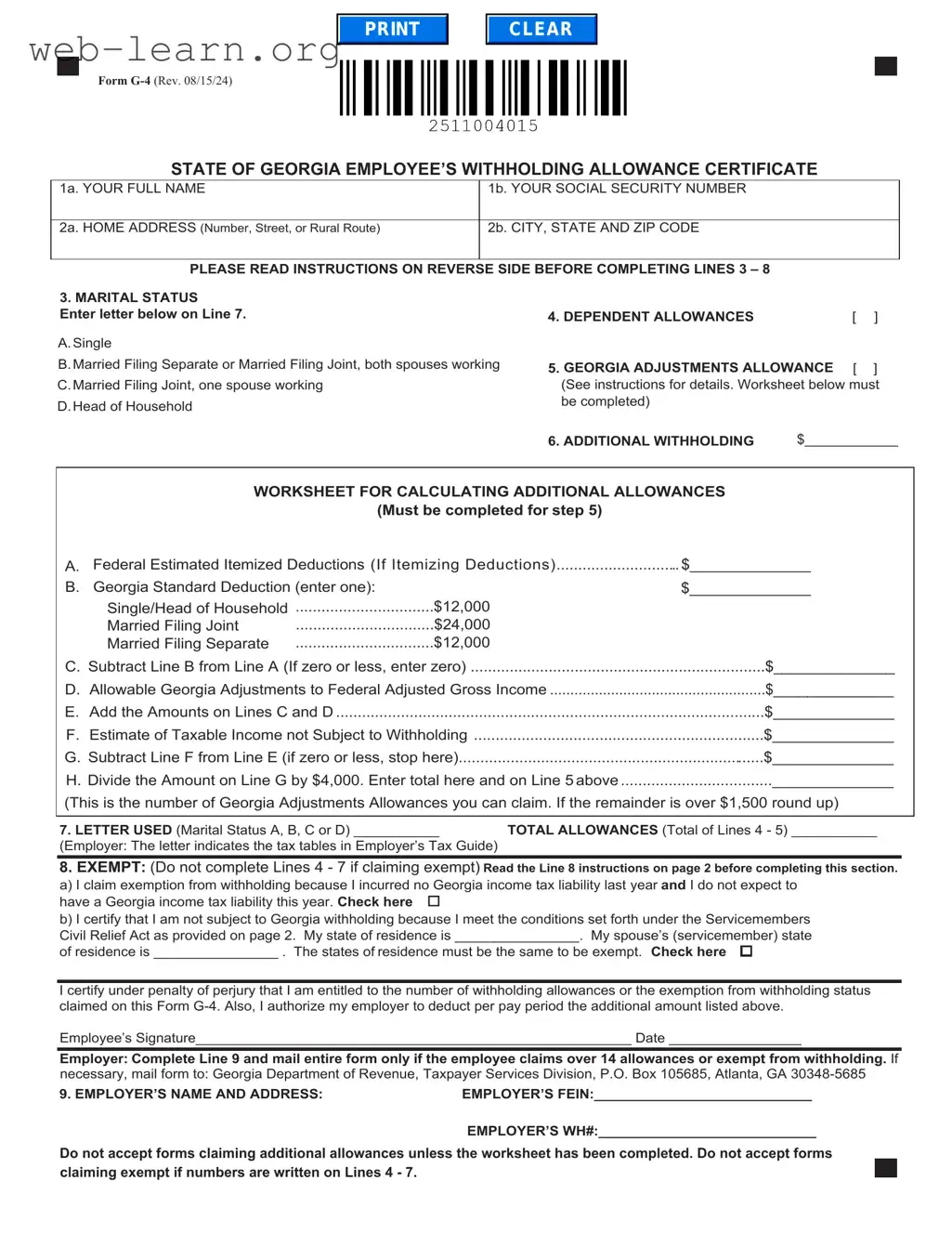

The G-4 Georgia form is a critical document for employees in the state of Georgia, as it determines how much state income tax is withheld from their paychecks. This form requires individuals to provide essential personal information, including their full name, social security number, and home address. Employees must also indicate their marital status, which affects their withholding allowances. The form allows for the declaration of dependent allowances and additional allowances that can be calculated using a worksheet provided within the form itself. This worksheet helps employees estimate their tax liability more accurately, ensuring that the correct amount is withheld throughout the year. Furthermore, the G-4 includes provisions for individuals who may qualify for exemption from withholding, such as those with no tax liability in the previous year or military spouses under specific conditions. Completing the G-4 accurately is essential; failure to do so may result in the default withholding rate being applied, which is typically the highest rate for single individuals claiming zero allowances. Understanding the nuances of this form can lead to better financial planning and potentially higher take-home pay for employees.

| Fact Name | Description |

|---|---|

| Form Purpose | The G-4 form is used in Georgia to determine the amount of state income tax withheld from an employee's paycheck. |

| Governing Law | This form is governed by O.C.G.A. § 48-7-102, which outlines the requirements for withholding taxes in Georgia. |

| Employee Information | Employees must provide their full name, social security number, and home address on the form. |

| Marital Status Options | Employees can select their marital status from options such as Single, Married Filing Joint, Married Filing Separate, or Head of Household. |

| Dependent Allowances | Employees may claim dependent allowances based on the number of dependents they have, which can affect their withholding amount. |

| Additional Allowances | Employees can claim additional allowances by completing a worksheet, which allows for more accurate tax withholding based on their situation. |

| Exemption Criteria | Employees may claim exemption from withholding if they had no Georgia income tax liability in the previous year and expect none for the current year. |

| Servicemembers Relief Act | Under certain conditions, spouses of servicemembers may be exempt from Georgia withholding tax as per the Servicemembers Civil Relief Act. |

| Submission Requirements | Employers must mail the G-4 form to the Georgia Department of Revenue if an employee claims more than 14 allowances or is exempt from withholding. |

Completing the G-4 form is essential for determining the amount of state income tax withheld from your paycheck. Follow these steps carefully to ensure accurate completion.

