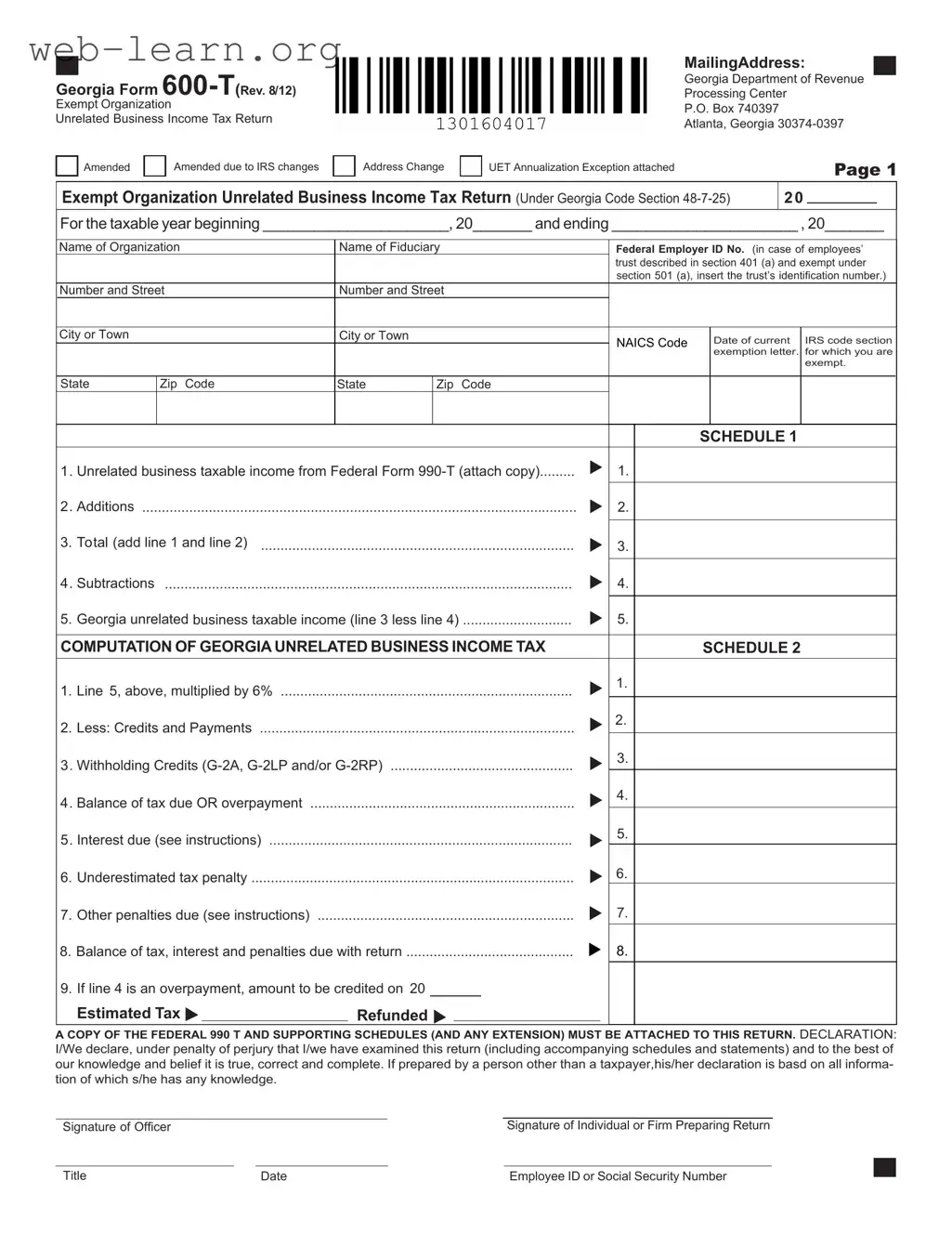

The Georgia Form 600-T is a critical document for exempt organizations that generate unrelated business income from Georgia sources. This form serves as the Exempt Organization Unrelated Business Income Tax Return, which must be filed by any organization required to submit a Federal Form 990-T. The form collects essential information such as the organization’s name, federal employer identification number, and details regarding the unrelated business taxable income. It includes specific schedules to calculate the total income, deductions, and applicable tax rates, which are set at 6% under Georgia law. Filing deadlines align with those of the federal return, and any necessary amendments or address changes must also be reported. Organizations are required to attach a copy of their Federal Form 990-T along with any supporting schedules. Failure to comply with these requirements can result in penalties and interest, making timely and accurate submission essential. Understanding the nuances of the Georgia Form 600-T is vital for maintaining compliance and avoiding potential financial repercussions.

