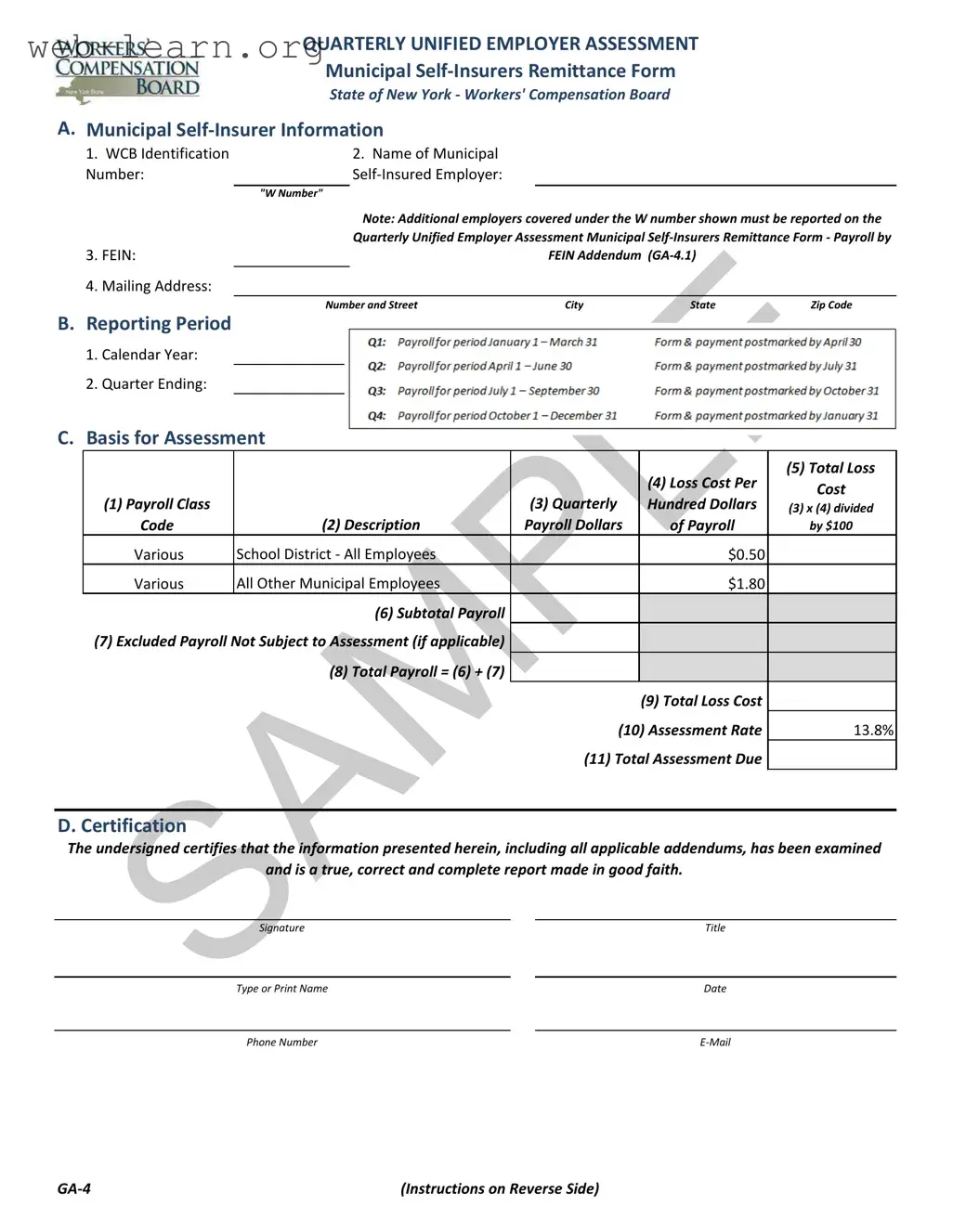

The Quarterly Unified Employer Assessment Municipal Self-Insurers Remittance Form, commonly referred to as the GA-4, serves as a critical tool for municipal self-insured employers in New York. This form must be completed each quarter and submitted within thirty days following the end of the quarter. It captures essential information about the municipal self-insurer, including the WCB Identification Number, the full legal name of the employer, and the Federal Employer Identification Number (FEIN). The form also requires details regarding the reporting period, payroll classifications, and the basis for assessment, which includes total payroll figures and loss costs. Municipal employers, such as school districts and other municipal entities, must report their payroll separately to ensure accurate assessments. The total assessment due is calculated based on a specified assessment rate applied to the total loss cost, which is derived from the reported payroll figures. In addition, if multiple employers are covered under a single W number, the Payroll by FEIN Addendum (GA-4.1) must accompany the GA-4 form. This structured approach helps maintain transparency and accountability in the self-insurance process, ensuring that municipal employers fulfill their financial obligations while adhering to regulatory requirements.

| Fact Name | Fact Description |

|---|---|

| Form Purpose | The GA-4 form is used for the Quarterly Unified Employer Assessment for municipal self-insurers in New York. |

| Governing Law | This form is governed by the New York Workers' Compensation Law (WCL) Section 151. |

| Submission Frequency | Municipal self-insured employers must submit the GA-4 form quarterly, within thirty days after the end of each quarter. |

| WCB Identification | Each municipal self-insurer is assigned a unique WCB Identification Number, commonly referred to as the "W Number." |

| Payroll Reporting | Payroll must be reported separately for school districts and all other municipal employees, using specific loss cost rates. |

| Payment Instructions | Payments are to be made via check, payable to the Chair of the NYS Workers' Compensation Board. |

| Excluded Payroll | Employers can report excluded payroll not subject to assessment, if applicable. |

| Certification Requirement | The form requires a certification from the undersigned, confirming the accuracy and completeness of the information provided. |

| Audit Provisions | The Chair of the Workers' Compensation Board may conduct audits to verify the accuracy of reported information. |

