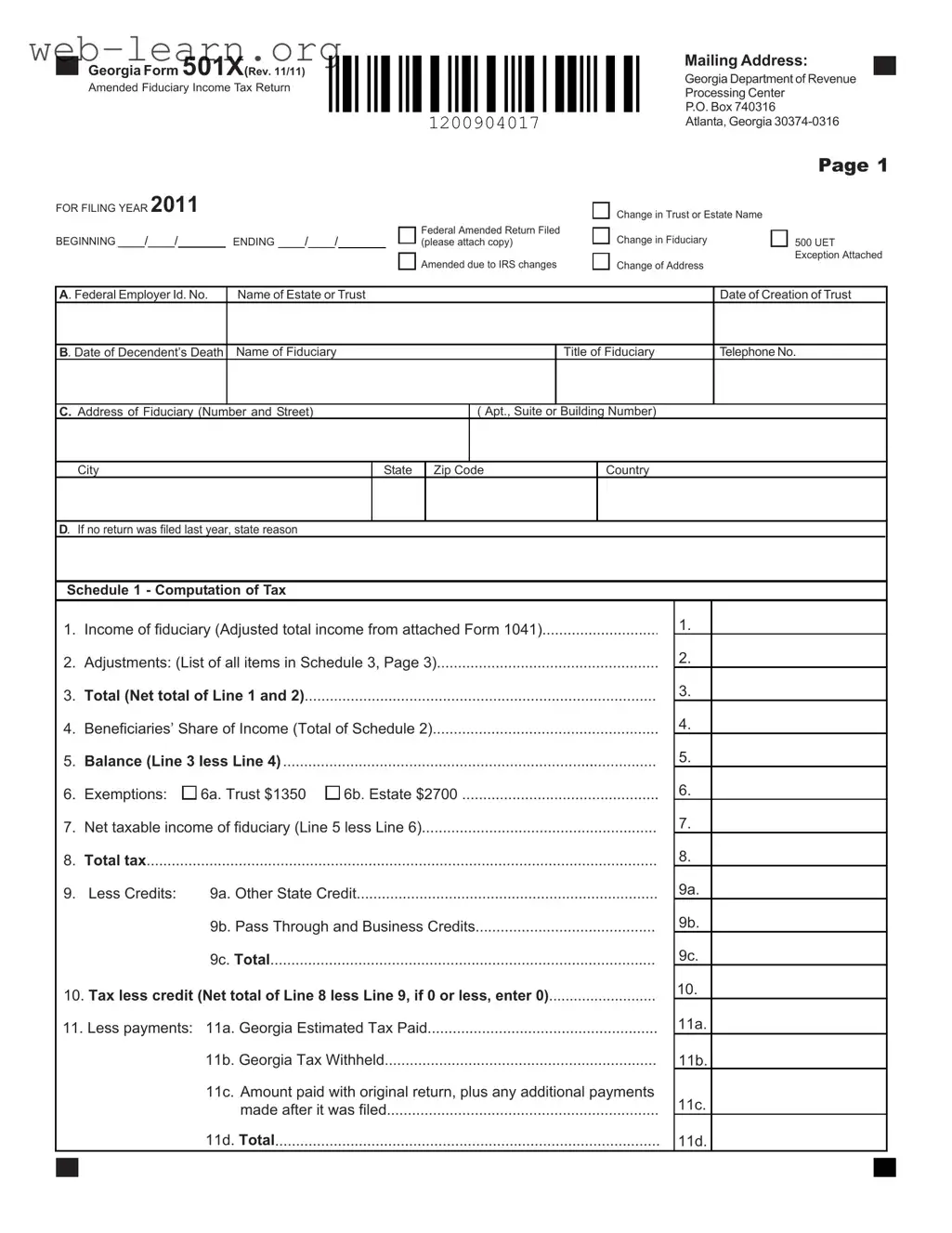

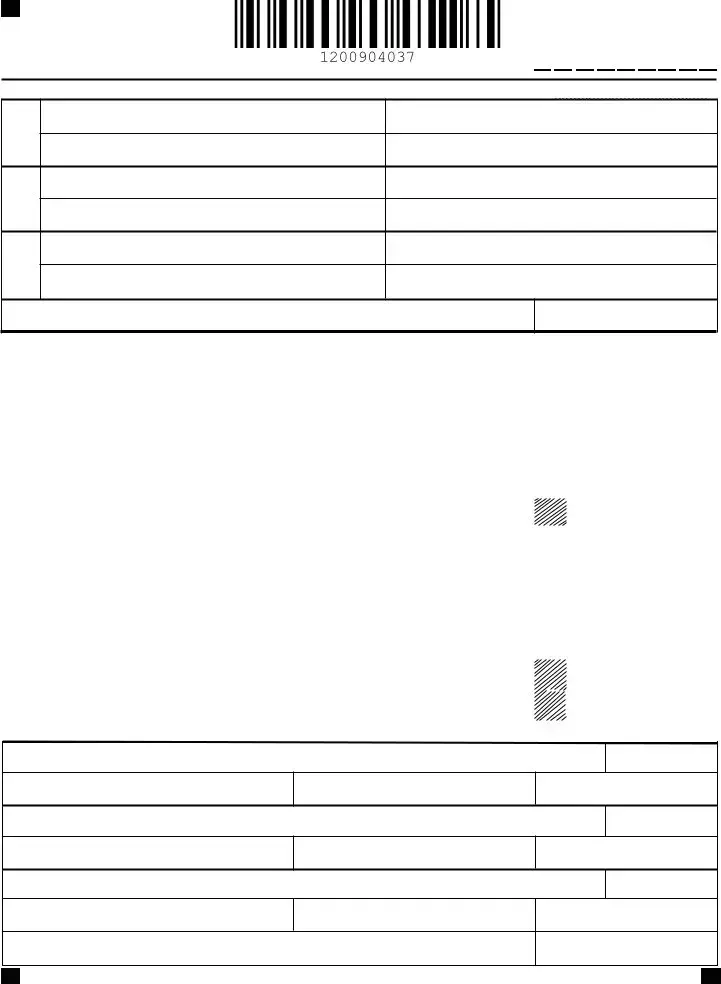

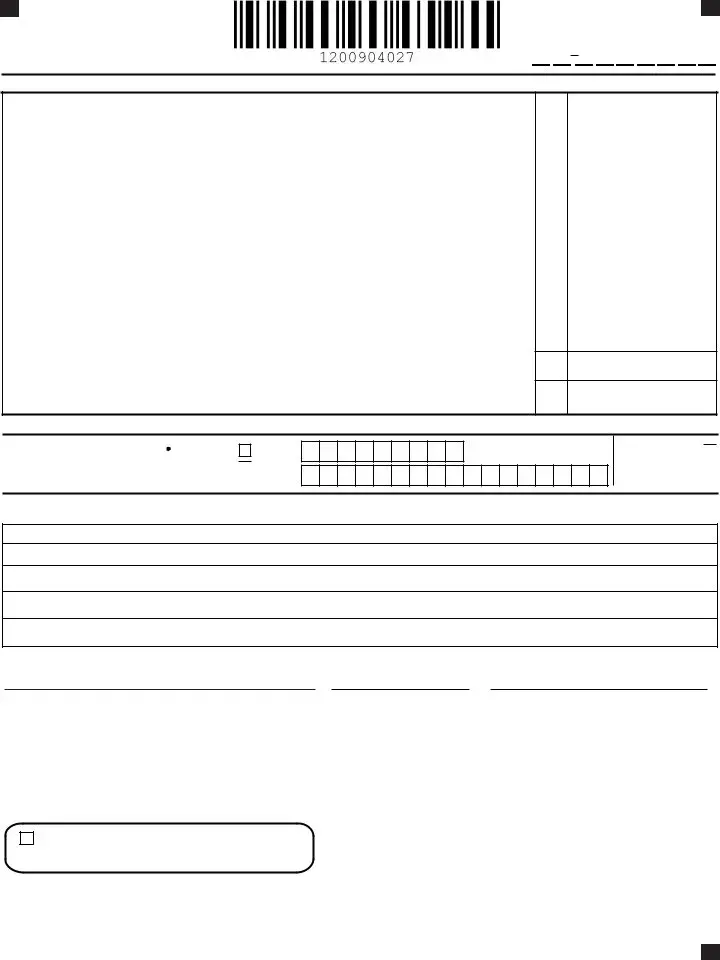

The Georgia Form 501X serves as an essential tool for fiduciaries managing trusts and estates that need to amend their income tax returns. This form is particularly relevant for those who have experienced changes that necessitate a revision of previously filed returns, such as modifications due to IRS adjustments, changes in the trust or estate name, or updates regarding fiduciary details. Completing the 501X involves providing key information, including the federal employer identification number, the name and creation date of the trust or estate, and the fiduciary's contact details. The form also requires a detailed computation of tax, adjustments to income, and the allocation of income among beneficiaries. Additionally, it includes sections for exemptions, tax credits, and any penalties that may apply. By submitting the 501X, fiduciaries ensure compliance with Georgia tax laws while accurately reflecting their financial circumstances, ultimately safeguarding their interests and those of the beneficiaries they serve.

| Fact Name | Details |

|---|---|

| Purpose | The Georgia Form 501X is used to amend the Fiduciary Income Tax Return for estates and trusts. |

| Filing Requirement | All fiduciaries with income from Georgia sources must file this form if they are amending a previously submitted return. |

| Governing Law | This form is governed by the Georgia Code, specifically O.C.G.A. § 48-7-27. |

| Filing Address | Completed forms should be mailed to the Georgia Department of Revenue at P.O. Box 740316, Atlanta, Georgia 30374-0316. |

| Deadline | The amended return must be filed by the 15th day of the 4th month following the close of the taxable year. |

| Attachments Required | A copy of the federal amended return and any supporting documents must be attached to the form. |

| Penalties for Non-compliance | Failure to file or pay taxes on time may result in penalties, including a 5% charge per month on unpaid tax, up to a maximum of 25%. |

Filling out the Georgia Form 501X requires careful attention to detail. This form is used to amend a fiduciary income tax return. It is important to ensure that all information is accurate and complete to avoid any potential issues with the Georgia Department of Revenue.