| Fact Name | Fact Description |

|---|---|

| Form Title | The Georgia Form 600-T is titled "Exempt Organization Unrelated Business Income Tax Return." It is used for reporting unrelated business income by exempt organizations. |

| Governing Law | This form is governed by Georgia Code Section 48-7-25, which outlines the taxation of unrelated business income. |

| Filing Requirement | Every exempt organization that files a Federal Form 990-T and has unrelated trade or business income from Georgia sources must file Form 600-T. |

| Filing Deadline | The return is due on or before the due date of the Federal Form 990-T, as specified by the Internal Revenue Code. |

| Mailing Address | Completed forms should be mailed to the Georgia Department of Revenue, Processing Center, P.O. Box 740397, Atlanta, Georgia 30374-0397. |

| Tax Rate | The unrelated business income is taxed at a rate of 6%, according to Georgia Code Section 48-7-25(c). |

| Extension of Time | An extension for filing may be granted upon application, provided it shows reasonable cause. This request must be made before the return's due date. |

| Penalties | Penalties for delinquent filing and payment can accumulate, with rates including 5% for late filing and 1/2 of 1% for late payments each month. |

| Required Attachments | A copy of the Federal Form 990-T and any supporting schedules must be attached to the Georgia Form 600-T when submitted. |

Filling out the Georgia 600 T form is a straightforward process, but attention to detail is crucial. This form is necessary for exempt organizations that have unrelated business income from Georgia sources. Completing the form accurately ensures compliance with state tax requirements.

What is the Georgia Form 600-T?

The Georgia Form 600-T is the Exempt Organization Unrelated Business Income Tax Return. It is specifically designed for exempt organizations that have unrelated business income from Georgia sources. If your organization is required to file a Federal Form 990-T, you must also file this state form to report your unrelated business taxable income.

When is the Georgia Form 600-T due?

The Form 600-T is due on or before the due date of your Federal Form 990-T. It is important to mail your completed return to the Georgia Department of Revenue Processing Center at P.O. Box 740397, Atlanta, GA 30374-0397. Make sure to check for any updates or changes to the filing deadlines.

What if I need more time to file?

If you need an extension of time to file the Georgia Form 600-T, you can apply for one using Form IT-303. This request must be submitted before the original due date and should explain your reasonable cause for needing the extension. If you have already received an extension from the IRS for your Federal return, you do not need to apply separately for Georgia.

What is the tax rate for unrelated business income?

The tax rate for unrelated business income in Georgia is 6%. This rate applies to the Georgia unrelated business taxable income calculated on your Form 600-T. Ensure that you accurately report your income and expenses to determine the correct taxable amount.

What happens if I file late or underpay my taxes?

Filing late can result in penalties. Georgia imposes a 5% penalty for each month or part of a month that the tax remains unpaid after the due date. Additionally, if you underpay your taxes, penalties can range from 5% for negligent underpayment to 50% for fraudulent underpayment. Interest on unpaid taxes accrues at a rate of 12% per year from the due date until paid. To avoid these penalties, file your return on time and pay any taxes due promptly.

Filling out the Georgia Form 600-T can be a challenging task for many organizations. One common mistake is failing to attach the required copies of the Federal Form 990-T and any supporting schedules. This form is essential for the Georgia Department of Revenue to process your return accurately. If these documents are not included, it may lead to delays or even penalties.

Another frequent error involves incorrectly calculating the unrelated business taxable income. Organizations must ensure that they accurately report the income derived from unrelated business activities. This means carefully reviewing the figures reported on the Federal Form 990-T and making sure that all additions and subtractions are properly accounted for. Mistakes in these calculations can result in incorrect tax liability, which could lead to unexpected penalties.

Many individuals also overlook the importance of providing a complete and accurate mailing address. If the address is incomplete or incorrect, important correspondence from the Georgia Department of Revenue may not reach the organization. This can result in missed deadlines or failure to receive critical information regarding the tax return.

Lastly, organizations sometimes forget to sign the return. A signature is a declaration that the information provided is true and correct to the best of the signer’s knowledge. Without a signature, the return may be considered invalid, leading to complications in processing. Taking the time to review each section of the form and ensuring all requirements are met can prevent these common pitfalls.

The Georgia Form 600-T is essential for exempt organizations reporting unrelated business income in Georgia. To ensure compliance and provide complete information, several other forms and documents are often used in conjunction with the Georgia 600-T. Below are some of the key documents that may be required.

Understanding these forms and documents can help organizations navigate their tax responsibilities more smoothly. By ensuring that all necessary paperwork is completed and submitted on time, organizations can avoid potential penalties and maintain compliance with state regulations.

The Georgia Form 600-T is an important document for exempt organizations reporting unrelated business income. Several other forms share similarities with the 600-T, particularly in their purpose and requirements. Here are nine documents that are comparable:

When filling out the Georgia Form 600-T, it’s important to ensure accuracy and compliance with state regulations. Here’s a list of things you should and shouldn’t do to make the process smoother.

By following these guidelines, you can help ensure that your Georgia Form 600-T is filled out correctly and submitted on time, minimizing potential issues down the road.

Understanding the Georgia Form 600 T can be a bit challenging, especially with all the details involved. Here are five common misconceptions about this form, along with clarifications to help clear things up.

Being informed about these misconceptions can help organizations navigate their tax responsibilities more effectively. It's always wise to consult with a tax professional if there are any uncertainties regarding the filing process.

Understanding the Georgia Form 600 T is essential for exempt organizations with unrelated business income. Here are key takeaways to guide you through the process:

Following these guidelines will help ensure compliance and minimize potential issues with the Georgia Department of Revenue.