| Penalties for Non-Compliance | Failure to submit timely assessments may result in penalties, including interest on underpaid assessments and potential revocation of self-insured status. |

Completing the GA-4 New York form is an important step for municipal self-insured employers to report their assessments. This form must be filled out accurately and submitted on time to ensure compliance with state regulations. The following steps outline how to properly fill out the form.

Once the form is completed, it should be submitted along with payment within thirty days of the quarter's end. Ensure that you include the W Number and applicable quarter on your check. If there are any additional employers covered under the same W Number, use the GA-4.1 addendum to report their payroll as well.

What is the GA-4 form?

The GA-4 form, or Quarterly Unified Employer Assessment Municipal Self-Insurers Remittance Form, is a document that municipal self-insured employers in New York must complete each quarter. It is used to report payroll information and calculate assessments for workers' compensation.

Who needs to file the GA-4 form?

Every active municipal self-insured employer is required to file the GA-4 form. This includes school districts and other municipal employers. If an employer has discontinued its self-insurance program, they do not need to submit this form.

When is the GA-4 form due?

The form must be submitted within thirty days of the end of each quarter. It is essential to adhere to this deadline to avoid penalties and ensure compliance with New York State regulations.

What information is required on the GA-4 form?

Each section must be filled out accurately to ensure proper assessment calculations.

How is the assessment amount calculated?

The assessment is calculated based on the total payroll reported, multiplied by the established assessment rate. For municipal employers, the assessment rate is currently set at 13.8%.

What should I do if I have multiple employers under one W number?

If there are multiple employers covered under the same W number, you must use the GA-4.1 addendum. This addendum allows you to report payroll information for each employer separately.

Where do I send the completed GA-4 form?

You can submit the completed GA-4 form via email to [email protected]. Additionally, you should mail the corresponding payment to:

New York State Workers’ Compensation Board

328 State Street

Finance Unit, Room 331

Schenectady, NY 12305-2318

What happens if I fail to submit the GA-4 form on time?

Failure to submit the form and payment on time may result in penalties, including interest charges on underpaid assessments. In severe cases, it could lead to the revocation of self-insured status.

Filling out the GA-4 New York form can be a straightforward task, but there are common mistakes that individuals often make. One frequent error is neglecting to include the WCB Identification Number or "W Number." This number is crucial as it uniquely identifies the municipal self-insurer. Without it, the form may be deemed incomplete, leading to potential delays in processing.

Another mistake is failing to provide the full legal name of the municipal self-insured employer. This name should match exactly with the records on file with the Workers' Compensation Board. Any discrepancies can cause confusion and may result in additional follow-up or corrections that could have been easily avoided.

People sometimes forget to report the Federal Employer Identification Number (FEIN). This number is essential for identifying the employer for tax purposes. Omitting it can lead to complications and might even result in penalties. It’s important to double-check that this number is accurate and clearly written.

Additionally, some individuals overlook the requirement to report excluded payroll not subject to assessment. If applicable, this information must be included to ensure that the total payroll is accurately calculated. Neglecting this step can skew the assessment results and lead to incorrect payments.

Another common oversight is not reconciling the total payroll reported on the GA-4 form with that on the NYS-45. If there are discrepancies, it is necessary to provide a reconciliation. Failing to do so can raise red flags during audits and complicate future submissions.

People also tend to miscalculate the total loss cost by failing to apply the correct assessment rate. This calculation is vital for determining the total assessment due. A simple math error can lead to underpayment or overpayment, both of which can have financial repercussions.

Moreover, some individuals do not submit the form and payment within the required thirty-day timeframe after the quarter ends. Late submissions can incur penalties and interest, which can add unnecessary costs. Staying organized with deadlines is key to avoiding this mistake.

Lastly, individuals sometimes forget to include their signature and the date on the certification section of the form. This certification is a declaration that the information provided is true and accurate. Without it, the form may not be accepted, leading to further delays.

By being mindful of these common pitfalls, individuals can ensure that their GA-4 New York form is filled out correctly, avoiding unnecessary complications and ensuring compliance with the Workers' Compensation Board requirements.

The GA-4 New York form, known as the Quarterly Unified Employer Assessment Municipal Self-Insurers Remittance Form, is essential for municipal self-insured employers in New York. It ensures that these employers report their payroll and pay the necessary assessments on a quarterly basis. Alongside the GA-4, there are several other forms and documents that are often used to provide additional information or fulfill reporting requirements. Below is a brief overview of four such documents.

Understanding these accompanying forms and documents is vital for municipal self-insured employers in New York. Proper completion and submission of these materials help ensure compliance with state regulations and avoid potential penalties. By staying informed and organized, employers can manage their self-insurance obligations effectively.

Things You Should Do:

Things You Shouldn't Do:

Misconception 1: The GA-4 form is optional for municipal self-insurers.

This is incorrect. Every active municipal self-insured employer must complete the GA-4 form each quarter. Submitting this form is a requirement, not a choice.

Misconception 2: Only large municipalities need to file the GA-4 form.

In reality, all municipal self-insured employers, regardless of size, must submit the GA-4 form. This includes small towns and local districts.

Misconception 3: The GA-4 form does not require supporting documentation.

This is misleading. While the form itself is critical, it must be accompanied by supporting documentation, such as payroll records and any applicable addendums, to ensure accurate reporting.

Misconception 4: The due date for submitting the GA-4 form is flexible.

This is false. The form must be submitted within thirty days of the end of each quarter. Late submissions can lead to penalties and interest charges.

Misconception 5: The assessment rate is the same every year.

This is not true. The assessment rate can change annually based on decisions made by the Chair of the Workers' Compensation Board. It is essential to check for updates each year.

Filling out and using the GA-4 New York form is an essential process for municipal self-insurers. Here are some key takeaways to keep in mind: