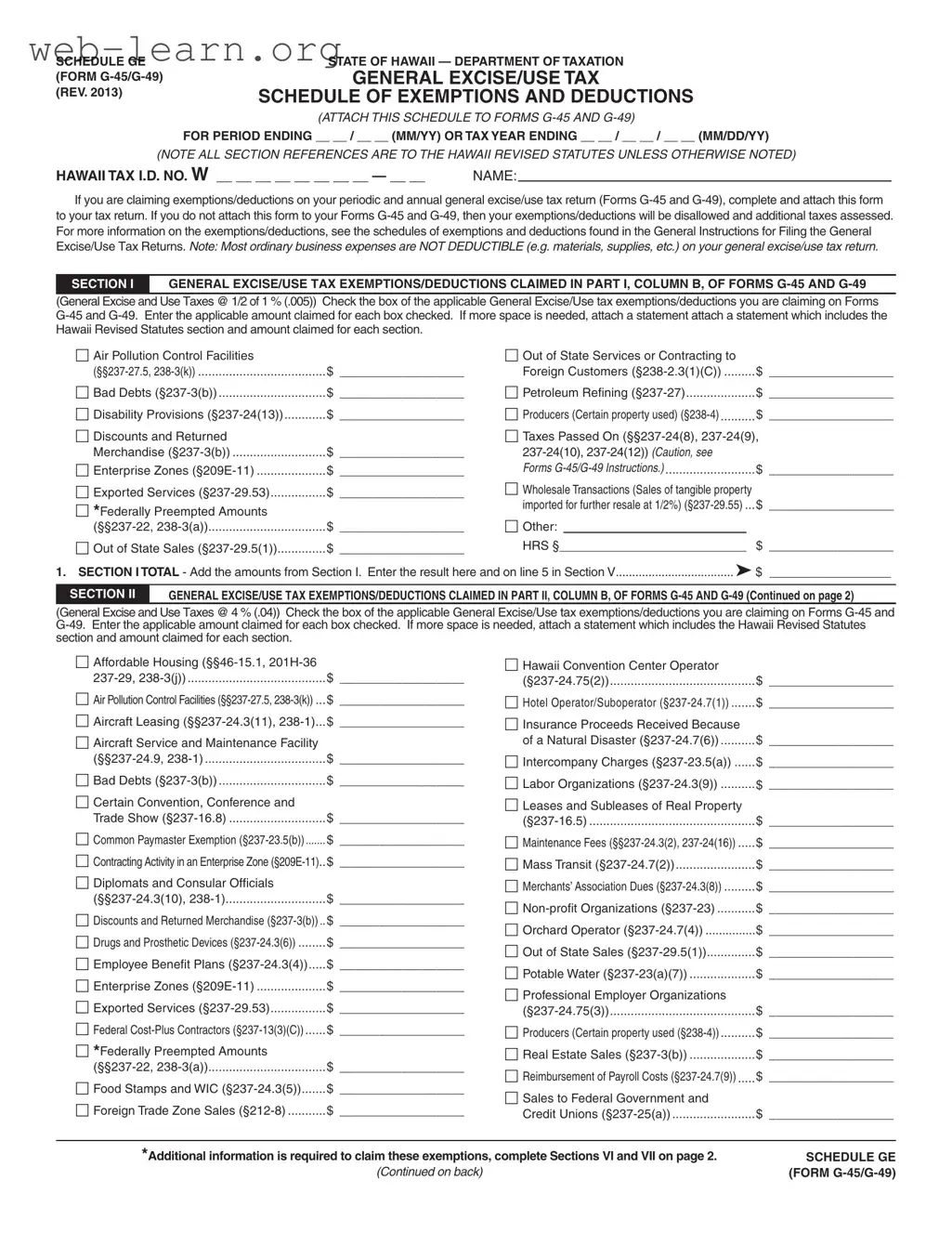

The G 45 Hawaii form serves as a crucial document for businesses operating in the state, particularly for those navigating the complexities of general excise and use tax obligations. This form is not merely a collection of numbers; it is a structured schedule that allows taxpayers to claim various exemptions and deductions that can significantly impact their tax liabilities. Each section of the form is meticulously designed to capture specific types of exemptions, ranging from air pollution control facilities to bad debts and exported services. Taxpayers must complete this form with precision, as failing to attach it to the periodic and annual returns—Forms G-45 and G-49—will result in the disallowance of claimed exemptions, leading to additional tax assessments. The form also outlines the importance of understanding which ordinary business expenses are not deductible under Hawaii law, thereby guiding taxpayers toward compliant and effective tax reporting. By providing detailed instructions and clear categories for exemptions, the G 45 Hawaii form aims to streamline the tax filing process while ensuring that businesses can take full advantage of the tax relief options available to them.

