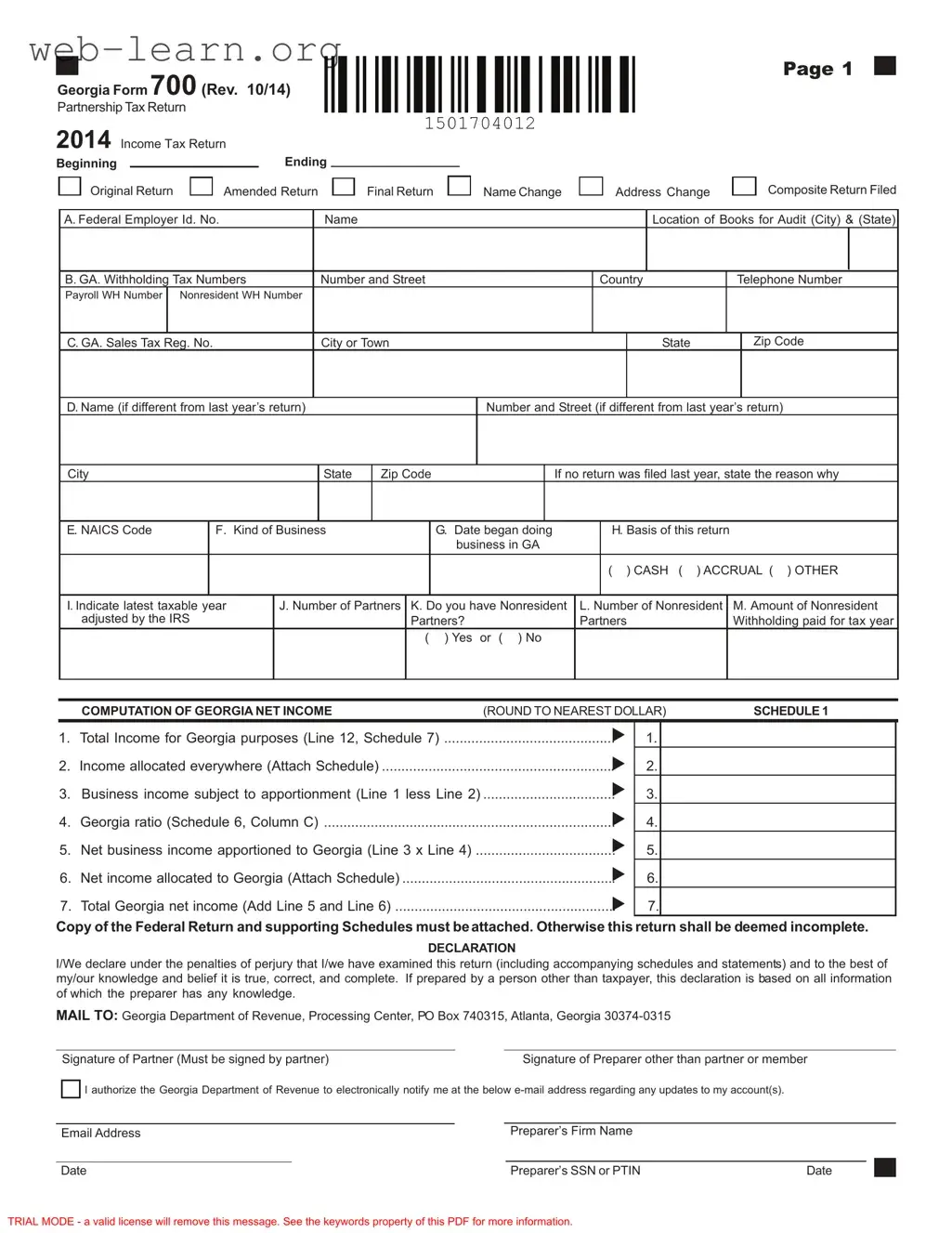

For partnerships operating in Georgia, understanding the Georgia Form 700 is essential for compliance with state tax regulations. This form serves as the Partnership Tax Return, capturing critical financial information that reflects the partnership's income and tax obligations. It includes sections for identifying the partnership, such as its name, address, and federal employer identification number. The form also requires details about the business's operations, including the type of business, the date it began operating in Georgia, and the basis of the return—whether cash, accrual, or other methods. Additionally, partnerships must indicate the number of partners and whether any are nonresidents. The computation of Georgia net income is a key aspect of the form, requiring partnerships to calculate total income, allocated income, and business income subject to apportionment. Various schedules within the form allow for the reporting of tax credits, distributions to partners, and adjustments to federal taxable income, ensuring a comprehensive view of the partnership's financial landscape. Filing the Georgia Form 700 accurately is crucial, as it not only affects tax liability but also ensures that partnerships remain in good standing with the Georgia Department of Revenue.

| Fact Name | Description |

|---|---|

| Form Purpose | The Georgia Form 700 is used for filing the Partnership Tax Return for income tax purposes. |

| Filing Requirements | This form must be filed by partnerships doing business in Georgia, including those with nonresident partners. |

| Governing Law | The form is governed by the Georgia Income Tax Act, O.C.G.A. § 48-7-1 et seq. |

| Submission Details | Completed forms must be mailed to the Georgia Department of Revenue, Processing Center, PO Box 740315, Atlanta, GA 30374-0315. |

Completing the Georgia Form 700 is an essential step for partnerships operating in Georgia. This form collects vital information about your partnership’s income, business activities, and tax obligations. Below are clear and concise steps to guide you through the process of filling out the form accurately.

What is the Georgia Form 700?

The Georgia Form 700 is the Partnership Tax Return used by partnerships operating in Georgia to report their income, deductions, and credits. It is essential for partnerships to file this form to ensure compliance with state tax laws.

Who needs to file the Georgia Form 700?

Any partnership that conducts business in Georgia must file the Georgia Form 700. This includes both resident and nonresident partnerships. If the partnership has nonresident partners, additional information regarding their income and withholding may also be required.

What information is required on the Georgia Form 700?

The form requires various details, including:

Additionally, partnerships must report the income allocated to Georgia and any applicable tax credits.

How do partnerships calculate their Georgia net income?

To determine Georgia net income, partnerships must follow these steps:

The final figure represents the total Georgia net income.

What are Georgia tax credits, and how are they reported?

Georgia tax credits are incentives provided by the state to encourage certain business activities. Partnerships must report these credits on Schedule 2 of the Form 700. Each credit claimed must include the credit type code, the company name, and the amount of credit. If more than ten credits are claimed, a detailed schedule should be attached.

What is the purpose of the declaration section on the form?

The declaration section requires the partner or preparer to affirm that the information provided is accurate and complete. This statement is made under penalties of perjury, emphasizing the importance of honesty in tax reporting.

Can the Georgia Form 700 be amended?

Yes, partnerships can file an amended return using the Georgia Form 700 if they need to correct errors or make changes to the originally filed return. The form provides a specific option to indicate that it is an amended return.

Where should the completed Georgia Form 700 be mailed?

The completed form should be mailed to the Georgia Department of Revenue, Processing Center, PO Box 740315, Atlanta, Georgia 30374-0315. It is crucial to ensure that the return is sent to the correct address to avoid processing delays.

What happens if the Georgia Form 700 is not filed?

If a partnership fails to file the Georgia Form 700, it may face penalties and interest on any taxes owed. Additionally, the partnership may be subject to audits and other enforcement actions by the Georgia Department of Revenue.

Are there any filing deadlines for the Georgia Form 700?

The Georgia Form 700 is generally due on the 15th day of the fourth month following the close of the partnership's tax year. For partnerships operating on a calendar year, this means the form is typically due by April 15. Extensions may be available, but they must be requested properly.

Filling out the Georgia Form 700 can be a complex task, and many individuals make mistakes that can lead to delays or issues with their tax filings. One common error is failing to include the correct Federal Employer Identification Number (FEIN). This number is essential for the processing of the return. Without it, the form may be deemed incomplete, which can result in penalties or additional scrutiny from the Georgia Department of Revenue.

Another frequent mistake is neglecting to check the appropriate box for the type of return being filed. Whether it is an original, amended, or final return, this selection is crucial. Incorrectly marking this section can lead to confusion and miscommunication with tax authorities.

Many filers also overlook the importance of providing accurate contact information. The address, phone number, and email should be current and correct. If the Georgia Department of Revenue needs to reach out for clarification or additional information, having outdated contact details can cause significant delays.

Additionally, some individuals fail to attach the required copy of the Federal Return and supporting schedules. This attachment is mandatory; without it, the Georgia Form 700 may be considered incomplete. This oversight can lead to rejection of the return or additional requests for information.

Another common error involves the calculation of Georgia net income. It is essential to ensure that all income is accurately reported and that the calculations are correct. Mistakes in this section can lead to underreporting or overreporting of income, which may trigger audits or penalties.

Some filers also forget to sign the return. The signature of a partner is required for the return to be valid. A missing signature can delay processing and create complications in the filing status.

Lastly, failing to claim all eligible tax credits can result in lost savings. Many individuals do not take the time to review the available Georgia tax credits thoroughly. Ensuring that all applicable credits are claimed can significantly reduce the overall tax liability.

The Georgia Form 700 is a crucial document for partnerships operating in Georgia, serving as the Partnership Tax Return. However, it is often accompanied by several other forms and documents that provide additional information and fulfill various requirements. Understanding these documents can help ensure compliance and facilitate the filing process.

Each of these forms and documents plays a significant role in the overall tax reporting process for partnerships in Georgia. By understanding their purposes and requirements, partnerships can better navigate the complexities of tax compliance and ensure that they meet all necessary obligations.

The Georgia Form 700 is a partnership tax return that shares similarities with several other tax documents. Here’s a look at four such documents:

When filling out the Georgia Form 700, it is essential to adhere to specific guidelines to ensure accuracy and compliance. Below is a list of things to do and avoid during this process.

This is not true. The Georgia 700 form is designed for all partnerships operating in Georgia, regardless of size. Small partnerships must also file this return to report their income and fulfill state tax obligations.

Many believe that if a partnership has no income, it does not need to file. However, even partnerships with no income must submit the Georgia 700 form. This ensures compliance with state regulations and avoids potential penalties.

Some individuals think they can submit the Georgia 700 form independently. In reality, a copy of the federal return and supporting schedules must accompany the Georgia 700 form. Failing to do so can render the return incomplete.

This is a common misunderstanding. A partnership can file the Georgia 700 form even if some partners reside outside Georgia. However, the partnership must still report income earned within the state.

While both forms serve similar purposes, they are not identical. The Georgia 700 form includes specific state requirements and calculations that differ from the federal partnership tax return. It is essential to understand these differences to ensure accurate reporting.

Ensure that you provide accurate information on the Georgia 700 form. Double-check details such as the Federal Employer Identification Number (FEIN), business address, and partner information.

Attach all required schedules and documentation. A copy of the Federal Return and supporting schedules must accompany the form, or it may be considered incomplete.

Be aware of the different types of returns. Indicate whether you are filing an original, amended, or final return, as this affects how the form is processed.

Understand the importance of the declaration section. This section must be signed by a partner, affirming that the information provided is true and complete.