Navigating financial agreements can sometimes feel overwhelming, especially when it comes to loans. The Florida Loan Agreement form serves as a crucial tool for defining the terms of lending between parties. This document outlines key aspects such as loan amounts, repayment schedules, interest rates, and consequences for default. Clarity and transparency are essential, which is why this form details the responsibilities of both the lender and the borrower. Understanding when payments are due, what happens in case of late payments, and any potential fees is vital for a smooth transaction. Additionally, the form may include provisions for collateral, securing the loan with specific assets. For both individuals and businesses, having a well-structured Loan Agreement in Florida is fundamental to establishing a trustworthy financial relationship and protecting everyone’s interests involved in the agreement.

Florida Loan Agreement

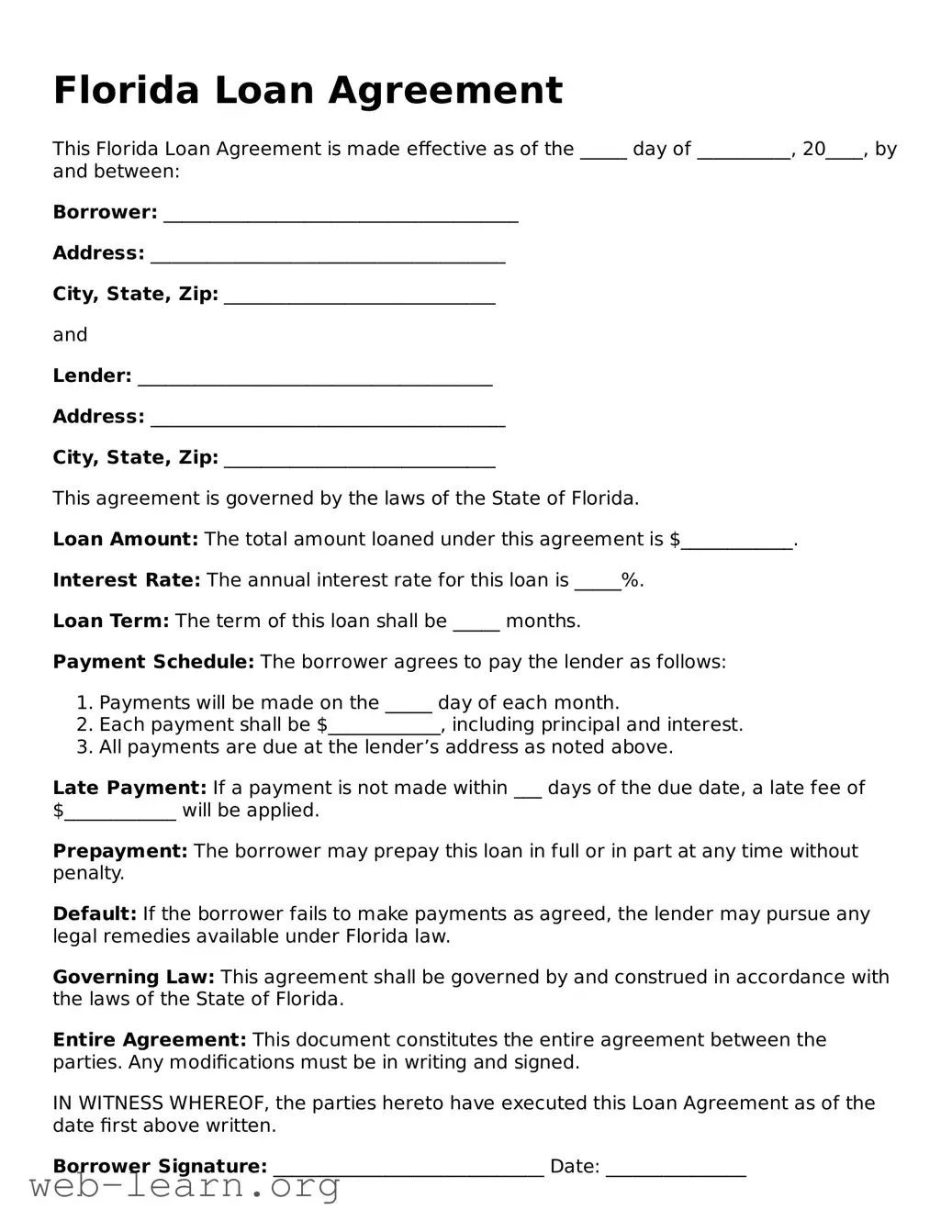

This Florida Loan Agreement is made effective as of the _____ day of __________, 20____, by and between:

Borrower: ______________________________________

Address: ______________________________________

City, State, Zip: _____________________________

and

Lender: ______________________________________

Address: ______________________________________

City, State, Zip: _____________________________

This agreement is governed by the laws of the State of Florida.

Loan Amount: The total amount loaned under this agreement is $____________.

Interest Rate: The annual interest rate for this loan is _____%.

Loan Term: The term of this loan shall be _____ months.

Payment Schedule: The borrower agrees to pay the lender as follows:

Late Payment: If a payment is not made within ___ days of the due date, a late fee of $____________ will be applied.

Prepayment: The borrower may prepay this loan in full or in part at any time without penalty.

Default: If the borrower fails to make payments as agreed, the lender may pursue any legal remedies available under Florida law.

Governing Law: This agreement shall be governed by and construed in accordance with the laws of the State of Florida.

Entire Agreement: This document constitutes the entire agreement between the parties. Any modifications must be in writing and signed.

IN WITNESS WHEREOF, the parties hereto have executed this Loan Agreement as of the date first above written.

Borrower Signature: _____________________________ Date: _______________

Lender Signature: _____________________________ Date: _______________

| Fact Name | Description |

|---|---|

| Governing Law | The Florida Loan Agreement is governed by the laws of the State of Florida. |

| Document Purpose | This form is used to outline the terms and conditions of a loan between a lender and borrower. |

| Parties Involved | Typically, the agreement involves a borrower (individual or business) and a lender (individual or institutional). |

| Loan Amount | The specified amount of money being borrowed is clearly stated in the document. |

| Interest Rate | The agreement defines the interest rate applicable to the loan, which can be fixed or variable. |

| Repayment Terms | Specific repayment terms, including the frequency of payments and duration of the loan, are detailed. |

| Default Clause | If the borrower fails to make payments, the agreement outlines the actions that the lender may take. |

| Governing Language | The form is drafted in clear and straightforward language to avoid ambiguity. |

| Amendment Process | It specifies how the agreement can be amended or modified after signing. |

| Signature Requirements | Both parties typically need to sign and date the agreement for it to be legally binding. |

Completing the Florida Loan Agreement form is an important step in securing a loan. To ensure accuracy, it is essential to follow each step carefully. This process will guide you in providing the necessary information clearly and efficiently.

After completing the form, double-check all entries for accuracy. Make sure to keep a copy for your records before submitting it. Following these steps will help facilitate the loan process smoothly.

The Florida Loan Agreement form is a legal document outlining the terms and conditions under which one party lends money to another. This form specifies the loan amount, interest rate, repayment schedule, and any collateral involved. It ensures that both the lender and borrower have a clear understanding of their obligations.

Any individual or entity wishing to lend or borrow money in Florida can utilize this form. This includes personal loans between friends or family, as well as loans between businesses. Regardless of the situation, having a formal agreement helps protect the interests of both parties.

While a verbal agreement may suffice in some cases, written agreements provide stronger legal protection. The Florida Loan Agreement should include essential details such as the names of both parties, the loan amount, repayment terms, and signatures. No specific registration or filing is required, but having it notarized can add an extra layer of credibility.

By including these elements, you ensure that all parties are on the same page and minimize potential disputes.

Modifying a loan agreement is possible, but both parties must agree to any changes. It’s best to document any modifications in writing. Having a signed amendment or addendum reduces the risk of misunderstandings. If significant changes are needed, consider consulting with a legal professional for guidance.

Filling out a loan agreement form can seem straightforward, but mistakes often occur. One common error is not providing accurate personal information. Borrowers may forget to include important details like their social security number or the correct address. Missing or incorrect information can lead to delays in processing or even the rejection of a loan application.

Another frequent error involves the financial details. Borrowers sometimes misstate their income or debt obligations. This can create a misleading picture of their financial situation. Lenders rely on these figures to assess risk, so accuracy is crucial.

Alongside financial inaccuracies, borrowers often neglect to review the terms of the loan agreement closely. Key provisions related to interest rates, repayment schedules, and penalties should not be overlooked. Skimming through these sections without understanding them can lead to unexpected financial burdens down the road.

Some individuals fail to include necessary documentation. Documentation may include proof of income, tax returns, or identification. Not providing these items on time can slow down the application process, or worse, result in a denial.

Incorrectly calculating the loan amount requested also happens. Borrowers may either ask for too much or too little. An excessive loan request may be perceived as risky, while an insufficient amount may leave the borrower short in their financial planning.

Lastly, one of the most significant mistakes is not asking questions. If anything is unclear, failing to seek clarification can lead to misunderstandings. Open communication with the lender can pave the way for a smoother borrowing experience.

When entering into a loan agreement in Florida, various forms and documents often accompany the primary Loan Agreement. Each of these documents serves a specific purpose and helps establish a clear understanding between the parties involved. Below is a list of common forms you may encounter alongside a Florida Loan Agreement.

Each of these documents plays a vital role in the borrowing process and helps protect the rights and obligations of all parties involved. Understanding these forms will provide clarity and confidence in your financial arrangements.

When filling out the Florida Loan Agreement form, it is important to follow certain guidelines to ensure accuracy and compliance. Here are six things to consider:

Understanding the Florida Loan Agreement form is crucial for both lenders and borrowers. Nevertheless, several misconceptions can lead to confusion and mishaps. Here are six common misconceptions:

Recognizing these misconceptions can help individuals navigate the process of securing a loan or lending money with greater confidence and clarity.

Understand the purpose of the Loan Agreement form. This document outlines the terms and conditions under which one party lends money to another.

Accurate information is crucial. Fill in the names, addresses, and contact details of both the lender and the borrower without errors to avoid confusion later.

Clearly define the loan amount. Specify the exact dollar amount being lent, as well as any applicable interest rates, to ensure transparency.

Be aware of repayment terms. Detail when and how the borrower must repay the loan, including due dates and payment methods, to prevent misunderstandings.

Include any collateral. If the loan is secured by assets, describe them clearly to establish ownership and rights in case of default.

Ensure both parties sign the agreement. A signature from both the lender and the borrower validates the contract, making it legally enforceable.

Free Promissory Note Template Georgia - Amortization schedules may be part of the repayment plan.

Promissory Note Template New York - This agreement assists in preventing misunderstandings about the loan.