What is the purpose of the Georgia Form 501X?

The Georgia Form 501X is used to amend a fiduciary income tax return. If there are changes to your original return due to IRS adjustments, or if you need to correct errors, this form allows you to report those changes. The form is specifically designed for estates and trusts, ensuring that any updates to income, deductions, or credits are accurately reflected in your tax filings.

Who is required to file the Georgia Form 501X?

Any fiduciary managing an estate or trust that has income sourced within Georgia must file this form. This includes both residents and non-residents. If you are responsible for managing funds or property for the benefit of a Georgia resident, you are obligated to file a Georgia income tax return using Form 501. If you need to make amendments to this return, Form 501X is the appropriate document to submit.

What information do I need to complete the Georgia Form 501X?

When filling out the Form 501X, you will need several pieces of information:

Having this information ready will streamline the process and help ensure accuracy in your amended return.

What are the penalties for not filing or for late filing of the Georgia Form 501X?

Failure to file the Georgia Form 501X on time can lead to penalties. Generally, if you do not file by the due date, you may incur a late filing penalty of 5% of the unpaid tax for each month or part of a month that the return is late, up to a maximum of 25%. Additionally, if you owe tax and do not pay it by the due date, you may face an additional penalty of 0.5% of the unpaid tax for each month, also capped at 25%. It is crucial to file on time to avoid these financial repercussions.

Filling out the Georgia Form 501X can be a challenging task, and several common mistakes can lead to complications. One frequent error is failing to attach the required federal return. The instructions clearly state that a copy of the federal amended return must accompany the Georgia form. Omitting this document can result in delays in processing or even rejection of the return.

Another mistake often made is incorrect or incomplete beneficiary information. Schedule 2 requires detailed information about each beneficiary, including their share of income. If this section is not filled out accurately or if the total does not match the amount reported on Line 4 of Schedule 1, it may lead to discrepancies. This can complicate the tax return and create issues with the Georgia Department of Revenue.

Additionally, many individuals neglect to double-check their calculations. Errors in mathematical computations, particularly on lines that involve income, adjustments, and tax owed, can lead to significant problems. Ensuring that all figures are accurate and that totals are correctly carried over is essential for a smooth filing process.

Lastly, failing to sign the form is a common oversight. The declaration at the end of the form requires signatures from both the fiduciary and any preparer, if applicable. Without these signatures, the return may be considered invalid. It is important to review the entire form before submission to confirm that all required sections are completed, including signatures.

The Georgia 501X form is an important document for fiduciaries filing an amended income tax return in the state. Along with this form, several other documents may be necessary to ensure compliance with state tax regulations. Below is a list of commonly used forms and documents that may accompany the Georgia 501X form.

In conclusion, understanding the various forms and documents that accompany the Georgia 501X form is crucial for fiduciaries. Properly completing and submitting these forms ensures compliance with state tax laws and facilitates the accurate processing of amended returns.

The Georgia Form 501X is an amended fiduciary income tax return. It shares similarities with several other tax-related documents. Below is a list of seven documents that are comparable to the Georgia 501X form, along with explanations of their similarities.

When filling out the Georgia 501X form, it is important to follow certain guidelines to ensure accuracy and compliance. Below are some key dos and don'ts.

Understanding the Georgia Form 501X is essential for fiduciaries managing estates and trusts. However, several misconceptions can lead to confusion. Here are four common myths about this form:

This is incorrect. The Georgia Form 501X is used to amend a fiduciary income tax return, regardless of whether the fiduciary owes taxes or is expecting a refund. It allows for corrections to be made for various reasons, including changes in income or adjustments required by the IRS.

This is a misunderstanding. When filing the Georgia Form 501X, you must attach a copy of the federal amended return. This requirement ensures that the state has the necessary information to process your amendments accurately.

In reality, if there are changes that affect your tax liability or the information reported on your original return, filing the 501X is not optional. It is necessary to ensure compliance with state tax laws and to avoid potential penalties.

This is misleading. There are deadlines for filing the 501X form. Generally, it must be submitted by the 15th day of the fourth month following the close of the taxable year. Late submissions can incur penalties and interest, so timely filing is crucial.

When filling out and using the Georgia 501X form, several important points should be considered to ensure compliance and accuracy.