| Fact Name | Details |

|---|---|

| Purpose | The G-45 Hawaii form is used to claim exemptions and deductions related to general excise/use tax. |

| Governing Law | The form is governed by the Hawaii Revised Statutes (HRS), particularly sections 237 and 238. |

| Filing Requirement | This form must be attached to Forms G-45 and G-49 to validate claimed exemptions/deductions. |

| Consequences of Non-Compliance | If the form is not attached, exemptions and deductions will be disallowed, resulting in additional taxes. |

| Exemptions/Deductions | Various exemptions are available, including those for out-of-state services and bad debts. |

| Section I | Section I lists exemptions claimed at a rate of 0.5% for general excise/use tax. |

| Section II | Section II includes exemptions at a rate of 4%, such as for affordable housing and mass transit. |

| Section III | Section III addresses exemptions specifically for insurance commissions, taxed at 0.15%. |

| County Surcharge | Section IV includes exemptions for the county surcharge tax, applicable at a rate of 0.5%. |

| Additional Information | Sections VI and VII require further information for federally preempted amounts and subcontract deductions. |

Filling out the G-45 form for Hawaii requires careful attention to detail. This form is essential for claiming exemptions and deductions related to general excise and use taxes. Ensure that all necessary information is accurate and complete to avoid any issues with your tax return.

The G-45 form is a tax return used for reporting general excise and use taxes in Hawaii. It is typically filed by businesses operating in the state. The form helps businesses claim exemptions and deductions for certain activities or expenses that qualify under Hawaii tax laws. To ensure proper processing, the G-45 must be completed accurately and submitted on time.

If you fail to attach the G-45 form to your periodic or annual tax return (Forms G-45 and G-49), your claimed exemptions and deductions will be disallowed. This means that you may face additional taxes assessed by the Department of Taxation. It is crucial to include this form to validate your claims and avoid potential penalties.

The G-45 form allows you to claim various exemptions and deductions. Some common categories include:

Each exemption has specific criteria, so it is essential to review the instructions carefully and ensure that you qualify for any deductions you claim.

Yes, the G-45 form must be filed periodically, typically on a quarterly basis, depending on your business's tax liability. The specific deadlines can vary, so it is advisable to check the latest guidelines from the Hawaii Department of Taxation to ensure timely submission and compliance.

Filling out the G-45 Hawaii form can be a straightforward process, but many individuals make common mistakes that can lead to complications. One significant error is failing to attach the required Schedule GE. This schedule is essential for claiming exemptions and deductions. Without it, the tax authorities will disallow these claims, resulting in additional taxes owed. Always ensure that this form is completed and attached to your G-45 and G-49 submissions.

Another frequent mistake is neglecting to check the appropriate boxes for exemptions and deductions claimed. It's crucial to review the list carefully and ensure that all relevant boxes are marked. If you miss a box, you may miss out on potential savings. Additionally, entering the claimed amounts incorrectly can lead to discrepancies and further complications. Double-check the figures before submitting the form.

Many people also overlook the importance of including the correct Hawaii Tax I.D. number. This number is vital for identifying your business and ensuring that your tax return is processed accurately. If this number is missing or incorrect, it can delay your return and lead to unnecessary confusion. Always verify that your Hawaii Tax I.D. is accurate and clearly written on the form.

Lastly, failing to provide additional information when claiming federally preempted amounts or subcontract deductions is a common oversight. Specific details are required for these claims, and not providing them can result in disqualification of the deductions. Make sure to complete Sections VI and VII thoroughly if these situations apply to you. Taking the time to avoid these mistakes can save you from future headaches and ensure a smoother filing process.

The G-45 form is an essential document for businesses in Hawaii to report their general excise and use taxes. When completing this form, several other documents may also be required to ensure accurate reporting and compliance with tax regulations. Below is a list of forms and documents that are commonly used alongside the G-45 form.

Using these forms in conjunction with the G-45 ensures that businesses maintain compliance with Hawaii's tax regulations. Proper documentation can help avoid penalties and ensure that all eligible deductions are accurately claimed.

The G-45 Hawaii form, used for reporting general excise and use tax exemptions and deductions, has several similar documents that serve related purposes in tax reporting and compliance. Below is a list of these documents, along with a brief explanation of how they are similar to the G-45 form:

Understanding these forms and their similarities can help ensure accurate reporting and compliance with Hawaii's tax regulations. Each document plays a crucial role in ensuring that taxpayers can appropriately claim their exemptions and deductions.

When filling out the G-45 Hawaii form, there are important guidelines to follow. Here are four things to keep in mind:

The G-45 Hawaii form is an important document for businesses operating in Hawaii, but several misconceptions surround its use. Understanding these misconceptions can help ensure compliance and proper filing.

Many people believe that all business expenses can be deducted on the G-45 form. However, most ordinary business expenses, such as materials and supplies, are not deductible. Only specific exemptions and deductions listed in the form are allowed.

Some individuals think they can submit the G-45 form without attaching the necessary documentation for exemptions and deductions. In reality, if the required schedule of exemptions and deductions is not attached, those claims will be disallowed, leading to additional taxes.

It is a common belief that filing the G-45 form is optional. In fact, businesses that earn income in Hawaii are required to file this form to report their general excise and use taxes. Failure to file can result in penalties and interest on unpaid taxes.

Many assume that only large businesses or corporations need to file the G-45. However, any business entity earning income in Hawaii, regardless of size, must file this form. This includes sole proprietors, partnerships, and small businesses.

Filling out the G-45 Hawaii form accurately is essential for claiming exemptions and deductions on general excise and use taxes. Here are key takeaways to keep in mind: