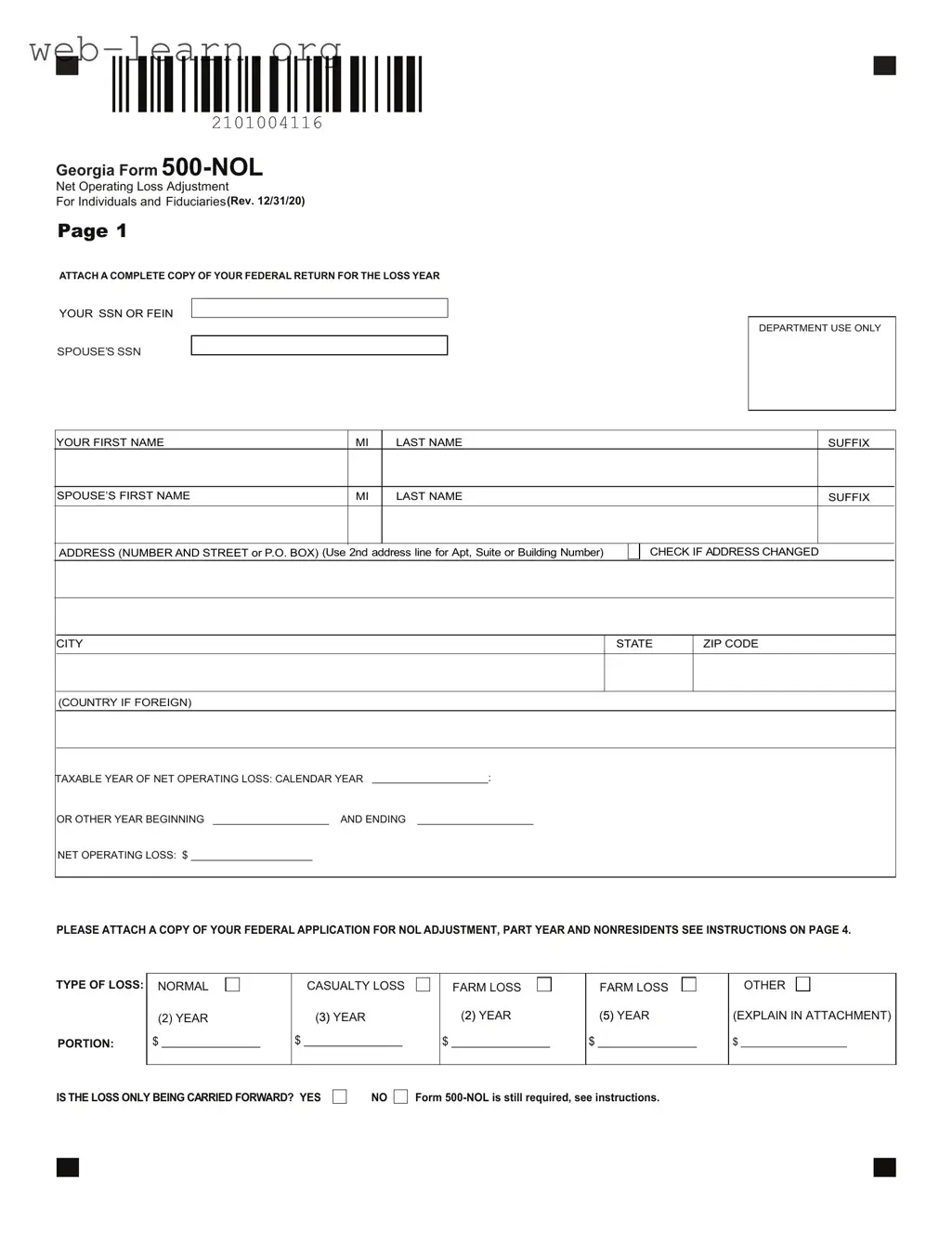

The Georgia Form 500-NOL serves as a crucial tool for individuals and fiduciaries seeking to adjust their net operating losses (NOL) for state tax purposes. This form is essential for those who have incurred a net operating loss and wish to either carry it back to previous tax years for a potential refund or carry it forward to offset future taxable income. The form requires the taxpayer's Social Security Number or Federal Employer Identification Number, along with pertinent personal information, including residency status and filing status. It outlines the taxable year of the loss, the amount of the net operating loss, and specifies whether the loss is being carried forward or back. Taxpayers must provide a complete copy of their federal tax return for the loss year, along with any necessary documentation for carryback years. The form also includes detailed calculations to determine the adjusted gross income, deductions, exemptions, and ultimately, the taxable income. Importantly, taxpayers must adhere to specific guidelines regarding the computation of their Georgia NOL, which may differ from federal calculations. This form must be filed within three years from the due date of the loss year return, including any extensions, making timely submission critical for tax compliance and potential refunds.

| Fact Name | Details |

|---|---|

| Purpose | The Georgia Form 500-NOL is used to adjust net operating losses for individuals and fiduciaries. |

| Governing Law | It is governed by Georgia Code Section 48-1-2 and the Internal Revenue Code Section 172. |

| Filing Deadline | This form must be filed no later than three years from the due date of the loss year income tax return. |

| Carryback Rules | Generally, losses can be carried back two years, but farmers have a five-year carryback period. |

| 80% Limitation | For losses incurred after December 31, 2017, only 80% of Georgia taxable net income can be offset. |

| Required Attachments | Taxpayers must attach a complete copy of their federal return for the loss year. |

| Signature Requirement | Taxpayers must sign the form under penalty of perjury, affirming the accuracy of the information provided. |

Filling out the Georgia Form 500-NOL is an important step for individuals and fiduciaries who have experienced a net operating loss. This form allows taxpayers to adjust their income tax returns based on losses incurred. Properly completing this form ensures that your application is processed smoothly.

After submitting the form, the Georgia Department of Revenue will review your application. They may contact you if any additional information is needed. Be sure to keep copies of everything you submit for your records.

The Georgia Form 500-NOL is used by individuals and fiduciaries to report a net operating loss (NOL) adjustment. This form allows taxpayers to claim a refund of taxes that may be owed due to the carryback of a net operating loss. It is essential for establishing the NOL in the Georgia Department of Revenue’s system, whether the loss is carried back or forward.

Any individual or fiduciary who has incurred a net operating loss and wishes to carry that loss back to offset taxable income from previous years must file this form. It is also necessary for those who only wish to carry the loss forward. The form must be submitted no later than three years from the due date of the loss year income tax return, including any extensions.

When filling out the Georgia Form 500-NOL, taxpayers need to provide various details, including:

Additionally, a complete copy of the federal return for the loss year and any applicable Georgia returns for the carryback or carryforward years must be attached.

Yes, there are specific rules regarding the carryback and carryforward of net operating losses in Georgia. Generally, losses incurred in taxable years ending on or before December 31, 2017, can be carried back for two years. For losses incurred after December 31, 2017, there is no carryback allowed, but losses can be carried forward indefinitely. However, the net operating loss cannot offset more than 80% of Georgia taxable net income in any given year. Taxpayers should also note that Georgia does not follow certain federal provisions related to net operating losses.

Filling out the Georgia Form 500-NOL can be a complex process, and mistakes can lead to delays or denials of your application. Here are ten common errors that individuals often make when completing this form.

One frequent mistake is failing to attach a complete copy of the federal return for the loss year. This document is crucial for the Georgia Department of Revenue to assess your net operating loss accurately. Without it, your application may be incomplete, which could result in rejection.

Another common error is neglecting to specify the correct taxable year of the net operating loss. It's essential to indicate whether the loss occurred in a calendar year or another specified year. Misidentifying this can lead to complications in processing your claim.

Some individuals mistakenly leave out the total amount of the net operating loss. This figure is vital for the calculation of your tax liability and must be clearly stated. Omitting this information can create confusion and may require additional follow-up with the tax department.

Many people also forget to check the box indicating whether the loss is being carried forward only. This detail is important as it informs the department of how to process your application. Failing to check this box can lead to misunderstandings about your intent regarding the loss.

Inaccuracies in reporting the type of loss can also be problematic. Whether it’s a normal loss, casualty loss, or farm loss, it’s important to select the appropriate category. Misclassification can affect the eligibility and calculation of the loss.

Additionally, some applicants do not provide the necessary residency and filing status information. This data is critical for determining your eligibility for the net operating loss adjustment. Without it, the processing of your application may be delayed.

Another mistake involves incorrect calculations in the income and deduction sections. Errors in these calculations can lead to significant discrepancies in your reported taxable income, which can ultimately affect your refund or tax liability.

People often overlook the requirement to include all relevant attachments, such as copies of previous Georgia returns for carryback or carryforward years. Missing documents can lead to an incomplete application, which may result in disallowance.

Some individuals also fail to sign the form or provide the necessary contact information. A missing signature can render the application invalid, and without proper contact details, the department may struggle to reach you for clarification or additional information.

Lastly, failing to keep copies of all submitted documents can create issues down the line. It's wise to maintain records of everything you send to the Georgia Department of Revenue, as these can be useful for future reference or if questions arise about your application.

By being aware of these common mistakes, individuals can better prepare their Georgia Form 500-NOL applications and increase the likelihood of a smooth processing experience.

The Georgia Form 500-NOL is an important document for individuals and fiduciaries seeking to adjust their net operating losses for state tax purposes. Alongside this form, several other documents are commonly used to ensure accurate reporting and compliance with Georgia tax regulations. Below is a list of these documents, each described briefly to provide clarity on their purpose and relevance.

These documents collectively support the accurate filing and adjustment of net operating losses in Georgia. It is crucial to ensure that all required forms are completed and submitted correctly to avoid any potential issues with the state tax authority. Proper documentation facilitates a smooth process for taxpayers seeking to manage their tax obligations effectively.

The Georgia Form 500-NOL is similar to several other tax documents. Here are four documents that share similarities:

When filling out the Georgia Form 500-NOL, it's essential to approach the task with care. Below is a list of important dos and don'ts to ensure that the form is completed accurately and efficiently.

Here are seven common misconceptions about the Georgia Form 500-NOL:

Even if you are only carrying the loss forward, you still need to file Form 500-NOL. This helps establish the loss in the state's system.

Georgia and Federal NOLs are calculated separately. You can have a Federal NOL but not a Georgia NOL, or vice versa.

The carryback period is limited. Generally, for losses incurred after December 31, 2017, there is no carryback, except for farmers who may have a two-year carryback.

For losses incurred in taxable years beginning on or after January 1, 2018, the NOL cannot offset more than 80% of Georgia taxable net income.

A complete copy of your federal return for the loss year must be attached when filing the Georgia Form 500-NOL.

When calculating your Georgia NOL, only Georgia amounts can be used. Adjustments for non-Georgia sources are necessary.

Form 500-NOL must be filed no later than three years from the due date of the loss year return. Late filings may result in disallowance of your claim.

Understand the Purpose: The Georgia Form 500-NOL is used to adjust your net operating loss for state tax purposes. This form is essential for individuals and fiduciaries who want to claim a refund for taxes due to a net operating loss carryback.

Attach Required Documents: When submitting the form, make sure to include a complete copy of your federal return for the loss year, along with any necessary schedules. Missing documents can lead to delays or disallowance of your application.

Know the Filing Deadline: This form must be filed no later than three years from the due date of the loss year income tax return. Be mindful of extensions, as they can affect your deadline.

Carryforward and Carryback Rules: Generally, net operating losses can be carried back two years and carried forward up to 20 years. However, specific rules apply, especially for farmers and casualty losses, so it’s important to understand how these rules affect your situation.