The Florida Promissory Note is an essential financial document that outlines the terms of a loan agreement between a borrower and a lender. This form serves as a written promise from the borrower to repay the borrowed amount, known as the principal, along with any agreed-upon interest, within a specified timeframe. Key components of the note include the names and addresses of both parties, the loan amount, the interest rate, and the payment schedule. Additionally, it may detail the consequences of default, such as late fees or legal action, and can include provisions for prepayment. Understanding these elements is crucial for anyone entering into a lending arrangement in Florida, as it ensures clarity and protects the rights of both parties involved.

Florida Promissory Note Template

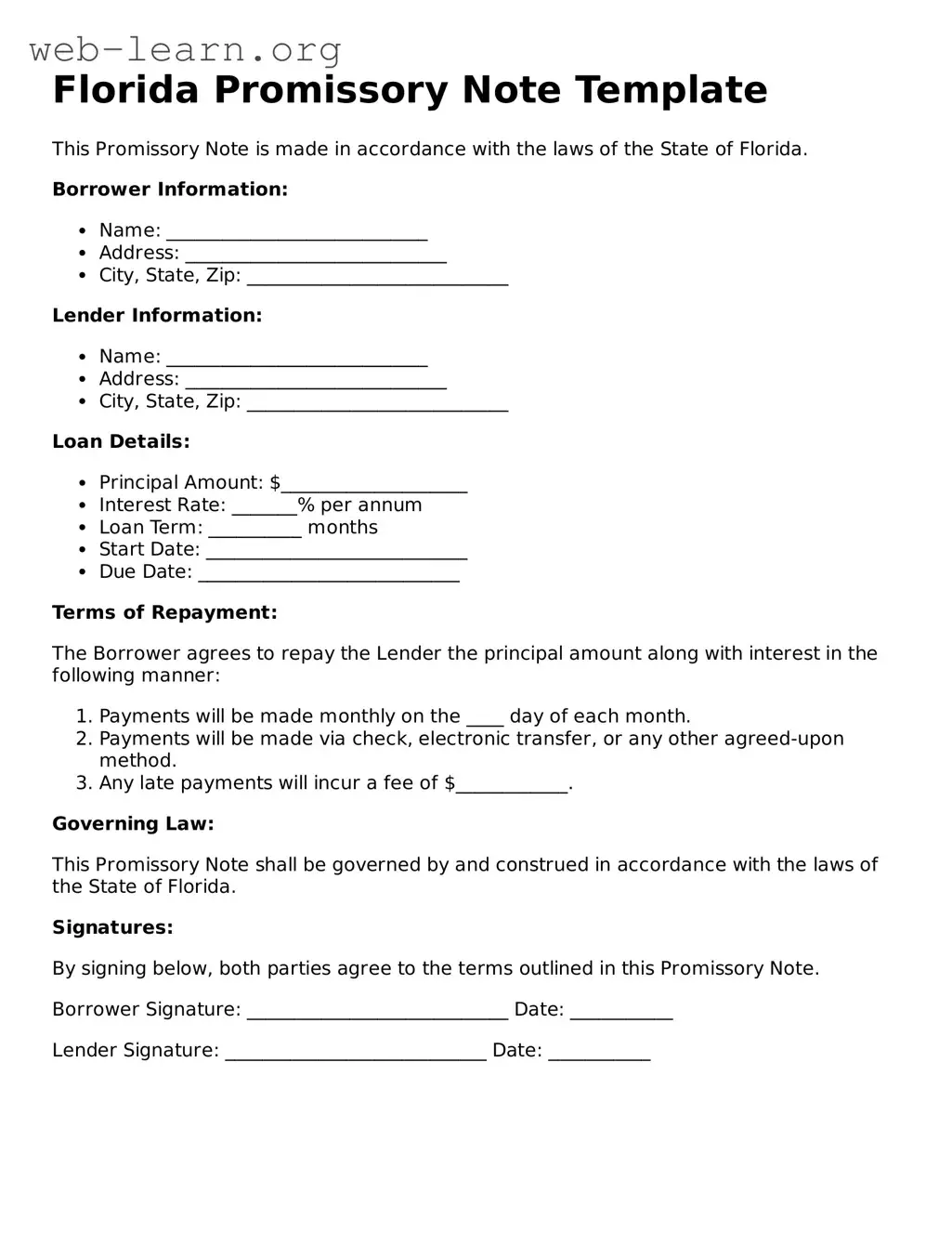

This Promissory Note is made in accordance with the laws of the State of Florida.

Borrower Information:

Lender Information:

Loan Details:

Terms of Repayment:

The Borrower agrees to repay the Lender the principal amount along with interest in the following manner:

Governing Law:

This Promissory Note shall be governed by and construed in accordance with the laws of the State of Florida.

Signatures:

By signing below, both parties agree to the terms outlined in this Promissory Note.

Borrower Signature: ____________________________ Date: ___________

Lender Signature: ____________________________ Date: ___________

| Fact Name | Description |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money to a designated person or entity at a defined future date or on demand. |

| Governing Law | The Florida Promissory Note is governed by the Florida Uniform Commercial Code (UCC), specifically under Chapter 673. |

| Parties Involved | The note typically involves two parties: the borrower (maker) who promises to pay, and the lender (payee) who is entitled to receive the payment. |

| Interest Rate | Interest can be specified in the note, and it must comply with Florida's usury laws to ensure it is not excessively high. |

| Payment Terms | Payment terms should clearly outline the schedule, whether it's a lump sum, installments, or on demand. |

| Default Clause | A default clause may be included, detailing the consequences if the borrower fails to make payments as agreed. |

| Signatures | Both parties must sign the note for it to be legally binding. In some cases, notarization is recommended. |

| Transferability | Promissory notes can be transferred to another party unless restricted by the terms of the note itself. |

| Enforcement | If the borrower defaults, the lender has the right to pursue legal action to enforce the terms of the note. |

After obtaining the Florida Promissory Note form, you will need to fill it out accurately. This document is essential for establishing the terms of a loan agreement between the lender and the borrower. Follow these steps to complete the form correctly.

A Florida Promissory Note is a legal document that outlines a borrower's promise to repay a loan to a lender. This document specifies the amount borrowed, the interest rate, repayment schedule, and any other terms agreed upon by both parties. It serves as a written record of the debt and can be enforced in court if necessary.

Key components typically include:

Yes, a properly executed Florida Promissory Note is legally binding. It creates an enforceable obligation for the borrower to repay the loan according to the terms outlined in the document. If the borrower fails to meet these obligations, the lender has the right to take legal action to recover the owed amount.

While it is not legally required to have a lawyer draft a Florida Promissory Note, it is often advisable. A legal professional can ensure that the document meets all state requirements and adequately protects the interests of both parties. If the loan amount is significant or if there are complex terms involved, seeking legal assistance can help prevent future disputes.

Filling out a Florida Promissory Note form requires careful attention to detail. One common mistake people make is leaving out essential information. Failing to include the names of both the borrower and lender can lead to confusion and potential legal issues. It is crucial to ensure that all parties involved are clearly identified.

Another frequent error is not specifying the loan amount. Without a clearly stated sum, the note may be deemed incomplete. This omission can complicate the repayment process and create disputes later on. Always double-check that the amount is clearly written and easy to read.

People often neglect to include the interest rate, which is a vital component of any promissory note. If the interest rate is omitted, it can lead to misunderstandings about the terms of repayment. It is advisable to clearly state whether the interest is fixed or variable and to specify the exact percentage.

Dates are another area where mistakes commonly occur. Failing to indicate the date the note is signed or the repayment due date can create ambiguity. Accurate dating helps establish a timeline for repayment and can be critical in case of default.

Some individuals make the mistake of not outlining the repayment schedule. A vague repayment plan can lead to confusion about when payments are due. Clearly detailing the payment frequency—whether monthly, quarterly, or otherwise—can help prevent misunderstandings.

Another common error is not including a default clause. This clause outlines the consequences if the borrower fails to make payments. Without this provision, lenders may find it difficult to enforce their rights in case of non-payment.

People sometimes forget to sign the document. A promissory note without signatures from both parties is not legally binding. Ensure that all required signatures are present to validate the agreement.

Lastly, many overlook the importance of having the note witnessed or notarized. While not always required, having a witness or notary can add an extra layer of protection and legitimacy to the document. This step can be especially important in disputes or if the note needs to be enforced in court.

When entering into a loan agreement in Florida, a Promissory Note is often accompanied by various other documents. Each of these documents serves a specific purpose and helps to clarify the terms of the agreement, protect the interests of both parties, and ensure compliance with state laws. Below is a list of common forms and documents that are typically used alongside a Florida Promissory Note.

Understanding these documents can help both borrowers and lenders navigate the complexities of loan agreements more effectively. Each form plays a critical role in ensuring that the terms of the Promissory Note are clear, enforceable, and protect the interests of all parties involved.

When filling out the Florida Promissory Note form, it is essential to approach the task with care and attention to detail. Here are some important dos and don'ts to keep in mind:

Understanding the Florida Promissory Note form is essential for anyone involved in lending or borrowing money in the state. However, several misconceptions can lead to confusion. Here are ten common misunderstandings:

Being aware of these misconceptions can help individuals navigate the complexities of promissory notes more effectively. Understanding the correct information is key to protecting your rights and ensuring a smooth lending process.

When filling out and using the Florida Promissory Note form, it is essential to understand several key aspects. Below are important takeaways to consider:

Understanding these components will help ensure that the Promissory Note is properly executed and enforceable in Florida.

Promissory Note Friendly Loan Agreement Format - Borrowers should carefully review the terms of the note to understand their obligations.

Basic Promissory Note - The terms of repayment can vary, including options for lump-sum payments or installment plans.