After submitting the form, your employer will adjust your withholding based on the information provided. It’s important to keep a copy for your records and monitor your paychecks to ensure the correct amount is being withheld.

What is the G-4 form?

The G-4 form is the Employee’s Withholding Allowance Certificate for the state of Georgia. It allows employees to indicate their marital status and the number of allowances they wish to claim for state income tax withholding. This form helps determine how much tax will be withheld from an employee's paycheck.

Who needs to fill out the G-4 form?

Any employee working in Georgia who wants to adjust their state income tax withholding must complete the G-4 form. This includes new hires, employees who wish to change their withholding status, and those claiming exemption from withholding.

How do I determine my marital status for the G-4 form?

Marital status options on the G-4 form include:

Choose the status that accurately reflects your situation and enter the corresponding number of allowances in the brackets provided.

What if I have dependents?

If you have dependents, you can claim additional allowances for them on Line 4 of the G-4 form. Make sure to enter the correct number of dependent allowances you are entitled to claim.

What is the purpose of the worksheet on the G-4 form?

The worksheet helps you calculate any additional allowances you may claim. You must complete this worksheet if you wish to enter an amount on Line 5. Failing to do so will result in your claim being denied.

Can I claim exempt from withholding?

You can claim exempt from withholding if you had no Georgia income tax liability last year and expect none this year. Additionally, if you meet the conditions under the Servicemembers Civil Relief Act, you may also qualify for exemption. Be sure to check the appropriate box on Line 8 if you meet these criteria.

What happens if I don’t submit the G-4 form?

If you do not submit a properly completed G-4 form, your employer will withhold taxes as if you are single with zero allowances. This may result in higher withholding than necessary.

How long is the G-4 form valid?

The G-4 form remains in effect until you change it or until February 15 of the following year. If your circumstances change, you should submit a new form to your employer to update your withholding status.

Where do I send the G-4 form?

Once completed, submit the G-4 form to your employer. If you are claiming more than 14 allowances or are exempt from withholding, your employer must mail the form to the Georgia Department of Revenue, Taxpayer Services Division, at the address provided on the form.

Filling out the G-4 Georgia form can be straightforward, but many people make common mistakes that can affect their tax withholding. One frequent error is failing to complete the worksheet for calculating additional allowances. If you claim additional allowances on Line 5 without filling out the worksheet, your employer will automatically deny your claim. This oversight can lead to higher tax withholding than necessary, impacting your take-home pay.

Another mistake involves misunderstanding marital status options. When selecting a marital status on Line 3, individuals sometimes enter the wrong number of allowances. For example, a married person may mistakenly claim allowances for "Single" or choose an incorrect number for "Married Filing Joint." This can result in incorrect tax withholding, leading to either underpayment or overpayment of taxes throughout the year.

People also often neglect to check the exemption box on Line 8 correctly. To claim exemption, you must have had no tax liability in the previous year and expect none in the current year. Misunderstanding these requirements can lead to claiming exempt status incorrectly. If you do not meet the criteria but claim exempt, your employer will not withhold any taxes, which may result in a tax bill when you file your return.

Finally, a common oversight is failing to provide accurate personal information. Missing or incorrect details, such as your full name, social security number, or address, can cause delays in processing your form. Employers need accurate information to ensure proper withholding. Double-checking these details before submission can help avoid unnecessary complications.

The G-4 Georgia form is essential for employees to declare their withholding allowances for state income tax purposes. Alongside this form, various other documents may be required or beneficial for accurate tax processing and compliance. Below is a list of related forms and documents that are often used in conjunction with the G-4 form.

Understanding these documents and their purposes can greatly assist employees in managing their tax responsibilities effectively. It is advisable to consult with a tax professional if there are questions regarding any of these forms or the withholding process.

The G-4 Georgia form serves as an Employee’s Withholding Allowance Certificate, allowing individuals to claim withholding allowances for state income tax purposes. There are several other documents that share similarities with the G-4 form, primarily in their function of determining tax withholding amounts. Below is a list of documents that are comparable to the G-4 form, along with explanations of their similarities.

Understanding these documents can provide clarity on how withholding allowances are calculated and reported, ensuring that individuals meet their tax obligations effectively.

When filling out the G-4 Georgia form, it’s essential to follow certain guidelines to ensure accuracy and compliance. Here’s a helpful list of things you should and shouldn’t do:

Following these simple dos and don’ts can make the process smoother and help avoid potential issues with your tax withholding. Remember, accuracy is key!

Here are seven common misconceptions about the G-4 Georgia form:

When filling out and using the G-4 Georgia form, keep these key takeaways in mind: