overlook the importance of indicating the correct form type, such as W-2, 1099-NEC, or 1099-Other Income. This selection directly impacts how your return is processed. If you select the wrong form type, it can lead to complications, including potential penalties for late filing.

In addition, not completing the sections for Georgia Taxable Wages and Georgia Tax Withheld accurately can be detrimental. These figures must reflect the correct amounts withheld and earned. If these fields are left blank or filled out incorrectly, it can lead to further inquiries from the Department of Revenue, causing unnecessary delays in processing your return.

Lastly, many individuals neglect to sign and date the return before mailing it. This step is crucial. A missing signature can render the entire submission invalid, leading to additional processing time or penalties. Ensure that you have signed and dated the form, and remember to cut along the dotted line before mailing it to the specified address.

The Georgia G 1003 form is an important document used for reporting income statements and withholding tax information to the Georgia Department of Revenue. Several other forms and documents are often used in conjunction with the G 1003 to ensure compliance with state tax regulations. Below is a list of these forms, along with brief descriptions of their purposes.

Understanding these forms and their purposes is essential for compliance with Georgia tax regulations. Properly completing and submitting the G 1003 along with the necessary supporting documents can help avoid penalties and ensure accurate reporting of income and withholdings.

The Georgia G-1003 form is an important document for employers in the state, particularly for reporting income and withholding taxes. Several other forms serve similar purposes in the realm of tax reporting and compliance. Below is a list of four documents that share similarities with the Georgia G-1003 form:

When filling out the Georgia G-1003 form, it's essential to follow specific guidelines to ensure your submission is accurate and compliant. Here’s a list of dos and don’ts to help you navigate the process smoothly.

Understanding the Georgia G-1003 form is crucial for employers and tax professionals. However, several misconceptions can lead to confusion. Here are four common misunderstandings:

While the G-1003 is primarily used to report Georgia tax withholdings, it can also be used by domestic employers who do not withhold Georgia tax. Employers must still file the form even if no tax is withheld.

This is not accurate. The instructions clearly state that no payment should be submitted with the G-1003. Instead, if additional tax is due, an amended G-7 should be filed separately.

In fact, any employer may choose to file the G-1003 electronically, regardless of whether they are federally required to do so. This option can streamline the filing process and reduce errors.

It is essential to note that only specific forms can be submitted with the G-1003. For instance, W-2s, W-2-Cs, and 1099-NEC can be filed together, but other form types must be submitted separately.

When filling out and using the Georgia G 1003 form, keep the following key takeaways in mind: