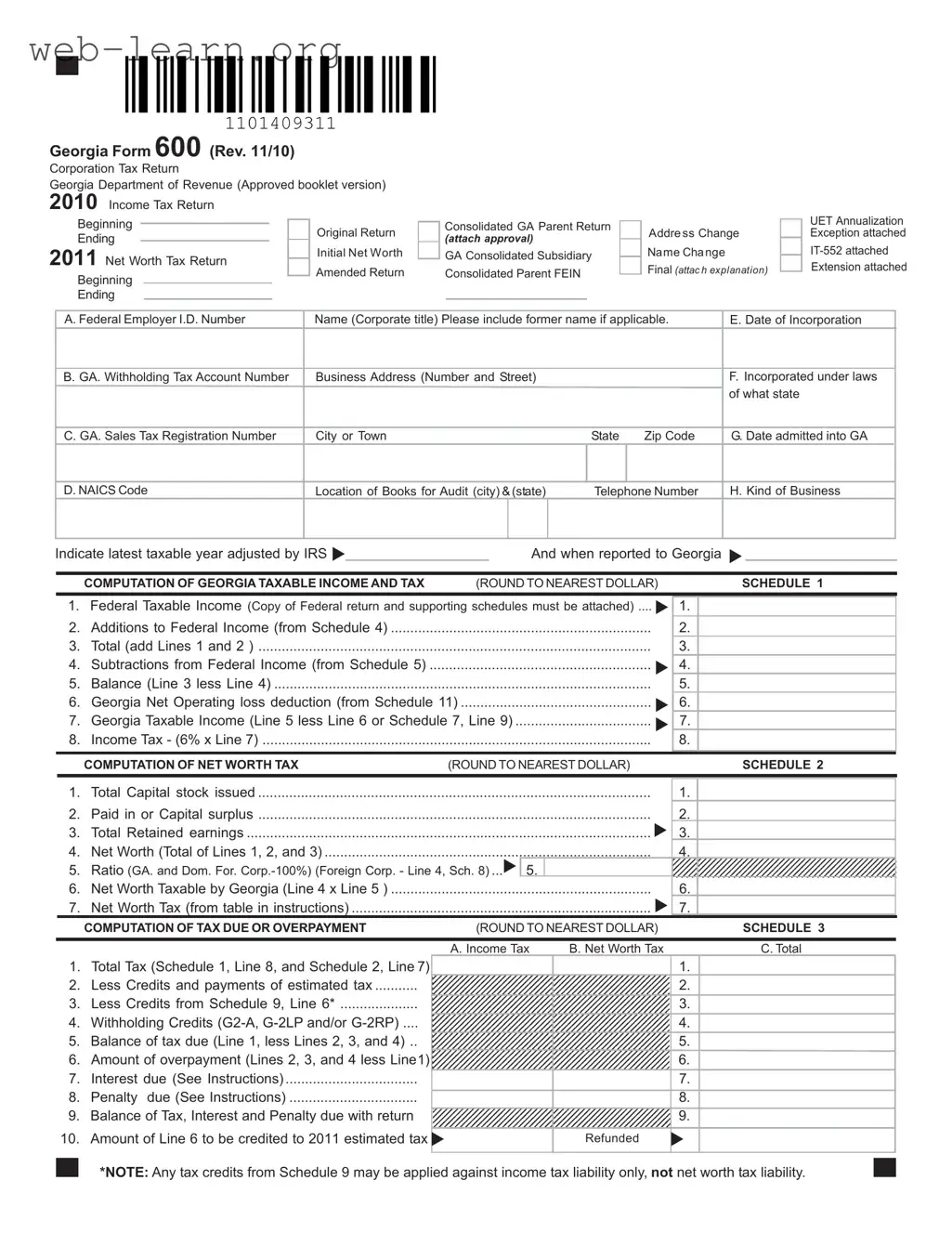

The Georgia Form 600 is a vital document for corporations operating within the state, serving as their Corporation Tax Return. This form is essential for reporting income, calculating taxes owed, and ensuring compliance with state regulations. It covers various aspects of corporate financials, including federal taxable income, net worth tax, and potential tax credits. Corporations must provide details such as their Federal Employer Identification Number (FEIN), business address, and date of incorporation. The form also requires corporations to report their income, deductions, and any additions or subtractions from federal taxable income. Additionally, it includes sections for calculating net worth tax and determining any tax due or overpayment. Proper completion of the Georgia Form 600 is crucial for avoiding penalties and ensuring accurate tax reporting, making it a key component of corporate financial management in Georgia.

| Fact Name | Description |

|---|---|

| Purpose of Form | The Georgia Form 600 is primarily used by corporations to report income and calculate taxes owed to the state of Georgia. |

| Filing Requirement | Corporations doing business in Georgia must file this form annually, regardless of whether they owe taxes, to comply with state regulations. |

| Governing Law | This form is governed by the Georgia Public Revenue Code, specifically under Section 48-7-20, which outlines corporate income tax regulations. |

| Attachments Needed | Taxpayers must attach a copy of their federal tax return and any relevant schedules to ensure the completeness and accuracy of their Georgia tax return. |

Filling out the Georgia Form 600 is an important step for corporations to report their income and taxes to the state. This form requires specific information about your business, including financial details and tax credits. After completing the form, it should be submitted to the Georgia Department of Revenue along with any necessary attachments.

What is the Georgia Form 600?

The Georgia Form 600 is the state corporation tax return that businesses must file with the Georgia Department of Revenue. It is used to report income, calculate taxes owed, and provide necessary information about the corporation. This form includes sections for both income tax and net worth tax, along with various schedules for detailed calculations.

Who needs to file Form 600?

Any corporation doing business in Georgia is required to file Form 600. This includes domestic corporations incorporated in Georgia and foreign corporations that are registered to operate in the state. If your corporation has income or activities in Georgia, filing is necessary.

What information is required on Form 600?

Form 600 requires various details, including:

Additional schedules may be necessary, depending on the corporation's specific circumstances.

How do I calculate Georgia taxable income?

To determine Georgia taxable income, start with your federal taxable income. Then, make necessary adjustments by adding certain amounts (like state bond interest) and subtracting others (like interest on U.S. obligations). The result is your Georgia taxable income, which is then used to calculate the income tax owed.

What is the net worth tax, and how is it calculated?

The net worth tax applies to corporations based on their total capital stock, paid-in surplus, and retained earnings. To calculate this tax, add these amounts together to find the total net worth. Then, apply the appropriate ratio for Georgia to determine the taxable amount and refer to the provided tax table for the final tax due.

Are there any credits available to reduce my tax liability?

Yes, Georgia offers various tax credits that can reduce your tax liability. These may include credits for job creation, investment in certain industries, and other incentives. You must list any claimed credits on Schedule 9 of Form 600, and additional documentation may be required to support your claims.

What happens if I need to amend my Form 600?

If you discover errors after filing your Form 600, you can file an amended return. You will need to complete the form again, indicating it is an amended return, and provide details about the changes. Be sure to include any necessary schedules and documentation to support the amendments.

When is the Form 600 due?

Form 600 is generally due on the 15th day of the fourth month following the end of your corporation’s tax year. If you need more time, you can file for an extension, but be sure to attach the extension request to your return. Remember, extensions only provide extra time to file, not to pay any taxes owed.

Where do I send my completed Form 600?

Once you have completed Form 600, mail it to the Georgia Department of Revenue, Processing Center, P.O. Box 740397, Atlanta, Georgia 30374-0397. Make sure to include any required schedules and payment if you owe taxes.

Filling out the Georgia Form 600 can be a daunting task, and mistakes can lead to delays or penalties. One common error is failing to attach the required copies of the federal return and supporting schedules. This form mandates that these documents accompany the submission; without them, the return may be deemed incomplete.

Another frequent oversight is neglecting to provide accurate identification numbers. The Federal Employer Identification Number (FEIN), Georgia Withholding Tax Account Number, and Sales Tax Registration Number must all be correctly entered. An incorrect number can cause confusion and may lead to processing issues.

Many filers also forget to include former names of the corporation if applicable. This detail is important for the Georgia Department of Revenue to accurately track the corporation's history and tax obligations. Omitting this information can lead to complications in processing the return.

Inaccurate calculations are another area where mistakes often occur. When calculating Georgia taxable income, ensure that all additions and subtractions from federal income are correctly tallied. Errors in these calculations can result in incorrect tax liabilities, which may lead to penalties.

Another mistake is failing to check the appropriate boxes for tax credits. If claiming credits, it’s essential to enter the correct type code and amount. Not doing so can result in missed opportunities for tax relief.

Additionally, some filers do not account for the proper apportionment of income. This is particularly crucial for corporations operating in multiple states. Incorrect apportionment can lead to overpayment or underpayment of taxes.

It's also important to ensure that all information is current and accurate. Changes in the business address or corporate structure should be updated on the form. Failing to do so can lead to miscommunication and potential penalties.

Another common error is neglecting to sign the form. A signature is necessary to validate the return. Without it, the submission may be rejected, leading to delays in processing.

Lastly, some people overlook the requirement to file an extension if they need more time. If an extension is necessary, a copy of the request must be attached. Not following this guideline can result in penalties for late filing.

By being aware of these common mistakes and taking the time to carefully review the form before submission, individuals can help ensure a smoother filing process and avoid potential issues with the Georgia Department of Revenue.

The Georgia Form 600 is a crucial document for corporations filing their tax returns in Georgia. Alongside this form, several other documents may be required or helpful in ensuring accurate and complete tax reporting. Below is a list of these forms, each accompanied by a brief description to clarify their purpose.

Understanding these accompanying forms can simplify the tax preparation process and help ensure compliance with Georgia tax laws. Each document serves a specific purpose in the overall tax filing, making it essential for corporations to gather and complete them accurately.

When filling out the Georgia Form 600, there are important guidelines to follow. Adhering to these can help ensure your submission is accurate and complete.

Following these guidelines can help streamline the process and reduce the chances of delays or issues with your filing. Take your time to review each section carefully before submission.

This form is primarily designed for corporations, but certain limited liability companies (LLCs) and partnerships may also need to file it under specific circumstances. It's crucial to determine your business structure before assuming the form does not apply to you.

Filing this form is not optional for businesses that meet the criteria set by the Georgia Department of Revenue. Failure to file can result in penalties and interest on unpaid taxes, making it essential to comply with the requirements.

It's a common belief that the form can be submitted on its own. However, you must attach a copy of your federal return and any relevant schedules. Without these documents, your submission may be considered incomplete.

Many assume that tax credits will be automatically applied to their tax liability. In reality, you must explicitly list and claim these credits on the form. If you miss this step, you could end up paying more than necessary.

While extensions can be requested, they are not granted automatically. You must provide a copy of your federal extension request or Form IT-303. If you fail to do so, your request may be denied.

Tax forms can change from year to year. It's vital to use the correct version of the Georgia 600 form for the tax year you are filing. Using an outdated form could lead to complications or delays in processing your return.

Here are some key takeaways about filling out and using the Georgia 600 form: